HI Market View Commentary 09-19-2022

Let’s learn some simple rules/idea to better understand the difference between investing and trading?

The first difference is usually timing BUT timing is a fools game

FOMC Rate hike of a leas 0.75 % or 75 basis points Wednesday 12 Noon MST

Investing allows for a longer trading horizon, and allows more time to make a decision

Day Trading is NOT a repeatable process

Investing means daily work to check numbers like a stock we trade = META

IF you do your research then sometime in the future you can have the profits you are expecting

Since Timing is a fools game we use the protective put to wait, in case we are wrong, incase the market is wrong on our research

We also can dollar cost average without having o ask for more money from you guys = Perk

Why do you not spread trade more?= Once you lose the money is gone and I HATE losing

Mentally It is easier to handle stock prices falling because I am making something up on the way down and they have forever to come back.

Something I find Interesting = NOBODY called me last week when he market had down days and accounts were positive

1.55% down week for HI and 4.8% down week for the S&P

The key to getting through the troughs in the market?= Using a mathematical and proven strategy

We all know that markets go through cycles or waves and they are completely unpredictable

AAPL, BA, BIDU, BAC, DIS, F, META, JPM, V, UAA,

ALK, CLX, COST, CVS, DG, GE, GOOGL, KEY, KO, MU, NEM, PYPL, SQ, TGT, VZ, CVX

Earnings dates:

COST 9/22 AMC – ????

MU 9/28 – NO

https://www.briefing.com/the-big-picture

The Big Picture

Last Updated: 14-Sep-22 17:02 ET | Archive

August CPI report gets in the way of the Hollywood ending

To put it mildly, the August Consumer Price Index (CPI) did not go over well with either the Treasury market or the stock market. It prompted a violent reaction in both markets because the data were out of sorts with the friendly narratives that had been working their way into the price action leading up to the report.

Everyone should be familiar with those narratives by now. They include peak inflation, peak hawkishness, and a soft landing for the economy.

Well, the August CPI report created a new chapter for those narratives that had an unhappy twist.

Eye on CPI

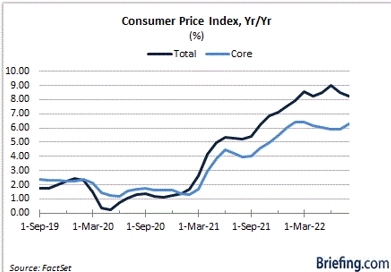

The Consumer Price Index increased just 0.1% month-over-month in August. Why the hubbub over such a small increase? There were two reasons:

- That was worse than the consensus estimate that projected a 0.1% month-over-month decline.

- The month-over-month increase occurred despite a 5.0% decline in the energy index that was paced by a 10.6% drop in the gasoline index. In other words, inflation was broad enough to offset the decline in energy prices.

The Consumer Price Index, excluding food and energy, was up 0.6% month-over-month. There were three reasons why that increase sent the markets into a tailspin:

- It was double the consensus estimate that called for a 0.3% increase, so it qualified as a major surprise/shock.

- It was a byproduct of broad-based inflation pressures that were led by a 0.7% month-over-month increase in the shelter index, which accounted for about 40% of the total increase in core CPI.

- It left the year-over-year rate for core CPI at 6.3% versus 5.9% in July. In other words, inflation in the components the Fed believes its policy tools have more influence over worsened in spite of prior rate hikes.

This was not the news the Fed wanted to hear — and the stock and bond markets instantly knew that. They also knew that it likely meant the Fed is going to stay on an aggressive rate-hike path.

The 2-yr note yield, sitting at 3.50% just before the CPI report, spiked to 3.75%. The S&P 500 plunged as much as 4.6% and suffered its fifth-largest point loss in history. The fed funds futures market priced out any expectation of a 50-basis point increase at the September 20-21 FOMC meeting. Instead, it priced in a 32% probability of a 100-basis point increase at that meeting, meaning it fully expects a rate increase of at least 75 basis points.

Yep, It Was Absurd

Arguably, there was more psychological fallout from the August CPI report than there was anything else. The stock market certainly wanted to believe that the Fed will stay on a glide path to 3.75-4.00% by year end, sit at that level for a bit, and then start cutting rates in 2023.

That was the script, and it was replete with a Hollywood ending of a soft landing for the U.S. economy.

The reason the stock market fallout after the August CPI report was as significant as it was had to do with the market re-thinking that happy ending. Now, it must contemplate an even higher terminal rate for the Fed, the specter of inflation staying higher for longer and, by default, the Fed sticking with a higher terminal rate for longer.

The other unsettling thought was that this will result in an unhappy hard landing for the U.S. economy as the Fed, late to the rate-hike game, overplays its hand and (cliche alert) makes a policy mistake.

This is not a new thought to us. We penned a column here last November entitled An absurd monetary policy position is a risk we should all see coming.

We said then that “The Fed is playing with fire still sitting on the zero bound with the inflation rate at 6.2%, an economy averaging 5.0% real GDP growth, and the unemployment rate at 4.6%. It’s an absurd policy position, because it’s the same position the Fed had when the inflation rate stood at 0.2%, real GDP was negative 31.2%, and the unemployment rate was close to 13.0%.”

We added that the stock market was taking advantage of the absurd policy stance, but understandably so, before cautioning that, the higher the stock market climbs, the harder it will fall when an exogenous shock hits or that policy support gets pulled abruptly.

The S&P 500 closed at 4,682.85 that day. It would eventually climb to 4,818.62 on January 4. Today, it sits at 3,950, down 18% from that high and armed with the knowledge that Russia invaded Ukraine in February and that the Fed is working feverishly to pull its policy support.

Quantitative easing is out, and quantitative tightening is in. The target range for the fed funds rate, at the zero bound at the end of January, is now 2.25-2.50% and destined to hit at least 3.00-3.25% by this time next week. Fed officials are now all jawboning the need to raise rates to get inflation under control and to stay at it as long as necessary.

Better Late than Never

What is that saying? Better late than never?

The Fed arrived late to the inflation-fighting game, but it is now on the playing field, and it means business. Unfortunately, that means trouble for the economy and for investors.

That was the added sting of the August CPI report. Market participants knew that it meant the Fed would be putting through another aggressive rate hike; moreover, with the core rate of inflation moving away from the longer-run goal of 2.0%, they also feared that the rate hike next week won’t be the last of the aggressive rate hikes.

The terminal rate, which the market previously had pegged in the 3.75-4.00% range, is now 4.25-4.50%. That moving target is moving in the wrong direction for a stock market that desperately wants the Fed to be its friend again.

That is a major roadblock, too. The Fed desperately wants to get inflation under control, and it has no interest in being the stock market’s friend. The Fed sounds as if it is willing to fall on its sword, too, if a hard landing is what it takes to get inflation back to its 2.0% target.

What It All Means

The Fed would like the Hollywood ending of a soft landing, too, but the pace at which it is raising the policy rate, the pace at which market rates and the dollar are following, and the higher interest costs to service the national debt, are diminishing the prospect of a soft landing and raising the potential for a financial accident.

That does not even account for the slowdown that is occurring elsewhere on account of other central banks aggressively raising their policy rates. The slowdown problem isn’t just a U.S. problem. It is a global problem and the rapid increase in all these policy rates will have a commutative effect on earnings prospects.

This is not a new revelation for Briefing.com readers. We have been warning about this commutative effect for some time:

July 16, 2021: Interest rates remain the change agent for the bull market

October 8, 2021: Wage inflation is a monetary policy problem in the making

October 22, 2021: Bull market okay until interest rate push comes to shove

November 12, 2021: An absurd monetary policy position is a risk we should all see coming

December 3, 2021: The end of the party is just getting started

December 10, 2021: 2022 stock market return expectations should get dialed down

December 16, 2021: Fed Chair Powell delivers understatement of the year

February 25, 2022: The Federal Reserve is in a bad spot

March 25, 2022: Let the front-loading begin

April 29, 2022: The Federal Reserve is about to cross the Rubicon

June 10, 2022: The Fed has much work left to do to tame the bane of our existence

July 29, 2022: Shelter costs create difficult proving ground for policy pivot

August 10, 2022: Peak inflation? Maybe. Peak hawkishness? Not yet.

August 26, 2022: Powell and the Fed mean business in restoring price stability

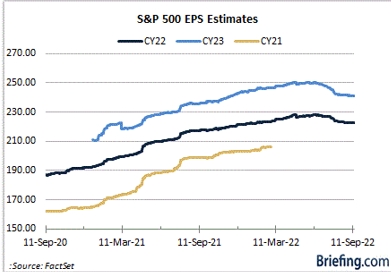

What the Treasury market seems to be accounting for more now is the lag effect of the Fed’s rapid-fire rate hikes. The yield curve is inverted, which is not a good harbinger for growth. The stock market hasn’t succumbed to the recession scenario, which is evident in earnings estimates that still call for year-over-year earnings growth in 2022 and 2023.

Here again Briefing.com readers know we think earnings estimates are still too high. They have been coming down but are apt to come down further knowing that the Fed has more work to do with rate hikes and that the lag effect has more work to do in kicking in for consumers and businesses.

Hence, there was more to the August CPI report than just high inflation. There were monetary policy implications that will make multiple expansion harder to come by given the uncertainty about how far the Fed and other central banks will go with their rate hikes and how fast they have been moving to correct the first policy mistake of not moving at all, or too little, when economic conditions allowed for it.

The ending here has yet to be written, but the writing is on the wall that catch-up efforts to correct the first policy mistake have increased the risk of making the next policy mistake of piloting a hard landing.

—Patrick J. O’Hare, Briefing.com

https://go.ycharts.com/weekly-pulse

| Market Recap |

| WEEK OF SEP. 12 THROUGH SEP. 16, 2022 |

| The S&P 500 index fell 4.8% last week, wiping out last week’s 3.6% climb, as investors were spooked by a report of higher-than-expected consumer price inflation in August as well as a profit warning by package delivery company FedEx (FDX). The market benchmark ended the week at 3,873.33, down from last Friday’s closing level of 4,067.36. This marks the index’s fourth weekly drop over the last five weeks. It is now down 2.1% for the month to date and down 19% for the year to date. The week included the largest one-day drop in the S&P 500 index since June 2020, coming Tuesday after data from the Labor Department showed US consumer prices unexpectedly edged higher in August versus July amid broad-based monthly gains, while core inflation accelerated more than expected, boosting expectations that the Federal Reserve would push forward with a more aggressive tightening cycle. The data showed the consumer price index rose 0.1% in August on a monthly basis. This compared with a flat reading in July and an Econoday consensus estimate for a 0.1% drop. It also showed annual inflation advanced 8.3% last month, lower than an 8.5% jump in July, but higher than the Street’s view for an 8.1% increase. Adding to investors’ worries later in the week, FedEx (FDX) preliminarily reported results for its fiscal Q1 ended Aug. 31 below analysts’ expectations and withdrew its fiscal 2023 earnings guidance. The company also disclosed cost-cutting measures after preliminary data showed a decline in global volume accelerated in the final weeks of the quarter. All of the S&P 500’s sectors fell last week, with materials leading the way lower with a 6.7% drop. Other top decliners included real estate, down 6.5%, while communication services and industrials fell by 6.4% each and technology shed 6.1%. Nucor (NUE) was the hardest-hit materials stock last week, tumbling 18% as the steel manufacturer said it expects fiscal Q3 earnings between $6.30 and $6.40 per share, down from $7.28 per share a year earlier and below analysts’ mean estimate at the time of $7.59. The downbeat guidance came as Nucor said its steel mills segment’s earnings for its fiscal Q3 ending Oct. 1 will be “considerably” lower than the prior quarter due to metal margin contraction and reduced shipping volumes. The real estate sector’s decliners included shares of Weyerhaeuser (WY), as the owner of timberlands said a work stoppage involving members of the International Association of Machinists and Aerospace Workers union is impacting its operations in Oregon and Washington. Weyerhaeuser shares fell 11%. Industrials were weighed down by FedEx’s warning, which included expectations for business conditions to weaken further in its fiscal Q2. “While this performance is disappointing, we are aggressively accelerating cost reduction efforts and evaluating additional measures to enhance productivity, reduce variable costs, and implement structural cost-reduction initiatives,” FedEx CEO Raj Subramaniam said in a statement. Shares of FedEx lost 23% on the week. In communication services, shares of Match Group (MTCH) shed 11% as Loop Capital downgraded its investment rating on the online dating company’s stock to hold from buy. This came after S&P lowered its outlook on the stock last week to stable from positive, citing weaker guidance. In the technology sector, shares of Adobe Systems (ADBE) fell 24% last week as the software company reported fiscal Q3 revenue slightly below the Street consensus estimate and unveiled an agreement to acquire web-first collaborative design platform Figma for $20 billion in cash and stock. The stock’s decline also came amid several rating downgrades on Adobe last week from firms including Mizuho Securities, BMO Capital, and Oppenheimer. Next week, all eyes will be on a meeting of the Federal Reserve’s policy-setting body, the Federal Open Market Committee. Housing data will also be in focus, with August building permits and housing starts scheduled for release Monday, followed by August existing home sales on Tuesday. On Friday, S&P Global will conclude the week with a release of its September readings on US manufacturing and services. Provided by MT Newswires |

Where will our markets end this week?

Lower

DJIA – Bearish

SPX –bearish

COMP – Bearish

Where Will the SPX end September 2022?

09-19-2022 -2.0%

09-12-2022 -2.0%

09-06-2022 -2.0%

08-29-2022 -2.0%

Earnings:

Mon: AZO,

Tues:

Wed: GIS, FUL, KBH, LEN, SCS, TCOM

Thur: DRI, FDX, COST

Fri:

Econ Reports:

Mon: NAHB Housing Market Index

Tues: Housing Starts, Building Permits

Wed: MBA, Existing Home Sales, FOMC Rate Decision

Thur: Initial Claims, Continuing Claims, Current Account Balance

Fri:

How am I looking to trade?

Everything has puts, ration protective puts or twice the puts right now.

www.myhurleyinvestment.com = Blogsite

customerservice@hurleyinvestments.com = Email

Questions???

Here’s what Gundlach’s watching in the yield curve, the ‘granddaddy’ of recession indicators

PUBLISHED WED, SEP 14 20221:42 PM EDTUPDATED 2 HOURS AGO

Jeffrey Gundlach, CEO of DoubleLine, is watching the Treasury yield curve as a primary harbinger of recession – and he warns that a downturn is almost assured if it inverts past a certain level.

A yield-curve inversion occurs when yields on short-term U.S. Treasury bonds are higher than those of longer-term Treasurys. Bond yields move inversely to prices.

“I’m waiting for the 2s/10s to invert by 50 [basis points],” Gundlach told CNBC in an interview on the sidelines of the Future Proof wealth conference in Huntington Beach, Calif., referring to yields on U.S. 2-year Treasury bonds and 10-year Treasurys.

“5s/30s finally reinverted again,” Gundlach added, referring to 5-year and 30-year Treasury bonds. “That might get to like 25 [basis points].”

“I think at that level, it’s almost assuredly on the edge of a coming recession,” he said.

While both of those respective parts of the yield curve are inverted, they haven’t yet reached Gundlach’s stated thresholds. The 2-year and 10-year spread was inverted by about 37 basis points (or 0.37%) as of 1:33 p.m. ET on Wednesday. The spread between the 5-year and 30-year was about 11 basis points (or 0.11%).

Bond yields had climbed on Tuesday as stocks sold off sharply after a hotter-than-expected inflation report. Spreads on Treasury yields narrowed. On Wednesday, even as stocks recovered, the yield on the 2-year Treasury — the part of the curve that’s most sensitive to the Federal Reserve’s policy — was still higher than those of the 5-, 10-, and 30-year notes.

Gundlach is watching for a “massive sell-off at the short end [of the yield curve] and the long end doing almost nothing. That’s a real sign that you’re getting very late, late cycle.”

He called the yield curve “the granddaddy” of recession indicators, during a Q&A with CNBC’s Scott Wapner.

“I think the chance of recession in 2023 is really quite high,” Gundlach told Wapner.

Stock market could rally big in fourth quarter, but there will be more pain first

PUBLISHED WED, SEP 14 20222:25 PM EDT

Patti Domm@IN/PATTI-DOMM-9224884/@PATTIDOMM

The stock market could still see a fourth quarter rally, but it’s likely to first feel more pain.

Strategists who follow charts say the big sell-off Tuesday was a negative and signals more selling ahead. But the market also could reach a bottom from which to pivot in the next couple of weeks, and the debate is whether that level will be below the June lows or above them.

Parts of the market were marginally higher Wednesday after Tuesday’s sharp decline. The S&P 500 fell 4.3% Tuesday, its worst one-day performance since June, 2020.

The sell-off came after a report of higher-than-expected consumer inflation Tuesday morning. That caused investors to reassess how aggressive the Federal Reserve could be in its fight against inflation.

It also threw into doubt whether the market will continue to follow the road map analysts expect to see in a typical mid-term election year. In most mid-term years, the market is typically negative in the second and third quarter, before bottoming in the third quarter, and rallying in the fourth quarter.

Ed Clissold, chief U.S. strategist at Ned Davis Research, said the Dow Industrials and S&P 500 do not need to go as low as the June lows in order to see a restest. The S&P touched 3,636 in mid-June, around the same time that the 10-year Treasury yield peaked at just below 3.5%.

Stocks had been higher ahead of Tuesday’s consumer price index, on expectations the data would show improvement and the Fed would soon be able to pause its rate hiking.

Giving back what it gained

“For the most part, the market gave back what it gained over the previous several sessions,” said Clissold. “We had been thinking this was the best window for a retest going into late September, early October.”

Clissold said while Tuesday was a negative day, it did not give a clear signal whether the retest will fail.

“From a broader perspective, the market backing and filling and trying to figure out if it can mount a year end rally or not, that’s probably what the next few weeks are about,” Clissold said.

Mark Newton, Fundstrat global head of technical strategy, said he expects the S&P could break last week’s lows and possibly trade down to the 3,650 to 3,750 area. The June low was 3,636, and the S&P was at about 3,950 Wednesday afternoon.

“Tuesday’s selloff looks important and negative technically, and likely jumpstarts the decline into early October,” notes Newton.

“At present, cycles look negative for at least the next three weeks,” he added.

The reversal in stocks Tuesday came alongside a selloff in the dollar, rising Treasury yields and decline in cryptocurrencies.

“All these sudden reversals likely could persist into early October. That should ultimately pave the way for higher prices in Q4 given how bearish sentiment was in recent weeks,” Newton added.

Oppenheimer technical strategist Ari Wald also expects the market to move higher in the fourth quarter, following the typical course of a mid-term election year.

He added that he studied the S&P 500 following one day declines of 4% or more and found the market is typically positive a month, three months and a year later.

Based on data going back to 1928, he said the S&P was higher by an average 1.1% one month after a major sell-off, compared to the average gain of 0.6% during any one month. After 12 months, the S&P averaged a 15.3% gain, better than the average 8% gain in a year.

Siding with higher lows

Wald said he expects the market could find a near term bottom soon. “We are siding with a higher low, rather than a lower low. A less intense lower low is possible,” he said.

Wald said he still expects a fourth quarter bounce. The leaders of that move could be big cap tech, which have been lagging. “It’s their weakness that has dragged the market…It’s actually masking the improving conditions under the surface,” he said.

For big cap tech, “once we get that turn they’ll likely be part of that but they’ll likely be in the penalty box near term,” he said.

Investors are now betting the Fed will raise interest rates higher than they had expected before the release of August’s CPI. That report showed a 0.1% gain in CPI, while the market expected a decline of 0.1%.

In the futures market, the Fed’s terminal or end rate, was priced at 4.38% Wednesday, up sharply from just below 4% before the CPI report. That is the rate where the Fed is expected to stop raising rates.

The Fed meets next Tuesday and Wednesday and is widely expected to raise interest rates by 75 basis points, though at least one Wall Street firm expects a full percentage point hike. A basis point equals 0.1 of a percentage point.

Besides raising rates, the Fed will present new forecasts for interest rates, inflation and the economy Wednesday afternoon.

“That’s going to be the next big piece of information that the markets will digest, and what the CPI report does is it increases the likelihood the Fed is going to maintain its stance of continuing to hike rates,” said Clissold. He also said the Fed is going to continue to sound hawkish to maintain its credibility.

“They don’t want to appear wishy washy. They are going to maintain this stance until they are ready to pivot,” he said.

Cathie Wood goes on a big buying spree during stock market’s worst sell-off of the year

Tuesday’s massive sell-off presented Cathie Wood an opportunity to scoop up more of her favorite innovation stocks.

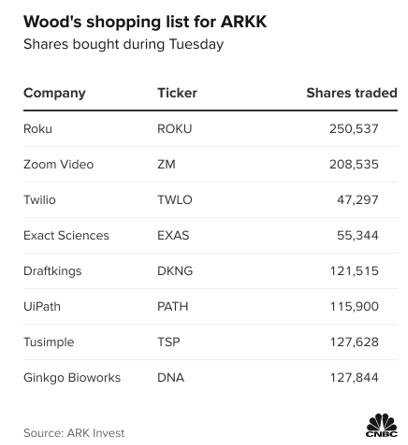

The popular investor added stocks for five of her exchange-traded funds Tuesday, when the S&P 500 suffered its worst day of 2022 with a 4.3% drop. Wood snapped up shares of eight companies for her flagship ARK Innovation ETF, including adding to two of her largest holdings, Roku and Zoom Video.

Roku and Zoom dropped 5.5% and 6.2%, respectively, on Tuesday. Wood’s purchases of the duo were worth about $33.5 million based on their closing prices.

Wood also bought more shares of molecular diagnostics company Exact Sciences, which is ARKK’s fourth biggest holding. The innovation investor also ramped up her bets on Twilio, DraftKings, UiPath, Tusimple and Ginkgo Bioworks for her flagship fund.

Her buying spree came as the market sold off after a key August inflation report came in hotter than expected, hurting investor optimism for cooling prices and a less aggressive Federal Reserve. The Dow Jones Industrial Average tumbled 1,200 points for its worst day since June 2020.

Despite the hot reading on the consumer price index, Wood still believes that deflation is the bigger threat right now, a risk she’s been warning about since last year. She said Tuesday in an investor webinar that the Fed is making a policy mistake with big rate hikes.

Wood also reiterated her conviction on innovation stocks to her clients, who have been disappointed with Ark’s performance this year. ARKK is down 55% this year as her disruptive darlings got hit hard by rising rates. ARKK also just suffered three straight months of outflows.

“Innovation solves problems,” Wood said Tuesday in the webinar. “We believe that truly disruptive innovation is priced in the global equity markets for roughly $8 trillion, and we believe that $8 trillion is going to scale to over $200 trillion in the next eight to 10 years.”

Warner Bros. Discovery CFO calls company’s HBO Max and Discovery+ ‘underpriced,’ suggesting price hikes may be coming

KEY POINTS

- Warner Bros. Discovery CFO Gunnar Wiedenfels said his company’s streaming services were ‘underpriced’ during Goldman Sachs Communacopia Tech Conference.

- Wiedenfels declined to say how his company will price a combined HBO Max-Discovery+ service.

- Disney announced sweeping price increases to its streaming services last month.

- HBO Max without ads is currently $14.99 a month; Discovery+ without ads is $6.99 a month.

Streaming service subscriber growth may be slowing, but that doesn’t mean prices won’t keep rising.

HBO Max and Discovery+, Warner Bros. Discovery’s two flagship streaming services, are “fundamentally underpriced,” Chief Financial Officer Gunnar Wiedenfels said during the Goldman Sachs Communacopia Tech Conference on Tuesday.

Oppenheimer upgrades Netflix, says new ad tier can boost growth

3 HOURS AGO

Wiedenfels suggested the company had ample room to raise prices given the strength of content on the services, which will be merged into one next year. Last month, Warner Bros. Discovery said it planned to launch a combined HBO Max-Discovery+ service in the U.S. in mid-2023, with international markets to follow.

While Warner Bros. Discovery hasn’t announced how it will price a combined service, Wiedenfels’ comments suggest the company may use the merging as a chance to raise prices. HBO Max is currently $14.99 per month without ads and $9.99 per month with commercials. Discovery+ is $6.99 per month without ads and $4.99 per month with commercials.

Wiedenfels noted HBO Max won more Emmys (38) this week than any other streaming service. HBO’s “The White Lotus” snared the most awards during the prime-time ceremony with five, including Outstanding Limited Series. Warner Bros. Discovery’s strategy is to combine HBO’s award-winning programming with Discovery’s lighter reality content, which should reduce “churn,” or number of subscribers who cancel the service, Wiedenfels said.

Price hikes abound

Netflix is currently the most expensive major streaming service with a standard plan price of $15.49 per month. Disney announced price increases for Disney+, ESPN+ and Hulu last month, including bumping the price of Disney+ without ads from $7.99 per month to $10.99 per month.

Warner Bros. Discovery set new streaming subscriber targets last month, including 130 million global subscribers by 2025. The company also reaffirmed its expectation for its streaming business to break even by 2024 and yield $1 billion in profit by the end of 2025.

Warner Bros. Discovery isn’t chasing subscriber growth at all costs, said Wiedenfels. That change — to prioritize profitability over growth — allows the company more “pricing power” over its streaming businesses, he said.

“We’re not optimizing for subscribers,” said Wiedenfels, who called that type of strategy “old world streaming” thinking.

–CNBC’s Sarah Whitten contributed to this report.

Apple may be seeing a demand split for iPhone 14 models, Bank of America says

There is a divergent picture of demand developing for Apple’s newest lineup of iPhones, according to Bank of America.

Analyst Wamsi Mohan said in a note to clients on Monday that the ship dates for the iPhone 14 Pro and iPhone Pro Max — which have higher average selling prices than the standard iPhones — have extended projected shipping times compared to prior launches. That could be a sign of strong demand, with more customers putting in early orders for the more expensive phones.

But that appetite does not appear to exist down the lineup, where the iPhone 14 and iPhone 14 Plus have shrunken wait times compared with prior years.

“The iPhone 14/14 Plus offer lesser differentiation than the Pro models as they have a similar form factor and same chip as last years’ iPhones. This could be driving customers to shift into the iPhone 14 Pro/Pro Max models which bodes well for mix and ASP, in our opinion. However, this might also suggest weaker demand overall for iPhone 14, which could be concerning,” Mohan wrote.

One wrinkle this year is that the iPhone 14 Plus isn’t officially ready for shipping until Oct. 7, instead of on the same day as the rest of the new models. That change and component shortages could be impacting the year-to-year comparisons of shipping times, Mohan cautioned.

Bank of America has a buy rating and a $185 per share price target for Apple. The stock closed at $150.70 per share on Friday.

Shares of Apple are down 15% year to date.

The S&P 500 could retest its bear market low as Fed meeting looms, according to chart analysts

Patti Domm@IN/PATTI-DOMM-9224884/@PATTIDOMM

With the Federal Reserve meeting this week, stocks could be volatile, and technical analysts say the S&P 500 looks increasingly set for a retest — and possible break — of its June low.

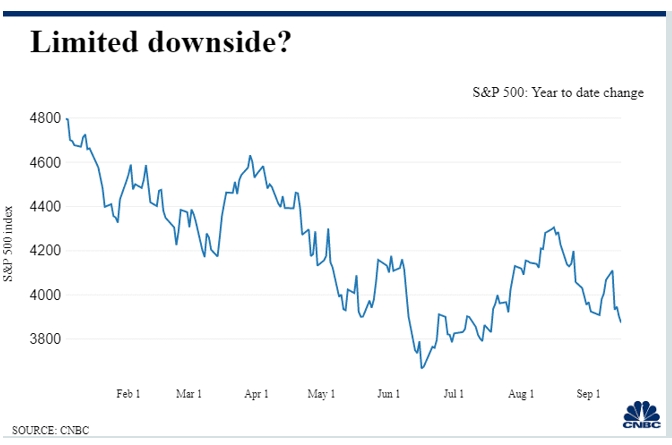

Stock charts have seen a lot of damage recently, and some technical strategists are becoming more pessimistic in the near-term. In the past week, the S&P 500 declined 4.8%, closing at 3,873, in its worst weekly performance since June.

“We’ve sided with a higher low in the S&P 500, and believe a ‘less intense’ lower low has become more likely following rollovers in select mega-cap stocks,” writes Oppenheimer’s Ari Wald this weekend. “The crux of our view is that mega-cap weakness is masking improving breadth which we think bottomed in June.”

Wald now says a dip to 3,500 on the S&P 500 is possible. That is the 50% bull market retracement. His previous expectation of a near-term low point was 3,800. Weakness in stocks like Alphabet, NVIDIA and Microsoft helped change his view.

Stocks could be volatile again this week, with the Federal Reserve meeting Tuesday and Wednesday. The Fed is expected to raise its target fed funds rate by another 75 basis points Wednesday and also provide new forecasts on the economy, inflation and interest rates. A basis point equals 0.01 of a percentage point.

“Significant seasonal headwinds in September suggest the market is vulnerable going into next week’s FOMC decision,” noted Wald. The analyst, however, continues to believe the market will bottom in October and then rally in the fourth quarter, in line with its typical behavior in mid-term election years.

Jonathan Krinsky, chief market technician at BTIG, said the 3,900 level was important and the area on the S&P 500 where the most volume traded over the last three years.

“It closed below that on Friday, which opens the door down to the June lows,” Krinsky wrote in a note. The June low was 3,636.

Krinksy also points to weakness in the charts of big cap tech – Apple, Microsoft, Alphabet and Amazon.

“They might be giants. But some of the biggest marquee names in the market continue to look vulnerable to us here,” Krinsky added.

In mid-term election years, the typically negative month of September has been a time of weakness, into October. Mark Newton, Fundstrat global head of technical strategy, said the market turned lower right on schedule in the past week, confirming seasonal bearishness.

“While one cannot rule out a 1-2 day bounce attempt given this week’s decline, I do not expect much strength until prices have reached support under 3,700 in October,” Newton wrote. “Tactically, ‘cash remains king’ and one should be patient until markets reach downside targets, and begin to show either volume and breadth divergences, or capitulation to buy.”

Stocks had been higher heading into last Tuesday’s report of August consumer inflation. The consumer price index for August was up 0.1% instead of falling 0.1%, as expected by economists. That kicked off a new round of higher expectations for Federal Reserve interest rate hikes in the central bank’s fight against inflation.

Wald said the market is still trading on the view that the Fed needs to pivot from its rate hiking policies in order for stocks to bottom. “Overall, while volatility is likely to linger into next month’s CPI print, market conditions are developing to support such a turn in Q4, based on our read of the tape,” he wrote.

The Oppenheimer technical analyst notes that the S&P 500 has typically bottomed around Oct. 9, before launching into a strong rally into year-end, based on the average composite of the last eight mid-term election years.

“This suggests the next CPI release (Oct. 13th) could act as a potential catalyst, should it provide flexibility for Fed policy. Overall, we maintain our view that market behavior suggests a base is forming, and volatility is at risk to linger until seasonal headwinds become tailwinds,” Wald wrote.

With inflation still high, the Fed may be a long way from where it can stop hiking

Jeff Cox@JEFF.COX.7528@JEFFCOXCNBCCOM

Rising interest rates have made only a modest dent in inflation so far and may need to go considerably higher, according to Morgan Stanley.

Declining gasoline prices have helped keep a lid on top-line inflation over the past two months. But that trend has masked cost-of-living increases that have spread to other areas.

For instance, food prices in the consumer price index have risen 1.9% over the past two months while shelter costs, which make up about one-third of CPI, are up 1.2% during the same period. Headline inflation, including food and energy prices, is still 8.3% higher year over year, while core inflation — excluding food and energy — has risen 6.3%, including a much higher than expected 0.6% monthly gain in August.

The inability to tame inflation on a broad level could make policymakers impatient and also drive up longer-term interest rates, Ellen Zentner, Morgan Stanley’s chief U.S. economist, said in a client note dated Friday.

“The real economy may simply be less sensitive to higher rates today, which means the level of interest rates needed to slow the economy is also likely to be higher,” Zentner said. “Getting there quickly can be costly.”

Markets expect the Fed on Wednesday to enact a third consecutive 0.75 percentage point rate increase and another hike of that size when it next meets in November, with pricing leaning toward a half-point move in December, according to the CME Group.

Current market pricing in fed funds futures indicates the Fed’s “terminal rate,” or the point where it halts the rate increases, will hit 4.39% in April 2023.

The Fed targets its benchmark rates in quarter-point ranges, so that’s consistent with a terminal rate of 4.25%-4.5%. According to the rate-setting Federal Open Market Committee’s projections in June, the terminal rate was expected to rise to 3.8% in 2023, meaning that current market pricing is about half a percentage point ahead of that outlook.

But Zentner thinks the central bank may have to go even further to tackle inflation. The Cleveland Fed’s measure of “sticky price” inflation of goods whose prices generally don’t fluctuate a lot continues to rise, up 6.1% in August on a 12-month basis and 7.7% on a one-month annualized basis.

Nor is Zentner alone in that sentiment.

Citigroup economist Andrew Hollenhorst also sees upside risk to the funds rate.

“Despite the dramatic upward revisions to policy rate projections, risks remain skewed to the upside: It is much easier to see scenarios where policy rates reach above 5% than where the cycle terminates below 4%,” he said in a note dated Sunday.

The funds rate hasn’t been above 5% since August 2007, according to Fed data.

Those expectations for higher rates are causing Wall Street economists to rethink their projections for growth.

Near term, Zentner cut her third-quarter outlook for gross domestic product to 0.8%, from 1%. That dovetails with the Atlanta Fed’s GDPNow tracker, which in its latest update last week is now pointing to just 0.5% growth in Q3.

Goldman Sachs also has raised its expectations for rate hikes this year, though it still sees a terminal rate in the 4%-4.25% range. The bank, however, cut its GDP outlook for 2023 to 1.1% from 1.5%.

As long as the jobs market remains strong and the economy avoids slipping into a deep recession, the Fed is likely to keep raising rates until it sees real progress on inflation, Zentner said.

“Thus far, higher rates have inflicted little widespread pain on the real economy, so the Fed has room to continue hiking into restrictive territory,” the Morgan Stanley economist said. “Bottom line is that the Fed needs more evidence that its actions are taking a bite out of the real economy.”

Three reasons why JPMorgan’s Kolanovic believes market downside is limited from here

JPMorgan’s Marko Kolanovic believes the market sell-off won’t get much worse than this as Wall Street’s top strategist found three big reasons to stay optimistic.

Fears of aggressive rate hikes prompted investors to dump risk assets, especially growth stocks in recent weeks. The S&P 500 dropped 4.8% last week, its worst weekly performance since June. Many notable investors including Jeffrey Gundlach and Scott Minerd have been projecting a 20% decline in the S&P 500 by mid-October.

Still, Kolanovic, one of the biggest bulls on Wall Street, reassured his clients that downside should be limited because of resilient earnings, low positioning and anchored inflation expectations.

“While more hawkish central bank pricing and the resulting increase in real yields is weighing on risk assets, we also believe that any downside from here would be limited given: 1) better than expected earnings growth and signs revisions may be bottoming,” Kolavovic said in a Monday note. “2) very low retail and institutional investor positioning, and 3) declines in longer term inflation expectations from both survey- and market-based measures.”

The Federal Reserve is expected to approve a third consecutive 0.75 percentage point interest rate increase this week, which would take benchmark rates up to a range of 3%-3.25%.

Kolanovic gained a wide following after correctly calling the March 2020 market bottom and the subsequent rebound during the pandemic. He was promoted to chief global markets strategist from the bank’s head of macro quantitative and derivatives strategy in 2021.

The strategist believes that high inflation and robust nominal GDP growth are cushioning nominal earnings growth in an environment of low real growth. Meanwhile, retail and institutional investors are poised to add back equities after being underweight for a few months, Kolanovic said.

“We thus remain cautiously optimistic and continue to combine a sizeable equity overweight in our model portfolio with a credit underweight as a hedge,” he said. “We stay long the dollar as a hedge to a hawkish Fed and see significant upside on commodities from here.”

—CNBC’s Michael Bloom contributed to this report.

Fed meeting ahead will decide whether stocks can stabilize or fall back to bear market lows

Patti Domm@IN/PATTI-DOMM-9224884/@PATTIDOMM

The Federal Reserve is expected to raise interest rates by another three-quarters of a point Wednesday, but it is what it signals about future rate hikes that will drive markets.

The central bank’s two-day meeting Tuesday and Wednesday comes in a week where investors will also be on high alert for more guidance about corporate earnings ahead of the next reporting season in October. FedEx rattled the market after it withdrew its full year earnings guidance Thursday, warning about global softness in its delivery business.

Stocks were sharply lower on the week, with the S&P 500 ending at 3,873, a decline of 4.8% and its worst week since June.

The stock market’s tone soured dramatically after Tuesday’s release of the consumer price index, which showed inflation to be hotter and more pervasive than expected in August. A multi-day rally came to an abrupt halt, and the Dow lost 1,276 points, or almost 4%, in the worst stock market day since June, 2020.

After the CPI, markets shifted to price in an even more aggressive Fed rate hiking path. That accelerated the wild ride higher in shorter duration Treasury yields, which pulled funds to fixed income investments as investors jumped on yield levels not seen since 2007.

“When you can get 4% yield in the front end of the yield curve that’s an attractive alternative,” said Jack Ablin, chief investment officer at Cresset Capital. “The bond market had been competing for capital with both hands tied behind its back. Now it’s not.”

Fed ahead

In the week ahead, there are just a few data releases, but they will provide an important window into how the housing market has been coping with the Fed’s rate hiking cycle. August housing starts are Tuesday and existing home sales are Wednesday, and the data is expected to show slowing as mortgage rates rose.

“The problem with that is it’s a ‘heads I win, tails you lose,’” said Art Hogan, chief investment strategist at National Securities. “Good economic data has been bad for the market, but we haven’t seen bad economic data be good for markets. Maybe we’ll flip the switch on that if you see enough of a drawdown in the housing data.” He said that would mean the Fed’s rate hikes are slowing the economy, as intended.

Strategists say the most important information investors are looking for from the Federal Reserve will be what’s on the dot plot, the Fed’s so-called interest rate forecast.

After the CPI release, the futures market for fed funds priced a big jump higher in the terminal rate, or end point where the Fed stops hiking. It had been pricing in a 4% terminal rate by April.

“It’s now effectively an upper bound of 4.50%,” said Ben Jeffery, fixed income strategist at BMO. “The potential shock that we could see on Wednesday could be in the dot plot, not in the size of the rate hike.” The market is also pricing in a slight chance of a 100 basis point hike, but most economists expect a third 75 basis point increase instead. [A basis point equals 0.1%]

Hogan said the stock market has been “freaking out over every tick higher in the 2-year yield,” which rose above 3.9% Friday.

“The 2-year is really an expression of what we think the terminal rate is, and that’s why it’s moving up so aggressively,” he said. “All of that said, it’s really hard to be in a market place where good news on the economic data is bad and bad data is bad as well, and the only thing we can lean against is an improvement in readings on inflation. We fall into the category of it’s hard to find a positive catalyst in the near-term.”

The next key inflation report is the PCE deflator, which is in the personal consumption expenditure data, due out Sept. 30. That inflation measure is closely watched by the Fed. The next CPI report is expected Oct. 13.

Earnings and warnings

There are also a handful of earnings in the week ahead, including General Mills and homebuilders KB Home and Lennar Wednesday, and Costco on Thursday.

“If you look at earnings weekly upgrades versus downgrades, it’s kind of flat,” said Ablin. “Companies have an open ended invitation, every excuse in the book to reduce expectations. I think we will see earnings declines, but a lot of it is really foreign. The FedEx announcement was really about China and Europe.”

General Electric also warned on Thursday that supply chain disruptions could impact its cash flow forecast.

Ablin said he expects to hear more warnings from multinationals, particularly from companies with a lot of dollar exposure. Foreign sales are worth less as the dollar rises.

“We still have a full weighting in small caps. That should benefit small caps and companies that do most of their business domestically,” he said.

The dollar index has been trading at a 20-year high, and the euro was trading at par with the dollar Friday but has been slipping below $1.

“What I’m really watching for is a rolling over of the dollar,” said Ablin. “Once investors sense light at the end of the tightening tunnel, we’ll see the dollar roll over and to me that’s an indication that it’s safe to get into the equity market, and we’ll see foreign stocks lead the way higher.”

Technically speaking

Strategists who follow charts have been monitoring the S&P 500 closely, to see if it breaks below 3,800. That level could open the door to a test of the June low, at 3,636.

The last two weeks of September are about as bad as it gets for stocks. The month of September into early October is the worst period for the S&P 500.

“This is the bad part of September. That’s the bad part,” said Hogan. “What’s the good news is that we’re in a mid-term election cycle so the last two months of the year are generally positive.”

Week ahead calendar

Monday

Earnings: Autozone

10:00 a.m. NAHB survey

Tuesday

Earnings: Stitch Fix, Aurora Cannabis

FOMC begins two-day meeting

8:30 a.m. Housing starts

8:30 a.m. Building permits

Wednesday

Earnings: Lennar, KB Homes, General Mills, Steelcase, Trip.com

10:00 a.m. Existing home sales

2:00 p.m. FOMC statement

2:30 p.m. Fed Chairman Jerome Powell briefing

Thursday

Earnings: Costco, Darden Restaurants, Accenture, FactSet, Manchester United

8:30 a.m. Initial claims

8:30 a.m. Current account Q2

10:00 a.m. Leading index

Friday

9:45 a.m. Manufacturing PMI

9:45 a.m. Services PMI

HI Financial Services Mid-Week 06-24-2014