HI Market View Commentary 09-27-2021

IF I was to ask you to complete the following sentence: The stock market is …….?

Unpredictable, Volatile, Still over-valued, hard, easy to lose money, lose half of the value of a portfolio, flat, a royal pain the in the A$$, forecasting upcoming conditions, a poor or lagging indicator of current economic conditions, influenced by events NOT necessarily affecting or can truly effect the markets,

Fluid because it is ever changing

That is why we collar trade, or use protective puts

It also includes fear and greed

Usually we start protecting the first or second week of October for the Oct/Nov earning events

We also capture profits from protection, try to add shares and re-protect at the lower cost basis

Why do we do this? Because a Christ Rally usually occurs after the earning period

$1, 0.90, 0.783, 0.603, 0.94, 1.02, 1.055, 1.203, 1.251, 0.775, 0.953, 107.6, 107.6, 1.216, 1.581, 1.755, 1.738, 1.911, 2.275, 2.115, 2.729, 3.166

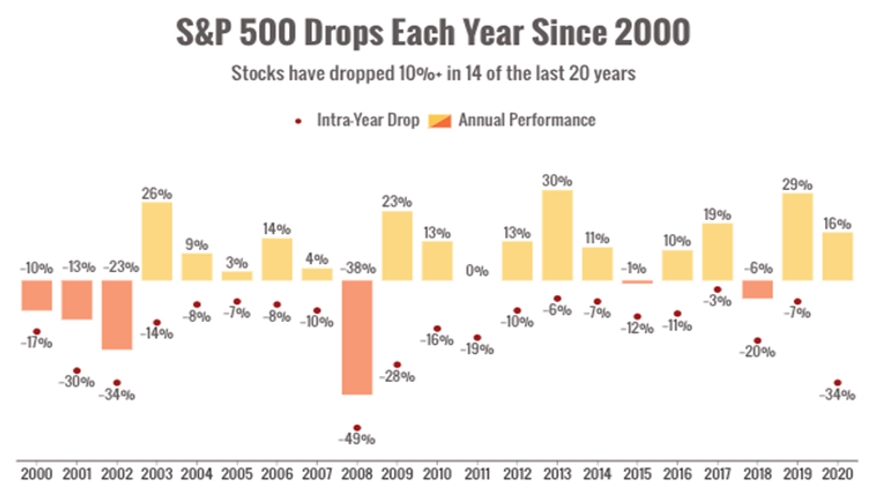

So you are told the S&P 500 double on average every 7.75 years 1=2=4= 7.20

IF you believe the slightly below 10%

1.10, 1.21, 1.33, 1.46, 1.61, 1.77, 1.94, 2.14, 2.35, 2.59, 2.85

Averages are NOT your friends and you have to do something different to beat the S&P 500

https://www.briefing.com/the-big-picture

The Big Picture

Last Updated: 24-Sep-21 12:42 ET

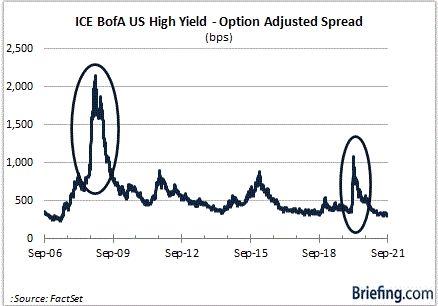

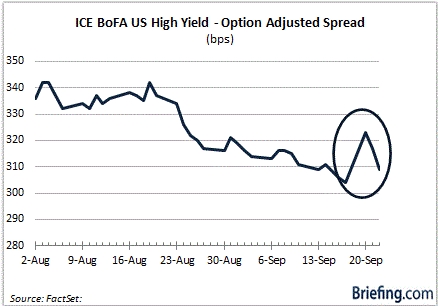

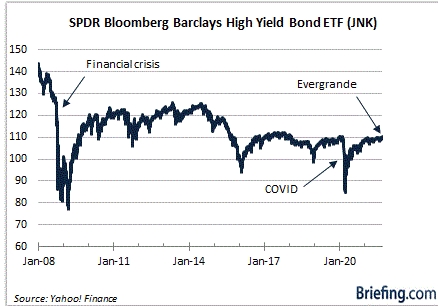

High yield market indicates Evergrande’s problems are not everyone’s problems

There are few phrases in finance that elicit more fear than “systemic risk.” That phrase imparts a view that something financially damaging — if not devastating — in a broad sense could happen.

In the past week, systemic risk was part of the market narrative each day as pundits discussed, and debated, the ramifications of a debt default by Chinese property developer Evergrande, which has over $300 billion in liabilities.

While the pundits talked, the high yield debt market acted — and the actions there spoke louder than words.

What Systemic Risk Looks Like

The global financial crisis of 2008? That was systemic risk at its worst. The COVID pandemic of 2020? That was another instance of systemic risk that led to an unprecedented monetary and fiscal policy response to combat the worst global recession since the Great Depression.

Don’t think the high yield market didn’t feel it either. The chart below makes it painfully clear that systemic risk hit home in a precipitous widening of high-yield spreads during those unsettling times.

Systemic risk events are not good for anything that relies on a smoothly functioning economy. That is especially true for high yield (aka “junk”) bonds, which trade on the belief that steady and dependable cash flows will ensure interest payments are going to be met in the timely manner they are expected to be met.

When there is a specific risk factor that threatens that capability, the price of that individual bond will decline, and its yield will increase. However, when there is a systemic risk factor that threatens that capability, or comes to fruition, the universe of high yield bonds typically gets thrown off its axis and experiences an abrupt correction.

Canary in a Cage

Oftentimes, the high yield market acts like a canary in a coal mine when it comes to systemic risk or approaching economic problems. If the high yield market is behaving badly, it can stoke fear in other markets, namely the stock market. If it is behaving well and remaining calm, it can in turn spur confidence in other markets.

So, how did the high yield market react to reports that Chinese property developer Evergrande might default on its debt and fuel systemic risk?

It acted more like a canary in a cage than a canary in a coal mine. That is, it didn’t do much — certainly not relative to other systemic risk events and certainly not like the headlines suggested it should. There was a short-lived arrhythmia on Monday, but a steady heartbeat was soon restored. In fact, the option adjusted spread never got above the high it saw in August when Evergrande wasn’t part of the daily market narrative.

What It All Means

The takeaway is that there was never a strong belief in the high yield market that the Evergrande situation had the makings of a problem carrying systemic risk. That’s not to say Evergrande isn’t going to cause problems. Rather, the high yield market just isn’t convinced Evergrande’s problems will be everyone’s problems.

The recognition that it remained calm helped calm the stock market, which had been suffering from a de-risking move predicated in part on systemic risk concerns that the high yield market didn’t embrace.

In this situation, the idiom proved true that one person’s trash (junk bonds) is another person’s treasure, only this time nothing was thrown out. Instead, the resilience of junk bonds contributed to a treasure hunt in the stock market that produced some riches for participants buying the oversold systemic risk dip.

—Patrick J. O’Hare, Briefing.com

| https://go.ycharts.com/weekly-pulse |

| Market Recap WEEK OF SEP. 20 THROUGH SEP. 24, 2021 The S&P 500 index edged up 0.5% last week, with the energy and financial sectors leading to the upside while real estate and utilities weighed. The market benchmark ended the week at 4,455.48, up from last Friday’s closing level of 4,432.99. This marks the index’s first weekly gain in three weeks and erases only part of the declines posted earlier in the month. The S&P 500 is now down 1.5% for September, with four sessions in the month remaining. Despite the September slide, the index is up about 19% for the year to date. The week’s move was slight as investors traded cautiously heading into the end of Q3. In the US, the Federal Reserve’s Federal Open Market Committee indicated it may begin tapering its asset purchases as soon as November and could raise interest rates next year. Overseas, investors continued to worry about Chinese property markets. The energy sector had the largest percentage increase of the week, up 4.7%, followed by a 2.2% rise in financials and a 0.9% advance in technology. Other sectors that rose last week included industrials, consumer discretionary, and materials. On the downside, real estate led with a 1.5% drop while utilities slipped 1.2%. Other decliners included communication services, health care, and consumer staples. The energy sector’s advance came as crude oil futures rose. Among the gainers, shares of Diamondback Energy (FANG) added 7.4% on the week while Devon Energy (DVN) jumped 11%. In the financial sector, shares of American Express (AXP) climbed 7.2% as the company said it is committing to a goal of net-zero carbon emissions by 2035. In real estate, Prologis (PLD) shares shed 1.7% as Evercore ISI downgraded its investment rating on the logistics real estate company’s stock to in-line from outperform. Among utilities stocks, Entergy (ETR) shares fell 9.2% as the company said the repair and replacement of electrical infrastructure damaged by Hurricane Ida are expected to cost $2.1 billion to $2.6 billion. The Gulf Coast utility also lost $75 million to $85 million of non-fuel revenue as a result of the power outages caused by the hurricane, according to the company’s statement. Next week, the final week of Q3, investors will get August readings on durable goods orders and core capital goods orders on Monday, followed by the September consumer confidence index on Tuesday and the August pending home sales index Wednesday. Thursday’s economic data will feature revised Q3 gross domestic product while Friday will include August readings on consumer spending and core inflation, among other data. Provided by MT Newswires |

Earnings Dates

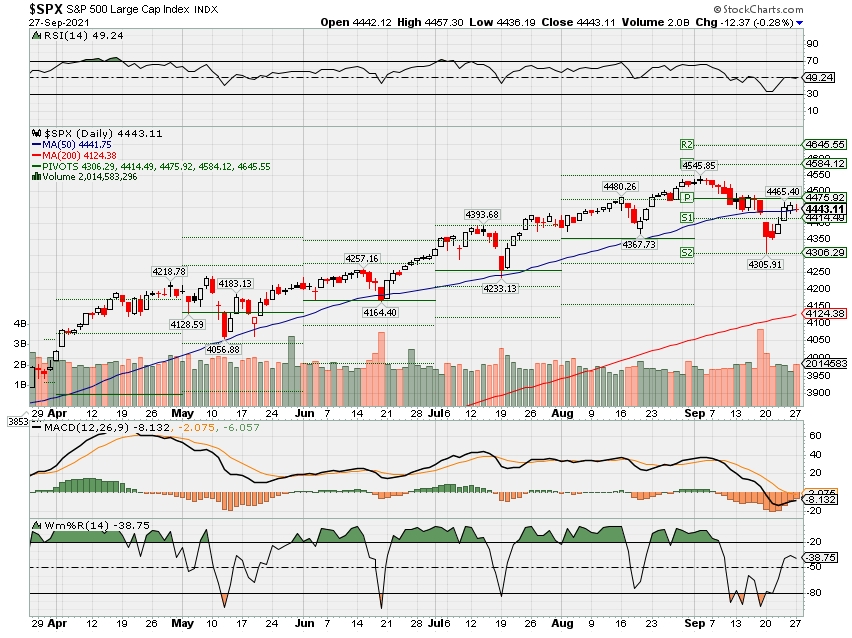

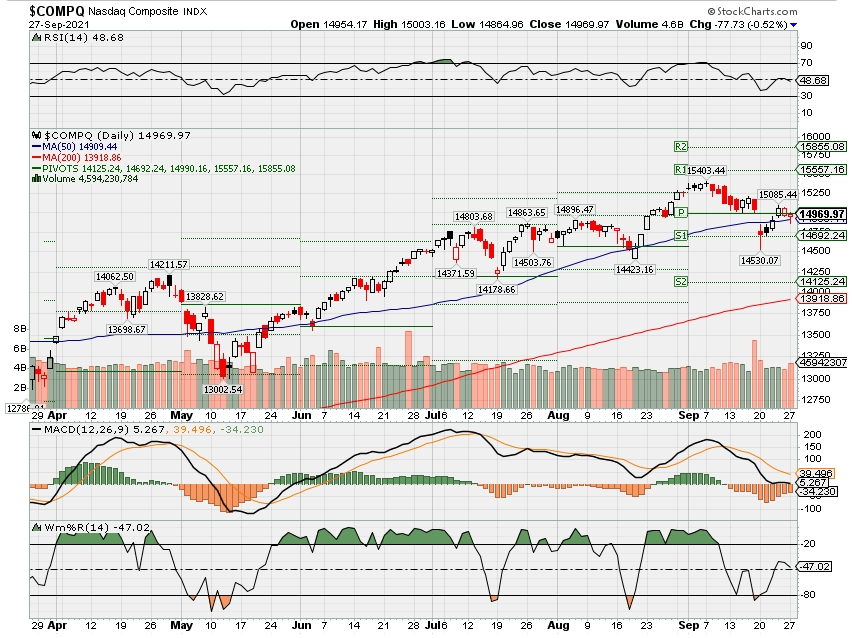

Where will our markets end this week?

Lower

DJIA – Bearish

SPX – Bearish

COMP – Bearish

Where Will the SPX end September 2021?

09-27-2021 -2.0%

09-20-2021 -2.0%

09-13-2021 -1.0%

09-07-2021 -1.0%

08-30-2021 -1.0%

Earnings:

Mon:

Tues: CALM, MU

Wed: CTAS, JBL, MLHR

Thur:

Fri:

Econ Reports:

Mon: Durable Goods, Durable ex-trans

Tues: FHFA Housing Price Index, Case Shiller, Consumer Confidence

Wed: MBA, Pending Home Sales

Thur: Initial Claims, Continuing Claims, GDP, GDP Deflator, Chicago PMI

Fri: PCE Prices, Core PCE Prices, Construction Spending, Personal Income, Personal Spending, ISM Manu Index, Michigan Sentiment

Int’l:

Mon –

Tues – Fed Chair Powell Testifies

Wed – Fed Chair Powell Testifies

Thursday – CN: NBS Non-Manufacturing PMI , Non Manu PMI

Friday-

Sunday –

How am I looking to trade?

Long put protection has been added

www.myhurleyinvestment.com = Blogsite

customerservice@hurleyinvestments.com = Email

Questions???

Evergrande Default Could Rock China’s Entire Economy

September 16, 2021 Updated: September 18, 2021

Analysis

China’s public debt already stands at 270 percent of GDP, and non-performing loans have hit $466.9 billion. In addition to existing economic challenges, real estate giant Evergrande Group has signaled that it may default on payments owed to creditors.

China’s second largest developer has been facing a liquidity crisis, as its onshore bond trading has been suspended. Without access to funding, Evergrande will find it impossible to pay suppliers, finish projects, or raise income, making default more likely—an eventuality which could send ripples through the entire Chinese economy.

Evergrande made $110 billion in sales last year and has $355 billion in assets. In June, it failed to pay some commercial paper and the government froze a $20 million bank account. The company now owes total liabilities of $305 billion, making it the most indebted real estate developer in the world. It is also the largest issuer of dollar junk bonds in Asia. Evergrande owes money to 128 banks and over 121 non-banking institutions. Consequently, the company’s stock price has dropped by 90 percent over the past 14 months, while its bonds were trading at 60 to 70 percent below par.

Evergrande accounts for 4 percent of total Chinese real estate high-yield debt. The company’s debt is of such significant size that it may pose systemic risk to China’s banking system. Late or defaulted payments by Evergrande could cause a chain reaction of defaults across institutions. An Evergrande sell-off could drive down prices, crashing over-leveraged developers. Authorities worry that this threatens to destabilize the entire real estate sector, which comprises about 30 percent of the Chinese economy.

Additionally, Evergrande has implications for the labor market. The company employs 200,000 people regularly and 3.8 million per year, on a project basis. After 18 months of sporadic COVID-19 lockdowns, China needs more, not fewer, jobs.

People gather to demand repayment of loans and financial products at Evergrande’s headquarters, in Shenzhen, Guangdong Province, China on Sept. 13, 2021. (David Kirton/Reuters)

Evergrande is expected to be unable to meet interest and principal payments due next week.

The People’s Bank of China and the China Banking and Insurance Regulatory Commission warned Evergrande’s executives to reduce its debt risks. Beijing instructed authorities in Guangdong Province to coordinate with potential buyers of Evergrande’s assets. Meanwhile, regulators have signed off on a proposal to let Evergrande renegotiate payment deadlines, which would grant a temporary reprieve.

Evergrande is not the only problem in China’s debt market. By midyear, Chinese onshore and offshore defaults already totaled more than $25 billion, which is nearly the same amount as for the entire previous year. Real estate firms accounted for about 30 percent of these defaults. Some of the larger culprits were China Fortune Land Development and Sichuan Languang Development. Furthermore, the transportation, tourism, and retailing sectors have been particularly hard hit by the pandemic lockdowns, increasing defaults in those sectors. Some state-linked companies have also suffered defaults, such as Yongcheng Coal & Electricity Holding Group and Tsinghua Unigroup. Additionally, China Huarong Asset Management, a majority state-owned company, failed to release its 2020 results on schedule. Between the main company and its subsidiaries, Huarong had $39 billion of debt outstanding, eventually posting a $15.9 billion loss for 2020.

Over the past several years, China’s corporate debt to GDP ratio has been steadily increasing. In 2017, it hit a record 160 percent, up from 101 percent 10 years earlier. Chinese leader Xi Jinping has made it a priority to rein in the debt, particularly in China’s $10 trillion shadow banking sector. Local government financing vehicles (LGFV) have defaulted on many trust loans in the shadow banking system, but not on a public bond. So far, this year, 915 million of LGFV have defaulted. This so-called hidden debt of local governments has become so pervasive that Beijing has named it a national security issue.

Investor confidence has been shaken, as both private and state-linked companies, once considered safe investments, have been in default. The danger is that investors, fearing contagion, might panic and begin selling off both good and bad debt, driving down the market.

A complete collapse of Evergrande could cause widespread economic turmoil and even civil unrest. The future of Evergrande and the Chinese economy depends on whether or not the central authorities will allow Evergrande to go into default, leaving its creditors high and dry, or if the Chinese Communist Party will intervene in order to maintain stability.

Views expressed in this article are the opinions of the author and do not necessarily reflect the views of The Epoch Times.

Antonio Graceffo

Follow

Antonio Graceffo, Ph.D., has spent over 20 years in Asia. He is a graduate of Shanghai University of Sport and holds a China-MBA from Shanghai Jiaotong University. Antonio works as an economics professor and China economic analyst, writing for various international media. Some of his China books include “Beyond the Belt and Road: China’s Global Economic Expansion” and “A Short Course on the Chinese Economy.”

Biden Administration Warns States Federal Debt Crisis Might Trigger Recession

September 19, 2021 Updated: September 19, 2021

The Biden administration has issued a warning that the pending federal debt crisis might trigger an economic recession that would affect economic growth and trigger job losses across the United States.

“Hitting the debt ceiling could cause a recession. Economic growth would falter, unemployment would rise, and the labor market could lose millions of jobs,” the White House said in a letter (pdf) to state and local governments that was released Sept. 17.

Arguing that Congress needs to raise or suspend the U.S. debt ceiling, the administration said the debt crisis may affect the country’s recovery after the CCP (Chinese Communist Party) virus pandemic. In July, Congress missed its deadline to suspend or raise the debt limit, prompting several recent warnings from Treasury Secretary Janet Yellen that her agency will exhaust its cash reserves.

“The U.S. economy has just begun to recover from the pandemic and a manufactured debt ceiling crisis would threaten the gains we’ve made and the future recovery,” the White House said.

If the United States defaults for the first time in its history should Congress not act, a number of federally funded programs could be stopped, the White House letter continued to say. That includes Medicaid, infrastructure funding, and disaster relief efforts.

“If the U.S. defaults on its obligations, the ripple effects will hurt cities and states across the country,” the letter added, further saying that the S&P 500 could plunge due to a prolonged standoff.

The warning comes after Congress approved trillions of dollars in spending and relief packages in recent months, while Democrats are currently pushing a $3.5 trillion budget reconciliation bill designed to provide funding for a variety of new programs targeting social welfare, the climate, and some infrastructure projects. Because trillions of dollars have been injected into the economy, some have expressed concern that the measures are triggering a rise in inflation, which has rattled markets in recent weeks, although the Federal Reserve has said it believes the inflation spike is transitory.

Yellen recently spoke with Senate Minority Leader Mitch McConnell (R-Ky.) to try to get Republican senators on board with the debt limit increase. The GOP leader told media outlets, however, that he doesn’t believe any Republicans would vote to raise the debt limit.

“I can’t imagine a single Republican in this environment that we’re in now—this free-for-all for taxes and spending—to vote to raise the debt limit,” McConnell told Punchbowl News.

But some Biden administration officials have said they’re optimistic that Congress will take action in the coming weeks to avoid a crisis.

“We have seen this done in a bipartisan way consistently and the best way to do this is without a lot of drama, without a lot of self-inflicted harm to the economy and to our country, and that’s what we’re going to do,” National Economic Council Director Brian Deese was quoted by Bloomberg News as saying. “Now there’s a lot of posturing on this issue, but we’re confident at the end of the day we’ll get this done.”

The current national debt total is about $28.7 trillion. In July 2019, Congress suspended the debt ceiling, which prevents the federal government from taking on a certain amount of national debt for two years.

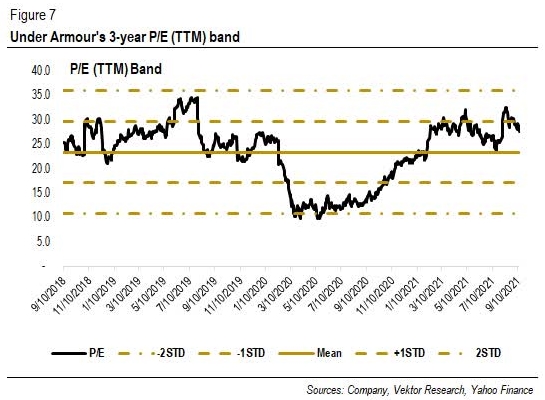

https://seekingalpha.com/article/4455317-under-armours-story-has-not-yet-changed

Under Armour’s Story Has Not Yet Changed

Sep. 15, 2021 5:48 AM ETUnder Armour, Inc. (UA), UAA12 Comments

Summary

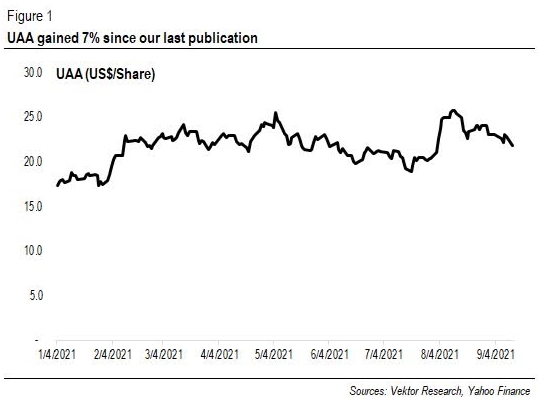

- Since our last publication, the stock price has increased by 7%, fueled by the solid 2Q21 results.

- In our view, despite Under Armour’s recent success, it was the industry’s demand pick-up that fueled the surge in revenue growth, which, in turn, drove the stock price.

- The story has not yet changed. Margins have been improving, and free cash flows continue to expand. But we have not yet seen a solid long-term revenue growth boost.

- Looking forward, we see that possible short-lived headwinds, such as supply constraints, could erase the positive sentiment on the stock.

Investment Thesis

Under Armour’s (NYSE:UA) (NYSE:UAA) stock price surged following the solid 2Q21 results last month. New products, such as apparel and footwear, are selling well. However, we think that those successes have not yet indicated that they could lift Under Armour’s long-term top-line growth rates, which have slowed down since 2017. The reason is that consumers may buy more sporting goods after social activities have restarted, as other players, too, recorded jaw-dropping results in the last quarter. Hence, expressing a slight reservation, we think the 3Q21 and 4Q21 results could give us a clearer picture of whether Under Armour has already been on the right track.

Have We Changed Our Stance?

Since our last publication titled “Under Armour Is Searching for A Much-Needed Revenue Growth Boost,” Under Armour (NYSE:UAA) has gained about 7% (per 13th September). Our thesis presented that the pandemic may encourage people to exercise more, possibly moving the athletic performance back on track, but that Under Armour must look for a long-term revenue growth boost amid the intense competition. Then, in early August, the much-awaited 2Q21 results bumped the stock price, which increased by more than 20% in total before it cooled off. This article will discuss whether the recent development suggests that Under Armour has finally found its long-awaited revenue growth boost.

Sources: Vektor Research, Yahoo Finance

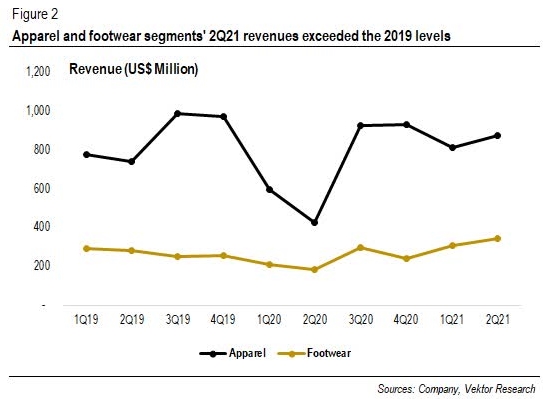

Satisfying is the apparel and footwear segments, whose revenues exceeded the 2Q19 and 2Q20 levels. During the 2Q21 earnings call, the company said that apparel products sold well, mentioning that running products (Iso-Chill), men’s bottom (Unstoppable), and women’s leggings (Meridian and No-Slip Waistband technology) had strong sell-through. Moreover, Patrik Frisk, the CEO of Under Armour, alluded to the fact that better pricing was at play: Flow’s price tag of US$160 far exceeded HOVR’s US$100-US$120 at inception. When asked whether the new products will help drive the top-line growth, Mr. Frisk said that Under Armour’s efforts to build franchises and stick to the “athletic performance” strategy bore fruit for the past few years.

Things appear to go smoothly for Under Armour, supported by strong sales and better pricing. But is that the case? Has the company’s better outlook been driving up the stock price? Or perhaps, has the optimism following the sporting goods industry’s recovery been the primary cause for the hype?

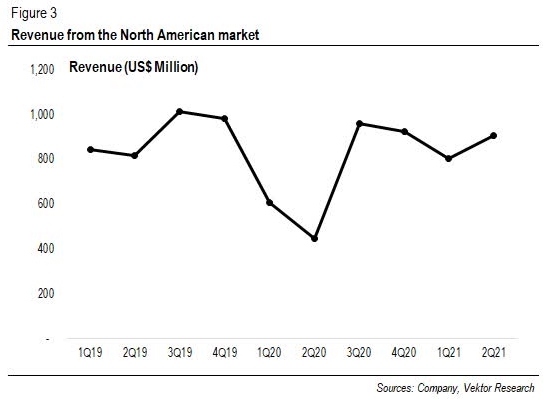

Sources: Company, Vektor Research

In 2Q21, revenue from the North American market grew at a staggering rate (+101% Y/Y) from the much lower base in the same period last year. Comparing the figure with the revenue in 2019 will bring us to 10.9% (Y/Y) of revenue growth, supported by “stronger sell-through and higher demand,” the company said.

Sources: Company, Vektor Research

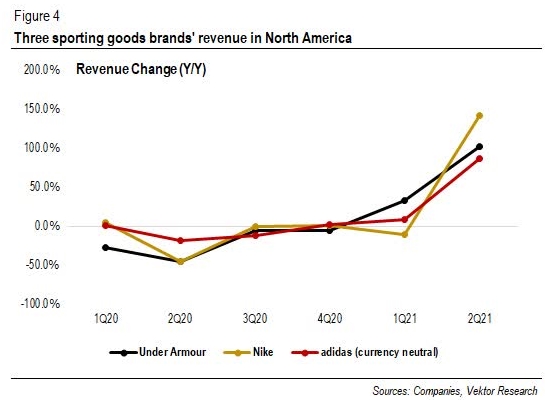

However, the jump could mean that Under Armour is recouping its losing sales, just as Under Armour’s competitors, Nike (NYSE:NKE) and adidas (OTCQX:ADDYY), are getting back on their feet, as seen in Figure 4. In addition, through the 4Q21 earnings call (as of 31st May 2021), Nike said that the company recaptured the delayed revenue, resulting in an “incredibly strong” revenue. In other words, we are saying that the hefty growth rate in the last quarter was not so much because of company-specific factors as because of the overall industry’s recovery.

Of course, the recently launched Flow franchise has indeed been a success. In addition, we read reviews and comments on Flow shoes, and those reviews are generally positive despite some voices concerning the relatively high price. But, expressing our cautious view, we are slightly unsure whether the franchise can carry forward Under Armour’s slowing revenue growth rates for the past few years.

Why? Consider, for example, that the sales surge was due to consumers simply buying more products following the prolonged social restrictions, which had forced gyms to close down. If that is the case, the tailwinds may be short-lived-at least not as long as we expect. Furthermore, the company mentioned that HOVR Machina, with the popular Pebax propulsion plate, has been a success, too. Yet, we have not seen a significant change in revenue growth.

Indeed, Flow’s success has indicated that Under Armour is moving in the right direction. However, will it become the much-needed growth boost for Under Armour?

Sources: Companies, Vektor Research

The management estimates Under Armour’s growth rate to slow down in the 3Q21 and be flat in the 4Q21, implying that the North American market faces headwinds, such as “lower expected sales to the off-price channel” and “supply and demand constraints.” For example, Under Armour is in the process of cutting down its wholesale partnerships, bringing down from about 12,000 to 10,000. Moreover, according to Yahoo, the closure of factories in Vietnam has hampered supplies for athletic brands. As a result, the management estimates the North American market will be closer to the 2019 levels in terms of revenue.

As we move forward, there may be short-lived headwinds coming into the second half of this year. Therefore, we may not see a positive sentiment in the subsequent quarters to drive the stock price. As a result, to reiterate our stance, we have not yet witnessed a strong catalyst that could lift Under Armour’s long-term revenue growth rates, although the Flow franchise has showcased its success, at least in these few months.

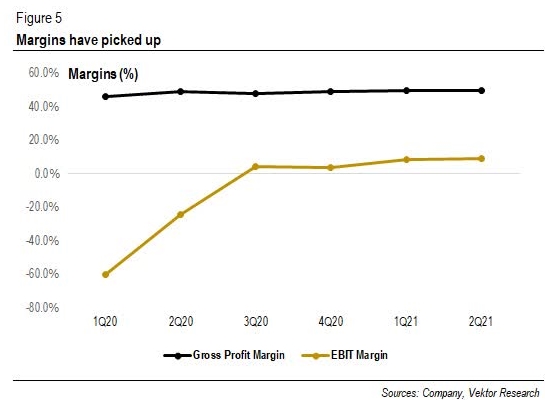

But the story has not yet changed. Under Armour has been doing nothing but a great job in expanding its margins, in our view. In 2Q21, gross profit and EBIT margins stood at 49.5% and 9.0%, respectively, far surpassing the 5-year average (excluding last year) of 46.3% and 4.7%.

Sources: Company, Vektor Research

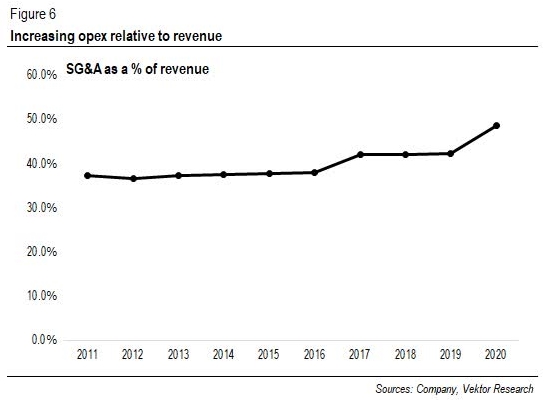

When asked about the company’s double-digit operating margin target, David Bergman, the CFO of Under Armour, said that as DTC made up a larger percentage, increasing operating costs could become the headwind going into the 4Q21. However, this is hardly a concern, in our opinion. In reality, in the last five years, operating expenses have already been on the upper side. From 2011 to 2015, SG&A expenses as a percentage of revenue sat at around 37.5%. From 2016 to 2020, the percentage went up to between 38% and 42% (48.5% in 2020).

Excluding the 2020 result, we found that the 5-year CAGR of marketing and other costs outpaced the 5-year CAGR of revenue. In other words, we are saying that the significant operating margin boost stems from things related to gross margin, not from the reduction of SG&A expenses. Take, for example, discounts. In this case, the migration to a more DTC-centric business is essential to instill the company’s perceived brand towards a premium one. Additionally, with its less reliance on the wholesale market, Under Armour can sell full-priced products. Therefore, looking forward, we believe that the company’s target of double-digit operating margin may be within reach.

Sources: Company, Vektor Research

Valuation

After delivering a solid performance in the last quarter, the company’s valuation looks more reasonable than before. Under Armour’s P/E (TTM) stood at 28x, lower than that of Nike (45x), adidas (35x), and Lululemon (NASDAQ:LULU) (67x), according to Yahoo Finance. So, is Under Armour a buy? Margins have been improving, and free cash flows, too, continue to recover. However, consistent with our thesis, we believe that Under Armour needs a strong catalyst that could help drive its long-term top-line growth rate because the lack of growth has put pressure on the stock price in the last few years, in our view.

Sources: Company, Vektor Research, Yahoo Finance

Our Thoughts

In the last quarter, the company’s resilience has uplifted the stock price: revenue growth pick-up and improving margins. However, we think that the strong results did not suggest a better future performance. In reality, Under Armour’s competitors have also shown signs of revenue growth pick-up. In other words, we are saying that the whole industry is simply in a period of recovery. But what we are looking for is a long-term revenue growth boost.

Valuation-wise, it is true that Under Armour looks attractive compared with other players. Moreover, it is also true that margins have been improving and that free cash flows are expanding. However, according to our thesis, the lack of top-line growth has pressured the stock price. In addition, upcoming headwinds could erase the positive sentiment that recently drove the stock price.

If I were an investor looking to invest, I would look for another sporting goods company that can offer more promising long-term revenue growth while keeping tabs on Under Armour. If I already had Under Armour, I would hold the stock, at least until the 3Q21 or 4Q21 results, to see whether the new products show further signs that Under Armour can get back on track soon. If you have any thoughts, please do not hesitate to comment below.

This article was written by

Vektor Research is an Indonesian-based independent research company. Founded in 2021, Vektor Research aims… more

Long/Short Equity, Value, Growth, Event Driven

Contributor Since 2021

Vektor Research is an Indonesian-based independent research company. Founded in 2021, Vektor Research aims to produce high-quality research and to promote independent opinions. Furthermore, Vektor Research plans to offer on-demand research service and corporate advisory in the future.

We will focus on writing under covered and IPO stocks here for Seeking Alpha. In addition, we also do research on Indonesian stocks published on our website, while the shorter version will also be published on the Instablog.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Research reports are written based on analysis and expectations of the analyst(s), and the analyst(s) is required to include sources for external data included in the analysis. The research analyst(s) is not responsible for any inaccuracy caused by human errors. Still, Vektor Research will make sure, with reasonable efforts, to reduce such mistakes as minimal as possible. Please note that the forecasts do not guarantee any future performance. Vektor Research, along with the analyst(s), is not responsible for any loss, expenses, and the reader’s decision-making. The reports do not force readers to act towards any securities.

https://seekingalpha.com/article/4455910-boeing-stock-the-bullish-outlook

Boeing Stock: The Bullish Outlook

Sep. 20, 2021 1:20 PM ETThe Boeing Company (BA)17 Comments10 Likes

Summary

- Single aisle aircraft forecast exceeds pre-pandemic levels.

- Projections for wide body aircraft are still down 8% compared to pre-pandemic levels.

- The long-term trend remains directed upward.

- I do much more than just articles at The Aerospace Forum: Members get access to model portfolios, regular updates, a chat room, and more. Learn More »

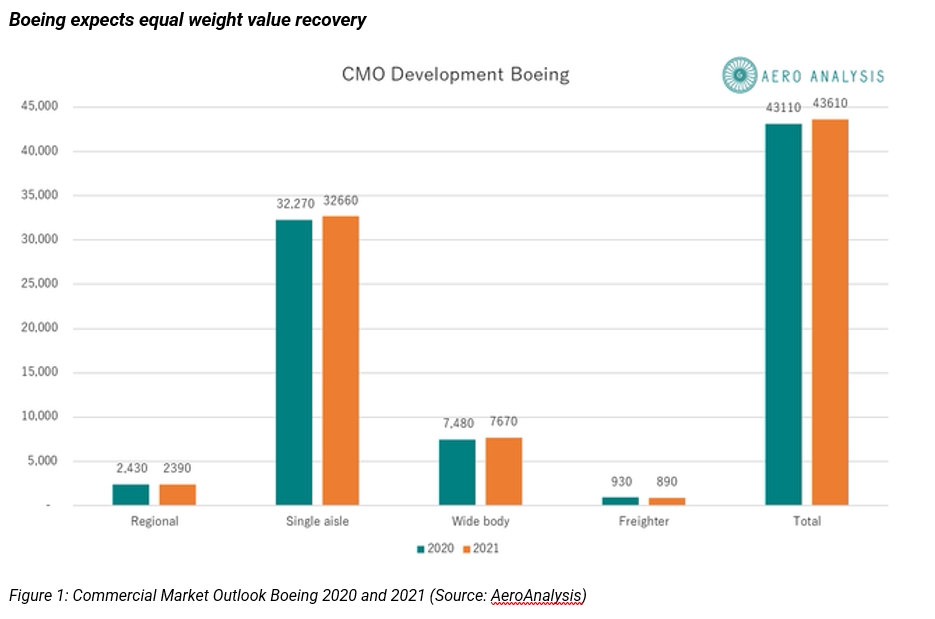

Figure 1 provides a tiny bit of context on how the 20-year forecast has developed since last year. Overall, the outlook has increased by 500 units from 43,110 expected deliveries to 43,610. That number is still down 430 units from the 2019 CMO, which we consider a baseline that Boeing and the industry would want to return to. So, what does the number mean? With over half of the decline compared to the baseline being recaptured in this year’s outlook, Boeing seems to be expecting a very fast market recovery for aircraft.

Late 2024 is what Cirium, a data analytics provider for the aviation industry, is using as their baseline, and Boeing seems to be expecting a stronger recovery that’s in line with expectations from IATA. Following the path from small aircraft to bigger aircraft, Boeing expects the recovery to be completed by 2023-2024. So, Boeing is expecting the recovery to take at least a year less.

With that assumption comes a downward revision of 40 units for regional jet deliveries. The longer the recovery takes, the more prominent the role of the regional jets would be. While Boeing’s assumptions on the recovery have not changed drastically, it seems that optimism on the recovery trajectory goes at the expense of regional jet forecasts as using bigger planes might becoming more compelling once again. Single aisle delivery forecasts were hiked by 390 units covering nearly 80% of the hike compared to last year. It seems like a huge deal, but one should consider that on monthly production levels it equates to slightly more than 1.5 aircraft, and assuming a perfect split between Boeing and Airbus which is optimistic this would mean that new projections support the delivery of roughly one additional single aisle jet per month. So, a big increase in absolute numbers but in relative sense it is very small around 1%. What’s more interesting is that the outlook for single aisle aircraft already is above the 2019 levels.

More interesting to look at is what happened to wide body projections. Last year the projections for wide body aircraft deliveries were dropped by 10%. This year, it is up by 190 units. Given that a widebody aircraft sells for 2-3 times the value of a single aisle jet, we can conclude that in terms of value the wide body passenger aircraft and single aisle aircraft have equal contributions to the hiked forecast but wide body deliveries remain down 8% from the baseline. What also should be considered is that around 360 aircraft wide body aircraft have been retired early according to our own research. With that in mind, one would have hoped for a stronger hike in the expected wide body deliveries. So, the wide body market is really showing that full recovery is still going to take a while but it should also be mentioned that the current projections leave a lot of room for increases in production rates on the wide body programs.

For the wide body freighter market, the forecast was reduced by 40 units year-over-year and that’s interesting because worldwide we’re seeing issues with logistics. But it seems that the dedicated freighter market is not expected to benefit over the longer term. There are two explanations for that. The first one is that as international wide body traffic recovers, belly cargo capacity will come online again, and the second explanation is that some passenger aircraft have been converted for freighter services permanently. So, Boeing’s strength in the converted freighter market is biting the company back in the dedicated freighter market.

Boeing’s delivery profile remains backloaded

Source: Boeing

What remains interesting to highlight are the 10-year delivery outlooks. The baseline 10-year outlook has not been specified by Boeing but the jet maker did say that the 18,350 aircraft deliveries expected over a decade were down 11% compared to the baseline which led to our conclusion that the pandemic will be resulting in a 11% adverse impact over a decade, which is substantial. This year, Boeing expects the 10-year delivery numbers to total 19,330 units marking a 5% increase driven by higher single aisle deliveries (+800) and higher wide body deliveries (+180). Those numbers were expected to be better, signaling the recovery in production and delivery rates with an important role for the Boeing 737 MAX production and delivery ramp and a release of wide body aircraft from inventory. So, the 10-year rolling number improving is not so much related to turning more bullish on the recovery but more that a year with low delivery volumes (last year) disappearing from the rolling number and a year with more deliveries replacing it. So, we cannot say that recovery is accelerating beyond what was earlier thought. This also is demonstrated by the rise in the 10-year forecasts being 980 units vs. a 500 unit hike in the 20-year forecast.

So, the numbers are moving in the positive direction. However, what we also have observed is that the delivery profile remains backloaded. In 2019, around 47% of the deliveries were expected in the first half of the 20-year outlook and in 2020 this reduced to 43% only to bump up modestly to 44% in the most recent outlook. Freighters and regional jets are the exception to that trend as reduced demand in the near term somewhat has strengthened the use case for regional jets and the disappearance of belly capacity on wide body aircraft vanished when international passenger transport was reduced significantly, resulting in an uptick in demand for freighter aircraft. While Boeing has had its fair share of headwinds over the past years, the backlog which is visualized in the TAF Boeing Backlog Monitor shows that the jet maker has thousands of aircraft in the order books and more to come in the coming years.

Conclusion

What we’re seeing is that Boeing is expecting a return to pre-pandemic conditions roughly a year earlier than some data analytics companies and possibly that’s also what Michael O’Leary from Ryanair hinted on when he said he did not share Boeing’s optimistic pricing scenario which without doubt is related to forecast demand. What’s most striking to me in the CMO is that wide body demand forecasts are still at a level where I would say investing in Boeing as well Airbus is a no-brainer. Boeing’s forecasts tend to be conservative, so in my view while I’m often critical on Being I do think that for long-term investors there’s a lot of reason to invest or remain invested in Boeing as well as Airbus.

While it seems that Boeing is more positive about the future, it should be noted that the 20-year outlooks are rolling numbers so last year was a year with lower deliveries and in this year’s outlook that year is obviously replaced with a production year 19 years from now when production is expected to be good. So, it’s very important to keep in mind that higher anticipated deliveries are not necessarily an indication that recovery timelines have accelerated. However, what the numbers in my view do show is that the commercial aircraft industry is very resilient and for Boeing the art will be to capitalize on the long-term trend and resilience by developing appropriate products.

This article was written by

Aerospace & Defense, Airlines, Commercial Airplanes

Contributor Since 2013

Dhierin is a leading contributor covering the aerospace industry on Seeking Alpha and the founder of The Aerospace Forum. With his Aerospace Engineering background he has a more indepth knowledge about aerospace products enabling him to cover a complex niche. Most of his reports will be about companies in the aerospace industry or airlines industry, comparing products and looking at market forecasts providing investors with unique and thorough insights. Dhierin has accumulated nearly 20 million views never failing to spark healthy and thoughtful discussions for investors and aerospace professionals.

His reports have been cited by CNBC, the Puget Sound Business Journal, the Wichita Business Journal and National Public Radio. His expertise is also leveraged in Luchtvaartnieuws Magazine, the biggest aviation magazine in the Benelux.

AeroAnalysis offers wide variety of services, ranging from providing data and cost models to consultancy possibilities. Check out our website for more information. Though we believe in the strong nature of our analysis, we are in no way giving buy or sell recommendations and advise everyone to do their own due diligence before making investment decisions.

Disclosure: I/we have a beneficial long position in the shares of BA, EADSF either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

As Democrats wrestle over funding for their $3.5 trillion spending package, some investors may be itching to sell appreciated assets ahead of possible tax hikes.

But the decision is more complex than rate increases alone.

House Democrats have floated raising the top federal long-term capital gains tax to 25% from 20%, according to a summary released by the Ways and Means Committee. If enacted, the highest earners would pay a total of 28.8% combined with the 3.8% surcharge on net investment income.

The proposed changes are retroactive for sales after Sept. 13, 2021, making it tough to lock in lower rates. However, lawmakers may still push the effective date.

In the meantime, investors eager to offload assets need to assess their entire tax picture before selling, financial experts say.

“When it comes to taxes, the devil’s always in the details,” said certified financial planner Peter Palion, founder of Master Plan Advisory in East Norwich, New York.

Top earners may be tempted to sell before the proposed changes to save 5% in taxes. But taking those gains off the table may trigger higher costs elsewhere, he said.

Whether someone’s nearing retirement or they have already left the workforce, selling assets at a profit increases their modified adjusted gross income, and may have other consequences, Palion said.

Retirees should consider how having a higher income could affect their monthly Medicare costs in the future.

Medicare uses your modified adjusted gross income from two years prior for premiums – meaning your 2021 income determines whether you’ll see higher premiums in 2023.

Investors with more than $88,000 ($176,000 for joint filers) modified adjusted gross income for 2021 will pay an extra surcharge every month, known as the Income Related Monthly Adjustment Amount or IRMAA, for Medicare Part B and Part D.

Surcharges for Part B medical insurance and Part D prescription drug coverage in 2021 may be as much as $504.90 and $77.10, respectively.

Another possible pitfall, Social Security taxes, kick in once half of someone’s benefits plus modified adjusted gross income exceeds $25,000 ($32,000 for married filers), making up to 50% of Social Security income taxable.

Once the same calculation passes $34,000 ($44,000 for joint returns), up to 85% of someone’s benefits may be taxable.

Savings for heirs

Moreover, if older investors want to pass assets to their children, they may defer taxes by holding their investments until death, Palion said.

This way, the heirs’ inheritance gets a so-called step-up in basis, which generally adjusts the assets’ purchase price to the value on the date of death, he said.

The benefit of the step-up in basis is that the heir receives the asset without facing taxes on what could be years’ worth of unrealized gains.

Before you impulsively quit your job as part of the ‘Great Resignation,’ do these four things

jayk7 | Moment | Getty Images

If you are like millions of Americans, you may dream of quitting your job.

You may be burned out, want to do something new or are simply inspired to find something better thanks to the “Great Resignation” wave happening across the country.

Several surveys have shown that many people want to walk away from their jobs.

In fact, a poll released in September by the Society for Human Resource Management found that over 40% of U.S. workers are actively searching for a new job right. The survey of 1,150 employed Americans was conducted from July 2 to 8.

“This generation-defining traumatic event has made them take a long, hard, honest look at how they constructed their life, or how their life was constructed for them,” said organizational psychologist Melissa Doman.

They may be asking themselves how they got there and if this job is really what they want. Yet not everyone is slowing down to ask themselves these reflective questions, she said.

“They’re so busy freaking out about the world literally and figuratively burning,” added Doman, author of “Yes, You Can Talk About Mental Health at Work…Here’s Why (And How To Do It Really Well).”

To be sure, how you quit matters. The last thing you want to do is act on impulse, or even rage quit. You could wind up tarnishing your reputation and may have a difficult time explaining why you left your last job to potential future employers.

“This can be a red flag,” said Toni Frana, a Destin, Florida-based career coach with FlexJobs.

If you have the impulse to hand in your walking papers, here’s what to do first.

1. Cope during work

Instead of bursting into your boss’ office or firing off an email stating “I quit,” leave your desk and take a walk. Do some quick meditation at your desk or vent your frustrations to a friend.

“All of those things will redirect the thought process for the time being and create a sense of calmness,” Frana said.

You can also remind yourself that this situation is temporary, Doman added.

“Making sure you have a laugh, reminding yourself that how you feel is not permanent, that is what can help the most with staving off those feelings of learned helplessness,” she said.

However, if your job situation is negatively impacting your mental health in and outside of work and you can financially afford to quit without another lined up, do so.

“It’s a risk, but if the price is your mental health, it’s too expensive,” Doman said.

2. Know your ‘why’

Be honest with yourself about why you want to leave your job, and even write it down, Doman suggests.

What are the circumstances and what is your motivation? Is it because you are tired of the job and want something new? Do you want to own your own business or leave a boss who is a bully?

3. Create a plan

After you know your why, figure out what you are going to do with that information. Come up with actionable steps you need in order to go from theory to practice, Doman said.

Being intentional rather than impulsive about your next move will make you feel a lot more settled.

When targeting possible new companies, be very clear about your top needs and preferences in a new role. Come up with a list of the top five non-negotiable things you need, as well as what you would prefer to have in your next job.

4. Search for a job

When you start looking for your next job, set reasonable goals, such as spending a certain number of minutes a day on your search, FlexJobs’ Frana suggests.

Break it into small pieces you can manage and still remain in control, she said.

Update your resume and start networking. Not only reach out to people who may be in a field or company you like, also speak to those who have successfully been through a similar situation — like changing industries or roles.

Just be mindful about who is giving you the advice. Someone who hasn’t been through the same process as you or did quit his or her job impulsively may not be the right fit.

In the end, it’s about making an informed decision.

“You want to go towards something as opposed to running away from something,” Doman said.

SIGN UP: Money 101 is an 8-week learning course to financial freedom, delivered weekly to your inbox.

CHECK OUT: 5 side hustles for people in their 60s that can bring in $10, $50, or even $500 per hour via Grow with Acorns+CNBC

Disclosure: NBCUniversal and Comcast Ventures are investors in Acorns.

Pfizer CEO Albert Bourla predicts normal life will return within a year and adds we may need annual Covid shots

Catherine Clifford@IN/CATCLIFFORD/@CATCLIFFORD

KEY POINTS

- “Within a year I think we will be able to come back to normal life,” Pfizer CEO Albert Bourla said in an interview on ABC’s “This Week” on Sunday.

- Bourla said “the most likely scenario” is the need for annual coronavirus vaccine shots.

There will be a return to normal life within a year, Pfizer CEO and Chairman Albert Bourla said on Sunday, adding that it’s likely annual Covid vaccination shots will be necessary.

“Within a year I think we will be able to come back to normal life,” Bourla said in an interview on ABC’s “This Week.”

Returning to normal life will have caveats, he said: “I don’t think that this means that the variants will not continue coming, and I don’t think that this means that we should be able to live our lives without having vaccinations,” Bourla said. “But that, again, remains to be seen.”

Bourla’s prediction about when normal life will resume is in keeping with that of Moderna CEO Stéphane Bancel. “As of today, in a year, I assume,” Bancel told the Swiss newspaper Neue Zuercher Zeitung, according to Reuters on Thursday, when asked for his estimate of a return to normal life.

In order to make that happen, Pfizer’s Bourla suggested it is likely annual coronavirus vaccine shots will be needed.

“The most likely scenario for me is that, because the virus is spread all over the world, that it will continue seeing new variants that are coming out,” Bourla said. “Also we will have vaccines that they will last at least a year, and I think the most likely scenario is annual vaccination, but we don’t know really, we need to wait and see the data.”

On Friday, the head of the Centers for Disease Control and Prevention Dr. Rochelle Walensky authorized the distribution of Pfizer and BioNTech’s Covid-19 booster shots for those in high-risk occupational and institutional settings, a move that overruled an advisory panel. Walensky approved distributing the booster shots to older Americans and adults with underlying medical conditions at least six months after their first series of shots, in line with the advisory panel.

The World Health Organization strongly opposes a widespread rollout of booster shots, saying wealthier nations should give extra doses to countries with minimal vaccination rates.

Bourla said on Sunday it is “not right to decide if you’re going to approve or not boosters” on any other criteria than “if the boosters are needed.”

https://platform.twitter.com/embed/Tweet.html?creatorScreenName=CatClifford&dnt=false&embedId=twitter-widget-0&features=eyJ0ZndfZXhwZXJpbWVudHNfY29va2llX2V4cGlyYXRpb24iOnsiYnVja2V0IjoxMjA5NjAwLCJ2ZXJzaW9uIjpudWxsfSwidGZ3X2hvcml6b25fdHdlZXRfZW1iZWRfOTU1NSI6eyJidWNrZXQiOiJodGUiLCJ2ZXJzaW9uIjpudWxsfSwidGZ3X3NwYWNlX2NhcmQiOnsiYnVja2V0Ijoib2ZmIiwidmVyc2lvbiI6bnVsbH19&frame=false&hideCard=false&hideThread=false&id=1440326022474334209&lang=en&origin=https%3A%2F%2Fwww.cnbc.com%2F2021%2F09%2F26%2Fpfizer-ceo-albert-bourla-said-we-may-need-annual-covid-shots.html&sessionId=25f8329b20a0ea0cfa2b9ef411e6b5488c2f27c2&siteScreenName=CNBC&theme=light&widgetsVersion=1890d59c%3A1627936082797&width=550px On Tuesday, Tom Frieden, former head of the CDC, criticized Moderna and Pfizer for not sharing vaccination intellectual property more broadly to help accelerate global vaccination rates.

“While focusing on selling expensive vaccines to rich countries, Moderna and Pfizer are doing next to nothing to close the global gap in vaccine supply. Shameful,” Frieden said tweeted on Twitter.

Bourla said it is not a good idea to wave intellectual property.

“Intellectual property is what created the thriving life sciences sector that was ready when the pandemic hit,” Bourla said. “Without that, we wouldn’t be here to discuss if we didn’t with us or not because we wouldn’t have vaccines … Also, we are very proud of what we have done. I don’t know why [Frieden] is using these words. We are very proud. We have saved millions of lives.”

Pfizer is selling vaccines at different prices to countries with different levels of wealth. Developing countries are buying vaccines at cost from Pfizer, Bourla said. And Bourla pointed to the fact that Pfizer is selling one billion vaccine doses to the U.S. government at cost. The U.S. government is then donating those vaccine doses “at no cost, completely free, to the poorest countries of the world,” he said.

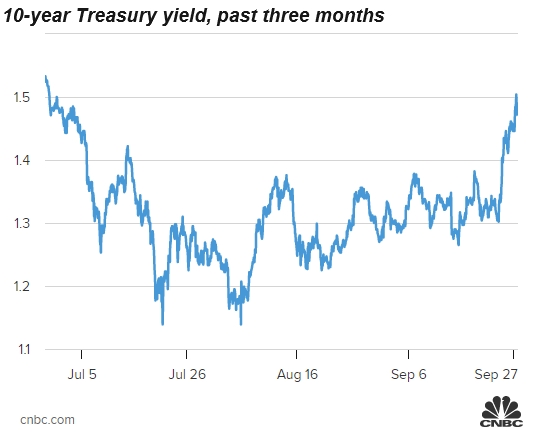

Dow rises 100 points as 10-year yield retakes key 1.5% level, tech shares weigh on broader market

U.S. stocks were split on Monday as traders braced for the final week of a volatile September and Treasury yields rose.

The S&P 500 fell by 0.3% and the Nasdaq Composite shed 0.7% as tech stocks showed weakness in early trading. The Dow Jones Industrial Average rose about 120 points as energy stocks and bank shares pushed higher.

The divergence for the major averages came as Treasury yields pushed higher. The 10-year Treasury yield increased on economic optimism and inflation fears, briefly topping 1.5% on Monday. That’s the highest since June and up from 1.30% at the end of August.

“We believe that these [bond market] moves have provided the spark for another ‘Value Rip’ across equity markets. In our view, the direction of longer-term interest rates should remain the #1 driver of market returns, sector rotation & thematic performance in the weeks ahead,” Chris Senyek of Wolfe Research said in a note to clients.

10-year Treasury yield, past three months

Line chart with 1372 data points.

The chart has 1 X axis displaying Time. Range: 2021-06-27 19:30:00 to 2021-09-27 12:30:00.

The chart has 1 Y axis displaying values. Range: 1.1 to 1.6.

Jul 5Jul 26Aug 16Sep 6Sep 271.11.21.31.41.51.6cnbc.com

Alphabet, Apple and Nvidia were lower in early trading, weighing the S&P 500 and Nasdaq. Tech stocks are seen as sensitive to rising interest rates because higher debt costs can make long-term growth less attractive to investors.

Also weighing on sentiment was a potential government shutdown to end the week.

Stocks linked to the economic comeback led the early gains as U.S. Covid cases continued to roll over.

U.S. cases averaged about 120,000 per day over the last week, according to data compiled by Johns Hopkins University, down from a 7-day average of more than 166,000 cases at the peak of this latest wave in early September. Pfizer CEO Albert Bourla said on Sunday that he thought the U.S. could return to normal “within a year” though annual vaccinations might be needed.

Carnival Corp rose 4.5% and United Airlines added 1.8% in early trading. Shares of Boeing jumped 2%.

The rise in yields appeared to boost financial stocks on Monday, with the KBW Bank Index climbing 2.8%. Shares of Goldman Sachs and JPMorgan Chase rose more than 2%, making them some of the best performers in the Dow.

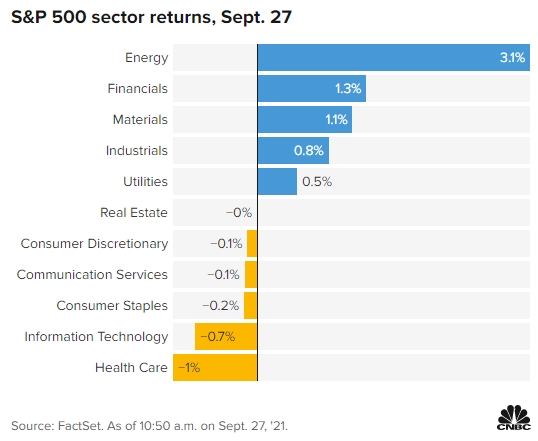

Exxon Mobil and Occidental Petroleum led gains in the energy sector as WTI crude continued its September run, topping $75 a barrel.

https://datawrapper.dwcdn.net/eoMEj/1/ Additionally, the August reading for durable goods orders came in well above expectations on Monday, powered in large part by a jump for the transport sector.

Government shutdown?

Investors are monitoring the progress in Washington as lawmakers try to prevent a government shutdown, a default on U.S. debt and the possible collapse of President Joe Biden’s sweeping economic agenda.

House Speaker Nancy Pelosi said Sunday that she expects the $1 trillion bipartisan infrastructure bill to pass this week, but voting on the legislation may be pushed back from its original Monday timeline.

Congress must pass a new budget by the end of September to avoid a shutdown, and lawmakers must also figure out a way to increase or suspend the debt ceiling in October before the U.S. would default on its debt for the first time.

“DC will start garnering more attention in the coming weeks as the political calculus around passing infrastructure bills and the debt ceiling debate likely guarantees some market moving headlines,” wrote Tavis McCourt, institutional equity strategist at Raymond James.

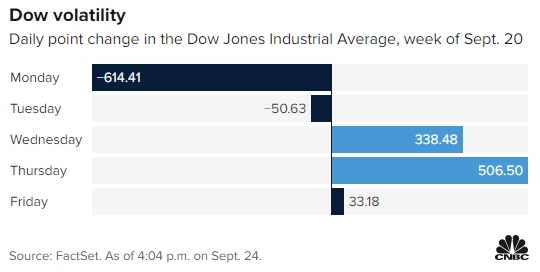

Wall Street is coming off a roller-coaster week amid a slew of concerns from the debt crisis of China’s real estate giant Evergrande, to the Federal Reserve’s signal on rollback in monetary stimulus, and to Beijing’s crackdown on cryptocurrencies. Still, major averages managed to wipe out steep losses earlier in the week and eke out small gains.

https://datawrapper.dwcdn.net/tGiG9/1/ The blue-chip Dow finished the week 0.6% higher, breaking a three-week losing streak. The S&P 500 rose 0.5% on the week, while the tech-heavy Nasdaq Composite edged up 0.02% last week.

“The market recovery indicated that the buy-the-dip mentality remains,” Mark Hackett, chief of investment research at Nationwide, said in a note.

So far, September is living up to its reputation for volatility and weakness as major averages have all registered modest losses. Entering Monday, the S&P 500 was off by 1.5%, on track to post its first negative month since January. The broad equity benchmark is about 2% off its record high from Sept. 2. The Dow was down 1.6% for the month, while the Nasdaq had slipped 1.4%.

But overall, investors continue to buy the dip for stocks. The S&P 500 fell as much as 4% from its record during the month before turning around. Friday was 224 trading days since the last 5% pullback, the 8th longest streak since 1930, according to Goldman Sachs.

“We continue to exercise caution in the near term, especially as we enter the seasonally weakest part of the year (late September — mid-October),” Larry Adam, CIO at Raymond James, said in a note. “However, given continued robust economic growth, our bias is to hold existing equity exposure or add opportunistically on weakness.”

Elsewhere, bitcoin rebounded about 2% to $43,454 after dropping 5% on Friday. The sell-off came after China’s central bank declared all cryptocurrency-related activities illegal.

Stocks face another turbulent week as the third quarter winds down

Patti Domm@IN/PATTI-DOMM-9224884/@PATTIDOMM

KEY POINTS

- Volatility could be the big story again for markets in the week ahead, as investors react to recent moves in both stocks and bonds.

- The Federal Reserve stays front and center again in the coming week, with Chairman Jerome Powell testifying before Congress and a host of other Fed officials speaking at events.

- Congress must address an appropriations bill in the coming week or the government could shut down by next Friday.

After recent turbulence, markets are likely to close out the final week of the third quarter with another bout of volatility.

Stocks posted big moves in the past week. First, fears of financial contagion coming from Chinese developer Evergrande sent stocks skidding Monday. Those losses were reversed by Thursday, when the market ripped higher. The S&P 500 and the Dow Jones Industrial Average were positive for the week, while the Nasdaq was flat.

“I think this market turmoil has yet to conclude,” CFRA chief investment strategist Sam Stovall said. “Certainly September is doing what it normally does. It frustrates investors.”

The three major stock indexes are also higher for the third quarter.

Strategists say how the market trades in the coming week may be the most important development, after the wild swings in stocks and also the rapid rise in Treasury yields late in the week. The 10-year rate had shot up to 1.46% by Friday after trading at about 1.31% on Wednesday.

https://datawrapper.dwcdn.net/Jk8NC/1/ The S&P 500 was down about 1.5% for September.

“We are getting long in the tooth. The technical indicators are pointing to distribution. We’re seeing prices roll over, breadth roll over. You’re seeing sentiment roll over,” Stovall said, noting the market’s breadth needs to improve, and many stocks are trading below their 200-day moving average.

October is a ‘seismic’ month

“I think October will be true to itself, which is a very volatile month. October’s volatility is 36% higher than the average of the other 11 months of the year,” Stovall added. “Volatility is higher and you have a greater number of pullbacks, corrections and bear markets that either start or end in the month. It is a seismic month.”

Wealth management firm Wellington Shields warns that the fact many stocks have fallen below their 200-day moving average is a negative for the market. Just 59% of the stocks on the New York Stock Exchange remain above it, or in an uptrend, according to the firm. The 200-day moving average is the average of the last 200 closing prices of a stock or index, and it’s viewed as a momentum indicator.

“The rule is that when this 200-day number drops from above 80% to below 60%, it usually goes below 30%. Forgetting that, the real point is that while most stocks may be advancing, barely more than half are advancing enough to be in uptrends. With the market just a few percent below its highs, this is a concern,” Wellington said in a note.

What to watch

In the coming week, there are a few key economic reports including including durable goods Monday and ISM manufacturing Friday. There is also personal consumption expenditure data Friday, which the Federal Reserve monitors for its inflation index.

The Federal Reserve will remain a big focus in the week ahead. There will be a host of Fed speakers, including Chairman Jerome Powell, who testifies twice before Congress on the pandemic and the policy response to it. Treasury Secretary Janet Yellen will join him for the hearings Tuesday and Thursday. Powell also appears on a European Central Bank panel with other central bank leaders Wednesday.

Investors will also be watching Congress in the week ahead, as lawmakers attempts to pass a funding plan in time to avert a government shutdown Oct. 1. The debt ceiling is expected to be part of that debate, but strategists do not expect it to be resolved at the same time. They say this could hang over the markets for several weeks before Congress raises the debt ceiling.

Fed speakers are not expected to provide any new information, but they could fine tune their message after the central bank signaled this past Wednesday that it expects to begin paring down its $120 billion in in monthly bond purchases soon. The Fed also released a new forecast for interest rates, which revealed that half of the 18 Fed officials expect to raise interest rates next year.

“I think what the Fed’s achieved so far is a taper without a tantrum,” Bannockburn Global Forex chief market strategist Marc Chandler said.

“I think a lot of people who invest in the market have a sense they are skating on thin ice, and any crack could be a big one. … People are highly sensitive and nervous because they know valuations are stretched,” he said. “That means we should expect these episodic jumps in volatility.”

Chandler said the market will need to digest the recent moves, particularly the move higher in Treasury yields.

https://datawrapper.dwcdn.net/mTlbt/1/ “What we’ve got to wait for now is finding this new equilibrium. What kind of market should we expect? Trending? Or do we try to find a range?” he said. “I think we find a range. We need some hurdles to pass.” Chandler added that one hurdle is the September jobs report on Oct. 8.

The Fed is expected to taper its $120 billion monthly bond purchases unless there is shockingly weak employment data. “That is the only thing that stands in the way of Fed tapering,” Chandler said.

Wells Fargo’s Michael Schumacher said the quarter end could be quiet in terms of big funds rebalancing. “The equity market bounced around. It’s up on the quarter. That wasn’t much when you compare it to the bond performance,” he said.

The 10-year yield made an unusually volatile round trip move in the third quarter. It was 1.47% on June 30, and it was as high as 1.46% on Friday. In between, it dipped to 1.12% in early August. Schumacher said the bond market could be quieter ahead of the quarter end, and the 10-year yield could then resume its move higher.

Some strategists watch the 10-year Treasury yield as a leading indicator for stocks. It is also linked to moves in technology and other high-growth stocks.

What’s next

Fairlead Strategies founder Katie Stockton said high growth and tech are susceptible now to moves in the 10-year Treasury yield. She said the technology sector is the most overbought in relative terms, when comparing the sector to the S&P 500. The S&P 500 tech sector was up nearly 1% for the week, and it was up nearly 6% for the quarter.

“We would consider reducing exposure to growthy ETFs like ARKK and would be respectful of any breakdowns,” Stockton said.

Investors have been fixated on the S&P 500′s 50-day moving average, which sat at 4,439 on Friday. For the first time this year, the index broke below and closed under the average for multiple sessions this past week. By Thursday, it regained the 50-day and finished above it. The broad-market index closed above the 50-day moving average on Friday, at 4,455.

The 50-day is literally the average of the last 50 closing prices, and it is viewed as an important momentum indicator, just as the 200-day moving average is. A break above could signal a positive move, and a break below it could mean more downside.

Stockton said the relief rally in the S&P 500 could resume in the coming week. “But we think it will fade by the end of the week given the downturns in our intermediate-term indicators. We expect the SPX to make a lower high,” she wrote in a note.

She expects the 10-year Treasury yield could continue higher. “Momentum appears to be shifting to the upside and next resistance is near 1.53%. The breakout should benefit the financial sector, which saw significant outperformance [Thursday],” Stockton noted.

Week ahead calendar

Monday

Earnings: Aurora Cannabis

8:00 a.m. Chicago Fed President Charles Evans

8:30 a.m. Durable goods

12:50 p.m. Fed Governor Lael Brainard

Tuesday

Earnings: IHS Markit, Micron, Cal-Maine Foods, Thor Industries, United Natural Foods, FactSet

8:30 a.m. Advance economic indicators

9:00 a.m. Chicago Fed’s Evans

9:00 a.m. S&P Case-Shiller home prices

9:00 a.m. FHFA home prices

10:00 a.m. Fed Chairman Jerome Powell and Treasury Secretary Janet Yellen before Senate Banking, Housing and Urban Affairs Committee on pandemic response

10:00 a.m. Consumer confidence

1:40 p.m. Fed Governor Michelle Bowman

3:00 p.m. Atlanta Fed President Raphael Bostic

7:00 p.m. St. Louis Fed President James Bullard

Wednesday

Earnings: Jabil, Cintas, Herman Miller

10:00 a.m. Pending home sales

11:45 a.m. Fed Chairman Powell on European Central Bank panel

2:00 p.m. Atlanta Fed’s Bostic

Thursday

Earnings: Jefferies Financial, CarMax, Bed Bath & Beyond, Paychex

8:30 a.m. Initial jobless claims

8:30 a.m. Real GDP Q2

9:45 a.m. Chicago PMI

10:00 a.m. Fed Chairman Powell and Treasury Secretary Yellen before House Financial Services Committee

11:00 p.m. Atlanta Fed’s Bostic

11:30 p.m. Philadelphia Fed President Patrick Harker

12:05 p.m. St. Louis Fed’s Bullard

12:30 p.m. Chicago Fed’s Evans

Friday

Monthly vehicle sales

8:30 a.m. Personal income and spending

10:00 a.m. Manufacturing PMI

10:00 a.m. ISM manufacturing

10:00 a.m. Consumer sentiment

10:00 a.m. Construction spending

11:00 a.m. Philadelphia Fed’s Harker