HI Market View Commentary 05-06-2019

What I want to talk about today?

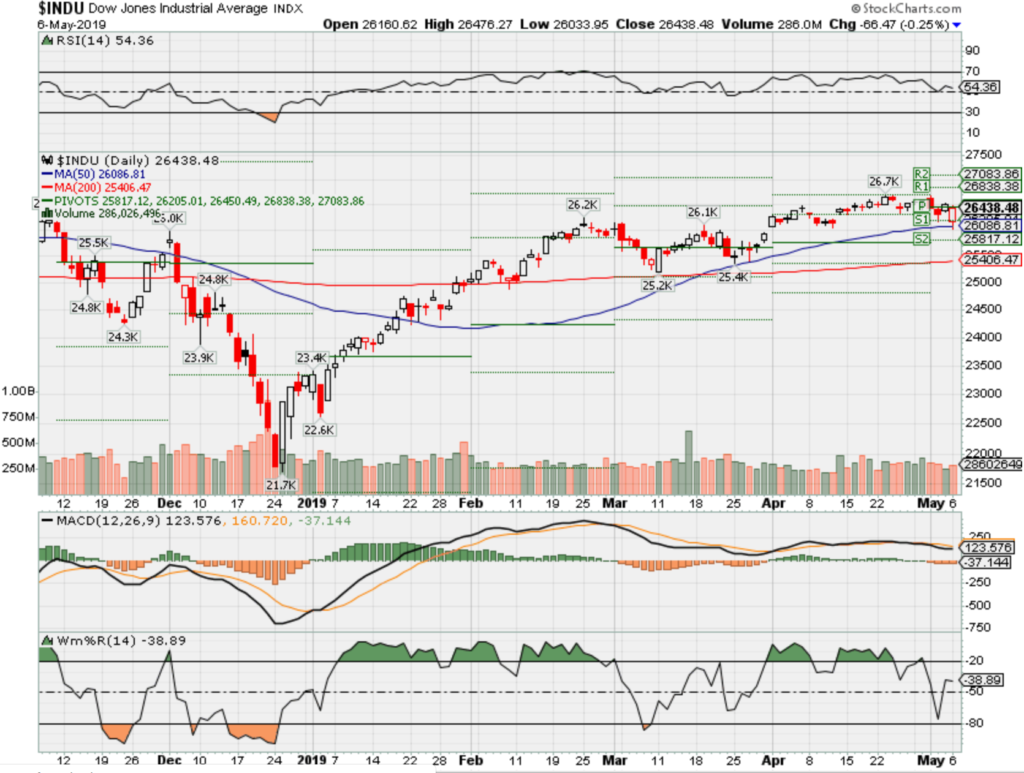

Sometimes the market catches you by surprise

News is going to tell you NO Trade deal!!!

How was I able to wait it out????

I usually like to wait for the first hour to go by so E minis clear out of the market

I still have some long puts in place from earnings

After the first hour support levels for some stock were holding

Problems are stock ownership with out protection and bull puts shorter term after a good earnings that have the shorts ITM or close to being ITM

Where will our markets end this week?

Higher

DJIA – Bullish

SPX – Bullish

COMP – Bullish

Where Will the SPX end May 2019?

05-06-2019 3.0%

04-29-2019 3.0%

Earnings:

Mon: TSN, TACO, MOS

Tues: AES, AGN, CROX, EMR, ADT, LYFT, PZZA, S, WYNN

Wed: BJ, HMC, MCK, VG, WEN, CTL, FOSL, KHC, DIS

Thur: CAH, DUK, DBX, GPRO, TIVO, ZG, YELP, VSLR

Fri: JD

Econ Reports:

Mon:

Tues: Jolts, Consumer Credit

Wed: MBA,

Thur: Initial, Continuing, PPI, Core PPI

Fri: CPI, Core CPI, Treasury Budget

Int’l:

Mon –

Tues –

Wed – CN: Trade Balance

Thursday – CN: CPI, PPI

Friday-

Sunday –

How am I looking to trade?

Going long for a China Deal and next Earnings which I expect to be better than expected Earnings

www.myhurleyinvestment.com = Blogsite

customerservice@hurleyinvestments.com = Email

Questions???

Here’s what Wall Street is saying about Trump’s tariff threat and what it means for investors

PUBLISHED MON, MAY 6 2019 7:08 AM EDTUPDATED MON, MAY 6 2019 1:47 PM EDT

Wall Street strategists urged calm after the latest threats from President Donald Trump after a series of tweets Sunday afternoon. Trump warned that tariffs on $200 billion worth of Chinese goods could rise to 25% on Friday and China was considering canceling this week’s trade talks with the U.S. in light of the threat.

The Dow Jones Industrial Average fell as much as 471 points, before rebounding and was last down about 280 points.

“We think it is more likely that the increase will be narrowly avoided and believe the odds of tariffs increasing on Friday are 40%, ” Goldman Sachs analysts said.

“Unless China walks away from the talks (which is not necessarily the same as Vice Premier Liu canceling his trip but rather having no talks at all), we do not expect an escalation of trade tensions into a trade war,” Citi said.

Some analysts differed as to whether Trump’s tweets were really a negotiating tactic.

“The timing of the threat suggests it is a tactic designed to increase leverage going into final trade negotiations,” UBS said.

But Raymond James wasn’t so sure.

“Based upon our conversations with our trade contacts, there appears to be a universal belief that this is not negotiating leverage, but what was almost a done deal last week, has derailed in recent days,” wrote analyst Ed Mills in a note to clients.

Here’s what strategists say about the U.S.-China tariff feud.

Goldman

“President Trump’s announcement that the tariff rate on $200bn of imports from China will rise from 10% to 25% lowers the odds of a successful conclusion to US-China trade talks and raises the odds of further tariff escalation. However, we think it is more likely that the increase will be narrowly avoided and believe the odds of tariffs increasing on Friday are 40%.”

Read more about that here.

Citi

“Unless China walks away from the talks (which is not necessarily the same as Vice Premier Liu He canceling his trip but rather having no talks at all), we do not expect an escalation of trade tensions into a trade war. Still, we note that the probability of a ‘Trade War today, Trade Deal tomorrow’ scenario remains high, with the potential to accelerate US inflation and to extend the timetable for a US-China trade deal into the 2020 electoral year. We are cautiously optimistic on a US-China trade deal in 2Q but with the tariffs-threat to remain as a way to get concessions from China and to enforce the agreement. ”

UBS

“There are no clear reports indicating what led President Trump to harden his stance on trade talks, with media reports suggesting it was designed to ‘send a message’ or was in response to China backtracking on previously negotiated points. The timing of the threat suggests it is a tactic designed to increase leverage going into final trade negotiations”.

Raymond James

“The progress towards a US-China deal has been up-ended with renewed tariff threats by President Trump (25% tariff on $200 billion in Chinese goods by Friday + 25% on $325 billion more), apparent balks by the Chinese (especially on tech transfers), and the threat of the Chinese delegation canceling this week’s round of negotiations. We have previously seen President Trump threaten a new tariff package in the lead up to last year’s G20 meeting last year, only to use it as negotiating leverage, leading to speculation that this is President Trump seeking to use the new tariff threats to get a deal across the finish line. Based upon our conversations with our trade contacts, there appears to be a universal belief that this is not negotiating leverage, but what was almost a done deal last week, has derailed in recent days. There is some hope that negotiations could be salvaged, but this situation highlights how tenuous any US-China deal remains.”

Oppenheimer

“With that in mind we would not take the President’s tweet as referring to an action planned that is set in stone but rather more an expression of frustration as talks have dragged on without reaching a resolution. We expect that any near-term downside moves by the equity markets could be quick to reverse as the US Presidential election of 2020 and a goal of ‘Made in China 2025’ remain paramount respective agenda items for the leadership of the US and China. In our view these key dates along with the potential considerable economic cost of a protracted trade war (for both countries as well as for their allies and trading partners) will dictate a positive resolution to the current trade dispute sooner than later notwithstanding a near-term ‘increase in hostilities.’ We suggest that investors consult their shopping lists for stocks that might have ‘gotten away’ from them in the recent rally should some ‘tweet-linked’ volatility waft through the markets and push stock prices lower.”

RBC

“Our thoughts on Sunday’s news that trade talks between the US and China have taken a turn for the worse. The news comes at a time when the US equity market has already become vulnerable to bad news again (and more at risk for a correction in the months ahead) due to excess euphoria among institutional investors and overvaluation. We see some eerie similarities between current conditions in the stock market and those that preceded the S&P 500′s peaks in January and September on our sentiment and valuation models. We also think a trade deal with China has been widely anticipated by investors, and a key contributor to the early 2019 rally in US equities. In this context, we see the weekend’s developments as a negative catalyst for the market, not only because of where investor expectations have been regarding the deal, but because of the downward earnings revisions that are likely to occur if the tariffs are expanded. In terms of positioning, we see some evidence that a profit-taking mind- set was already taking hold before this weekend’s news. We view these steps backwards on the trade deal with China as particularly negative for Industrials (where we’ve been market weight) and Semis/ Semi Equipment (which we’ve had a neutral stance on), which have both outperformed strongly this year due partly to improved outlooks on trade. TIMT (which has strongly outperformed in 2019) may also be at risk broadly given the sharp decline in the Nasdaq futures that was in place early Monday morning. On the flip side, we are buyers of defensives today, specifically Consumer Staples (which we’ve been overweight) and Utilities (we have been market weight, but valuations have recently improved and political risks from both trade and the 2020 election are low).”

Morgan Stanley

“It could be a pressure tactic to speed an agreement on pending issues such as existing tariff removal timing, details related to the enforcement mechanism and industrial subsidies. While we expect a re-escalation would be temporary, as market weakness would help bring both sides back together, any escalation inherently augments uncertainty and further undercuts risk markets, where a Goldilocks outcome was already priced in.”

Bank of America

“The immediate market response suggests that the latest escalation of the trade war was a complete surprise to investors. This means that markets could be in for a bumpy ride before a trade deal is reached.”

J.P. Morgan

“We think President Trump’s comment on China’s ‘attempt to renegotiate’ may reflect his likely frustration with the progress on some structural issues (as China may have resisted on US demands in some key areas); alternatively, China may have pushed hard for the US to roll back on the existing tariffs. As such, the near-term outlook on the trade negotiations has become somewhat unclear, and the next few days would be crucial to watch… Looking back, US-China trade negotiations have been a rather bumpy process. Indeed, back in May last year, shortly after both governments issued a joint statement to avoid an imminent trade war on May 19th, the Trump government indicated on May 29th plans to impose 25% tariff on $50 billion of Chinese imports and curb investment in sensitive technology sectors. Overall, the next couple of days will be crucial to watch. While the escalation of rhetoric and tariff threats by President Trump could be seen as part of the negotiation techniques to pressure China for further concessions, the timeline seems short, with the next stage of tariff hike to take place on Friday May 10th, according to President Trump’s tweet messages.”

Macquarie

“While we’ve been

complacent about the positive prospect for a trade deal (it has been one basis

for our view

that the EUR/USD, GBP/USD, and AUD/USD will slowly rally in H2 2019), we can’t

presume to have special insights into how the current impasse will resolve

itself in the next few weeks. As for the next few days, we suspect that

President Trump has put himself in a corner with the Friday deadline, so the

risk now is that the escalation of the tariff rate from 10% to 25% will take

place on Friday. From that point, if China President Xi Jinping chooses to not

make concessions to the US, it will be difficult to overturn his decision, and

a stalemate may ensue with traders waiting for the 25% tariffs on the final

tranche (USD 325bn) of US imports to be imposed. From then on, it may be the

action in the stock market that determined whether one side (presumably, the US) relents. After all, it would be detrimental to President Trump’s perception of self-value and re-election prospects is stocks are suffering in 2

Economics

America’s Big Deficits Are Solving a Big Problem for Markets

By Katia Dmitrieva and Liz McCormick

April 24, 2019, 4:00 AM MDT

America’s budget deficits are often described by economists as a problem. In the markets right now, they look more like a solution.

Even investors who worry about President Donald Trump’s loose fiscal policy are finding other things that worry them more. From China’s credit bulge to the European slowdown, warning signs are flashing globally. At home, the economy’s expansion is about to set records for longevity –- a reminder that it won’t last forever.

When that kind of foreboding takes hold, it translates into demand for safe assets. And Trump is supplying them — at a pace of about $1 trillion a year, matching the projected shortfalls in the U.S. budget.

Into the Red

Actual and projected U.S. budget deficits

Source: U.S. Treasury, Congressional Budget Office

“When people are afraid of something bad happening around the world, they typically go for buying Treasuries,’’ said Thomas Wacker, head of credit in the chief investment office at UBS Global Wealth Management, which oversees about $2 trillion. Right now, “there are so many things cooking everywhere,’’ he said. As a result, “there’s a constant flow into dollar debt.’’

‘…Or Is It?’

The appetite is sharpened by the fact that U.S. government bonds — unlike many of those issued by other stable, developed countries –- actually offer a positive yield. It’s a meager one by historical standards, but at least it doesn’t start with a minus sign. Trillions of dollars of debt in Europe and Japan has negative yields.

Better Than Nothing

Average yield on 2-year government bond since start of 2019

Source: Bloomberg

Then there’s the extra scrutiny that comes when investors sense trouble ahead, and start asking: What’s truly safe, and what’s just mispriced? After all, much of the private, asset-backed debt that crashed the U.S. financial system and then the world economy a decade ago received top marks from the safety inspectors at credit-rating companies.

“People did think last time, before the crisis, that they had bought safe assets,’’ said Andrew Milligan, head of global strategy at Aberdeen Standard Investments. “Then they realized those assets were less safe than they thought.’’

Milligan thinks the same kind of doubts may start to creep in again, and gives an example. “Italian bonds today, how safe do you regard them? It’s a G-7 country, has almost the same yield as the U.S.,’’ he said. “It’s a safe home, surely… or is it?’’

In Lockstep Now…

…but they weren’t always

Source: Bloomberg

Sovereign Pile

One reason to think Treasuries are safer is that they’re backed by a government that controls its currency and so can always meet liabilities denominated in dollars. That’s not the case for Italy, which is a user of the single European currency rather than an issuer of its own.

The distinction was vividly illustrated during the euro crisis early this decade. Yields on Italian bonds spiked above 7 percent, amid concern that the country could follow fellow euro-member Greece into default. They only subsided after the European Central Bank improvised a backstop.

Economists, meanwhile, were puzzling over the contrast with Japan, which appeared to suffer from the same fundamental problems as Italy: slow growth, high debt, stagnant demographics. Yet with its own currency and central bank, it had no trouble financing deficits at low interest rates.

Over the past decade, this has proved true for the U.S., too -– and for other currency-issuing governments in the developed world, like the U.K., even as their growing national debts cause alarm among fiscal hawks.

Who’s Borrowing?

Percentage change in debt as share of GDP under low-rates regime

Source: IMF, Bank for International Settlements

Note: Chart measures change since end-1998 in Japan, end-2008 for others. Business = non-financial corporations

‘Peculiar Phenomenon’

Some analysts see it differently, pointing out that investor demand for safe assets drove a lot of the financial innovation that blew up in 2008. In other words, if there’d been more government debt back then, there would have been less need for exotic and unstable securities engineered to look like they were just as solid as Treasuries.

“It’s an argument a lot of people made for why the financial crisis was so severe, and the recovery after was so slow — because there was a lack of safe assets,’’ said J.W. Mason, a fellow at the Roosevelt Institute in New York who focuses on the history and politics of American debt. “When the government spends money and borrows money, it’s creating safe assets. That’s the thing that’s being missed.’’

There are long-term reasons why investors want more of those assets — aging populations that need more retirement savings, for example. Add in the short-run jitters about another recession or market slump, and the effect has so far been strong enough to confound a widespread belief that when deficits widen and more bonds go on sale, yields must rise.

“As and when the U.S. Treasury market explodes due to more issuance, you’ll be seeing a lot of investors simply dashing for safety and buying that debt,’’ said Milligan at Aberdeen Standard.

“Supply often creates its own demand in the bond market,’’ he said. “It’s a peculiar phenomenon.”

Ford’s rebound is just getting started — here’s why it’s the only auto Cramer endorses

PUBLISHED 4 HOURS AGOUPDATED 3 HOURS AGO

Tyler Clifford@_TYLERTHETYLER_

He gave a stamp of approval to CEO Jim Hackett, who has helmed the company for nearly two years.

MAY 6, 2019 / 2:28 PM / UPDATED 7 HOURS AGO

Factbox: Winners and losers in Trump’s trade war with China

(Reuters) – U.S. companies in everything from computer chips to tractors have said President Donald Trump’s trade wars, including disputes with Beijing and global steel tariffs, have had an impact on them.Even for some of the expected winners, such as steel companies, the benefits of the president’s tariffs are not entirely clear.

Trump said on Sunday he will raise tariffs on $200 billion worth of Chinese goods from 10 percent to 25 percent, ratcheting up pressure on Beijing to agree to a deal.

TECHNOLOGY

Apple Inc

Apple Inc cut its fiscal first quarter sales forecast, blaming slowing iPhone sales in China where uncertainty around U.S.-China trade relations has hurt the economy.

Late last month after Apple slashed prices, sales picked up and Apple cited the improved tone of the trade war for a stronger outlook.

Intel Corp

The chipmaker last month cut its revenue forecast for 2019, citing a slowdown in demand from China.

VEHICLES

Fiat Chrysler Automobiles NV forecast higher commodities costs, driven by tariffs, would cost 750 million euros for the year.

General Motors Co projected $1 billion extra costs this year for tariffs and raw materials. Steel and aluminum prices have eased, but prices for other commodities such as palladium have risen, it said.

Ford Motor Co Ford said that in 2018 it incurred “headwinds” of about $750 million in tariff-related effects. Lower sales volume and increased commodity costs including tariff-related effects added $500 million to first-quarter costs over the prior year.

Harley-Davidson

The motorcycle manufacturer said European Union and China tariff-related costs were $23.7 million in 2018 and are expected to range between $100 million and $120 million in 2019.

HEAVY EQUIPMENT

Caterpillar Inc

Caterpillar said tariffs would cost the company $250 million to $350 million in 2019 if there was no relief.

Deere & Co

The manufacturer said in February it expects U.S. tariffs on Chinese imports will cost $100 million in 2019.

AGRICULTURE

Archer Daniels Midland Co

The commodities trader’s adjusted operating profit slumped 30 percent in the fourth quarter to $183 million as the China trade war hit its sorghum and soybean origination business.

Bunge Ltd The company reported a $125 million mark-to-market loss in August on a position in soybeans that bet a China trade war would be averted. Bunge’s profits then plunged in the fourth quarter as a temporary truce with China caused soybean prices to fall and slashed the value of its Brazilian soybean inventory by $125 million.

Cargill Inc

Commodities trader Cargill said in March that U.S.-China trade tensions and other supply chain disruptions continued to drag on earnings in origination and processing, the company’s primary grain-trading unit.

STEEL

Nucor Corp

No.1 U.S. steel producer Nucor Corp posted record earnings and shipped a record amount of steel in 2018, benefiting from the tariffs.

But the company last month forecast first-quarter profit below Wall Street estimates, citing lower average selling prices of steel sheets and delay in shipments to customers in the construction sector.

The tariffs imposed by the Trump administration on steel imports, mainly from China, have increased domestic production, leading to a drop in steel prices.

JBS SA

Brazil’s JBS, the world’s largest meatpacker, has been able to boost meat exports to China as the tensions between the Washington and Beijing escalated. The company’s share of exports to China rose to more than 24 percent last year vs under 21 percent in 2016 and 2017.

Louis Dreyfus Company

The global agricultural commodity merchant said that trading opportunities created by the U.S.-Chinese trade dispute boosted its soybean business last year.

The company posted record soybean export volumes from Brazil , boosting profits 12 percent vs the previous year.

Reporting by Chris Prentice and Timothy Aeppel in New York, Ana Mano in Sao Paulo, Karl Plume and P.J. Huffstutter in Chicago, Ankit Ajmera and Arathy Nair in Bengaluru, Joe White in Detroit and Stephen Nellis in San Francisco; Editing by Cynthia Osterman

Our Standards:The Thomson Reuters Trust Principles.