HI Market View Commentary 12-04-2023

HI Toll Free 888-287-1030

Let’s look at the core holding tonight

You have to do your own due diligence !!!

DIS – Owns its own county = people within the county pay taxes but DIS provides waste management services, police services, fire departments, etc….

Federalist – Kyle Griswold Dec 4, 2023 about the Disney RCID Scam

2 Reasons – Cheaper taxes and infrastructure costs, Lawsuits = Universal Studios,

Winner is ONLY DeSantis because he looked tough

You don’t have to like the company to make money on it !!!

What is the most WOKE company out there ?? Richest ?? AAPL

Trust the system and if all hell breaks loose (2008) we know how to have a profitable year = Double up on puts

Election years 8.5% Yrly return, Bonds 7.5% yrly returns

https://www.briefing.com/the-big-picture

The Big Picture

Last Updated: 17-Nov-23 15:03 ET | Archive

A value hiding in plain sight

What a difference three weeks makes. In late October, the 10-yr note yield was pushing 5.00%, the S&P 500 was on the brink of breaking below 4,100, and the CBOE Volatility Index was north of 20.00.

As we write, the 10-yr note yield sits at 4.45%, the S&P 500 is at 4,500, and the CBOE Volatility Index is under 14.00.

It has been quite a reversal in all respects, so here we are. Holiday spirit is in the air, and, dare we say, maybe even some animal spirits as the term “seasonality” gets tossed around in a positive way like a football on Thanksgiving Day.

The implication is that investor sentiment has taken a marked turn for the better in the past three weeks, largely because interest rates have come down on the assumption that the Fed is done raising rates and is apt to cut rates in the first half of 2024.

Higher stock prices are the manifestation of the improved sentiment, but accompanying those higher stock prices are higher valuations. Three weeks ago, the S&P 500 was trading at a 17.1x forward 12-month earnings, or a slight discount to its 10-year historical average (17.5x), according to FactSet. Today, it trades at 18.7x forward 12-month earnings.

Raising the Valuation Bar

The S&P 500 doesn’t trade at a super-rich valuation, but it’s up there. Just about everyone regularly following the market this year knows why.

- Apple (AAPL) trades at 29.0x forward 12-month earnings (5-yr average is 23.7x)

- Microsoft (MSFT) trades at 33.2x forward 12-month earnings (5-yr average is 28.1x)

- Alphabet (GOOG) trades at 21.5x forward 12-month earnings (5-yr average is 23.5x)

- Amazon.com (AMZN) trades at 43.8x forward 12-month earnings (5-yr average is 63.6x)

- NVIDIA (NVDA) trades at 32.1x forward 12-month earnings (5-yr average is 39.4x)

- Tesla (TSLA) trades at 66.4x forward 12-month earnings (5-yr average is 95.9x)

- Meta Platforms (META) trades at 19.4x forward 12-month earnings (5-yr average is 21.0x)

Source: FactSet

These seven companies in the market-cap weighted S&P 500 have raised the valuation bar. To be fair, that isn’t anything new. They have typically sported premium valuations, but it may surprise some to learn that only Apple and Microsoft are trading at a premium to their five-year average. That doesn’t necessarily make the others “cheap” per se, but there is not as much to the premium valuation as meets the eye at first blush.

If anything, there is concentration risk in these seven names. Investors have flocked to them because they are market leaders with healthy financials. They have flocked to them, because, for the most part, they keep delivering results that validate their must-own status. Fund managers have flocked to them, because everybody else has, and the risk of underperforming “the market” is too great not to own them.

Of course, therein lies the risk for these stocks and “the market.” If their fundamental story changes for the worse, their stock prices will, too, and perhaps in a material way, as Meta Platforms (META) discovered before it got back on fundamental track.

Where there isn’t any concentration risk is in the rest of the market.

Some Q&A

We’ve covered this point before, but it’s worth covering again after the move the market has made in the past three weeks. The market-cap weighted S&P 500 is being driven by a handful of stocks. The S&P 500 Equal-Weighted Index is being driven equally by 500 stocks.

Whereas the market-cap-weighted S&P 500 has looked more like Lightning McQueen this year, the equal-weighted S&P 500 has resembled his best friend, and tow truck, Mater. Granted it hasn’t had the same happy, go-lucky disposition that Mater does, but it has had Mater’s clunky style.

Three weeks ago, it was down 5.5% for the year. As we write, the S&P 500 Equal-Weighted Index is up 2.7% for the year. That won’t win it many plaudits knowing the returns on money-market funds, certificates of deposit, and T-bills are higher, but at least it is something.

It is also something to see that the equal-weighted S&P 500 is trading at just 14.9x forward twelve-month earnings. That is a 9% discount to its 10-year average of 16.4x. That isn’t a super-cheap valuation, but it’s down there.

Why flock to the narrowly concentrated, market-cap weighted S&P 500, which is trading at a premium valuation, when there is ample value to be found in the widely distributed, equal-weighted S&P 500, which is trading at a discounted valuation.

That is the question which begs another question: why aren’t investors taking advantage of this value opportunity?

Here are some possible answers:

- If it ain’t broke, don’t fix it. The mega-cap trade has continued to deliver the goods for investors, so it is hard to walk away from it when it is still working.

- It makes no difference to an investor in a market-cap weighted index fund how the return was achieved. It all counts the same when you need to cash out.

- There isn’t faith in the value proposition — not yet anyway.

What It All Means

That last answer might be the one that matters most both in terms of its meaning and its opportunity.

It means investors think forward earnings estimates are too high, so what looks like a value today isn’t the value it appears to be at first blush if there is going to be a material downward revision to earnings estimates. Accordingly, investors default to the mega-cap stocks, which they expect to be more dependable in a more challenging earnings environment. An economy in recession would be considered a challenging earnings environment.

The opportunity, of course, is in forward earnings estimates holding up because the economy is holding up. That brings us back to interest rates. They have come down sharply in recent weeks for a variety of reasons, but one of the primary drivers is the belief that the Fed is done raising rates because a softening economy will lead to softening inflation.

The extrapolation ends at a softening economy.

There doesn’t seem to be any allowance at the moment for anything other than a soft landing. Interest rates would presumably be chased lower in the event of a hard landing, but the offset in that situation is that earnings estimates would be chased lower, too, which wouldn’t be good for stock prices.

There is a lot riding on the economic outlook. We would argue that the vast outperformance of the market-cap weighted S&P 500 dominated by the mega-cap stocks versus the equal-weighted S&P 500 is not a reflection of the confidence in the outlook so much as it is a reflection of the uncertainty surrounding the outlook.

If the investment community was more certain of the favorable economic view, it would show greater interest in the value-based opportunity that appears to be available in the equal-weighted S&P 500. That opportunity seems to be hiding in plain sight for some opaque reasons.

If the economic future clears in the manner the market is inclined to think it will, the opportunity seen today in the equal-weighted S&P 500 will be worth the, uh, “weight.”

—Patrick J. O’Hare, Briefing.com

(Editor’s Note: The next installment of The Big Picture will be posted the week of December 4)

Earnings dates:

COST – 12/14 est

MU- 12/21 est

Where will our markets end this week?

Higher

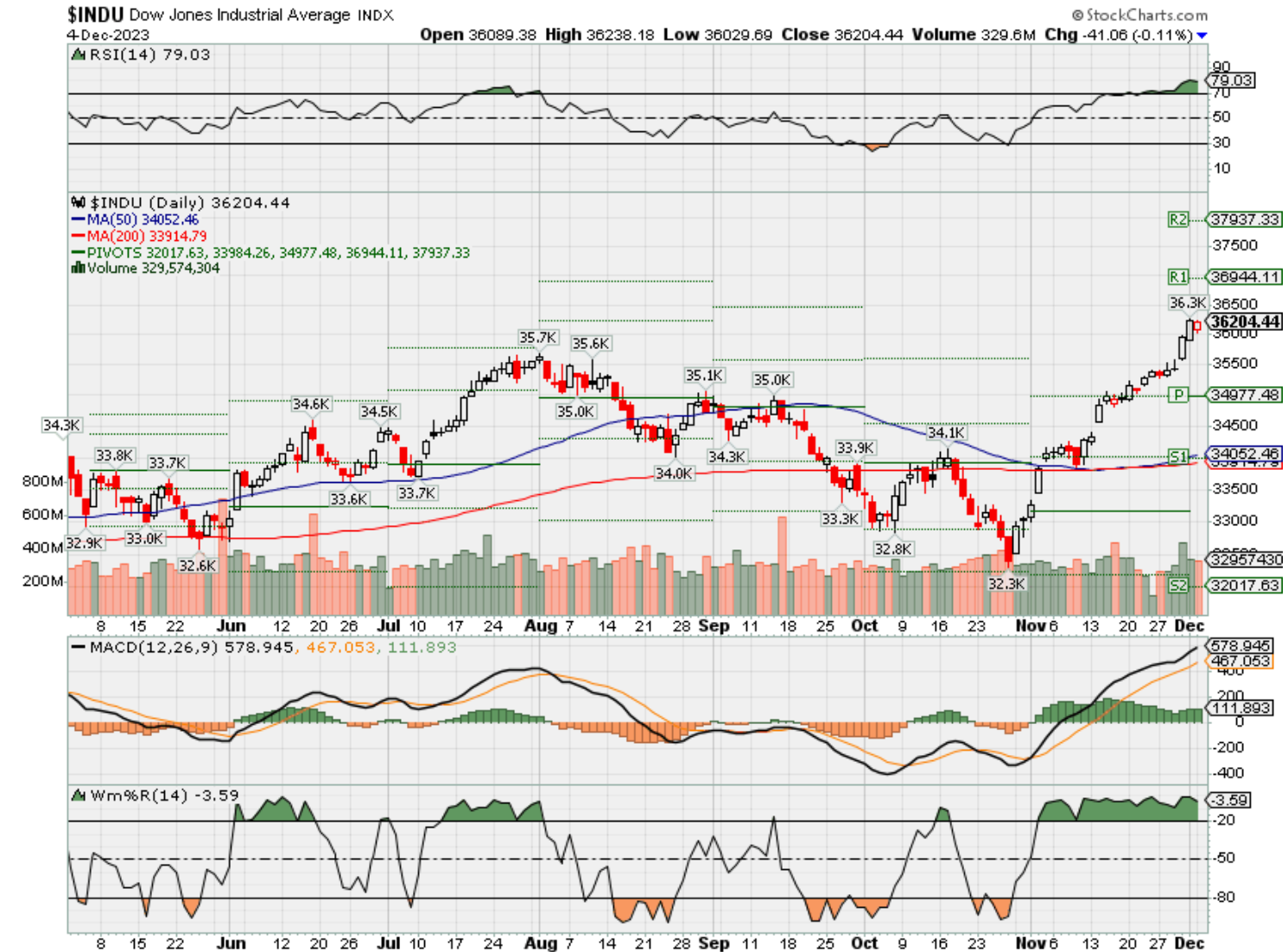

DJIA – Bullish Overbought

SPX –Bullish overbought

COMP – Bullish Overbought

Where Will the SPX end Dec. 2023?

12-04-2023 +2.5%

11-27-2023 +2.5%

Earnings:

Mon:

Tues: PLAY, TOL

Wed: KFY,

Thur: DG, AVGO, DOCU, LULU, SWBI, MTN

Fri:

Econ Reports:

Mon: Factory Orders,

Tue JOLTS,

Wed: MBA, ADP Employment, Productivity, Trade Balance, Unit Labor Costs

Thur: Initial Claims, Continuing Claims, Wholesale Inventory, Consumer Credit,

Fri: Average Workweek, Non-Farm Payroll, Private Payroll, Hourly Earnings, Unemployment Rate, Michigan Sentiment

How am I looking to trade?

www.myhurleyinvestment.com = Blogsite

info@hurleyinvestments.com = Email

Questions???

These regional banks are at greatest risk of being taken over by rivals, according to KBW

PUBLISHED MON, NOV 27 202311:23 AM ESTUPDATED MON, NOV 27 20232:43 PM EST

KEY POINTS

- Comerica, Zions and First Horizon might ultimately be acquired by more profitable competitors, according to KBW.

- Larger banks with strong returns including Huntington, Fifth Third, M&T and Regions Financial are positioned to grow through taking over smaller lenders.

- Two other lenders, Western Alliance and Webster Financial, could also consider selling themselves, KBW analysts said.

A trio of regional banks faces increasing pressure on returns and profitability that makes them potential targets for acquisition by a larger rival, according to KBW analysts.

Banks with between $80 billion and $120 billion in assets are in a tough spot, says Christopher McGratty of KBW. That’s because this group has the lowest structural returns among banks with at least $10 billion in assets, putting them in the position of needing to grow larger to help pay for coming regulations — or struggling for years.

Of eight banks in that zone, Comerica, Zions and First Horizon might ultimately be acquired by more profitable competitors, McGratty said in a Nov. 19 research note.

Zions and First Horizon declined comment. Comerica didn’t immediately have a response to this article.

While two others in the cohort, Western Alliance and Webster Financial, have “earned the right to remain independent” with above-peer returns, they could also consider selling themselves, the analyst said.

The remaining lenders, including East West Bank, Popular Bank and New York Community Bank each have higher returns and could end up as acquirers rather than targets. KBW estimated banks’ long-term returns including the impact of coming regulations.

“Our analysis leads us to these conclusions,” McGratty said in an interview last week. “Not every bank is as profitable as others and there are scale demands you have to keep in mind.”

Banking regulators have proposed a sweeping set of changes after higher interest rates and deposit runs triggered the collapse of three midsized banks this year. The moves broadly take measures that applied to the biggest global banks down to the level of institutions with at least $100 billion in assets, increasing their compliance and funding costs.

While shares of regional banks have dropped 21% this year, per the KBW Regional Banking Index, they have climbed in recent weeks as concerns around inflation have abated. The sector is still weighed down by concerns over the impact of new rules and the risk of a recession on loan losses, particularly in commercial real estate.

Given the new rules, banks will eventually cluster in three groups to optimize their profitability, according to the KBW analysis: above $120 billion in assets, $50 billion to $80 billion in assets and $20 billion to $50 billion in assets. Banks smaller than $10 billion in assets have advantages tied to debit card revenue, meaning that smaller institutions should grow to at least $20 billion in assets to offset their loss.

The problem for banks with $80 billion to $90 billion in assets like Zions and Comerica is that the market assumes they will soon face the burdens of being $100 billion-asset banks, compressing their valuations, McGratty said.

On the other hand, larger banks with strong returns including Huntington, Fifth Third, M&T and Regions Financial are positioned to grow through acquiring smaller lenders, McGratty said.

While others were more bullish, KBW analysts downgraded the U.S. banking industry in late 2022, months before the regional banking crisis. KBW is also known for helping determine the composition of indexes that track the banking industry.

Banks are waiting for clarity on regulations and interest rates before they will pursue deals, but consolidation has been a consistent theme for the industry, McGratty said.

“We’ve seen it throughout banking history; when there’s lines in the sand around certain sizes of assets, banks figure out the rules,” he said. “There’s still too many banks and they can be more successful if they build scale.”

Tech to rally in 2024 as AI leads biggest transformation since birth of the internet: Wedbush

Dec. 04, 2023 10:29 AM ETMeta Platforms, Inc. (META), GOOG, AAPL, MSFTAMZN, NVDA, PANW, CRWD, GOOGL, PLTR, ZS, MDB, NDX, DDOGBy: Christiana Sciaudone, SA News Editor41 Comments

Wedbush sees the tech sector ready to accelerate in 2024, even after rallying this year.

The bank expects artificial intelligence and cloud computing spending to boom next year as use cases spread.

“We view AI as the most transformative technology trend since the start of the Internet in 1995 and believe many on the Street are still underestimating the $1 trillion of AI spend set to happen over the next decade in a bonanza for the chip and software sectors looking forward with Nvidia and Redmond leading the way,” analysts led by Dan Ives wrote in a note.

“The tech sector is set up for an acceleration of spending around cloud and AI spending that we believe is still being significantly underestimated by the Street.”

The high expectations for the tech industry come as the NASDAQ 100-Index (NDX) is up 47% in 2023 so far. Nvidia (NVDA), expected to be a major beneficiary of artificial intelligence, is up 227% year-to-date after easily trouncing earnings expectations.

Microsoft (NASDAQ:MSFT), a major investor in OpenAI, which created ChatGPT, rose 56% in 2023 through today.

Ives and his team note that murky macroeconomic environment that remains and the shadow of the Federal Reserve’s high interest rates, as well as tech stocks having high valuations. Nonetheless, the bank is fully behind the industry.

“The fundamental picture for growth tech stocks is rock solid based on our recent checks in the field,” the bank said. “The new tech bull market has now begun and tech stocks are set up for a strong 2024 with tech stocks we expect to be up 20%+ over the next year led by Big Tech as the AI spending tidal wave hits the shores of the broader tech sector.”

The analysts cite Nvidia (NVDA), Microsoft (MSFT), Datadog (DDOG) and Palantir (PLTR) as having delivered robust results that give further confirmation that AI use cases are multiplying across the enterprise and consumer landscape.

“While IT budgets are expected to be up modestly in 2024, we believe cloud and AI driven spending will be up 20%-25% over the next year with use cases now exploding across the enterprise and consumer landscape.”

Wedbush’s favorite tech names include Apple (NASDAQ:AAPL), Microsoft (MSFT), Google (NASDAQ:GOOG) (GOOGL), Palo Alto Networks (PANW), Palantir (PLTR), Zscaler (ZS), Crowdstrike (CRWD) and MongoDB (MDB).

Cloud service divisions will be among the first to benefit from AI, including Amazon’s (AMZN) AWS and Alphabet’s (GOOG) (GOOGL) Google Cloud Platform. The two segments will acquire AI-capable chips, build AI-capable service offerings and sell those services into their respective installed bases.

GM initiates $10 billion buyback, boosts dividend and reinstates 2023 guidance after UAW strikes

PUBLISHED WED, NOV 29 20236:32 AM ESTUPDATED WED, NOV 29 20235:03 PM EST

KEY POINTS

- General Motors is working to regain Wall Street’s confidence heading into 2024 with several investor-focused initiatives Wednesday following a tumultuous year.

- The Detroit automaker is initiating a stock buyback, increasing its dividend and reinstating its full-year 2023 guidance.

- GM CEO Mary Barra in a statement said the company is finalizing a budget for next year that will “fully offset the incremental costs of our new labor agreements.”

General Motors is working to regain Wall Street’s confidence heading into 2024 with several investor-focused initiatives Wednesday following a tumultuous year of labor strikes and setbacks in its plans for electric and autonomous vehicles.

The Detroit automaker plans to increase its quarterly dividend next year by 33% to 12 cents per share; initiate an accelerated $10 billion share repurchase program; and reinstate its 2023 guidance to include an estimated $1.1 billion in earnings before interest and tax, or EBIT-adjusted, impact from roughly six weeks of U.S. labor strikes by the United Auto Workers union.

GM CEO Mary Barra in a statement said the company is finalizing a budget for next year that will “fully offset the incremental costs of our new labor agreements.

“The long-term plan we are executing includes reducing the capital intensity of the business, developing products even more efficiently, and further reducing our fixed and variable costs,” she said.

Shares of GM jumped 9.4% Wednesday. Heading into the announcement, the stock was down 14.1% so far this year.

Barra during an investor call Wednesday said the stock price “is disappointing to everyone.”

GM’s reinstated 2023 guidance also includes:

- Net income attributable to stockholders of $9.1 billion to $9.7 billion, compared with a previous outlook of $9.3 billion to $10.7 billion.

- Adjusted EBIT of $11.7 billion to $12.7 billion, compared with the previous outlook of $12 billion to $14 billion.

- Adjusted earnings per share of roughly $7.20 to $7.70 including the stock buyback, compared with the previous outlook of $7.15 to $8.15.

- EPS in the range of $6.52 to $7.02, including the stock buyback, compared with the previous outlook of $6.54 to $7.54.

- Adjusted automotive free cash flow of $10.5 billion to $11.5 billion, compared with the previous outlook of $7 billion to $9 billion.

- Net automotive cash provided by operating activities of $19.5 billion to $21 billion, compared with the previous outlook of $17.4 billion to $20.4 billion.

GM pulled its guidance when it reported its third-quarter earnings on Oct. 24, citing volatility caused by the UAW negotiations and labor strikes. The work stoppages ended Oct. 30 when the sides reached a tentative deal.

UAW impact

Before the UAW strikes, CFO Paul Jacobson said the company was on track to achieve “toward the upper half” of its earnings forecast.

On Wednesday the automaker said new labor deals in the U.S. and Canada are expected to increase costs by $9.3 billion and add approximately $575 in costs per vehicle. A majority of that impact is from the UAW deal, which expires in April 2028.

The UAW agreement includes at least 25% hourly pay raises, the reinstatement of cost-of-living adjustments and enhanced profit-sharing payments, among other benefits.

To offset some of those increased costs, GM said Wednesday it now anticipates 2023 capital spending to be between $11.0 billion and $11.5 billion, down from prior guidance of between $11 billion and $12 billion. That’s driven by previously announced plans to delay some new products and investments, specifically regarding EVs.

Barra in a letter to shareholders Wednesday said she was “disappointed” in the company’s production this year of its next-generation EVs, known as Ultium vehicles. She said the company expects “significantly higher Ultium EV production and significantly improved EV margins.”

“We’ve spent years preparing the company for an all-electric future, and our long-term EV profitability and margin goals are intact, despite recent headwinds,” Barra said.

GM has said it plans to earn low- to mid-single-digit EBIT-adjusted margins on its EV portfolio in 2025, before the positive impact of clean energy tax credits. It also has said it plans to exclusively offer electric vehicles by 2035.

Cruise

Barra also said the automaker is “addressing challenges” at Cruise, its majority-owned autonomous vehicle subsidiary.

GM is planning to spend “hundreds of millions of dollars” less on Cruise next year compared to 2023, CFO Jacobson said. The automaker has reported $1.9 billion in 2023 Cruise losses through the third quarter of the year.

Cruise recently issued a voluntary recall affecting 950 of its robotaxis and suspended all vehicle operations on public roads following a series of incidents that sparked criticism from first responders, labor activists and local elected officials, especially in San Francisco.

The events, specifically an October accident involving a pedestrian, led to co-founder and CEO Kyle Vogt resigning from the company.

“Our priority now is to focus the team on safety, transparency and accountability,” Barra said in the letter. “We must rebuild trust with regulators at the local, state and federal levels, as well as with the first responders and the communities in which Cruise will operate.”

Barra declined to further elaborate on GM’s plans for Cruise, pending ongoing independent investigations into the company. She reiterated that when Cruise does eventually relaunch, it will be in more focused, disciplined way.

“After we get the results of these two independent reviews, we will chart the course forward,” Barra said.

Cruise previously said its strategy is “to re-launch in one city and prove our performance there, before expanding.”

Stock buyback

The accelerated stock buyback includes an aggregate of $10 billion to the banks executing the program: Bank of America, Goldman Sachs, Barclays and Citibank.

GM will immediately receive and retire $6.8 billion worth of its common stock. The company had approximately 1.37 billion shares of common stock outstanding prior to the program.

Jacobson said the size of the buyback was determined after the company built up cash amid the uncertainty of its labor deals.

“I would say it’s stretched us a little bit, but we could do it comfortably and still maintain the liquidity and targets that are important to maintain the credit ratings that we have,” he said. “I think it was a really good mark.”

The total number of shares ultimately repurchased under the initiative will be determined at the end of the program, which is expected to occur during the fourth quarter. It will be based on the average of the daily volume-weighted prices of GM stock.

Outside of the announced program, GM said it will have $1.4 billion of capacity remaining under its share repurchase authorization “for additional, opportunistic share repurchases.”

The company said it has returned $4.2 billion in common stock dividends and buybacks from the start of 2022 through the third quarter of 2023, while generating more than $20.5 billion in adjusted automotive free cash flow after business investments.

“These strategies are designed to keep our margins and free cash flow strong, and we are well-positioned as we head into 2024,” Barra said at the end of her letter to shareholders. “I’m confident we’ll be able to execute our plan and excited about what the future holds. We look forward to sharing our progress with you.”