HI Market View Commentary 03-04-2019

What I want to talk about today?

Crashes, Dips, Spikes and Recessions because I feel…….”toppy”

Next push higher wasn’t earnings and must be a China Deal which is a couple of months away

We did have a 20% drop in the S&P500 but it wasn’t a normal bear market correction

As I talked about the Trade Findings and Adjustments last week ITM = In the Money

If I was a trader I would want a nice cushion on my trades = ITM

Where will our markets end this week?

Down

DJIA – Bullish

SPX – Bullish

COMP – Bullish

Where Will the SPX end March 2019?

03-04-2019 0.0%

02-25-2019 0.0%

Earnings:

Mon: CTRP, CRM

Tues: KSS, TGT, ROST, URBN, VSLR,

Wed: ANF, BJ, DLTR

Thur: BKS, BURL, KR, COST, MRVL

Fri: BIG, MTN

Econ Reports:

Mon: Construction Spending,

Tues: ISM Index, New Home Sales, Treasury Budget,

Wed: MBA, ADP Employment, Trade Balance, Factory Orders, Fed Beige Book,

Thur: Initial, Continuing, Productivity, Consumer Credit,

Fri: Avework, Non-Farm, Private, Hourly Earnings, Unemployment Rate, Housing Starts, Building Permits

Int’l:

Mon –

Tues –

Wed –

Thursday –

Friday- CN: CPI, PPI

Sunday –

How am I looking to trade?

I’m in just stock positions

Look at Long Puts on DIS closer to $115

AAPL closer to $178

UAA looking to protect closer to $25

F looking to protect closer to $9.25

MRVL – 3/17

RHT – 3/26

www.myhurleyinvestment.com = Blogsite

customerservice@hurleyinvestments.com = Email

Questions???

https://traderhq.com/illustrated-history-every-s-p-500-bear-market/

TRADING SECURITIES

Share

Illustrated History of Every S&P 500 Bear Market

Stoyan BojinovApr 05, 2014

Talk to any professional money manager and they will warn you that picking markettops and calling bottoms is very risky and should only be attempted by fortune-tellers. While this piece of advice is undeniably sound, investors shouldn’t completely give up on identifying major turning points in the stock market. In fact, looking back at history can offer some valuable insights as to how certain major benchmarks have behaved leading up to critical turning points.

As such, below we have profiled every bear market that the S&P 500 Index has endured since the 1950s, noting the fundamental catalyst, performance, and behavior of the benchmark in each instance. The tables below are based on returns from the market peak to the following low and include the dates of each turning point as well as the respective magnitude and length of each bear trend. Any investors looking for an ETFthat mimics this index should look at SPY or VOO.

The Crash of 1957

| Top | Bottom | Bear Return | Duration |

| Jul 15, 1957 | Oct 22, 1957 | -20.7% | 3 Months |

The U.S. government began to tighten monetary policy years prior to the recession in 1958, also known as the Eisenhower Recession, in an effort to curb inflation; however, prices continued to climb and the strengthening U.S. dollar led to a growing foreign trade deficit. Notice how the S&P 500 hit the same low point on three occasions before finally resuming its bull-run, giving patient investors several clues that new lower-lows would be highly unlikely as buyers began to step back in. The higher-lows seen from the start of 1958 confirmed the bottom.

See Also: 25

Stocks Day Traders Love

The Crash of 1962

The expansionary period that followed the recession in 1960-61, which was a result of high unemployment and a shift to foreign-made cars, was met with another sharp decline as the Fed began to tighten monetary policy. Keen investors kept their eye on the critical support level (red line), which was confirmed after a double-bottom prior to the start of 1963; a sharp rally with higher-lows confirmed the bear market was very likely over.

| Top | Bottom | Bear Return | Duration |

| Dec 12, 1961 | Jun 26, 1962 | -28.0% | 6 Months |

The Crash of 1966

| Top | Bottom | Bear Return | Duration |

| Feb 9, 1966 | Oct 7, 1966 | -22.2% | 8 Months |

Many economists recognize the credit crush of 1966 as the first significant post-war financial crisis. Amid economic expansion at home, the Federal Reserve proceeded to tighten monetary policy so much that it threatened the profitability of financial institutions. Policymakers had to intervene to save the municipal bond market after a credit crunch ensued and confidence was restored; the S&P 500 Index proceeded to post higher-lows prior to the start of 1967.

The Crash of 1969-70

| Top | Bottom | Bear Return | Duration |

| Nov 29, 1968 | May 26, 1970 | -36.1% | 18 Months |

Rising inflation, increased deficits from the Vietnam War, and monetary tightening sent markets tumbling at the start of 1969. The economic recession at the time put a further damper on investors’ confidence and the S&P 500 endured a nasty losing stretch lasting well over a year and half, shedding upwards of 35% in that time frame. The market formed a double-bottom in the first half of 1970 and proceeded to resume its bull run with higher-lows in the months following.

The Crash of 1973-74

| Top | Bottom | Bear Return | Duration |

| Jan 5, 1973 | Oct 3, 1974 | -48.4% | 21 Months |

The abandonment of the Bretton Woods system in 1971, which terminated the convertibility of the U.S. dollar to gold, sent financial markets around the globe into a tailspin, with the United Kingdom getting hit particularly hard. Adding to the turmoil, the OPEC oil embargo in 1973 sent crude prices higher, further hurting U.S. consumers who also battled with the devaluation of the U.S. dollar. The S&P 500 endured its worst and longest bear market to date and higher-lows in mid-1975 confirmed that the bottom was in.

The Crash of 1980-82

| Top | Bottom | Bear Return | Duration |

| Nov 28, 1980 | Aug 12, 1982 | -27.1% | 20 Months |

A second oil crisis followed in 1979 in the wake of the Iranian Revolution, sending crude prices higher and hurting consumer spending. Lingering inflation from the 1970s also prompted the Federal Reserve to raise rates dramatically, which sparked the second longest bear market to date. By the start of 1973, inflation had been tamed to 3.2% and the S&P 500 Index had snapped back higher, confirming the bottom with higher-lows.

See Also: 50 Blogs Every Serious Trader Should Read

The Crash of 1987

| Top | Bottom | Bear Return | Duration |

| Aug 25, 1987 | Dec 4, 1987 | -33.5% | 3 Months |

The Federal Reserve started raising rates in 1986 to combat inflation as equity markets had enjoyed a stellar run-up; tightened monetary policy at home was welcomed with a steep sell-off that became known as ‘Black Monday’ and led to stock market crashes around the globe, starting in Hong Kong and spreading to Europe. At the same time, Iran had fired on a U.S. oil-supertanker, which led to a conflict in the Persian Gulf that further deteriorated investors’ confidence in the markets. The S&P 500 endured its steepest three-month decline in history and proceeded to resume its bull run by the start of 1988.

The Dot-Com Bubble

| Top | Bottom | Bear Return | Duration |

| Mar 24, 2000 | Oct 9, 2002 | -49.1% | 31 Months |

The ‘90s were characterized by exceptional economic expansion, brought on largely by the rampant growth and adoption of the Internet, which forever changed the world of business and entertainment. However, speculation over technology companies peaked and then coupled with the September 11th terrorist attacks to bring the period of growth to an end. The economic recession that ensued was short-lived, however, as the dot-com bubble’s impact was fairly contained to Wall Street. The S&P 500 carved out a triple-bottom in the second half of 2002 and confirmed this with higher-lows into mid-2003.

The Housing Bubble

| Top | Bottom | Bear Return | Duration |

| Oct 9, 2007 | Mar 9, 2009 | -56.8% | 17 Months |

Speculative lending practices fueled a massive housing boom in the U.S. that inevitably led to the subprime mortgage crisis. The subsequent collapse in housing prices combined with rising oil and food costs to send the market crashing as investors pulled money out of Wall Street amid intensifying fears over the looming global financial meltdown. This remains the steepest bear market in the S&P 500’s history and contributed to what is regarded as the ‘Lost Decade’ in the U.S. stock market – the period spanning the dot-com and housing bubbles. The Federal Reserve rode to the rescue and bailed out a number of financial institutions, helping to restore confidence and bolstering equities sharply higher by mid-2009.

Be sure to sign up for our free newsletter for more infomation

The Bottom Line

Though history seldom repeats itself, looking back at the causes and impacts of every S&P bear market should help investors better understand how these events occur and how their portfolios are affected.

5G: Faster speeds, faster connections, faster access

By David Goldman Business, CNN | Posted – Feb 25th, 2019 @ 10:34am

NEW YORK (CNN) — 5G will be the lifeblood of the new economy.

Self-driving cars, virtual reality, smart cities and networked robots will all be powered by 5G networks. 5G promises to open the door to new surgical procedures, safer transportation and immersive video games.

Major telecommunications companies are far along in their 5G network development, and the first 5G networks are already up and running.

5G is primarily about three new things: Faster speeds, faster connections and faster access to the cloud.

Faster speeds

Like every “next generation” wireless network technology, 5G will give your phone a speedier connection — up to 100 times faster than 4G. That’s enough to stream “8K” video or download a 3D movie in 3 seconds. (On 4G, it would take six minutes.)

5G’s extra bandwidth will make service more reliable, allowing more gadgets to connect to the network at the same time.

But 5G is about much more than smartphones. Sensors, thermostats, cars, robots, and other new technology will all connect to 5G one day. Today’s 4G networks don’t have the bandwidth for the vast amounts of data all those devices will transmit.

Advertise with usReport this ad

To accomplish all that, much of the 5G network will travel over super-high-frequency airwaves. These higher frequencies bring faster speeds and more bandwidth. But they can’t travel through walls, windows or rooftops, and they get considerably weaker over long distances.

That means wireless companies will need to install thousands — perhaps millions — of miniature cell towers on top of lamp posts, on the side of buildings and inside homes.

That’s why 5G will initially complement 4G rather than outright replace it. In buildings and in crowded areas, 5G might provide a speed boost, but 4G will still be used to cover wider areas for the time being.

Faster connections

5G networks will also reduce to virtually zero the latency, or lag time, between devices and the servers they communicate with.

Today’s networks take a split second to send and receive communications between a device and the network. A split second isn’t much, but gadgets constantly communicate with the network when displaying huge files like virtual reality games or HD videos.

Zero latency can allow self-driving cars to process all the information they need to make life-or-death decisions in the blink of an eye. The health care industry believes 5G could help power the next generation of telemedicine and robotic surgeries. Those innovations will only be possible if the communication between a network and a device is seamless.

Faster access to the cloud

The 5G network can also act like a cloud server, performing much of the computing and storage that otherwise would have to be done by the self-driving cars themselves. That could potentially save the cars a lot of power and space.

Today’s data centers are in centralized locations. The farther the data center, the longer it takes to access that data. 5G networks bring data storage much closer to devices and help them quickly access information.

With 4G technology, self-driving cars and virtual reality need to store data on-site. Accessing data centers takes too long, creating a herky-jerky experience on VR and a potentially life-threating one in cars.

The-CNN-Wire™ & © 2018 Cable News Network, Inc., a Time Warner Company. All rights reserved.

Cramer: ‘Solid evidence’ shows that investors can make money in this market even without a China trade deal

- “If we can advance without a trade ceasefire, just imagine how high we could go if the White House and the Chinese Communist Party can reach some kind of accommodation?” Jim Cramer says.

- The “Mad Money” host says mergers and acquisitions, earnings, and the tech sector are showing they can continue to rally with or without a trade agreement.

- “Both of the cloud kings and the semis were able to advance again solidifying their status as market leaders. They’ve really powered this rally,” he says.

Tyler Clifford | @_TylerTheTyler_

Published 6:25 PM ET Mon, 25 Feb 2019 Updated 7:37 PM ET Mon, 25 Feb 2019CNBC.com

There are signs showing that investors can make more money on this market rebound even with a trade deal still pending between the two world’s largest economies, CNBC’s Jim Cramer said Monday.

In fact, there’s a chance that stocks can continue this rally even without an agreement between the United States and China, the “Mad Money” host said.

“If we can advance without a trade ceasefire, just imagine how high we could go if the White House and the Chinese Communist Party can reach some kind of accommodation?” he said. “Today, we got some solid evidence that there’s enough good happening away from China to justify sticking with this market in order to enjoy what Warren Buffett called the ‘tailwind of American greatness’ in his annual Berkshire-Hathaway letter that came out this weekend.”

Stocks are expected to spike whether or not a prospective trade deal drops tariffs currently in place. President Donald Trump said over the weekend that he will delay increasing tariffs on billions of dollars worth of Chinese imports originally scheduled to begin on March 1, citing progress in trade talks with Beijing.

Whether trade officials can deliver on a deal or not, Cramer ran through a number of reasons that stock traders can keep winning by way of mergers and acquisitions, future earnings and tech stocks.

On the M&A front, Cramer noted that a number of potential mergers could reveal that companies can sell for more than they are worth on the market. Barrick Gold, the host’s favorite gold miner, is making a hostile $17.8 billion bid for Newmont Mining. European drug giant Roche made a $4 billion deal— which Cramer pointed out is a 120 percent premium—for U.S.-based gene therapy specialist Spark Therapeutics. Additionally, Eli Lilly, GlaxoSmithKline, and Novartis have made multi-billion dollar moves in the biotech sector, he said.

Most notably, Cramer pointed out that shares of General Electric, which has had a list of troubles as of late, surged more than 6 percent Monday after health sciences conglomerate Danaher announced it would buy the company’s biopharma unit for $21.4 billion. Danaher gained more than 8 percent and reached a new 52-week high.

“Sure, there are still serious problems—the bedraggled power division, the expensive long-term care insurance policies that they’re on the hook for—but $21 billion goes a long way toward curing those woes,” said Cramer, who acknowledged that GE will hold on to its their health care division. “This deal tells me when you put China to the side, many companies may be worth a lot more than their stocks are currently selling for.”

When it comes to earnings, results this quarterly report season have not been the best but there have been some upside surprises that tend to have legs, the host said. Wayfair, which has yet to make profit, continued last week’s $32 rise off of a revenue beat by adding another $10 to its stock price Monday.

Cramer highlighted that child and baby apparel company Carter’sand heavy equipment maker Terex had some good action after reporting before he bell Monday: the stocks rose more than 8 percent and nearly 2 percent, respectively.

“By themselves I know they don’t mean much, but consider the implications: Carter’s can’t sell a lot of children’s sleepwear without department stores doing better. And Terex can’t sell a lot of heavy equipment without construction doing better.,” he said. “In that sense, you know what, those two represent some real good pin action.”

Cramer said the tech sector also got a boost Monday off of trade deal developments and praises from Buffett, who said that he would buy more Apple if the stock were to fall. He also pointed out that so-called FANG stocks are beginning to show life, but semiconductors and cloud companies have been leading the charge.

“The really good news? Both of the cloud kings and the semis were able to advance again solidifying their status as market leaders,” Cramer said. “They’ve really powered this rally.”

“The bottom line: We’ve got a heck of a lot of ways to win even without a trade deal, and if we get some kind of arrangement with the Chinese, I think we could have way more upside than most people expect or suspect,” he said.

The US can solve its trade problems while relaunching the world economy

- The next G-20 summit in late June is an opportunity to position the U.S. trade problem as a central issue in international economic policy coordination.

- Those are very technical questions that require meticulous preparation, with agreed solutions ready to be presented to conference participants.

- Leaving such questions for deliberations by heads of state and government would lead to failure.

Dr. Michael Ivanovitch | @msiglobal9

Published 4:46 AM ET Mon, 25 Feb 2019

Pursuing one of American core national interests, the U.S. administration lost a multilateral dimension of its forceful quest to balance trade accounts.

Washington’s unassailable trade case against China, the European Union, its North American neighbors and Japan is fundamentally an issue of world economy. Reducing that case to bilateral quarrels robs America of a powerful negotiating advantage, and of the high moral ground of a world leader.

Buying more than half-a-trillion dollars worth of goods and services more than it sells to the rest of the world, America is making a large net contribution to the rest of the world, and remains an indisputable locomotive of the global economy. Washington, therefore, has a very different role on the world stage than major trade surplus countries taking nearly a trillion dollars of purchasing power from their trading partners.

As a result, America is squarely at the helm of the crucial issues of international economic policy coordination — the key mission of G-20 summits, which serve as the world’s principal economic forum.

The G-20 meeting, scheduled for late June in Japan, could be an opportunity for the U.S. to begin reducing its trade deficits — large subtractions from its aggregate demand — by leading the way to an appropriate economic policy coordination on a global scale.

Insist on policy coordination

The time for such an initiative could not be better: The world economy is expected to slow down considerably, mainly as a result of the weakening aggregate demand in Europe and China, which represent nearly 40 percent of global demand and output.

Those two large trade surplus areas have been for years a drag on global growth. Their slowdown will now aggravate the downward pressure on the rest of the world because their businesses will be stepping up exports to escape the shrinking markets at home.

Perversely, in spite of that, those trade surplus areas are getting a free pass. By contrast, the U.S. is branded a culprit because it is trying to fight such beggar-thy-neighbor policies in a — so far — unsuccessful attempt to reduce its large trade deficits and put an end to its soaring net foreign debt.

Here are a few ideas on how the U.S. can rebalance its trade accounts by relaunching the global economic activity.

First, Washington should weave its strategy around the established principles of international trade adjustment that have guided efforts of global policy coordination ever since the first G-6 summit at Rambouillet, France, in November 1975.

Second, those principles are used to determine which countries should be expanding or contracting their aggregate demand as a result of their trade positions, fiscal stance, inflation and employment.

Europe and Asia can boost world economy

Usually, the trade surplus countries — which are producing more than they are consuming and exporting their excess production — are prime candidates for expansionary demand management policies. They also tend to run relatively sound budget accounts and low inflation. Conversely, trade deficit countries are forced to restrict their domestic demand for reasons of rising inflation and budget deficits.

For a balanced world economy, trade adjustments symmetrically apply to surplus and deficit countries. In practice, however, surplus countries have ignored those rules because they are under no market pressure to adjust their external accounts. The burden of adjustment is, therefore, entirely borne by deficit countries because they have to attract, if they can, foreign savings to fund their deficits. In most cases, they have to submit to stringent adjustment policies as part of conditional lending by the International Monetary Fund.

Third, on the basis of trade adjustment rules one can show, as an example, that the euro area, whose trade interests are represented by the European Union, is a prime candidate for expansionary demand management policies. The monetary union is currently running a trade surplus of more than $600 billion, it has nearly balanced public sector accounts and shows a headline inflation of 1.4 percent in January. At the same time, the euro area is struggling with a 7.9 percent jobless rate, 16.6 percent of its youth is unemployed, and a total of 12.9 million of its people are out of work.

A similar analysis for major Asian trade surplus economies like China, Japan and South Korea — accounting for one-fourth of the world output — would also show that their stronger domestic demand and greater openness to international flows of trade and finance could make a substantial contribution to a faster growing global economy.

Fourth, Washington should be aware that the European and Asian trade surplus countries are expecting to continue dumping their excess output on U.S. markets. Those are decade-old habits deeply ingrained into their economic policies. The White House has to clearly signal that those times are over. America’s trade accounts have to be balanced, the growth of its debts and deficits must be stopped and reversed — and the U.S. now expects that its main trade partners will do their share of supporting global economic growth.

Investment thoughts

The next G-20 meeting is an excellent opportunity for the U.S. to enhance its global economic and political leadership. It can do so with a strong demand for trade surplus countries to actively contribute to the growth of the world economy with expansionary monetary and fiscal policies and more open markets for global commerce and finance.

A U.S. advocacy for an effective international economic policy coordination would be at the core of the G-20 mission. Such an enlightened multilateralism would in no way prevent Washington to press its trade case on a bilateral basis whenever appropriate. In fact, that multilateral cover would invalidate the argument of America’s trade opponents that it is out to destroy the global system of free trade.

Can that work? Yes, it can, but it all depends on how well the U.S. prepares its participation at the next G-20 summit. Those are very technical questions that must be solved and ready for signature by conference participants. Leaving such questions for deliberations by heads of state and government would lead to failure.

The world expects the U.S. to lead. To do that, Washington must place its trade problem in a broader context of a balanced and growing world economy. If Washington does that, Europe and China would have to do their part of supporting the global economic activity, and they would have no chance of resisting America’s unassailable case for balancing its trade accounts.

Commentary by Michael Ivanovitch, an independent analyst focusing on world economy, geopolitics and investment strategy. He served as a senior economist at the OECD in Paris, international economist at the Federal Reserve Bank of New York, and taught economics at Columbia Business School.

https://seekingalpha.com/article/4244446-3-reasons-buy-hold-disney-stock

3 Reasons Why You Should Buy And Hold Disney Stock

Feb. 26, 2019 5:38 PM ET

Research analyst, tech, long-term horizon, value

Summary

Up until 2015, The Walt Disney Company’s stock has been in limbo trading between $90 and $120.

A big swing is likely to happen, and investors may be too cautious at this point.

Three reasons to buy and hold: Disney will likely own more or all of Hulu, it has widely underestimated content, and the stock is cheap right now.

Introduction

Up until 2015, The Walt Disney Company (DIS) had been a great investment. It more than quadrupled since 2010, but the stock has since been range-bound between $90 and $120 per share. In fact, it tested the $120 mark at least four times since 2015 and, compared to the major indexes, has underperformed.

Disney continues to launch blockbuster hits and even crushed estimates in its most recent quarter, but investors have been focused on the risks. Investors’ initial response to this month’s earnings was very positive; shares were up as much as 5% or near $118 per share in after-hours trading following the report. However, as Iger reminded investors during the conference call of Disney’s intention to go all-in with streaming, otherwise perceived as a costly and late venture, the stock ultimately erased its gains and closed negative the next day, falling below $111 per share.

As the story shifts to an adventure in a direct-to-consumer streaming model, an obvious upside or downside exists in the stock. Thus, even though Disney trades at a multiple well below the S&P 500 or its fellow Dow components, there is a strong argument against what’s supposed to be a blue chip stock. I think investors are a little too cautious, though. Here are three reasons why.

1. Disney’s 60% Stake In Hulu Likely Becomes 100%

Disney’s acquisition of Fox’s (NASDAQ:FOX) studio assets also came bundled with an additional 30% stake in Hulu. With that, Disney will own 60% of Hulu and the remaining 40% will be held by Comcast (CMCSA) and AT&T (T) (10%), which each has its own direct-to-consumer plans. With no control over the business and a conflict of interest with their own streaming efforts, it makes no sense for Comcast and AT&T to hold onto a money-losing service (Disney reported a $580 million loss from Hulu for its fiscal 2018). In fact, it’s been reported that Comcast’s successful bid for Sky has inspired it to sell its Hulu stake to Disney.

Since Bob Iger has already stated his interest in acquiring all of Hulu, it’s now starting to look like a done deal. Hulu has over 25 million subscribers, and although it’s a drop in the bucket compared to Netflix’s (NASDAQ:NFLX) 140 million, the service has yet to expand beyond the US; Hulu has roughly 43% the US subscribers as Netflix (58.5 million).

Hulu does not equal Disney+ or ESPN+, but in its most recent earnings call, Disney stated that its end goal in streaming is to have multiple services available to choose from under one account or credit card.

Many have pointed out that by simply pulling content from Netflix, Disney, along with other studios, will be losing hundreds of millions in royalties from the streaming service. Unfortunately, with Netflix becoming a very large spender in studio production, it effectively became a competitor leaving Disney with no other choice. After all, why would Netflix pay premiums for Disney content when it could entertain its customers with its own content for less? In order to succeed, Disney must continue to become a distributor of its own content; if streaming is the way to do it – just like launching the Disney Channel was in the ’80s – it will be done.

Eventually, Disney+ could be jumpstarted by Hulu’s existing 25 million paying subscribers. Since it has taken nearly a year for ESPN+ to obtain 2 million subscribers, Hulu is a big win for Disney.

2. Disney’s Streaming Content Is Underestimated

With no official date in sight, Disney+ will launch later this year and with Hulu and ESPN+ already under its belt, the new service will be its third angle of attack into the highly competitive industry. On its information webpage, Disney+ is advertising Pixar, Star Wars, Marvel, and National Geographic. However, this merely scratches the surface of what’s under the House of Mouse. Here is a brief list of studio content; I’ve excluded what I know must be liquidated in an effort to meet government regulations across the globe such as Lifetime, History Channel, A&E, Fox Sports, and others.

- Disney XD

- Disney Junior

- Disney Channel

- Disney Studio Pictures (movies)

- Marvel Studios

- Pixar Animations

- Lucas Films Ltd

- ABC Studios

- Freeform

- National Geographic

- Fox Network

- FX Networks

- Vice

- Blue Sky Studios

- Star

- Endemol Shine

- Star India

- Hulu Originals

Content, especially quality content, is what will help drive Disney’s success. Netflix, as an example, continues to increase its debt position and burn through roughly $1B in cash per quarter to expand its content library. While Disney may be late to streaming, it’s most certainly not late to content, which is equally important. Disney sits on decades of content and will have dozens of studios expanding upon its library. Whether it’s for children or adults, Disney has entertainment for just about everyone. Personally, I can’t wait to watch some childhood classics.

Netflix doesn’t have to lose for Disney to win. Bob Iger stated that Disney+ would cost less than Netflix, and that was before the price hike. This could either make Disney+ more attractive at a much lower price or the service could charge more than originally anticipated to help cover the expenses of launching.

This was written before the Oscars, so here are some quick notes. At the surface, it wasn’t a slam dunk for Disney having won just four awards, but with Fox winning 7 academy awards, I’d call this a slam dunk. Let’s remember that Disney capitalizes on its content for decades whether it be through new attractions, games, or toys. It even lost its 6-year winning streak from the best animated movie award. Disney’s animated movies for 2018 were Ralph Breaks The Internet and Incredibles 2 – both which are sequels from movies that were nowhere near the success of 2019’s animated movies: Toy Story 4 and Frozen 2.

Finally, Disney is also a very powerful brand. When Netflix debuted Roma in theaters, movie chains such as AMC refused to show it as it would be available for streaming before what is currently a standard 90-day waiting period. I’m not sure how resistance to a big customer like Disney would result. Disney could utilize this approach and accelerate customer adoption to Disney+ by releasing new movies on Disney+ before the 90-day period. After all, not everybody wants to watch a movie at the theater (especially Disney movies that tend to attract the younger audiences that can be a bit clamorous).

3. Disney Is Cheap And Profitable Despite Streaming Costs

Disney lost over $1 billion in streaming from Hulu and ESPN+ in its fiscal 2018 but, as a company, still produced $10B in free cash flow and a net income of $12.6 billion for its fiscal year. That’s very impressive. While analysts recognize these costly ventures, Disney has exceeded earnings estimates in three out of the last four quarters. In its most recent, it had an EPS of $1.84 versus the estimated $1.55.

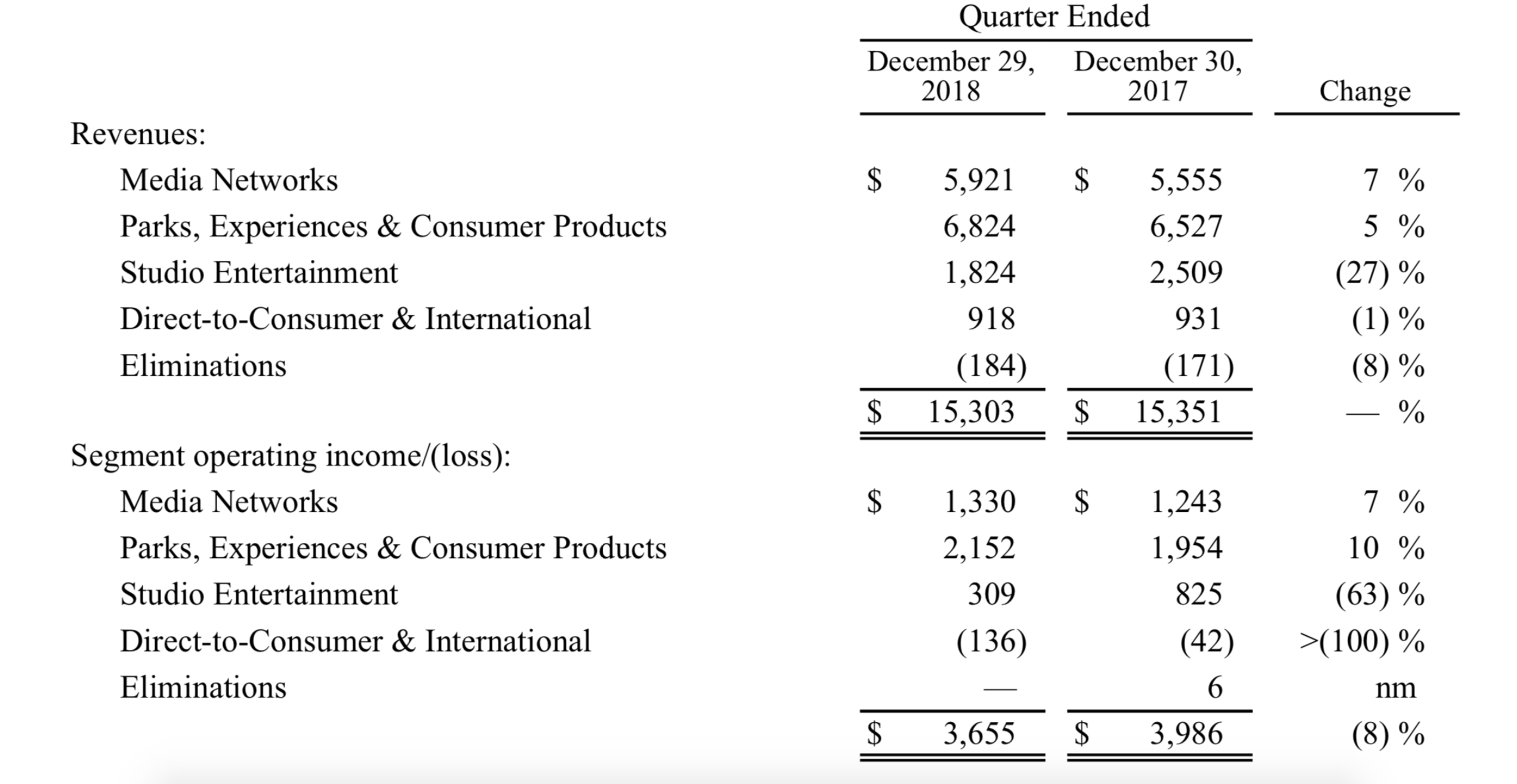

Additionally, as seen below, Disney’s largest revenue streams, Media Networks and Parks, Experiences & Consumer Products were, respectively, up 7% to $5.9B and 5% to $6.8B. Disney’s theme parks are now its biggest source of revenue and profit. This is not something that a streaming service like Netflix has, and is incredibly valuable. Eventually, Disney will be selling a movie ticket, a streaming service, an amusement park ride, a dining experience, hotel room, a toy, and so much more.

Such a large product portfolio softens the initial expenses of expanding into streaming, and despite its initial efforts, it still manages to hold a price-to-earnings ratio of 15.5. The multiples of the DJIA and S&P 500 are significantly higher, respectively, at 18.21 and 20.23.

{kind=link}

When making heavy investments to fuel growth, it is common for PE ratios to jump. Walmart (WMT) tripled its PE ratio to more than 40 as its heavy investments in e-commerce to compete with Amazon (AMZN) put a drag on earnings. With a relief that Walmart would remain relevant and still sustain profits and pay dividends, the stock jumped as much as 80% in three years. If investors are pleased by the success of Disney+, its stock could easily duplicate these results.

Disney+ will be costly, but The Walt Disney Company will still remain profitable. As long as the streaming service is a success, in which its strong content library suggests should be easy, a clear path to victory comes into sight. In a sense, Disney owning a direct-to-consumer platform is essentially the modern approach to launching the Disney Channel in the 1980s where it previously licensed all of its content to other networks.

Conclusion

While Disney’s stock has been in limbo in recent years, a big swing in some direction is bound to happen. Streaming is a big potential source of income for Disney and an opportunity to maintain its customers in an ecosystem similar to the Disney Channel that launched in 1983. With the acquisition of Fox, Disney will have controlling interest in Hulu with 60% ownership. Comcast and AT&T are each working on their own direct-to-consumer services making Hulu a costly conflict of interest. With over 25 million paying subscribers, housing ESPN+ and Disney+ under the same house would jumpstart the newer services.

The question then shifts to whether Disney can be successful in streaming. If Netflix’s ambitious spending in content is any evidence that content is important, then the answer is a resounding yes. With Fox, Disney is sitting on dozens of studios, including international operations that are constantly producing new content while sitting on decades of work. Netflix doesn’t need to lose for Disney to win. Just like there is more than one channel in television, there can be more than one streaming service.

Finally, relative to the market, Disney is cheap. With a PE ratio of about 15.5, Disney is well below the S&P 500’s average PE of 20 and the Dow’s average multiple of 18. Given that Disney+ will be an expensive venture, I’d expect to see that figure jump. Provided that Disney+ is successful, investors will very likely pay the premium to ride with Disney. I see a similar scenario to Walmart. Just like Walmart’s PE ratio tripled and the stock nearly doubled in the last three years, its profitability and ability to sustain dividends have still made it attractive to investors. Over the next few years, Disney will be most likely be an excellent stock to buy and hold.

Disclosure: I am/we are long DIS. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.