HI Market View Commentary 03-06-2023

What is up for this week?= Powell speaks to congress Tues/Wed

He can (will) be hawkish and crash the market

“interest rates will keep going up and stay higher longer

IS inflation retreating? Of course not when you are still paying $4.99 for a dozen eggs, in some things but not others,

Inflation not coming down in items that really matter and hit the normal folks

Residential real estate is definitely coming down but NOT the property taxes

Commercial real estate huge glut of unused real estate

Fed’s Powell heads to Capitol Hill this week, and he’s going to have his hands full

PUBLISHED MON, MAR 6 20233:04 PM ESTUPDATED 3 HOURS AGO

Jeff Cox@JEFF.COX.7528@JEFFCOXCNBCCOM

KEY POINTS

- Federal Reserve Chairman Jerome Powell appears before Congress this week as part of semiannual testimony on monetary policy.

- Democratic legislators in particular have been worried that the Powell Fed risks dragging down the economy with its determination to fight inflation.

- Markets also have been torn between wanting the Fed to bring down inflation and being worried that it will go overboard.

Federal Reserve Chairman Jerome Powell is set to appear before Congress with a tall task: Persuade legislators that he’s committed to bringing down inflation while not pulling down the rest of the economy at the same time.

Markets have been on tenterhooks wondering whether he can pull it off. Sentiment in recent days has been more optimistic, but that can swing the other way in a hurry should the central bank leader stumble this week during his semiannual testimony on monetary policy.

“He has to thread the needle here with two messages,” said Robert Teeter, Silvercrest Asset Management’s head of investment policy and strategy. “One of them is reiterating some of the comments he has made that there has been some progress on inflation.”

“The second thing is being really persistent in terms of the outlook for rates remaining high. He’ll probably reiterate the message that rates are staying elevated for some time until inflation is clearly solved,” Teeter said.

Should he take that stance, he’s likely to face some heat, first from the Senate Banking Committee on Tuesday, followed by the House Financial Services Committee on Wednesday.

Democratic legislators in particular have been worried that the Powell Fed risks dragging down the economy, and in particular those at the lower end of the wealth scale, with its determination to fight inflation.

Slow out of the blocks

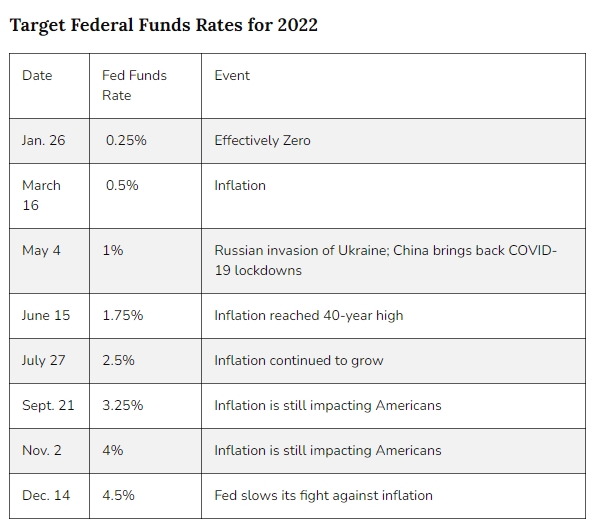

The Fed has raised its benchmark interest rate eight times over the past year, most recently a quarter percentage point increase early last month that took the overnight borrowing rate to a target range of 4.5%-4.75%.

Markets also have been torn between wanting the Fed to bring down inflation and being worried that it will go overboard. The central bank’s slow start in tackling the rising cost of living has intensified fears that there’s virtually no way it can bring down prices without causing at least a modest recession.

“Inflation is a pernicious problem. It was made worse by the Fed not recognizing it in 2021,” said Komal Sri-Kumar, president of Sri-Kumar Global Strategies.

Sri-Kumar thinks the Fed should have attacked sooner and more aggressively — for instance, with a 1.25 percentage point hike in September 2022 when inflation as measured by the consumer price index was running at an 8.2% annual rate. Instead, the Fed in December began reducing the size of its rate hikes.

Now, he said, the Fed likely will have to take its funds rate to around 6% before inflation abates, and that will cause economic damage.

“I don’t believe in this no-landing scenario,” Sri-Kumar said, referring to a theory that the economy will see neither a “hard landing,” which would be a steep recession, nor a “soft landing,” which would be a shallower downturn.

“Yes, the economy is strong. But that doesn’t mean you’re going to glide by with no recession at all,” he said. “If you’re going to have a no-landing scenario, then you’re going to accept 5% inflation, and that’s politically unacceptable. He has to work on bringing inflation down, and because the economy is so strong it’s going to get delayed. But the more delay you have in recession, the deeper it’s going to be.”

‘Ongoing increases’ ahead

For his part, Powell will have to find a landing spot between the competing views on policy.

A monetary policy report to Congress released by the Fed on Friday that serves as an opener for Powell’s testimony repeated oft-used language that policymakers expect “ongoing increases” in rates.

The chairman likely “will strike a tone that is both determined and measured,” Krishna Guha, head of global policy and central bank strategy at Evercore ISI, said in a client note. Powell will note the “resilience of the real economy” while cautioning that the inflation data has turned higher and the road to taming it “will be lengthy and bumpy.”

However, Guha said that Powell is unlikely to tee up a rate hike of a half-point, or 50 basis points, later this month, which some investors fear. Market pricing on Monday pointed to about a 31% probability for the larger move, according to CME Group data.

“We think the Fed hikes 50bp in March only if inflation expectations, wages, and services inflation reaccelerate dangerously higher and/or incoming data is so strong the median peak rate ends up going up 50,” Guha wrote. “The Fed cannot end a meeting further from its destination than it was before the meeting started.”

Interpreting the data will be tricky, though, going forward.

Headline inflation actually could show a precipitous decline in March as year-over-year comparisons of energy prices will be distorted because of a pop in prices around this time last year. The Cleveland Fed’s tracker shows all-item inflation falling from 6.2% in February to 5.4% in March. However, core inflation, excluding food and energy, is projected to increase to 5.7% from 5.5%.

Guha said it’s likely Powell could guide the Fed’s endpoint for rate hikes — the “terminal” rate — up to a 5.25%-5.5% range, or about a quarter point higher than anticipated in December’s economic projections from policymakers.

Where is the risk? = For me the risk is to the downside -448 points

Earnings dates:

MU – 3/29

https://www.briefing.com/the-big-picture

The Big Picture

Last Updated: 24-Feb-23 13:47 ET | Archive

Inflation is sticky business

First, the relatively good news: core-CPI, which excludes food and energy, moderated to 5.6% year-over-year in January from 5.7% in December. That was the smallest 12-month increase since December 2021 and down from the peak rate of 6.6% seen in September 2022.

Second, the relatively bad news: the core-PCE Price Index, which excludes food and energy and is the Fed’s preferred inflation gauge, increased to 4.7% year-over-year in January from 4.6% in December.

Third, the bad news: services inflation, seen in the CPI report, is still rising, up 7.6% year-over-year and sitting at its highest level since August 1982.

That’s a problem and the Fed knows it because services inflation can be sticky. It is a principal reason why the Fed is keen on seeing wage growth moderate more since higher wages often drive higher prices as companies aim to protect profit margins.

That worry is also a principal reason why the Fed has been sticking it to the market with rate hikes.

At Your Service(s)

The stock market is anxious to see the Fed pause its rate hikes. The Fed, however, isn’t making any promises. The only implied promise now from the Fed is that it will raise rates again at its March FOMC meeting.

There also seems to be an implied promise from the Fed that it won’t be cutting rates anytime soon. The chart below is the Fed’s sticking point on that front.

The inflation rates for total services, services less rent of shelter, and services less energy services are all north of 7.0%. The Fed’s overall inflation target is 2.0%, so when inflation in the services sector, which comprises the largest swath of the U.S. economy, is north of 7.0%, it is little wonder that the Fed isn’t communicating an inclination to cut rates anytime soon.

The Treasury market was a lot quicker than the stock market to process that position following the much stronger-than-expected January employment report, which was followed by a stronger than expected ISM Services PMI, and January CPI, PPI, and PCE Price Index data that exuded signs of stickiness on the inflation front.

The 2-yr note yield, sitting at 4.10% in front of the employment report, is at 4.80% today, up 38 basis points for the year.

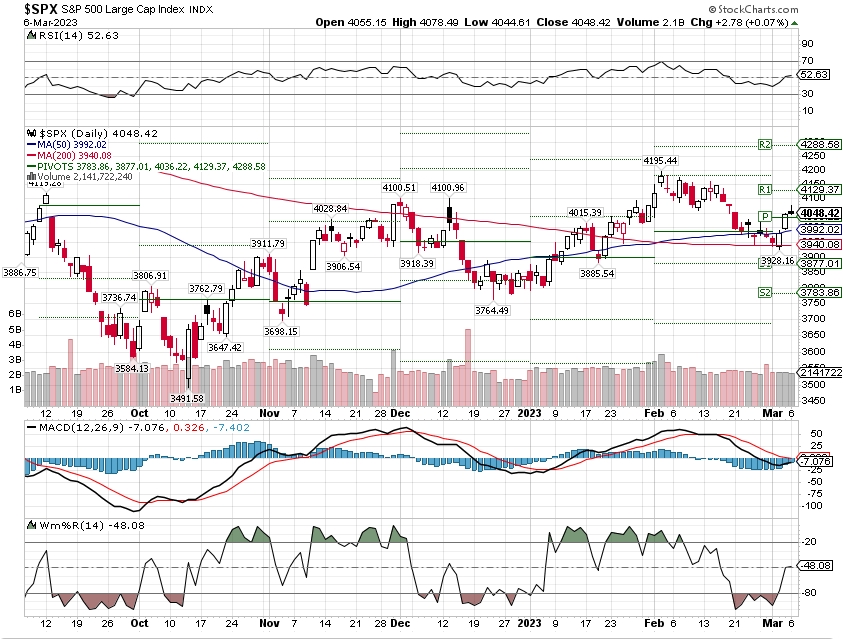

The stock market finally looks to be falling in-line with this reality. The S&P 500 is down 3.0% in February, recognizing that it got ahead of itself with a January rally that was predicated on the Fed pausing its rate hikes soon and then cutting rates once, if not twice, before the end of the year.

Eye on Wages

One Fed official after another has conceded that inflation is still too high, that more work needs to be done to get it back down to the 2.0% target, and that the Fed is committed to doing that.

An area that is being watched closely is wage growth. There has been some moderation in wages but not enough yet in Fed Chair Powell’s view that would be consistent with a 2.0% inflation rate. He hasn’t specifically quantified the wage growth he would like to see, but if the chart below were any guide, we would venture to guess it is in the neighborhood of average hourly earnings growth being up 2-3% year-over-year. In January, average hourly earnings were up 4.4% year-over-year.

The sticking point in this desire is that, when the core-PCE Price Index was stuck between being up 1.0-2.0% year-over-year, there was also globalization, more immigration, and more workers in the workforce.

Now, there is a trend of de-globalization, tighter restrictions on immigration, and fewer workers in the workforce given retiring baby boomers, COVID complications, and the opioid crisis. Hence, there is a huge number of job openings and a seeming scarcity of workers to fill those jobs, which threatens to keep wage growth sticking at higher levels for longer as employers compete to fill those openings.

What It All Means

Consumers and businesses are stuck with inflation. Granted overall inflation pressures aren’t as pronounced as they were last year, but services inflation is and then some.

That’s a sticking point on the road to the Fed’s 2.0% target, which is a road we expect the Fed to drive in a committed manner knowing it allowed inflation to go off road by waiting too long to remove its policy accommodation. The Fed doesn’t want to make another driving mistake, which in its mind means doing too little right now rather than doing too much.

This approach is going to create some bumps for the stock market and bond market alike. It already has. There are likely more bumps ahead, though, because the Fed is not done sticking it to the market with rate hikes. Furthermore, with services inflation as high as it still is, the market looks poised to be stuck with higher rates for longer than it previously expected.

—Patrick J. O’Hare, Briefing.com

https://go.ycharts.com/weekly-pulse

| Market Recap |

| WEEK OF FEB. 27 THROUGH MAR. 3, 2023 |

| The S&P 500 index rose 1.9% last week, led by the materials sector, as investors were encouraged by stronger-than-expected services sector data and a Fed official’s comments supporting a “slow and steady” approach to monetary policy.

The market benchmark ended Friday’s session at 4,045.64, up from last Friday’s closing level of 3,970.04. On Tuesday, the S&P 500 closed out February with a 2.6% monthly loss as investors worried about the impacts of inflation and interest rate increases on the economy. Concerns were magnified last month after companies including Home Depot (HD) and Walmart (WMT) issued weaker-than-expected earnings guidance. However, the index is still up 5.4% for the year to date thanks to a 6.2% January jump that had come on hopes for the pace of rate increases to slow. While concerns about the pace of rate increases weighed on the market in February, investors found some comfort on Thursday in comments from Atlanta Fed President Raphael Bostic, who told reporters that “slow and steady is going to be the appropriate course of action.” Investors were also encouraged on Friday by two reports showing US services sector activity was stronger than projected in February. The Institute for Supply Management’s purchasing managers’ index for February came in higher than the consensus estimate and showed a second consecutive month of growth. Separately, S&P’s services PMI gauge for February ended a seven-month sequence of contraction and surpassed the consensus estimate. S&P’s report also showed year-ahead output expectations were the strongest since May 2022. The materials sector had the largest percentage increase last week, up 4%, followed by increases of 3.3% each in communication services and industrials. Just two sectors fell: Utilities slipped 0.7% and consumer staples edged down 0.4%. In the materials sector, shares of Steel Dynamics (STLD) rose 15% on the week as the steel producer and metals recycler reported a 25% boost to its quarterly dividend payment. In communication services, shares of Facebook parent Meta Platforms (META) climbed 8.8%. The company said it is slashing the price of two virtual reality headsets and it will implement — either fully or partially — most of the recommendations made by its independent oversight board regarding its so-called “cross-check” content moderation system. In industrials, shares of Union Pacific (UNP) gained 7.9% as the railroad company said it expects to name a new chief executive this year that will take over from Lance Fritz, who has been CEO since February 2015. The plan prompted BofA Securities to upgrade its investment rating on Union Pacific’s shares to buy from neutral while raising its price target on the stock to $241 each from $218. On the downside, the decliners in utilities included shares of Sempra (SRE), which fell 2.8% from a week ago as the energy infrastructure company reported Q4 revenue below analysts’ mean estimate. Next week, economic data will be fairly light earlier in the week but all eyes will be on February jobs data later in the week. January factory orders are due on Monday, followed by January wholesale trade and consumer credit on Tuesday. February private-sector jobs data from ADP will be released on Wednesday, followed by weekly jobless claims on Thursday and the February nonfarm payrolls and unemployment reports on Friday. Provided by MT Newswires |

Where will our markets end this week?

Lower

DJIA – Bearish

SPX –Bearish

COMP – Bearish

Where Will the SPX end March 2023?

03-06-2023 -2.0%

02-27-2023 -2.0%

Earnings:

Mon:

Tues: DKS, CRWD, PRPL

Wed: CPB

Thur: BJ, GCO, JD, DOCU, LOCO, GPS, ORCL, SWBI, ULTA, MTN

Fri: BKE

Econ Reports:

Mon: Factory Orders

Tue Wholesale Inventories, Consumer Credit

Wed: MBA, ADP Employment, Trade Balance, Jolts, Fed Beige Book

Thur: Initial Claims, Continuing Claims,

Fri: Average Workweek, Non-Farm Payroll, Private Payroll, Unemployment Rate, Hourly Earnings, Treasury Budget

How am I looking to trade?

Currently running mostly stocks with protection

www.myhurleyinvestment.com = Blogsite

info@hurleyinvestments.com = Email

Questions???

SEC Commissioners’ Portfolios Laden with This Manager’s Funds

As the SEC looks to update ethics rules governing the type of investments its staff can own, FA-IQ examined the five commissioners’ personal investments.

By Michael Taffe|March 3, 2023

This is the first of a two-part series on the SEC commissioners’ investment holdings. Look next week for a deep dive into their portfolios.

Roughly 80% of mutual fund assets are controlled by just three managers: BlackRock, State Street and Vanguard. But for the five members of the Securities and Exchange Commission who oversee these asset managers, one stands as the clear favorite.

More than 95% of the five SEC commissioners’ personal investments are in Vanguard products.

Gary Gensler, chair since 2021, was the most Vanguard-heavy, with 95% of the value of his holdings in the firm’s funds, according to an analysis of financial disclosure forms. Commissioner Mark Uyeda, who joined last year, had about 81% of his portfolio invested with the world’s second largest mutual fund provider, while Commissioners Hester Peirce and Caroline Crenshaw each had roughly half of their investments in Vanguard products.

mThe only investments Commissioner Jaime Lizárraga reported were in 529 accounts for his five children.

“It points to consolidation in the economy,” said Jeff Hauser, founder and director of the Revolving Door Project. “Does the SEC alone have as an institution the authority to further open up the fund manager market such that it’s less likely that one manager is so dominant?”

Portfolio Parameters

SEC commissioners, as well as staff members, must abide by certain rules outlining what personal investments they can and can’t own. In late January, the agency proposed updates that would explicitly bar officials from holding financial sector funds and exempt certain reporting requirements for diversified mutual funds.

As the SEC awaits public comment on the proposed changes, Financial Advisor IQ analyzed the most recent financial disclosure forms Gensler and the four other commissioners filed with the agency’s Office of the Ethics Counsel.

The commission’s current ethics rules bar staff from holding individual stocks of companies or entities the regulator directly oversees, as well as short-selling and other prohibitions. The additional provisions would also cover companies exempted from registration under the ’40 Act and pooled investment vehicles that explicitly concentrate investments in entities regulated by the commission.

Protocols for government officials’ transactions came under scrutiny in 2021 when Bloomberg reported that the presidents of multiple Federal Reserve regional banks had actively traded securities affected by the central bank’s interventions at the beginning of the Covid-19 pandemic.

And an unidentified SEC official received a seven-day suspension in 2019 for failing to report securities transactions over a seven-year period, including stocks the SEC’s inspector general concluded were a conflict of interest, the Wall Street Journal reported.

Questions have also arisen over the management style of funds held by political appointees, Hauser said.

“One excuse that I see all too often that I think is just really bogus is that we hired a financial advisor and gave them authority and they weren’t supposed to do it,” he said. “But they should be held responsible, and it’s not clear to me that your money should be actively managed.”

Getting Active

At a minimum of $44.6 million as of December 2021, the value of Gensler’s portfolio outstripped that of the next wealthiest commissioner 10 times over. The former Goldman Sachs partner held mainly passive funds or ETFs spread across retirement accounts, brokerages and family or marital trusts, the analysis finds.

While just about 10% of Gensler’s holdings were in actively managed funds, around half of the funds in Peirce’s portfolio, valued at between $462,000 and $1.4 million, were actively managed. That included holdings in the Gabelli Gold Fund and the Timothy Plan Aggressive Growth Fund.

Uyeda’s and Crenshaw’s portfolios were about 38% and 30% actively managed, respectively, according to the financial disclosures. They owned funds managed by Dodge & Cox, Janus Henderson, Virtus, Touchstone and American Funds, among others.

The SEC’s pending update to its ethics guidelines reflects an increasingly complex investing environment, Hauser said.

“There are so many more financial instruments to buy and sell in 2023 than there were in the 1970s when America started having ethics rules in earnest, and most of them have not been updated,” he said. “At a place like the SEC, it’s more likely that you could place a bet into something that is not a single company’s stock, but where there’s a disproportionate impact on a specific sector or financial instrument.”

Of the five current commissioners, none reported holdings of financial industry sector funds in their required ethics disclosures.

“As we look toward tightening rules, we should look first at the people with the most power to do harm. And for those, we can justify a much more rigorous set of rules than for a population of career employees where you’ve got to be able to recruit experts,” said Walter Shaub Jr., who served as director of the U.S. Office of Government Ethics from 2013 to 2017. “I would not be opposed to saying a Federal Reserve Board commissioner or an SEC commissioner should have to stop all trading.”

Shaub resigned at the onset of Donald Trump taking office amid disputes over the former president’s refusal to divest his business interests and delays in submitting ethics waivers for administration officials. Shaub is now a senior ethics fellow at the Project on Government Oversight.

“The SEC exists to make sure that people feel the market for trading stocks is safe. And so, appearance is everything,” he said.

The concern, Shaub said, is not so much about what will influence a commissioner, but what effect “even the slightest appearance of corruption or self-dealing” will have on citizens in their business and personal finance activities.

“I think it would be very reasonable to come up with a very hardline set of rules that says the political appointees in those agencies had to stop all trading activity and divest all assets other than diversified mutual funds,” he said.

Tracking Portfolios

SEC commissioners, as well more than 100 others deemed to be “senior officers” at the agency, disclose investments that they and their spouses own in a filing known as OGE Form 278e. Although they must specifically identify each investment, those holdings’ values are only disclosed in ranges as narrow as between $0 to $1,000 at the low end to as wide as between $25 million and $50 million at the high end.

FA-IQ analyzed the portfolio holdings of the five commissioners, taking the median of each disclosed investment range. The analysis excluded assets held in bank or credit union accounts and any defined-benefit plans.

“You can have significant movements in the range that we are not currently seeing and probably ought to be able to see, because otherwise we’re getting proportionately a lot of disclosure by middle class government officials, and very little disclosure by extremely wealthy officials,” Shaub said.

One of Gensler’s family trusts, for example, reported holding between $25 million and $50 million of Vanguard’s Total Stock Market Index ETF.

The SEC is proposing to eliminate pre-clearance trading, reporting and holding period requirements for diversified mutual funds because “they generally pose a low risk of conflicts of interest, misuse of nonpublic information for personal gain, or appearance problems,” according to the proposal and a news release.

Mutual funds that concentrate investments in a particular sector or foreign country would remain subject to existing ethics rules.

There are other reasonable exceptions that can be made, Shaub said, including to account for investments held by an official’s spouse or in a multi-generational family trust they may not have control over.

The cleanest solution for ethics rules governing political appointees? Bar all trading while in office, Hauser said.

“Our general rule of thumb is that you need cleaner rules to make the enforcement easier in terms of the amount of time it takes to enforce, easier to prove that something was problematic and that some responsibility needs to be taken. So, there’s less of an excuse, and also less loophole creation,” he said. “We generally prefer fewer and simpler rules whenever possible.”

An SEC spokesperson told FA-IQ in an email that “the Commissioners comply with all SEC and government-wide ethics rules,” but said the agency had “no further comment on their holdings.”

Cash Is Paying More Than Traditional Stock-Bond Portfolio

by Bloomberg News

February 28, 2023

For the first time in more than two decades, some of the world’s most risk-free securities are delivering bigger payouts than a 60/40 portfolio of stocks and bonds.

The yield on six-month US Treasury bills rose as high as 5.14% Tuesday, the most since 2007. That pushed it above the 5.07% yield on the classic mix of US equities and fixed-income securities for the first time since 2001, based on the weighted average earnings yield of the S&P 500 Index and the Bloomberg USAgg Index of bonds.

The shift underscores how much the Federal Reserve’s most aggressive monetary tightening since the 1980s has upended the investing world by steadily driving up the “risk-free” interest rates — such as those on short-term Treasuries — that are used as a baseline in world financial markets.

The steep jump in those payouts has reduced the incentive for investors to take risks, marking a break from the post-financial crisis era when persistently low interest rates drove investors into increasingly speculative investments to generate bigger returns. Such short-term securities are typically referred to as cash in investing parlance.

“After a 15-year period often defined by the intense cost of holding cash and not participating in markets, hawkish policy is rewarding caution,” Morgan Stanley strategists led by Andrew Sheets said in a note to clients.

The yield on six-month bills rose above 5% on Feb. 14, making it the first US government obligation to reach that threshold in 16 years. That yield is slightly higher than those on 4-month and one-year bills, reflecting the risk of a political skirmish over the federal debt limit when it comes due.

The 60/40 yield has also risen since stocks cheapened and Treasury yields climbed, but not as fast as the T-bills’.

The high rates on short-term Treasuries are casting broad ripples in financial markets, according to Sheets. It has reduced the incentive for typical investors to take on more risk and driven up the cost for those who use leverage — or borrowed money — to boost returns. He said it has also cut the currency-hedged yields for foreign investors and made it more expensive to use options to bet on higher stocks.

Investing in stocks and bonds has also been challenging recently. After a strong start to the year, the 60/40 portfolio has given up most of its gains since a string of strong economic and inflation data prompted investors to bet on a higher peak to the Fed’s policy rate. That sparked a simultaneous selloff in stocks and bonds this month. The 60/40 strategy has returned 2.7% this year, after tumbling 17% in 2022 in its biggest decline since 2008, according to Bloomberg’s index.

How’s the return to office going? Just look at shares of one of the largest office REITs

PUBLISHED FRI, MAR 3 20239:20 AM ESTUPDATED AN HOUR AGO

For a window into how America’s return to the office is going in the first quarter of 2023, not to mention the effect of surging interest rates on commercial real estate in general, look no further than the shares of Vornado Realty Trust (VNO).

At one point on Thursday, shares in the real estate investment trust headed by CEO Steven Roth had fallen 59.5% from their 52-week high a year ago — and almost 80% from their all-time reached in early 2015. In fact, Vornado shares on Thursday briefly touched their lowest level since 1998.

The vast majority of Vornado’s portfolio is concentrated in what it calls “the nation’s key market — New York City,” along with far smaller holdings in Chicago and San Francisco. Vornado says it owns 20 million square feet of office space plus 2.6 million square feet of street retail space in Manhattan alone, 3.7 million square feet at The Mart in Chicago and a controlling stake in almost 2 million square feet of office in San Francisco.

One problem for Vornado is that the national office occupancy rate last week — as measured by the number of employees coming into the office rather than working from home — topped 50% “for only the second time since the start of the pandemic,” according to Kastle Systems, which monitors the number of employees swiping in each day.

But in the New York metropolitan area last week, the rate fell to 46.7% from 47.8% the week before, Kastle said. In San Francisco, the rate was even lower last week, at 43.9%, while in Chicago it was 49.4%.

Maybe that’s why Vornado took a $600 million non-cash impairment charge in a retail joint venture in New York City in late January.

All REITs face a second problem: the higher cost of capital. With the Federal Reserve raising benchmark interest rates for the past year to almost 5% from almost nothing, that also raises capitalization rates in real estate, increasing the level of risk.

Vornado owed $8.39 billion in proforma long-term debt as of March 1, according to FactSet.

Deutsche Bank analyst Derek Johnston ranked office REITs last out of eight REIT subindustry groups in a monthly review released on Tuesday. In January, subsector year-over-year cap rates climbed the most for office owners, he said, up 80 basis points, or 8/10ths of a percentage point.

Vornado Realty Trust

Vornado’s fourth-quarter results and earnings call were “directionally … positive,” JPMorgan analyst Anthony Paolone wrote last week, but “VNO still has a lot of wood to chop with respect to managing its capital structure (higher leverage and rate exposure than peers) in the years to come amidst a challenging office environment.” He has an underweight rating on Vornado and a price target of $20.

That said, Vornado’s woes are far from unique. Boston Properties (BXP) touched its lowest since 2010 on Thursday, while Hudson Pacific Properties (HPP) on an intraday basis Thursday fell to a record low, going back to its 2010 initial public offering. Elsewhere, JBG Smith Properties (JBGS) intraday dropped to the lowest since its 2017 IPO, and Kilroy Realty (KRC)’s 52-week low was its weakest price since 2011.

— CNBC’s Michael Bloom contributed to this report.

China sets GDP target of ‘around 5%’ for 2023

PUBLISHED SAT, MAR 4 20238:14 PM ESTUPDATED SAT, MAR 4 20239:43 PM EST

KEY POINTS

- China set a growth target of “around 5%” for 2023, according to Premier Li Keqiang’s government work report released Sunday.

- China also set a goal of 3% for the consumer price index, and a 5.5% unemployment rate for people in cities — with the creation of around 12 million new urban jobs.

- The work report called for implementing “prudent monetary policy” in a “targeted” way.

BEIJING — China set a growth target of “around 5%” for 2023, according to Premier Li Keqiang’s government work report released Sunday.

Analysts generally expected China to set a GDP target of above 5% for 2023. The average forecast for growth is 5.24%, according to CNBC analysis.

China also set a goal of 3% for the consumer price index, and a 5.5% unemployment rate for people in cities — with the creation of around 12 million new urban jobs. That’s more than last year’s target of “over 11 million.”

The work report called for implementing “prudent monetary policy” in a “targeted” way. The deficit-to-GDP ratio is expected to increase to 3% from 2.8% last year, the report said.

Li presented the report Sunday at the opening of the National People’s Congress, part of the annual “Two Sessions” parliamentary meeting. This is his last such congress as premier.

The work report noted the coming change in central government leadership, while laying out eight priorities for economic policy.

Spurring domestic demand — from consumption and investment — ranked first, followed by improving the industrial system and supporting non-state-owned enterprises, according to the report.

Other priorities included “intensifying efforts to attract and utilize foreign investment,” “preventing and defusing” financial risks, stabilizing grain production, continuing green development and developing social programs.

“We should strive to develop the digital economy, step up regular oversight, and support the development of the platform economy,” the report said in English.

While it did not name specific companies, internet tech companies such as Alibaba typically fall under the “platform economy,” which has been subject to increased scrutiny from Beijing in the last few years.

Real estate

On real estate, the work report called for supporting people in buying their first homes and to “help resolve the housing problems of new urban residents and young people.”

“We should ensure effective risk prevention and mitigation in high-quality, leading real estate enterprises, help them improve debt-to-asset ratios, and prevent unregulated expansion in the real estate market to promote stable development of the real estate sector,” the report said.

A slump in the massive property sector has weighed on China’s economic growth in the last year. Beijing cracked down on developers’ high reliance on debt for growth in 2020.

China’s real estate policy will likely support high-quality real estate companies’ reasonable financing needs, and guide them toward areas of sustainable growth, said Bruce Pang, chief economist and head of research for Greater China at JLL.

On the other hand, developers “that cannot take the initiative to complete business adjustment and transformation are naturally cleared by the market,” he said in Mandarin, translated by CNBC.

China’s GDP only rose by 3% last year in a rare miss of the national goal.

The country had set a target of around 5.5% growth for 2022. But Covid controls, including the two-month lockdown of Shanghai, and the real estate slump dragged down growth.

This year, the Two Sessions is also set to formalize government titles for the new premier, vice premiers and heads of different ministries. This year’s National People’s Congress is set to end on March 13.

“Given the complete reshuffling of the government, a key issue to watch in the next few months is how the new leaders will boost private sector confidence,” said Zhiwei Zhang, president and chief economist at Pinpoint Asset Management. “This is more important than the fiscal and monetary policies, in my view.”