A Registered Investment Adviser

HI Market View Commentary 01-22-2024

Lesson #2

Averages Are NOT your friends !!!

Averages vs Portfolio Growth

IF you average 50% return in year 1 and then a 50% loss in year 2, what is the average return?= 0%

BUT does a 0% return equal your portfolio got back to break even?

$1.00 x 1.5 = $1.50 but then $1.50 minus a 50% loss = $0.75

$1.00 x 0.5 = $0.50 but then you make 50% or 1.50 =$0.75

Portfolio growth is down 25%

Annualized returns = Hurley Investments last week we had 100% returns in all trades

We also annulized our first Trade Findings and Adjustments trade = Long Puts on BA

How many minutes were in the trade= 30 minutes

$9.45 – $8.20 = 1.25 profit / 8.20= 15.24% ROI per every contract $125

How many half hours are there in a single 7.5 hour trading day ?= 15

15 * 15.24% ROI = 228.6% Daily return

228.6 * 5 trading days of the week = 1,143% Weekly ROI

1,143% Weekly ROI * 52 weeks in year = 59,436% ROI Annualized Return

40 successful PIP trades and have the 41st be a loser and give up EVERTHING you gained in he previous 40 winners

https://www.briefing.com/the-big-picture

Last Updated: 11-Jan-24 16:21 ET | Archive

Q4 earnings bar is low, but valuation hurdle is high

It is a new year, and a new year in the stock market always starts with a look back at the fourth quarter. That would be fourth quarter earnings, which are going to start trickling out in a steady fashion starting Friday, January 12, and continuing, yes, through March.

This earnings season gets dragged out with fiscal year-end reporting, so much so that the first quarter earnings season starts almost as soon as the fourth quarter reporting period ends.

For those of us covering the earnings announcements, that is our quantitative misfortune. For everyone else, though, it will be a fortune of fundamental news that will shape investment views. That’s no small consideration for a market high on 2024 earnings prospects.

Looky Here

Every earnings reporting period is a look back, but the market is more interested in the look ahead.

A lot of companies don’t provide guidance, but the market makes its inferences nonetheless from the qualitative remarks about business conditions and the tone CEOs and CFOs adopt on their earnings conference calls.

That will be true of the banks, which get things rolling in the early portion of the reporting season. Bank of America (BAC), BNY Mellon (BK), Citigroup (C), JPMorgan Chase (JPM) and Wells Fargo (WFC) will all report their results before the open on Friday, January 12.

These reports will have extra importance this period, because the market has a lot riding on the U.S. economy achieving a soft landing — or no landing at all. The banks have a front row seat to economic activity. In fact, they do the driving in many respects as the issuers of credit, the purveyors of capital, and the stewards of assets.

There will be a lot of interest, then, in what these banks and other banks say about credit quality, deposit flows, asset values, regulatory constraints, and investment banking activity.

The focal point will likely be comments about credit quality since that will be looked at as a harbinger of economic conditions. If there is concerning commentary about a deterioration in credit quality, concerns will build about the economy possibly being headed for a hard landing. If the commentary sounds nonplussed about the credit situation, then market participants will continue to embrace the soft-landing view.

A sidebar to all of that is that the banks are expected to be the biggest drag on the financial sector’s earnings in the fourth quarter. According to FactSet, the blended growth rate for the financials sector is -6.2%. The banks, however, have a blended growth rate of -29.3%.

A Disparate View

There isn’t much earnings growth expected for the fourth quarter. The blended growth rate for the S&P 500 sits at just 0.4%, according to FactSet, down from 8.0% on September 30.

What this suggests is that analysts were slashing their earnings estimates during the quarter — a quarter that saw stock prices surge amid expectations that inflation will continue to come down, that the economy will enjoy a soft landing, and that the Fed will soon be cutting rates.

Of course, when earnings estimates go down and stock prices go up, you get multiple expansion. The forward 12-month P/E ratio for the S&P 500 went from 18.0 on September 29 to 19.6 on December 29. The five-year average is 18.9 and the 10-year average is 17.6, according to FactSet.

That has created a disparate view in front of the reports: the earnings reporting bar has been lowered (a lot) while the valuation hurdle has gone up.

In other words, the companies reporting earnings need at least to get over the low bar with their reports, but to get over the high valuation hurdle, they need guidance (preferably quantitative, but qualitative will suffice in certain cases) that isn’t disappointing or doesn’t sound disappointing.

The current FactSet consensus estimate for the first quarter calls for year-over-year earnings growth of 5.6%. For calendar 2024, the bar is much higher at 11.8%.

The Blended View

Turning back to the fourth quarter, the communication services sector, where Alphabet (GOOG), Meta Platforms (META), and Netflix (NFLX) reside, has the highest projected growth rate at 41.3%. Next is the utilities sector (+32.7%) followed by consumer discretionary (+22.4%), information technology (+15.5%), and real estate (+3.6%).

That’s it. The remaining sectors aren’t expected to deliver any earnings growth.

The energy sector is expected to register a 30.4% year-over-year decline in earnings. The materials sector (-21.1%) and the health care (-21.0%) sectors are the next biggest drags followed by financials (-6.2%), industrials (-2.5%), and consumer staples (-0.1%).

These are blended growth estimates, which take into account actual results from companies that have reported and estimates for companies that have not reported. That means these growth estimates will be shifting as the earnings reporting period progresses.

If history is any indication, the shift in aggregate should be higher by at least two percentage points. When the reporting period is over, therefore, there should not be a zero in front of the decimal point as there is now.

Suffice to say, if there is — or worse, if there is a minus sign in front of the first digit — the fourth quarter reporting period can be deemed a true disappointment.

What It All Means

The stock market’s road ahead is paved with good intentions. There is a good inflation outlook; there is a good economic outlook; and there is a great policy outlook in the market’s mind that includes six rate cuts by the end of 2024.

The stock market’s behavior at the end of 2023 certainly made it appear as if those rate cuts won’t be happening for deleterious economic reasons that would undermine the current earnings outlook. No, they will presumably happen on the back of a smooth glide path for inflation driven by a further easing in supply chain pressures.

It is an optimistic view alright, and all anyone can hope for is that it is right. We’ll soon have a line on that thinking when the fourth quarter earnings results trickle in and the quantitative and qualitative earnings guidance starts flowing out.

—Patrick J. O’Hare, Briefing.com

(Editor’s Note: the next installment of The Big Picture will be posted the week of January 22.)

71% of all S&P 500 Companies underperformed the S&P 500 Average last year

61% of all S&P 500 Companies are down yr/yr

Earnings dates:

AAPL 2/01 AMC

AMZN 2/01 AMC

BA 1/31 BMO

BABA 2/21 est

BIDU 2/20 est

COST 3/07

CVS 2/07 AMC

CVX 2/02 BMO

DIS 2/07 AMC

F 2/06 AMC

GM 1/30 BMO

GE 1/23 BMO

GOOGL 1/30 AMC

ISRG 1/23 AMC

KO 2/13 BMO

LMT 1/23 BMO

MA 1/31 BMO

META 2/01 AMC

MRO 2/18 est

MSFT 1/30 AMC

MU 3/30 est

NFLX 1/23 AMC

NVDA 2/21 AMC

PYPL 2/07 AMC

SBUX 1/30 AMC

SIRI 2/01 BMO

SQ 2/21 est

TGT 2/26 est

TSLA 1/24 AMC

UAA 2/06 est

V 1/25 AMC

VZ 1/23 BMO

XOM 2/02 BMO

ZION 1/22 AMC

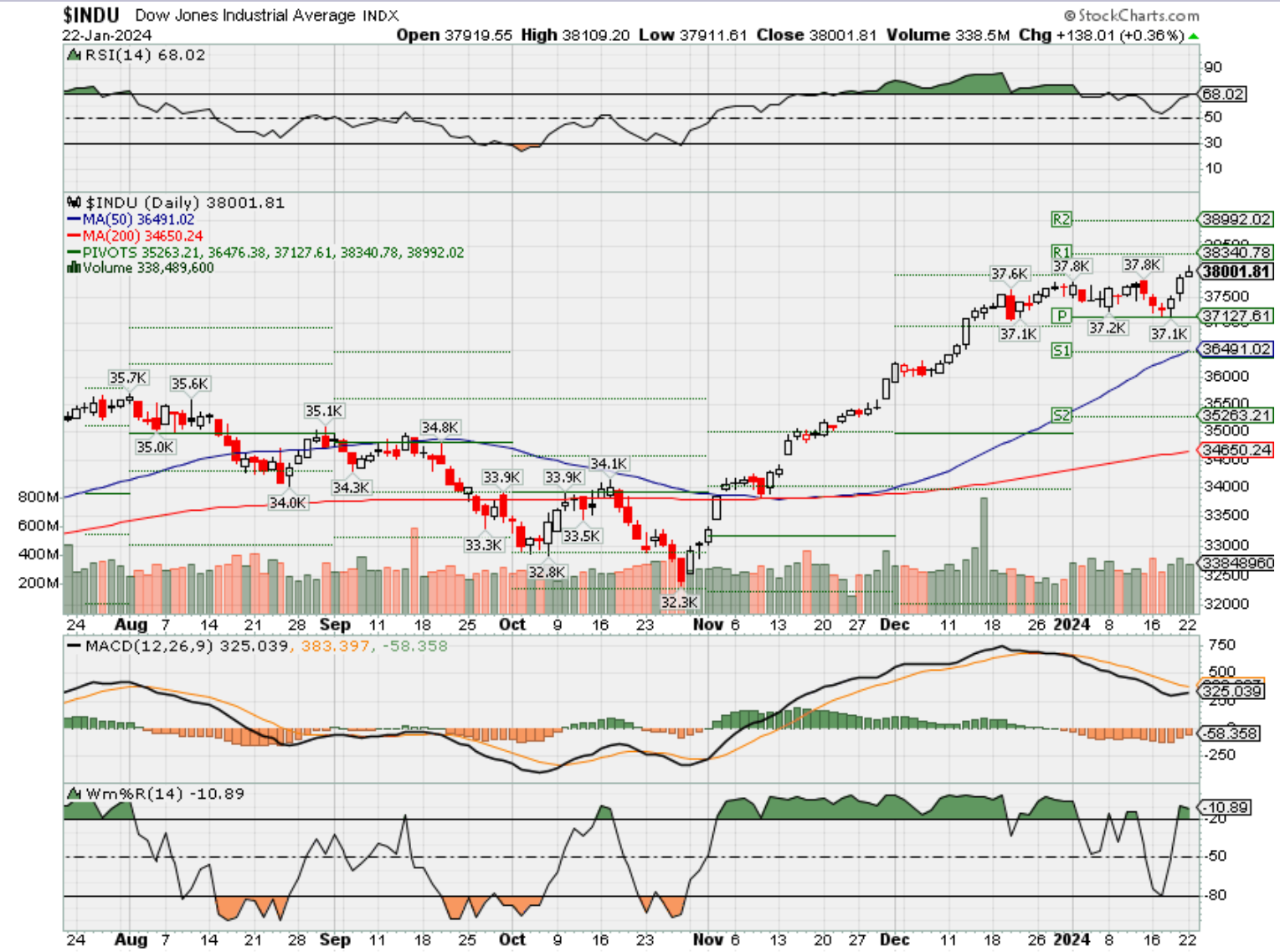

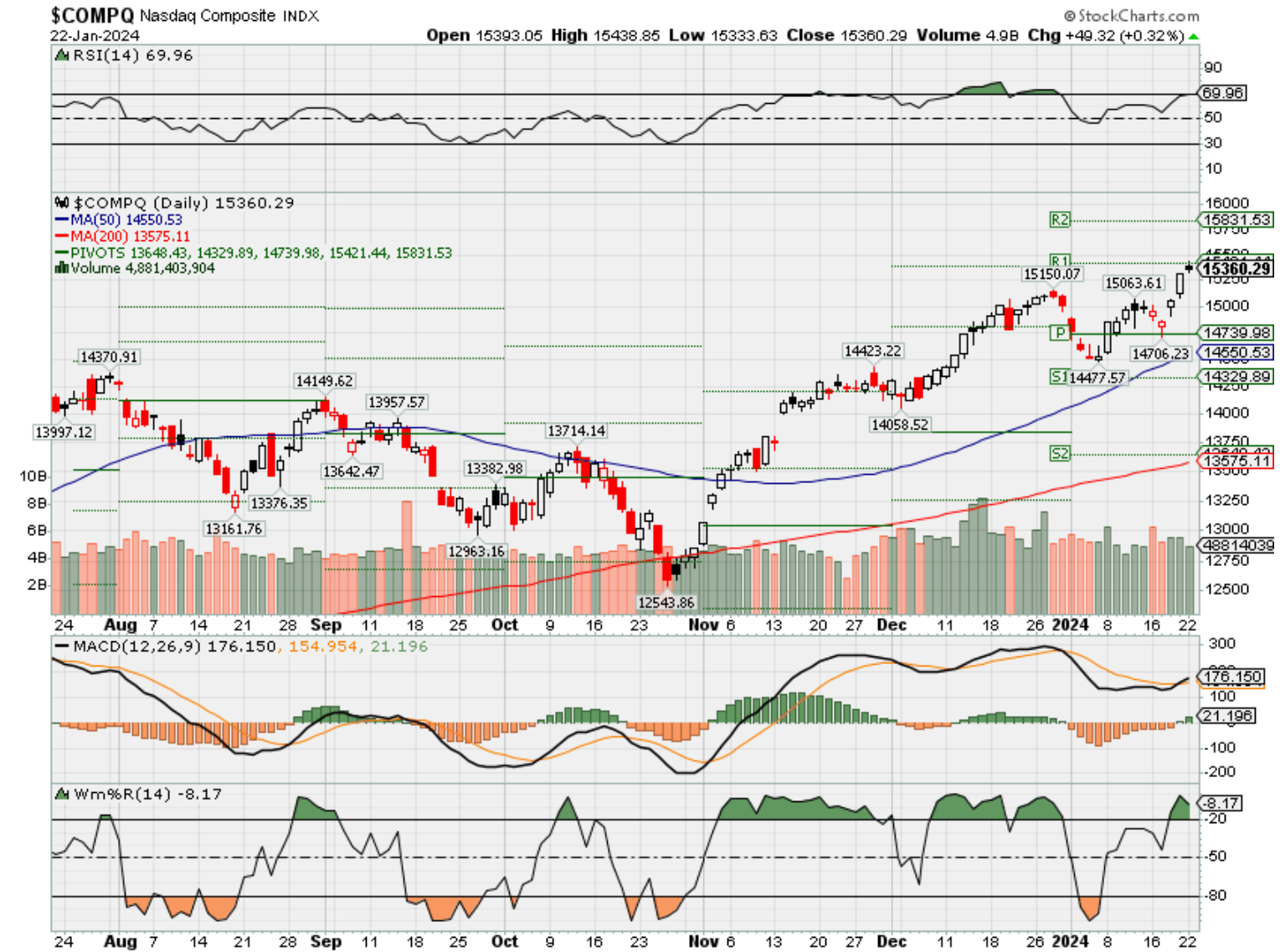

Where will our markets end this week?

Higher

DJIA – Bullish just touching overbought

SPX –Bullish but just touching over-bought

COMP – Bullish just touching overbought

Where Will the SPX end Jan 2024?

Higher

01-22-2024 +3.0%

01-16-2024 +2.5%

01-08-2024 +3.0%

Earnings:

Mon: ZION,

Tues: MMM, DHI, HAL, JNJ, PG, GE, LMT, VZ, ISRG, NFLX

Wed: ABT, FCX, IBM, LVS, TSLA

Thur: ALK, BX, HUM, MUR, LUV, VLO, CPF, INTC, TMUS, V

Fri: ALV, CL

Econ Reports:

Mon: Leading Indicators,

Tue

Wed: MBA,

Thur: Initial Claims, Continuing Claims, Durable Goods, Durable ex-trans, GDP, Chain Deflator, New Home Sales,

Fri: Personal Income, Personal Spending, PCE Prices, Core PCE, Pending home Sales,

How am I looking to trade?

Preparing for earning and may run current long put protection OTM

www.myhurleyinvestment.com = Blogsite

info@hurleyinvestments.com = Email

Questions???

IWM covered call strategy or protective put strategy can be closed for a profit today

https://www.barrons.com/articles/chinese-stocks-cheap-buy-sell-f1df014b?siteid=yhoof2

Chinese Stocks Are Very Cheap. Why Investors Aren’t Jumping In.

Follow

Updated Jan 19, 2024, 9:14 am EST / Original Jan 19, 2024, 1:30 am EST

Chinese stocks keep sinking, hitting the lowest levels since before the pandemic, yet foreign investors are increasingly reluctant to try to take advantage. Hope is fading that Beijing will take stronger measures to bolster the economy or restore confidence among consumers and businesses.

The CSI 300 Index has fallen to its lowest point since January 2019 as investors weigh an unpleasant picture. Data point to a still sputtering post-Covid economic recovery, but there are few indications that policymakers in Beijing are ready to move much beyond the limited stimulus they have already provided. Growing concerns about the international backdrop and domestic policy are only adding to foreign investors’ wariness.

“The recovery from zero-Covid—disappointing though it was—is over,” says Shehzad Qazi, managing director of China Beige Book. Fourth-quarter data from the independent research firm showed that growth in companies’ revenue and profits slowed as the year ended, with few signs of an increase in borrowing despite Beijing’s efforts to prop up the economy.

Expectations for more meaningful stimulus revived investor interest in the fourth quarter, but that appears to be fading. Each uptick in optimism about stimulus is less intense and fades quicker, says Cameron Branch, director of research at EFPR, which tracks fund flows. Interest in Chinese stocks is also becoming more domestically driven, he says.

The MSCI China , down 9% so far this year, is back to the low it reached in October 2022, before China eased the strict restrictions that had strangled the economy during the pandemic. The onshore MSCI China A-shares index has held up only slightly better, with a loss of almost 8% year to date.

A problem for investors is that those declines are unlikely to change Beijing’s tune about stimulus. Not only are foreign investors not significant in the domestic market, they are largely invested in the offshore market dominated by internet companies. And those businesses are out of favor as the government tries to boost areas such as semiconductors and industrials that can aid its efforts to become more self-reliant, Arthur Kroeber, head of research at Gavekal, an investment and research firm based in Hong Kong, tells Barron’s via email.

A second issue is that Chinese businesses remain able to raise capital by issuing equity, perhaps making action appear less urgent to Beijing. The domestic market has been buoyed by roughly 400 initial public offerings on the A-share market last year, with another 800 in the IPO queue.

“Despite lower valuations, they still accounted for 40% of all global IPO fund-raising,” Kroeber says. “The moment they start to care is when bad market sentiment makes it much harder to do IPOs, and as far as I can tell that moment hasn’t arrived yet.”

While Kroeber expects a bit more economic stimulus over the course of the year, largely through infrastructure spending and investment in affordable housing, that likely would only bring inflation-adjusted economic growth to within range of the government’s target of around 5%.

Including deflation, that implies growth of about 4% in nominal terms. According to Kroeber, that is what matters most for stock prices—a reason he expects another poor year for Chinese markets.

A third bearish factor for stocks is that some parts of the economy don’t urgently need help, he says, making it less likely that Beijing will turn to the type of stimulus investors have been wanting. While property investment is still suffering, Kroeber notes that other pockets of the economy are healthier and manufacturing is showing signs of strength at the margin.

“Policymakers look at that kind of data and say, right, things are going the way we want, we just have to ride out the pain in the property sector,” he says.

That pain, though may be around for a while. While Nick Borst, director of China research at the emerging markets-focused investment firm Seafarer Capital Partners, thinks there could be some stabilization in the property market this year, he says the shrinking property sector translates to a huge hole in spending that can’t be filled by Beijing’s increased investment in technology and industrials.

And while much of the concern about the property market has focused on distress among developers, Borst is worried about the fiscal health of local governments. While they have been the main channel for Beijing’s stimulus efforts in the past, they are now hamstrung. Local government financing vehicles owe an estimated $9 trillion, and the land sales government have long relied on to raise cash are drying up because many developers are in financial trouble.

The needed fix, Borst says, is a debt restructuring, along the lines of a 2014 fiscal overhaul that allowed local governments to issue bonds. Though that would be painful for the broader economy, it could help Beijing deal with a persistent cloud over its longer-term growth prospects.

The geopolitical backdrop adds still more reason for caution. As the U.S. election nears, both parties are trying to take a tougher stance on China, giving investors and companies another reason to hold back. For the first time in decades, more foreign capital left China than entered the country last year.

Chief Executive Jamie Dimon was onto something when he said in a CNBC interview this week that the balance of risks and potential rewards in China have “changed dramatically.” Investors appear to be recalibrating their expectations before jumping into one of the cheaper markets around the world.

https://finance.yahoo.com/news/baidu-inc-bidu-trending-stock-140011053.html

Baidu, Inc. (BIDU) Is a Trending Stock: Facts to Know Before Betting on It

January 10, 2024

Baidu Inc. (BIDU) has been one of the most searched-for stocks on Zacks.com lately. So, you might want to look at some of the facts that could shape the stock’s performance in the near term.

Over the past month, shares of this web search company have returned +2.7%, compared to the Zacks S&P 500 composite’s +3.4% change. During this period, the Zacks Internet – Services industry, which Baidu Inc. falls in, has gained 4.2%. The key question now is: What could be the stock’s future direction?

While media releases or rumors about a substantial change in a company’s business prospects usually make its stock ‘trending’ and lead to an immediate price change, there are always some fundamental facts that eventually dominate the buy-and-hold decision-making.

Earnings Estimate Revisions

Here at Zacks, we prioritize appraising the change in the projection of a company’s future earnings over anything else. That’s because we believe the present value of its future stream of earnings is what determines the fair value for its stock.

We essentially look at how sell-side analysts covering the stock are revising their earnings estimates to reflect the impact of the latest business trends. And if earnings estimates go up for a company, the fair value for its stock goes up. A higher fair value than the current market price drives investors’ interest in buying the stock, leading to its price moving higher. This is why empirical research shows a strong correlation between trends in earnings estimate revisions and near-term stock price movements.

Baidu Inc. is expected to post earnings of $2.90 per share for the current quarter, representing a year-over-year change of +31.2%. Over the last 30 days, the Zacks Consensus Estimate remained unchanged.

The consensus earnings estimate of $11.20 for the current fiscal year indicates a year-over-year change of +31.2%. This estimate has remained unchanged over the last 30 days.

For the next fiscal year, the consensus earnings estimate of $13.67 indicates a change of +22.1% from what Baidu Inc. is expected to report a year ago. Over the past month, the estimate has remained unchanged.

With an impressive externally audited track record, our proprietary stock rating tool — the Zacks Rank — is a more conclusive indicator of a stock’s near-term price performance, as it effectively harnesses the power of earnings estimate revisions. The size of the recent change in the consensus estimate, along with three other factors related to earnings estimates, has resulted in a Zacks Rank #3 (Hold) for Baidu Inc.

The chart below shows the evolution of the company’s forward 12-month consensus EPS estimate:

12 Month EPS

Projected Revenue Growth

While earnings growth is arguably the most superior indicator of a company’s financial health, nothing happens as such if a business isn’t able to grow its revenues. After all, it’s nearly impossible for a company to increase its earnings for an extended period without increasing its revenues. So, it’s important to know a company’s potential revenue growth.

In the case of Baidu Inc. the consensus sales estimate of $4.98 billion for the current quarter points to a year-over-year change of +3.9%. The $19 billion and $20.75 billion estimates for the current and next fiscal years indicate changes of +4% and +9.2%, respectively.

Last Reported Results and Surprise History

Baidu Inc. reported revenues of $4.72 billion in the last reported quarter, representing a year-over-year change of +3.2%. EPS of $2.80 for the same period compares with $2.37 a year ago.

Compared to the Zacks Consensus Estimate of $4.65 billion, the reported revenues represent a surprise of +1.5%. The EPS surprise was +14.29%.

The company beat consensus EPS estimates in each of the trailing four quarters. The company topped consensus revenue estimates each time over this period.

Valuation

No investment decision can be efficient without considering a stock’s valuation. Whether a stock’s current price rightly reflects the intrinsic value of the underlying business and the company’s growth prospects is an essential determinant of its future price performance.

Comparing the current value of a company’s valuation multiples, such as its price-to-earnings (P/E), price-to-sales (P/S), and price-to-cash flow (P/CF), to its own historical values helps ascertain whether its stock is fairly valued, overvalued, or undervalued, whereas comparing the company relative to its peers on these parameters gives a good sense of how reasonable its stock price is.

As part of the Zacks Style Scores system, the Zacks Value Style Score (which evaluates both traditional and unconventional valuation metrics) organizes stocks into five groups ranging from A to F (A is better than B; B is better than C; and so on), making it helpful in identifying whether a stock is overvalued, rightly valued, or temporarily undervalued.

Baidu Inc. is graded B on this front, indicating that it is trading at a discount to its peers. Click here to see the values of some of the valuation metrics that have driven this grade.

Conclusion

The facts discussed here and much other information on Zacks.com might help determine whether or not it’s worthwhile paying attention to the market buzz about Baidu Inc. However, its Zacks Rank #3 does suggest that it may perform in line with the broader market in the near term.

1 Artificial Intelligence (AI) Growth Stock Down 68% You’ll Regret Not Buying on the Dip in 2024

By Parkev Tatevosian, CFA – Jan 18, 2024 at 4:06PM

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services. Become a Motley Fool member today to get instant access to our top analyst recommendations, in-depth research, investing resources, and more.

Sen. Mike Lee says he won’t vote yes to fund the government until a border deal is in place

By Gitanjali Poonia, Deseret News | Posted – Jan. 11, 2024 at 9:41 p.m.

Sen. Mike Lee, R-Utah, center, speaks during a news conference on border security and funding on Capitol Hill on Wednesday, as Rep. Cory Mills, R-Fla., right, and Rep. Andrew Ogles, R-Tenn., left, listen in Washington. (Mariam Zuhaib, Associated Press)

WASHINGTON — As Congress considers another short-term spending bill — while working on the 2024 appropriations bills behind closed doors — some Republicans, including Utah Sen. Mike Lee, are making their stance clear: No immigration reform? No government funding.

During a press conference Wednesday, a group of GOP lawmakers — Lee, along with Sen. Rick Scott, R-Fla., Montana Rep. Matt Rosendale, Florida Rep. Cory Mills, Illinois Rep. Mary Miller and others — made it clear that they will use all the tools at their disposal to block funding for the U.S. government, or for foreign military aid, until a border deal is secured.

Lee said that President Joe Biden has the authority to secure the border, but the migrant crisis continues because there’s “a willful desire to not enforce that legislation.”

He pointed to the start of the “uncontrolled wave of illegal migration” of people seeking asylum, which began after Biden took office. The U.S. Customs and Border Protection’s data shows that at least 6 million people have entered the U.S. over the border under the current administration. The agency has released more than 2.3 million migrants into the U.S., as the Washington Post reported.

In December alone, more than 300,000 migrants crossed the border, marking an all-time monthly high in three years. CBS News, which obtained government data, reported that the numbers also showed a record number of families traveling with children.

Lee noted that federal law does not include a “cognizable unconditional right to asylum.” Instead, it is an authority granted to the Secretary of Homeland Security.

He pushed back on the Biden administration’s current catch-and-release process, which is not a part of federal law.

“When you hear (Biden) speak, you will hear him speak in terms that will lead you to think that all this is the inevitable inexorable result of federal law that leaves him no choice but to unleash 10 million illegal immigrants on the American people,” Lee said. “Now this is his choice.”

The Utah senator proposed reinstating the Remain in Mexico policy, implemented during the Trump administration, which requires migrants to wait in Mexico until their asylum court date. He said it would allow the Biden administration to send a clear message to incoming migrants to not come to the U.S., and instead visit a U.S. embassy and figure out other legal options to enter the country.

He recalled working at the U.S.-Mexico border in Texas 30 years ago, before the crisis at the southern border. Lee said he “lived and worked among the poorest of the poor, many of them recent immigrants themselves, some documented some not.”

“No one fears uncontrolled waves of illegal immigration more than the poorest of the poor recent immigrants,” the senator said. “It is their homes, it is their neighborhoods, it is their children’s schools, it is their jobs that are most put at risk by this.”

Lee acknowledged that the U.S. is a country of immigrants. But, he said, it is also a country of laws.

“We can be both. I hope and demand that we always will be,” he said before pressing Biden to shut down the flow of migrants at the border. He also vowed to not aid in funding the government without immigration reform.

Scott said the only way to get a border security deal would be “to hold up whatever we can, whether it’s Ukraine funding, whatever it is they want, and say we don’t get that funding unless we get a secure border,” according to Fox News.

“Otherwise … we’re going to continue to have an open border, ” he said.

Congress faces two fast-approaching deadlines: The first is Jan. 19, when funding for federal programs related to transportation, housing, agriculture, energy, veterans and military construction runs out, followed by Feb. 2, when the stopgap bill balancing other programs, including defense, expires.

House and Senate leadership struck an agreement over a $1.59 trillion top-line for fiscal year 2024 on Sunday. They also made a side deal of roughly $70 million. But, on Tuesday, Republican Senate leadership said a short-term spending bill will be necessary, as the Deseret News reported.

enate Republican Whip John Thune, S.D., said it would be “unrealistic” for Congress to pass the spending package that congressional leaders agreed upon over the weekend before the two fast-approaching deadlines