And this to shall pass When Donald J Trump announces he’s basically done bombing the military infrastructure

Did we take out the son and who’s in charge now?

That this war was the most orderly bearish movement I’ve ever seen

Tech Pattern = Down 1.5 – 2% overnight, 1%+ downward open and then we recovered throughout the day

MISTAKES = Adding puts immediately for a high volatility expense and then taking them off the last hour

Selling and then buying back at a higher price

Buying bullish credit spreads 30 days out.

Prudent option play was selling calls ITM, DITM or ATM

Let’s go over positions by looking at charts and going over what we have in place.

AAPL we had short calls and then rolled to 17April $285

BA puts 2April $230

DIS 20Mar $110 Covered calls

GOOGL 17April $340 CC

JPM 10 April $295 and we had 27Feb $320 CC rolled to 20 Mar $320

Key – 20Mar $22 Puts

META – 20Mar $685 Puts, 17April750 CC

META spreads we had the short side what we might be looking to take off for HUGE Profits

MU – Spreads to take off short side soon

NVDA 27Mar190 Puts we took off

PLTR – Puts through earnings and took them off

The hardest part of the last three weeks was finding credits to roll to after the war started

Even when we miss the S&P 500 – 0.62 we don’t start making up new rules, we don’t start a new investing mryhodology, we don’t quit and sell it al off because we would miss the bounce, We REEVAULATE !!!!

Earnings

DG 03/12 BMO

MU 03/18 est

https://www.briefing.com/the-big-picture

The Big Picture

Last Updated: 27-Feb-26 12:35 ET | Archive

AI uncertainty to cap multiple expansion

Briefing.com Summary:

*Markets are struggling to price AI’s long-term impact, creating volatility and delaying broad-based confidence in future earnings durability.

*Earnings growth remains strong, but surprise levels haven’t been as strong.

*Companies across industries must prove AI enhances profitability rather than disrupts business models and compresses profit margins.

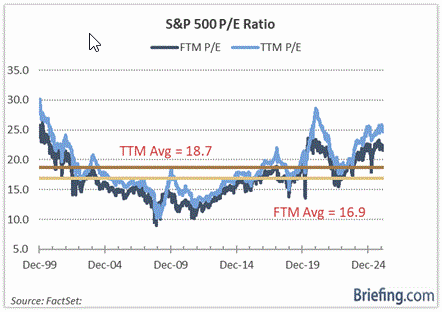

We are going to share a story about valuation. It is going to begin with a picture and end with a twist.

Multiple Compression

We have seen some multiple compression to begin the year thanks largely to a rollback in many of the mega-cap stocks. Specifically, the S&P 500 entered 2026 trading at 22.1x forward twelve-month earnings and 25.4x trailing twelve-month earnings. Today, those P/E multiples sit restlessly at 21.8x and 25.1x, respectively.

In other words, they haven’t come down that much and are still stretched appreciably relative to averages covering the period from 2000 to present. Another interesting consideration is that the multiple compression stems from earnings growth rising faster than prices.

The S&P 500 is up 0.2% year-to-date versus a 3.0% increase for the forward twelve-month estimate and a 3.2% increase for the trailing twelve-month estimate. On the plus side, these things are all moving in the right direction, but on the downside, the existing stretched valuations are standing in the way of multiple expansion.

Said another way, the good earnings news has been mostly priced in. That is partly why a stock like NVIDIA (NVDA) would trade down 5.5% after the AI leader reported quarterly revenue up 73% year-over-year, a non-GAAP gross margin of 75.2%, and adjusted diluted EPS up 82% year-over-year.

Positive Feedback Loop

There were other factors involved with NVIDIA’s post-report decline, as was the case with Amazon’s (AMZN) post-report decline, Microsoft’s (MSFT) post-report decline, and declines in many stocks, either immediately after their reports or in subsequent weeks, like in the cases of Meta Platforms (META), Tesla (TSLA), and Alphabet (GOOG/GOOGL).

The hangup for NVIDIA is that its results were too good. Investors appeared skeptical that NVIDIA could continue to deliver the same monstrous growth as it contends with the law of large numbers, budding competition, and a potential scaling back of capex budgets by the hyperscalers.

Ironically, hyperscalers faced investor backlash for investing too much in their AI buildout plans without a quantifiable pathway to meaningful returns on their investment. At this point, it is a bill of sale that the returns will be there eventually. Other companies, meanwhile, got pummeled on the notion that their business models, cash flows, and earnings prospects will be weakened by the rise of AI models, tools, and agents borne out of the heavy investment in AI.

This positive feedback loop has thrown the market for a loop to begin the year, never mind that each of the major indices is higher year-to-date.

The fact that the consumer staples sector has outperformed the information technology sector by nearly 2100 basis points year-to-date and the financial sector by nearly 2300 basis points, that the 10-yr note yield has declined 20 basis points, and that the CBOE Volatility Index is up 34% underscores how loopy the stock market has been even though the earnings growth, in aggregate, has been better than expected… or has it?

The S&P 500 is on pace for its fifth consecutive quarter of double-digit earnings growth. According to FactSet, companies, in aggregate, have reported earnings 7.2% above expectations, but here is the relative rub: that is below the one-year average of 7.4% and the five-year average of 7.7%.

In short, the fourth-quarter earnings reporting has been good, as expected. It just hasn’t been as good as past periods from a surprise perspective, so it hasn’t led to multiple expansion.

Briefing.com Analyst Insight

When you have a rich valuation, it gets harder to provide a true positive surprise. The reason being is that the rich valuation is a byproduct of investors frontrunning the expected good earnings news, so much so that by the time the good earnings news arrives, it is already in the stock price (and then some).

It gets even harder, though, when doubts emerge about being able to follow through quarter after quarter with impressive earnings results. That is the predicament the mega-cap stocks find themselves in, and the predicament many other industries are facing with respect to being disrupted by AI advancements.

That is why the market cap-weighted S&P 500, anyway, has been range-bound since October even though the forward twelve-month earnings estimate has continued to be revised higher.

The hyperscalers are going to have to prove that they are getting meaningful returns on their massive AI investments. Hardware companies that need memory are going to have to prove that the spike in memory costs is not adversely impacting their profit margins. Software companies are going to have to prove that they aren’t being disintermediated by AI tools. The same goes for logistics companies and financial services firms, and right on down the line.

AI is a change agent, but it is unclear to what degree for just about every business out there. It will be better for some than others, but every publicly traded company is a show-me story now.

How long it takes to convince investors that AI is a change agent for the better is the great unknown. That uncertainty will be a headwind for multiple expansion, certainly at the index level, which is dictated by the behavior of the mega-cap stocks, but it will infiltrate (and already has) other industry groups.

It will take some patience to watch things get sorted out. We expect many twists and turns along the way. We just don’t expect any significant multiple expansion at this juncture when the AI plot twist has thickened.

—Patrick J. O’Hare, Briefing.com

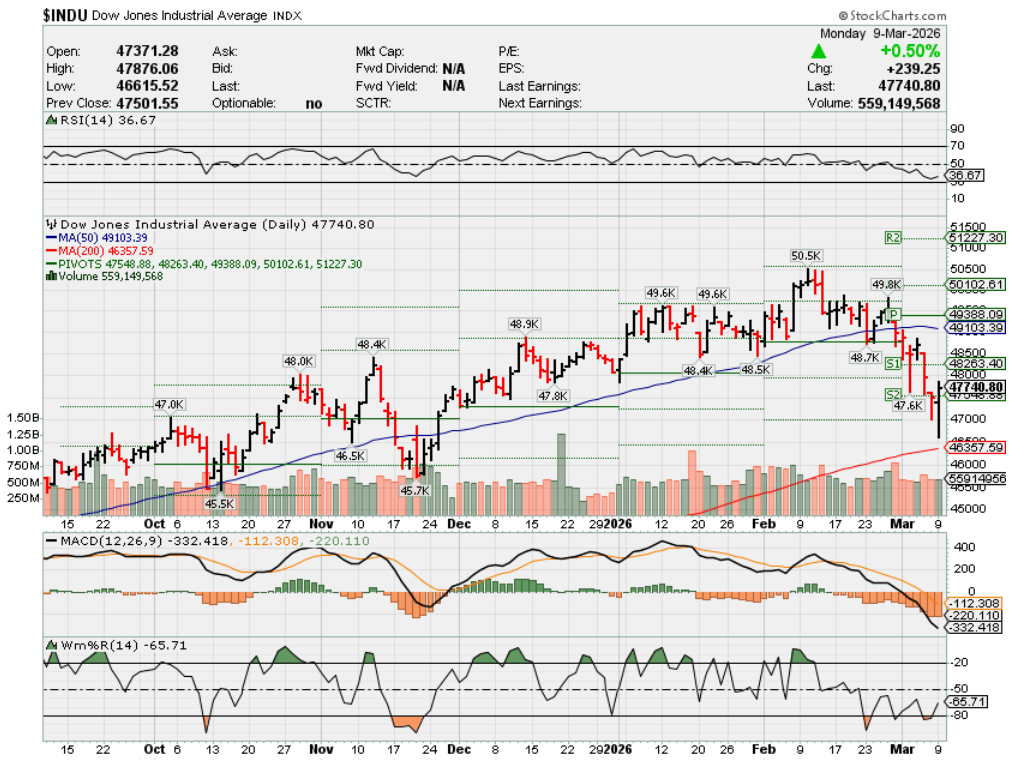

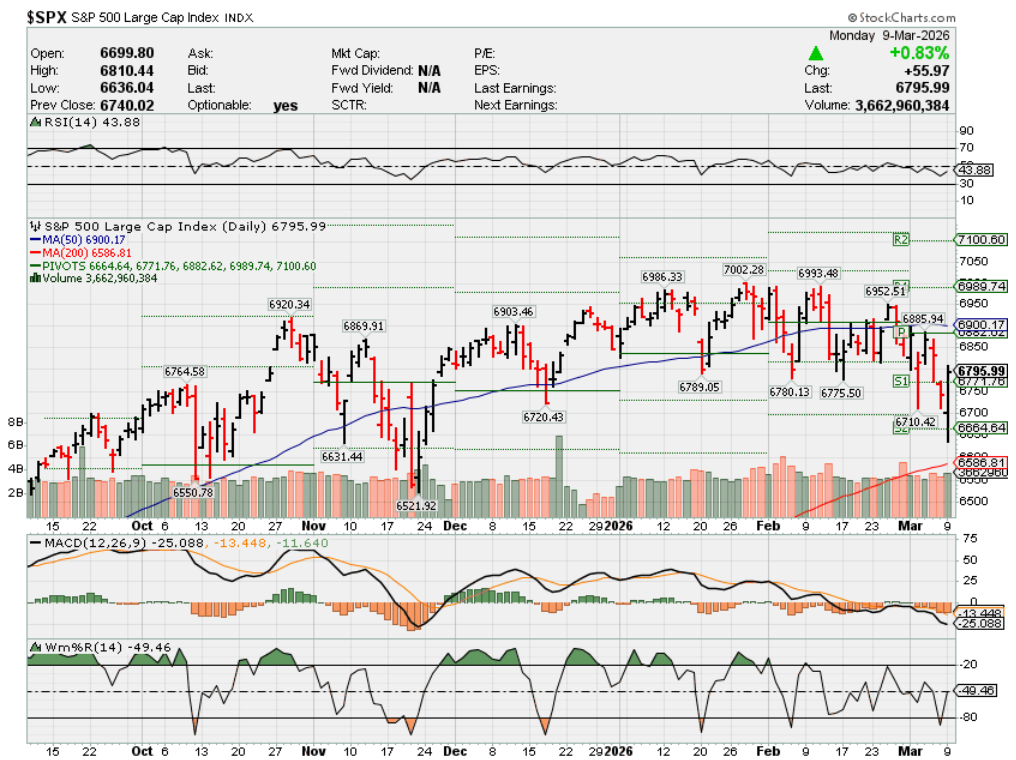

Where will our markets end this week?

Lower

DJIA – Bearish

SPX – Bearish

COMP – Bearish

Where Will the SPX end March 2026?

03-09-2026 -2.0%

03-02-2026 -2.0%

Earnings:

Mon: HPE, MTN

Tues: KSS, ORCL,

Wed: BMBL,

Thur: DKS, DG, LI, ADBE, LEN, ULTA

Fri: BKE,

Econ Reports:

Mon:

Tue Existing Home Sales,

Wed: MBA, CPI, Core CPI, Treasury Budget

Thur: Initial Claims, Continuing Claims, Housing Starts, Building Permits, Factory Orders,

Fri: Michigan Sentiment, Durable Goods, Durable ex-trans, Personal Income, Personal Spending, PCE Prices, PCE Core, GDP, GDP Deflator,

How am I looking to trade?

Protection and still holding onto cash we raised end of last year/beginning of this year

www.myhurleyinvestment.com = Blogsite

info@hurleyinvestments.com = Email

Questions???

Looking for bargains in stock prices, taking CC credit off the table, taking the short side of leap bulls calls off

Maybe Dollar cost averaging the long side of leap bull calls ???

Why Fixed Income No Longer Means What Retirees Think It Does

David Beren

Mon, February 23, 2026 at 8:20 AM MST

For as long as most of us can remember, “fixed income” has meant the same thing to retirees, and it generally appears in the form of safe and predictable bonds that pay out steady interest, all while allowing the preservation of capital. If you bought a 10-year Treasury or corporate bond ladder, you could collect coupons and never worry about principal.

Quick Read

- Bond portfolios dropped 20% in 2022 as rates climbed. This broke traditional fixed income safety assumptions.

- A 4.06% Treasury yield minus 2.4% inflation equals 1.5% real return before taxes are applied.

- Stock-bond correlation turned positive in 2022. The 60/40 portfolio lost its diversification protection.

- A recent study identified one single habit that doubled Americans’ retirement savings and moved retirement from dream, to reality.

As far as a retiree looked at everything, their income was fixed, risk was low, and the strategy, albeit boring, was the best possible scenario. Unfortunately, this same scenario is the one many retirees still envision, and it’s dangerously out of date thanks to the bond market in 2022 shattering any such assumptions.

Retirees who had previously purchased bonds expecting them to hold to maturity and collect steady income watched as portfolio values dropped by as much as 20%, if not more, as rates climbed. The income itself might have stayed fixed, but purchasing power did not, and in this case, “fixed income” became a very real loss.

Inflation Broke the Fixed Income Promise

The biggest issue of all for retirees may be that even when bond yields look attractive, inflation has a nasty way of eating up much of what you are actually earning. A 10-year treasury earning 4.06% in mid-February 2026 might sound great, at least until you learn that inflation is holding around 2.4%, which means that the real return you are actually earning is only 1.5%.

Of course, this 1.5% comes before taxes, which takes another chunk out of the money, and after you account for both state and federal taxes, depending on where you live, some retirees could be earning close to zero in real terms.

The hope was that Treasury Inflation-Protected Securities (TIPS) were supposed to solve this problem, but they have their own set of issues. TIPS provide inflation protection, but their yields are lower and hover around 2.46%, depending on maturity. This is better than losing money to inflation, but it’s not the kind of income a retiree can count on to fund the golden years.

The Diversification Myth Collapsed

Retirees who came into retirement with the 60/40 portfolio split in mind, something of a default level driven by good financial planning, worked well because stocks and bonds would move in opposite directions. Whenever equities fell, bonds would rally, which in turn would help smooth out portfolio returns and reduce volatility.

This negative correlation was the entire foundation of why diversification has become such a big deal if you are invested. This entire concept disappeared in 2022 when the stock-bond correlation turned positive, and since then, bonds have lost more money as stocks declined.

Any idea that bonds would provide safety during stock market downturns has all disappeared. The truth is that the 60/40 portfolio split didn’t just underperform, it failed at the very job it was designed to do, and that is to protect capital when equities stumbled.

What Fixed Income Actually Means Now

If traditional bonds no longer deliver what retirees need, the definition of “fixed income” now has to expand. Income-focused strategies now have to include dividend-paying stocks, REITs, preferred stocks, and even covered call ETFs, depending on your risk comfort.

These assets generate regular cash flow, but they are not bonds, and they do carry different risk levels. The trade-off is that many of them offer yields in the 5% to 9% range, well above what investment-grade bonds provide, and some even have built-in inflation protection through dividend growth.

Enterprise Product Partners (NYSE:EPD), for example, offers a 5.99% yield, which is backed by fee-based revenue from energy infrastructure. Realty Income (NYSE:O) pays 4.87% with 22 years of dividend increases. The JPMorgan Equity Premium Income ETF (NYSE:JEPI) pays 8.00% through a combination of dividends and covered call premiums. None of these are bonds, but they function as revenue generators that someone can use to replace traditional fixed income or complement it.

The New Fixed Income Portfolio

Building a retirement income strategy in 2026 means having to rethink what belongs in the “fixed income” bucket. Short-term investment-grade bonds still have a place for both stability and liquidity, especially if you can find them at over 4%, and TIPS provides inflation protection. However, the bulk of income generation is now going to increasingly come from more diversified sources like dividend growth stocks for companies that have strong cash flow, REITs for monthly income tied to real estate, MLPs for energy infrastructure distributions, and bond alternatives like preferred stocks.

The goal isn’t to abandon bonds entirely, only to stop relying on them as the only source of fixed income. In 2026, one recommendation for a retiree who needs $50,000 annually might be to invest 20% in short-term bonds for stability, 30% to dividend-paying blue chips, and REITs for income, 30% to high-yield alternatives like covered call ETFs or MLPs, and another 20% to equities that can provide long-term growth.

Why This Matters for Retirees

The phrase “fixed income” still carries some psychological weight for retirees because it once implied safety. The 2026 bond market just cannot safely deliver on that anymore, as volatility is higher, real yields are lower, and the diversification benefits have weakened. Retirees who are clinging to old definitions are either accepting returns that don’t keep up with inflation or taking on more risk than they might be aware of. Today, shifts in investment strategy are not about taking on unnecessary risk, but more about recognizing that the income landscape has changed and adapting to it.

Data Shows One Habit Doubles American’s Savings And Boosts Retirement

Most Americans drastically underestimate how much they need to retire and overestimate how prepared they are. But data shows that people with one habit have more than double the savings of those who don’t.

And no, it’s got nothing to do with increasing your income, savings, clipping coupons, or even cutting back on your lifestyle. It’s much more straightforward (and powerful) than any of that. Frankly, it’s shocking more people don’t adopt the habit given how easy it is.

Michael Burry sees Nvidia ‘purchase commitment’ parallel to Cisco at dot-com bubble top

Published Thu, Feb 26 202610:14 AM ESTUpdated Thu, Feb 26 20262:53 PM EST

Michael Burry of “The Big Short” fame is doubling down on his bearish thesis on Nvidia, raising red flags on a line item in the chipmaker’s latest earnings report that echoes a pattern seen at the height of the dot-com bubble in the late 1990s.

Burry, in a Thursday Substack newsletter, pointed to a surge in Nvidia purchase obligations, which climbed to $95.2 billion from $16.1 billion a year earlier. Total supply obligations, including inventory and purchase agreements, now stand at roughly $117 billion, nearly matching Nvidia’s annual operating cash flow.

On the company’s fiscal fourth quarter earnings call Wednesday, Chief Financial Officer Colette Kress said inventory rose 8% quarter over quarter and that Nvidia had “strategically secured inventory and capacity to meet beyond the next several quarters, further out in time than usual.”

For Burry, Nvidia’s comments suggest that the largest public company in the United States is committing to buy large amounts of supply before it knows exactly the strength of future demand. That means more cash is tied up in inventory for longer periods.

‘Not temporary’

“What is happening now is not temporary. It is no export shock. It is not even external. This is coming from within the business plan,” he wrote. “This new reality reflects a deliberate decision to lock up supply chain capacity further than Nvidia has ever done before.”

The noted investor compares the current situation to that of Cisco Systems during the height of the dot-com boom in the late 1990s and the early 2000s.

In 2000 and 2001, Cisco secured large supply commitments to support expectations of rapid growth. When corporate technology spending suddenly tumbled, Cisco was left with excess inventory and contractual obligations it couldn’t use. The company ultimately had to write down billions of dollars, and its stock plunged.

“This is not business as usual. This is risk,” Burry said of Nvidia. “Back in 2000-2001, Cisco extended purchase commitments with its suppliers to ensure capacity for that 50% annual growth Cisco expected,” he said.

To be sure, Nvidia’s profit margins, now above 70%, are higher than Cisco’s were at the time, which could provide some downside protection, the investor noted. But Burry believes those margins have been boosted by unusually strong demand and Nvidia’s ability to raise prices.

“That type of margin would likely revert quickly with a shift in demand,” he wrote.

Addressing concerns

Still, not everyone sees the buildup as a warning sign. Analysts at Rosenblatt Securities said management addressed multiple investor concerns during the quarter, including GPU capacity, competition from custom chips, power availability, memory supply and customer financing.

“We view this as a confident management team that will support customer demand for its next generation platforms and continue to lead the AI market development,” Rosenblatt analysts wrote in a note to clients.

The Wall Street firm on Thursday lifted its 12-month price target on Nvidia to $300 from $245, which implies upside of more than 50% over the next year.

Nvidia was near session lows, off almost 4% in early trading Thursday. The stock is higher by less than 1% so far in 2026, after soaring in 2023-2025 following the introduction of ChatGPT.

Will Iran war fallout end the bull market? When investors really need to worry

Published Sat, Mar 7 20268:41 AM EST

If oil trades above $100 a barrel for a while, the U.S. economy could be in for major shocks, according to Bank of America.

Oil prices have surged since the U.S.-Israeli strikes on Iran last weekend, with West Texas Intermediate futures posting their biggest ever weekly gain, soaring 35%. The benchmark U.S. crude closed at $90.90 a barrel on Friday, close to the level that BofA global economist Claudio Irigoyen said will prompt “non-linear” effects in the economy.

“If the status quo persists … we would fade (oil induced) inflation concerns,” Irigoyen wrote to clients in a report on Friday. “But an escalation driving oil prices persistently above $100 would become more concerning.”

West Texas Intermediate oil over the past five days.

The economy is “more sensitive than usual to markets” because higher-income consumers are driving spending, Irigoyen said. This group is more likely to hold stocks, whose surge in recent years has helped buoy confidence and encourage spending.

Cooler spending

A sustained stock market downturn as a result of rising oil prices could push higher-income consumers to cool their spending, exacerbating the economic shock, Irigoyen said.

Lower-income consumers will take an even harder hit as gasoline prices rise, the economist said. The average cost of a gallon of gas nationally rose the most in three days since 2008, according to a Bespoke Investment Group analysis of AAA data. An average gallon of gas in the U.S. hit $3.25 on Thursday, 27 cents higher than the week before, the U.S. travel organization said.

Households at the lower end of the income spectrum “are already struggling, so further erosion of their real spending power from surging energy prices could cause another leg up in delinquencies,” Irigoyen said of credit card and car loans and other types of fixed payments. “In turn, this could have a lasting impact on their ability to spend, if it constrains their access to credit.”

More expensive energy could also create “a bottleneck” for artificial intelligence capital spending, Irigoyen said.

Bank of America’s forecast for gross domestic product includes a tailwind from AI-related investment, such as the data center buildouts planned by the largest technology companies, like Microsoft and Google-parent Alphabet. But if any of those projects are delayed as a result of energy price increases, the economist said that would prove a headwind for growth this year.Ultimately, Irigoyen said if oil saw a sustained move above $100 per barrel, it would probably shave more than 0.60 of a percentage point off GDP growth. If oil prices doubled, a recession would likely ensue, he said.