HI Market View Commentary 12-18-2023

Holidays

Jan 8th, 2024 HI Commentary starts up again

BOTH Christmas and New Years Fall on a Sunday = The following Monday Markets are closed

12/25/2023 & 01/01/2024 markets are closed

Tomorrow is really the last day of ANY volume trading = Retail trades run the show = The Christmas Rally by Definition Dec 26th– Jan 5th is completely up to Retail traders.

Tax Harvesting is real so the first down day should/historically be a doosie !!!!

IF someone says to you paying more taxes is the cost for making money in the stock market has NEVER really made any money in the stock market !!!

IF you are selling for a profit you can buy right back in

IF you are selling for a loss then you have to wait and buy back in 31 days later OR you don’t get the tax loss

Some of you will have two 1099 Misc from Schwab and MoneyBlock

Next Years Expectations (in no particular order)

Elections = There are consequences with either party

Joe Biden is mentally and physically impaired = Who might take his place ????

Trump has it right now on both polls meaning republicans and as a president

That doesn’t mean he might be in jail

Election years are usually on average up 8.5% Stock Market and 7.4% Bond Market

Wars = Ukraine vs Russia to me seems to be leaning towards Russia Winning, Israel vs Gaza seems to be leaning towards a middle eastern war Israel, US, Saudi Arabia vs Gaza, Lebanon, Palestine, Iran, Syria, Yemen, Afghanistan

Volatile OIL and other Commodity pricing

Recession = with a soft landing, that significantly lowers the stock market: >20% but mathematically 31% is the target number and some people are calling for a 50% loss in the stock market

What catalyst would create a 50% loss in the stock market?= Nuclear threat, Rising in inflation leading to no cuts or even a rate hike, Global Recession, Lending/Banking Crisis for the huge amount of loans / restricting of debt coming up in 2024

Next Weeks Expectations= Still moving higher with one or two big down days

Tax Harvesting will be most likely felt on the big 7

https://www.briefing.com/the-big-picture

Last Updated: 15-Dec-23 15:40 ET | Archive

Rate-cut sugar plums dancing in market’s head

Could things have gone any better for the market this past week? If one wants to be literal about it, then, yes, things could have been better, but a fair summation is that this past week was a banner week for the stock market and the Treasury market, which have been kindred spirits since late October.

The equal-weighted S&P 500 is up 4.1% for the week as of this writing, whereas the 2-yr note yield is down 36 basis points for the week to 4.38% and the 10-yr note yield is down 32 basis points for the week to 3.91%.

Don’t look now, but the 2-yr note yield is down four basis points for the year while the 10-yr note yield is just three basis points away from being unchanged for the year.

It has been a stunning turn of events, and it got even more stunning this past week when Fed Chair Powell stunned the markets with some surprisingly dovish-sounding insight into the Fed’s thinking.

All Rolled into One

Fed Chair Powell had the chance to be the policy Grinch who stole Christmas. Instead, he was Santa Claus, Rudolph, and Frosty all rolled into one.

- Santa Claus (ho-ho-ho!): “The question of when will it become appropriate to begin dialing back the amount of policy restraint in place, that begins to come into view and is clearly a topic of discussion out in the world and also a discussion for us at our meeting today.”

- Rudolph (won’t you guide my sleigh?): “We’re aware of the risk that we would hang on too long, you know. We know that that’s a risk, and we’re very focused on not making that mistake.”

- Frosty (Happy Birthday!): “Fed would need to reduce restriction on economy well before 2% inflation.”

From “Two Behind” to “Three Behind”

The market responded like a child rounding the corner and seeing the presents under the tree for the first time on Christmas morning.

Wide-eyed in near disbelief at what they saw and heard from Fed Chair Powell, Treasury yields cascaded lower and stock prices took another parabolic step that sent the Dow Jones Industrial Average to a record closing high and the S&P 500 within striking distance of its own record closing high.

Santa’s helpers played a part, too. The stocking stuffer was the Summary of Economic Projections, which showed a median estimate for three rate cuts in 2024 versus two previously.

It didn’t matter that the fed funds futures market had four rate cuts priced in for 2024. The takeaway for the market was that the Fed is coming closer to the market’s thinking rather than staying stuck in its ways and remaining further away from the market’s thinking.

The irony is that the Fed is technically further away from the market’s thinking today than it was ahead of this week’s FOMC meeting. Again, the median estimate in September called for two rate cuts in 2024, so the Fed was “two behind” the four cuts expected by the market for 2024 going into this week’s meeting. Now, the fed funds futures market is pricing in six rate cuts (!) in 2024, which means the Fed is now “three behind” the market’s expectations.

| FOMC Meeting | Target Range | Probability |

| March 2024 | 5.00-5.25% | 69.5% |

| May 2024 | 4.75-5.00% | 58.5% |

| June 2024 | 4.50-4.75% | 54.7% |

| September 2024 | 4.25-4.50% | 80.5% |

| November 2024 | 4.00-4.25% | 66.9% |

| December 2024 | 3.75-4.00% | 58.8% |

Source: CME FedWatch Tool

The market, however, remains inclined to think that the Fed will follow the course that is being set for it. Whether that is truly a good thing remains to be seen. We have discussed before that it is one thing to cut rates because inflation is falling toward the 2% target on its own supply chain accord. It is another thing to cut rates because economic growth is falling by the wayside and into recession.

The latter would not be good for earnings prospects.

For now, though, the market is of the belief that Rudolph will help Santa Powell land the economic sleigh softly, and so far, the economic data is cooperating with that view.

Conveying a Policy Pivot

The source of all the excitement this week was the recognition that Fed Chair Powell had a chance to sound overtly hawkish given the easing in financial conditions that could make it harder to get inflation back down to target, but he instead chose to walk a more dovish-minded path.

By doing so, he was deemed to have conveyed a Fed policy pivot away from a tightening bias.

Naturally, the Fed Chair made it clear that the Fed is prepared to tighten policy further, if appropriate, but he also made it clear that the policy directive was crafted in a way to acknowledge that the Fed is at, or near, the peak rate for the cycle. The market interpreted that as some necessary lip service, which is why it focused on the unexpected remark that rate cuts were discussed and that the Fed is very focused on not making the mistake of hanging on too long with its policy restraint.

New York Fed President Williams (permanent FOMC voter) made an attempt seemingly to walk back some of the market’s excitement about the Fed policy shift, telling CNBC in an interview on Friday that the Fed isn’t really talking about rate cuts right now and that it is premature to think about the timing of rate cuts.

Ostensibly, the market is quite premature then, because all it has on its mind these days is multiple rate cuts from the Fed in 2024, beginning in March.

Atlanta Fed President Bostic (2024 FOMC voter) preyed on the market’s rate-cut expectations as well on Friday, talking like the Ghost of Christmas Yet to Come in telling Reuters that he expects two rate cuts in 2024, starting in the second half of the year.

What It All Means

The year ahead will be another battle of interest rate expectations. The market is gliding into the new year, however, with a confident sense that it will have its Christmas cake and eat it, too, with a series of rate cuts in 2024 that are more passive than active in nature.

What we mean by “passive” is rate cuts that happen with inflation gliding back to target in an easy economic manner, as opposed to “active” rate cuts that happen because the economy is foundering under the weight of prior rate hikes and/or a Fed that stayed restrictive too long.

In listening to Fed Chair Powell, he seems to be entertaining the passive glide path, which is why it was showtime this past week for him and the market.

The questions now are, when will it be go time and why?

The answers will matter greatly in the 2024 outlook for the stock market and the Treasury market, which are closing out 2023 with visions of rate-cut sugar plums dancing in their head.

—Patrick J. O’Hare, Briefing.com

(Editor’s Note: The next installment of The Big Picture will be posted December 29.)

Earnings dates:

MU- 12/20 AMC

Where will our markets end this week?

Higher because it is retail sales

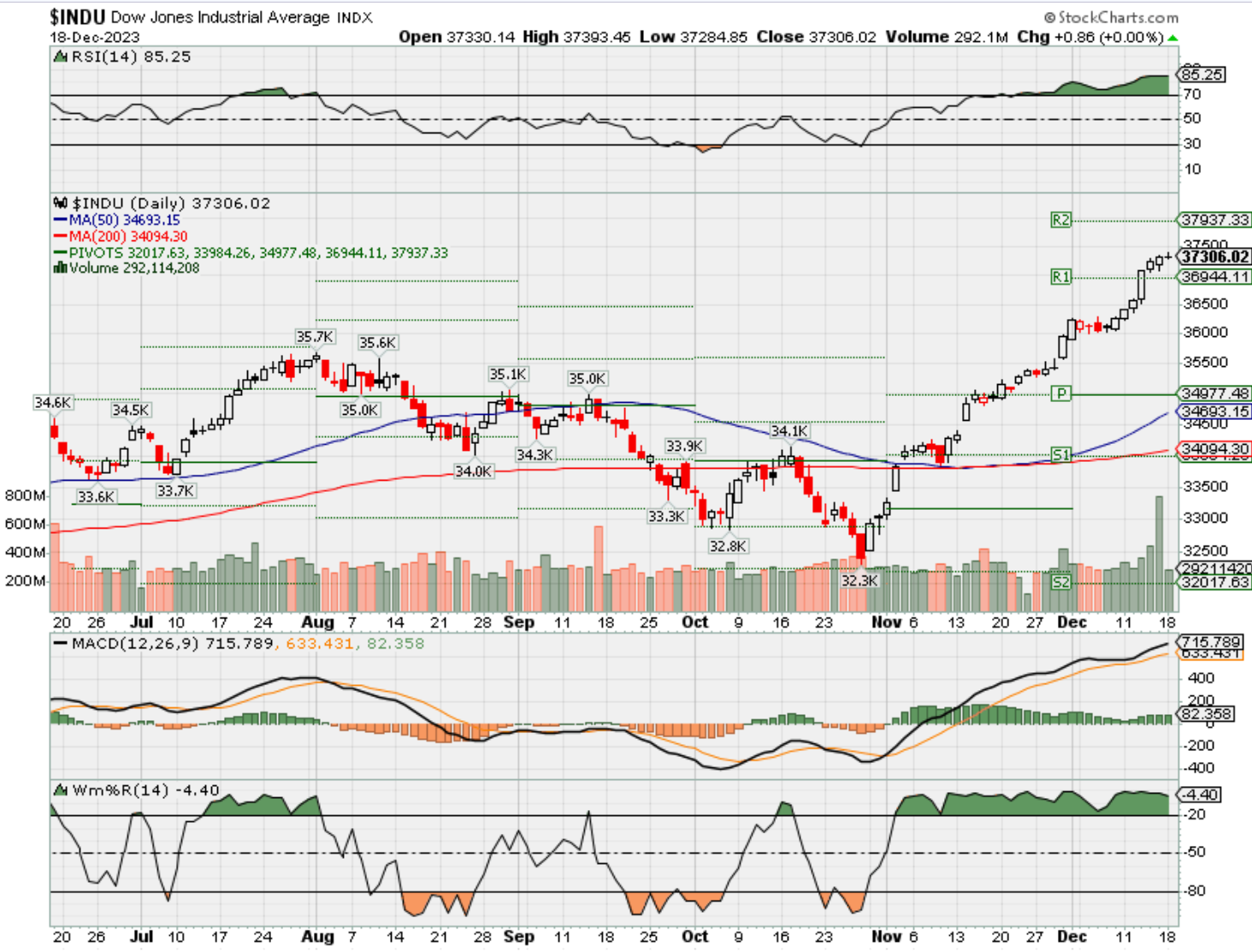

DJIA – Bullish Overbought

SPX –Bullish overbought

COMP – Bullish Overbought

Where Will the SPX end Dec. 2023?

12-18-2023 +3.0%

12-11-2023 +2.5%

12-04-2023 +2.5%

11-27-2023 +2.5%

Earnings:

Mon:

Tues: FDX, SCS,

Wed: GIS, BB, MU,

Thur: KMX, CCL, CTAS, NKE

Fri:

Econ Reports:

Mon: NAHB Housing Price Index,

Tue Building Permits, Housing Starts,

Wed: MBA, Consumer Confidence, Existing Home Sales,

Thur: Initial Claims, Continuing Claims, GDP, GDP Deflator, Phil Fed, Leading Indicators,

Fri: Personal Income, Personal Spending, PCE Prices, PCE Core, Durable, Durable ex-trans, New Home Sales, Michigan Sentiment

How am I looking to trade?

www.myhurleyinvestment.com = Blogsite

info@hurleyinvestments.com = Email

Questions???

Here’s why bringing down inflation has been different this time, according to Jerome Powell

PUBLISHED WED, DEC 13 20233:47 PM ESTUPDATED WED, DEC 13 20234:50 PM EST

Jesse Pound@/IN/JESSE-POUND@JESSERPOUND

KEY POINTS

- The Fed has viewed its inflation fight as a two-front battle of trying to weaken the demand in the economy while the “vertical” supply curve normalized, Fed Chair Jerome Powell said.

- The supply side of various parts of the economy is now getting closer to where it was pre-pandemic, Powell said.

- “So far, so good, although we kind of assume it will get harder from here,” he said.

Fed Chair Jerome Powell said Wednesday that the unique economic conditions created by the Covid-19 pandemic have helped the central bank’s effort to bring down inflation without causing a recession, a rare feat in economic history.

The Federal Reserve signaled in its latest economic projections that it will cut interest rates in 2024 even with the economy still growing, which would potentially be a path to the “soft landing” that many economists viewed skeptically when the central bank began aggressively hiking rates last year to fight post-pandemic inflation.

“This inflation was not the classic demand overload, pot-boiling over kind of inflation that we think about. It was a combination of very strong demand, without question, and unusual supply-side restrictions, both on the goods side but also on the labor side, because we had a [labor force] participation shock,” Powell said at a press conference after the Fed’s last meeting of the year.

The Fed has viewed its inflation fight as a two-front battle of trying to weaken the demand in the economy while the “vertical” supply curve normalized, Powell said. The supply side of various parts of the economy is now getting closer to where it was pre-pandemic, he said.

“Something like that has happened, happened so far. The question is once that part of it runs out — and we think it has a ways to run… — at some point, you will run out of supply side help and then it gets down to demand, and it gets harder. That’s very possible, but to say with certainty that the last mile is going to be different, I’d be reluctant to say we have any certainty around that,” Powell said.

“So far, so good, although we kind of assume it will get harder from here,” he added.

The description of the economy is similar to how Powell and other Fed members described the inflation situation in 2021, sometimes saying that the rapid price increases would prove to be “transitory.” The central bankers dropped that language as inflation accelerated and then began aggressively hiking rates in March 2022. The Fed has hiked its benchmark rate more than 5 percentage points in total since then.

Powell has maintained over the past year and a half that it was still possible, though not necessarily likely, that the U.S. economy could achieve a “soft landing,” where inflation returned to the Fed’s 2% target without causing a significant rise in unemployment.

Though rate hikes to slow inflation are often associated with recessions, the U.S. economy has sometimes expanded during such cycles before, most notably in the mid-1990s.

While many economists and Wall Street forecasters entered the year projecting a recession in 2023, the U.S. economy has instead proven surprisingly resilient. The stock market has also rallied after a deep sell-off in 2022, with the Dow Jones Industrial Average closing at a record high on Wednesday.

Although Powell said the U.S. economy has “slowed substantially” in recent months, the Fed still projects GDP to grow 1.4% next year.

Don’t miss these stories from CNBC PRO:

https://www.investors.com/news/china-stocks-baba-jd-bidu-miners-rise-on-data-stimulus/

Alibaba, JD.com, Baidu, These Miners Rise On Chinese Data, Stimulus

China stocks including Alibaba (BABA), JD.com (JD) and Baidu (BIDU) are on the rise early Friday after mixed economic data and fresh stimulus. China-influenced commodities stocks like copper giant Freeport-McMoRan (FCX) and diversified miners Rio Tinto (RIO) and BHP Group (BHP) continued their recent momentum, aided by a weak dollar following Wednesday’s pivotal Fed meeting.

Industrial output rose to a 21-month-high 6.6% from a year ago in November, up from 4.6% in October and ahead of expectations. However, retail sales missed expectations, with the 10.1% year-over-year gain boosted by soft year-ago data before China fully ditched its zero-Covid policies.

Chinese officials also took more steps to revive economic growth. The People’s Bank of China is offering a record 800 billion yuan (about $112.40 billion) in one-year loans to the banking system, doubling estimates. On Thursday, Beijing and Shanghai cut down payments for home purchases, while Beijing extended the maximum length of mortgages to 30 years from 25. Those moves are part of an effort to shore up falling home prices and lost faith in the property market that continues to drag down the economy.

So far, betting that Chinese stimulus will revive stocks has largely been a bust, though some top stocks have performed well.

BABA, JD Stocks Bounce

BIDU stock rose 1.7%, BABA 3.2% and JD 5.2% in midday Friday market action. Still, those stocks were about 30%, 40% and 60% off their respective 52-week highs as of Thursday’s close. EV upstart NIO (NIO) rose 1.2%, but had lost more than half its value.

However, PDD Holdings (PDD), which added 1.5%, is at a two-year high.

Still, Chinese stocks were mixed overall. Hong Kong’s Hang Seng was up 2.4% and the Shanghai Stock Exchange composite index fell 0.6%.

Non-Chinese mining stocks that would benefit from improvement in China’s economy were mixed early Friday. FCX stock, which jumped 7% to clear an early entry point on Thursday, dipped 0.6%. But BHP and RIO, both big iron ore producers, rose 0.2% and 0.6%, respectively. Both BHP and RIO cleared early entries earlier in the week.

Be sure to read IBD’s The Big Picture column after each trading day to get the latest on the prevailing stock market trend and what it means for your trading decisions.

Under Armour (UAA) Up 17.7% Since Last Earnings Report: Can It Continue?

Zacks Equity Research December 08, 2023

COLM Quick QuoteCOLM UAA Quick QuoteUAA

It has been about a month since the last earnings report for Under Armour (UAA Quick QuoteUAA – Free Report) . Shares have added about 17.7% in that time frame, outperforming the S&P 500.

Will the recent positive trend continue leading up to its next earnings release, or is Under Armour due for a pullback? Before we dive into how investors and analysts have reacted as of late, let’s take a quick look at the most recent earnings report in order to get a better handle on the important drivers.

Under Armour’s Q2 Earnings Top, Revenues Down Y/Y

Under Armour delivered better-than-expected earnings in second-quarter fiscal 2024, wherein the metric also increased year over year. Management also revised the guidance for fiscal 2024. The company reported earnings of 24 cents a share, which beat the Zacks Consensus Estimate of earnings of 21 cents per share. The company recorded earnings of 19 cents a share in the year-ago period.

Meanwhile, net revenues of $1,566.7 million came almost in line with the consensus estimate of $1,566 million but fell 0.5% on a year-over-year basis. The metric also slipped 1% on a currency-neutral basis.

The company’s wholesale revenues dipped 1% year over year to $940 million, while direct-to-consumer (DTC) revenues inched up 3% to $596 million due to a 2% rise in e-commerce revenues, which represented 35% of the total DTC business. Growth in the e-commerce and retail channels aided the performance. The company recorded 4% growth in owned and operated store revenues.

Let’s Delve Deeper

By product category, Apparel revenues edged up 3.1% year over year to $1,070.4 million, while Footwear revenues dipped 6.6% to $351.2 million. Revenues from the Accessories category inched up 2.5% to $113.9 million. Meanwhile, Licensing revenues tumbled 13.5% to $28.6 million.

Net revenues from North America decreased 2% to $991.4 million. Meanwhile, revenues from the international business increased 5% (up 3% on a currency-neutral basis) to $573 million.

Within the international business, net revenues in EMEA jumped 9% to $287.1 million (up 4% at constant currency), 3% in Asia-Pacific to $232.1 million (up 7% at constant currency) but fell 8% in Latin America to $53.7 million (down 19% at constant currency).

The company’s gross margin expanded 260 basis points to 48% from the prior-year period owing to gains from the supply chain with respect to reduced freight expenses, partly offset by a channel mix impact associated with the normalization of off-price sales. Selling, general and administrative (SG&A) expenses rose 2% to $606 million.

The company’s operating income increased to $145.8 million from $119.4 million. The operating margin was 9.3%, up from 7.6% in the year-earlier quarter.

Other Financial Details

Under Armour ended the quarter with cash and cash equivalents of nearly $655.9 million, long-term debt (net of current maturities) of $594.7 million and total stockholders’ equity of $2,089.7 million. The inventory jumped 6% to $1.1 billion.

FY24 Guidance

Management revised the view for fiscal 2024. For the current fiscal year, Under Armour expects revenues to decline 2-4% versus the earlier view of flat to slightly up. It expects the gross margin to be up 100-125 basis points from the prior year’s margin of 44.9% compared with 25-75 basis points projected previously. SG&A expenses are anticipated to be flat to slightly down, versus the previous view of flat to slightly up.

UAA still envisions earnings to be in the band of 47-51 cents per share, down from 84 cents per share reported in fiscal 2023. The company reported adjusted earnings of 58 cents a share for the comparable baseline period. Capital expenditures are likely to come in the band of $230-$250 million.

How Have Estimates Been Moving Since Then?

It turns out, estimates review have trended downward during the past month.

The consensus estimate has shifted -32.63% due to these changes.

VGM Scores

At this time, Under Armour has a subpar Growth Score of D, a grade with the same score on the momentum front. Charting a somewhat similar path, the stock was allocated a grade of C on the value side, putting it in the middle 20% for this investment strategy.

Overall, the stock has an aggregate VGM Score of D. If you aren’t focused on one strategy, this score is the one you should be interested in.

Outlook

Estimates have been broadly trending downward for the stock, and the magnitude of these revisions indicates a downward shift. Notably, Under Armour has a Zacks Rank #3 (Hold). We expect an in-line return from the stock in the next few months.

Performance of an Industry Player

Under Armour is part of the Zacks Textile – Apparel industry. Over the past month, Columbia Sportswear (COLM Quick QuoteCOLM – Free Report) , a stock from the same industry, has gained 4.2%. The company reported its results for the quarter ended September 2023 more than a month ago.

Columbia Sportswear reported revenues of $985.68 million in the last reported quarter, representing a year-over-year change of +3.2%. EPS of $1.70 for the same period compares with $1.80 a year ago.

For the current quarter, Columbia Sportswear is expected to post earnings of $2 per share, indicating a change of -18.4% from the year-ago quarter. The Zacks Consensus Estimate has changed -0.8% over the last 30 days.

Columbia Sportswear has a Zacks Rank #3 (Hold) based on the overall direction and magnitude of estimate revisions. Additionally, the stock has a VGM Score of F.

Apple makes surprise decision to pause some Watch sales before Christmas over patent dispute

PUBLISHED MON, DEC 18 202312:01 PM ESTUPDATED 2 HOURS AGO

Jake Piazza@IN/JAKE-PIAZZA-01AAB8200/

KEY POINTS

- Apple will pause sales on two of its latest Apple Watches, beginning in part on Thursday.

- The decision stems from an intellectual property disagreement between Apple and Masimo over the Blood Oxygen feature.

- Online sales of the Apple Watch Series 9 and Apple Watch Ultra 2 will pause at 3 p.m. Thursday and in stores after Sunday.

Apple will pause U.S. sales of two of the latest versions of its Apple Watches due to an intellectual property dispute over their Blood Oxygen feature, the company said.

The decision stems from two orders issued by the U.S. International Trade Commission on Oct. 26, which would restrict Apple’s ability to sell products that use the Blood Oxygen feature after an intellectual property disagreement between Apple and Masimo, a medical technology company.

U.S. customers won’t see a change in their access to buying either watch until Thursday. Online sales of the Apple Watch Series 9 and Apple Watch Ultra 2 will pause at 3 p.m. Thursday and in stores after Sunday.

The White House had 60 days to review the restrictions, per ITC policy, or until Dec. 25, but Apple said it started the pause early to ensure it is compliant with the order if the ITC ruling holds up.

Apple’s stock closed down less than 1% Monday and Masimo posted a gain of just more than 3%.

If the decision stands, one of the ITC’s orders will bar Apple and its affiliates from importing watches that use the Blood Oxygen feature, as well as materials used to make that feature, according to the FTC document. The ITC’s second order, a cease and desist, instructs Apple to stop selling the products using the Blood Oxygen feature.

If the ITC’s order stands, Apple has said it plans to “take all measures” to resume the sales of both watches as soon as possible.

People who have already bought either of the two Apple Watches in question will not have any issues with their product, according to Apple, and there is no change to the availability of either model outside of the U.S.

Apple’s wearables, home and accessories unit is the company’s third-largest revenue generator, bringing in $9.3 billion in the company’s last quarter.

In a statement, Apple wrote that the company “strongly disagrees with the order and is pursuing a range of legal and technical options to ensure that Apple Watch is available to customers.”

Masimo said that the ITC ruling shows that “even the world’s most powerful company must abide by the law” in a statement.

https://finance.yahoo.com/news/micron-mu-q1-earnings-horizon-174400212.html

Micron (MU) Q1 Earnings on the Horizon: Analysts’ Insights on Key Performance Measures

Zacks Equity Research

Fri, December 15, 2023 at 10:44 AM MST·2 min read

Analysts on Wall Street project that Micron (MU) will announce quarterly loss of $1 per share in its forthcoming report, representing a decline of 2400% year over year. Revenues are projected to reach $4.6 billion, increasing 12.6% from the same quarter last year.

Over the last 30 days, there has been an upward revision of 16.9% in the consensus EPS estimate for the quarter, leading to its current level. This signifies the covering analysts’ collective reconsideration of their initial forecasts over the course of this timeframe.

Before a company announces its earnings, it is essential to take into account any changes made to earnings estimates. This is a valuable factor in predicting the potential reactions of investors toward the stock. Empirical research has consistently shown a strong correlation between trends in earnings estimate revisions and the short-term price performance of a stock.

While investors typically use consensus earnings and revenue estimates as indicators of quarterly business performance, exploring analysts’ projections for specific key metrics can offer valuable insights.

In light of this perspective, let’s dive into the average estimates of certain Micron metrics that are commonly tracked and forecasted by Wall Street analysts.

The consensus among analysts is that ‘Revenue by Technology- DRAM’ will reach $3.22 billion. The estimate suggests a change of +14% year over year.

Analysts expect ‘Revenue by Technology- Other (primarily NOR)’ to come in at $62.58 million. The estimate suggests a change of -59.1% year over year.

It is projected by analysts that the ‘Revenue by Technology- NAND’ will reach $1.22 billion. The estimate indicates a year-over-year change of +10.7%.