HI Market View Commentary 03-23-2020

“But investing isn’t about beating others at their game. It’s about controlling yourself at your own game.”

– Benjamin Graham, The Intelligent Investor

“The investor’s primary interest lies in acquiring and holding suitable securities at suitable prices. Market movements are important to him in a practical sense, because they alternately create low price levels at which he would be wise to buy and high price levels at which he certainly should refrain from buying and probably would be wise to sell.”

– Benjamin Graham, The Intelligent Investor

The Bad, The Bad’er and the Real Ugly

I received an email

https://www.forbes.com/sites/jrose/2015/11/14/fixed-index-annuity/#2929f9995041

Don’t Buy A Fixed Index Annuity Until You Read This

Jeff RoseContributor

Several years ago while tuning into Dateline on NBC, I watched as they conducted one of their typical undercover operations.

This one was a bit different though – and closer to home – as they were running sting operations on financial advisors.

To be clear, it was specifically about independent life insurance agents who were pitching equity-indexed annuities to seniors.

At the time I had only been in the business for around four years, and while I was familiar with fixed annuities and variable annuities, I didn’t quite understand what fixed-indexed annuities were all about.

The gist of the Dateline special was showing how crooked financial advisors (aka advisors I would like to punch in the face) were using every sales tactic possible to try to generate a sale – otherwise known as a big fat commission.

While I have no problem with anybody trying to earn a living, I do have a problem with someone trying to line their pockets while putting someone else’s best interest out of sight. And that’s what these advisors were doing: selling fixed-indexed annuities while not conveying the whole truth.

At that point in time I got a really bad taste from fixed-indexed annuities. I have to confess, I still didn’t know much about them, though with Dateline promoting them as the worst investment product ever made, I decided it would be in my best interest to stay away.

Note: I want to stress here that these advisors weren’t selling an inferior product. In the right situation, fixed index annuities can make sense. In the Dateline sting situations, these advisors were not being truthful with how these products really worked.

In the market collapse of 2008, fixed-indexed annuities have become much more popular.

I’ve talked to several individuals who have purchased them merely for the fact that they are fed up with the stock market. They were looking for a guarantee and didn’t mind locking up their money for an extended period of time while also taking a lower interest rate in exchange for less risk and volatility.

Understanding that I should have been well-versed regarding how these products worked, I knew that I needed to start doing some research.

Sharing the Basics

I want to share some of the basics of how an fixed-indexed annuity works and to see if it might be a good investment for you.

What is a Fixed- or Equity-Indexed Annuity?

Good question.

Like all other annuities, an fixed-indexed annuity is a contract between you and an insurance company where they guarantee some sort of payment.

Essentially, a fixed-indexed annuity (also known as an equity-indexed annuity and sometimes referred to as “FIAs” or “EIAs”) is sort of a hybrid between a standard fixed annuity and a variable annuity – like a hybrid annuity (for more information on these annuities read 5 Reasons Why You Should Never Buy A Variable Annuity on Forbes and Hybrid Annuities Revealed – Should You Believe The Hype? which is also on Forbes).

I say “sort of” because while they do have similar characteristics, there are significant differences. According to FINRA’s website, they describe them as the following:

FIAs are complex financial instruments that have characteristics of both fixed and variable annuities. Their return varies more than a fixed annuity, but not as much as a variable annuity. So FIAs give you more risk (but more potential return) than a fixed annuity but less risk (and less potential return) than a variable annuity. FIAs offer a minimum guaranteed interest rate combined with an interest rate linked to a market index. Because of the guaranteed interest rate, FIAs have less market risk than variable annuities. FIAs also have the potential to earn returns better than traditional fixed annuities when the stock market is rising.

There’s no doubt that fixed-indexed annuities are confusing. When variable annuities started offering their income benefit riders (these are special add-ons that annuity products offer to give investors a guaranteed income stream), I became overwhelmed with all the mechanics behind them because every insurance company offered something slightly different. To compound the problem, they were constantly making small tweaks to their offerings making it difficult to sort out which one was which.

Now imagine if it’s difficult for the advisor to understand how these products work, how do you think the clients feel? Exactly.

To best understand how these annuities work, I thought it would be best to break it down into two parts. The first part we’ll look at is the “index option” and explain how that works. In the second part we’ll explore the “income rider” or “guaranteed benefit withdrawal” that most of these products offer. This income rider is one of the major selling points for most individuals so I definitely want to take a closer look at that.

How a Fixed-Indexed Annuity Works

A common selling point in regard to fixed-indexed annuities is the guarantee of principal (meaning that you will never lose a dime of your money that you pay to it).

While yes that is certainly the case, one thing that you need to be aware of is that all annuities come with some form of surrender charge meaning that if you were to cash out your annuities early, you would pay a significant surrender charge just to get your principal back. We’ll look at a sample surrender schedule so that you can see exactly how much you would pay in penalties.

Going back to the original point, yes your principal is guaranteed so as long as you keep the annuity for the entire length of the contract. As you can imagine, for many investors who scorn the stock market, this is a valuable characteristic to have.

How Does the Index Option Work?

For the sake of this post, I want to keep it very simple and just explore one of the indexed options that are currently available. Please keep in mind that all indexed annuities have various indexed options and various cap strategies – so understanding what you’re actually getting into is essential.

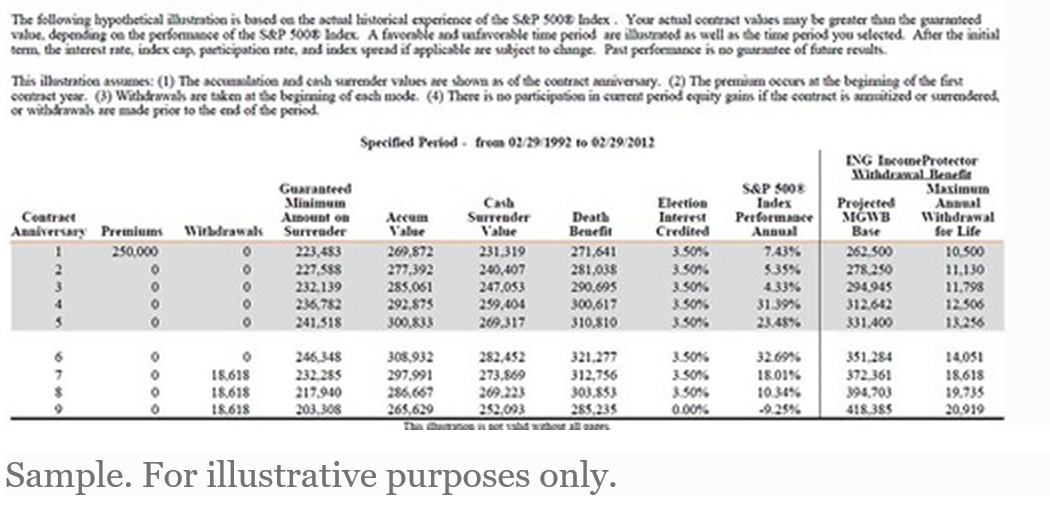

The scenario in the screenshot below shows investing $250,000 into an fixed-indexed annuity. This particular annuity has a 10-year contract period and is currently using a basic indexed option known as the S&P 500 point-to-point index strategy. The S&P 500 Index is probably the most common index that you will see used in any of the fixed-indexed annuity products.

I’m starting to see more of these using international indexes, other market indexes such as the value index, and I’ve even seen some now using a gold index.

Sample. For illustrative purposes only.

In this illustration, since we are taking on a 10-year contract, the investor is entitled to a bit of a higher cap on the interest rate.

For example, in this case the election of interest credit is 3.5% (usually referred to as the “cap rate”). With the rates being at all-time lows, these cap credits are significantly lower than they were in years past. With this same product, had the investor taken out a five-year product they would’ve been capped at 3% instead of 3.5%. Most insurance companies will give you a higher rate if you lock up your money longer.

So how does the interest rate cap work? Looking at the illustration in year one, if an individual was to put $250,000 in and the S&P 500 Index performed 7.43%, the investor would get a cap of 3.5% credited to their account. The difference goes back to the insurance company. If there is a “catch” in these types of policies, that would be the big one.

In year two, the illustration shows the the S&P 500 Index going up 5.35%. Once again you’re capped at 3.5% with the remaining difference going back to the insurance company.

At this point you’re probably wondering why in the heck you would want to be capped on your upside. Looking at year nine should put that into perspective for you.

In year nine – when the S&P 500 is down 9.25% – you don’t make the 3.5%, but most importantly you don’t lose anything showing a net return of zero. That’s one of the attractive features of the fixed-indexed annuities.

With fixed-indexed annuities, your principal is protected in years the market loses money no matter how steep the losses.

Note: Personally, I’m not a big fan of these types of illustrations. Why? Primarily because in the first couple of years they usually show constant growth and as we all know, the market does not work in that way. We have ups and downs. Personally, I would like to see an illustration that shows losses in the beginning to not give the potential investor high hopes in their expected returns.

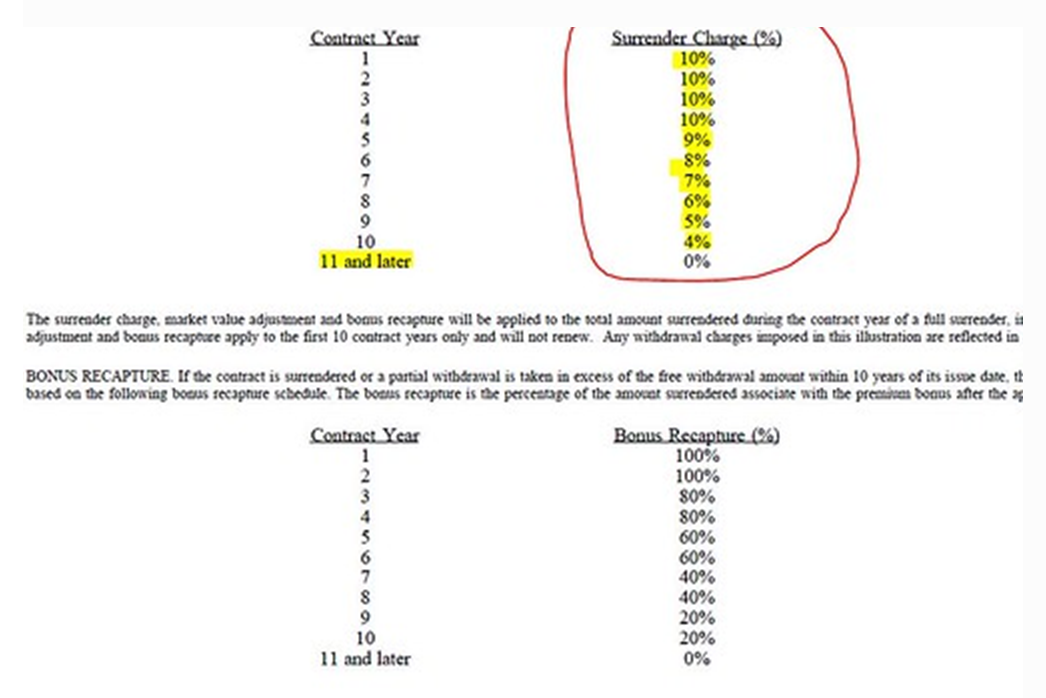

Beware of Surrender Charges!

In the Dateline special that I watched several years ago, one of the main points that they focused on was the lack of disclosure of surrender charges when it came to fixed-indexed annuities. A lot of the bad advisors were very misleading or deceptive when sharing if there was, in fact, a surrender charge.

In one case, one independent insurance agent flat out lied to the potential client telling them that they could withdraw their money at any time. That was far from the truth.

The first thing that you have to realize is that fixed-indexed annuities come in different contract lengths. They can be anywhere from seven years on up to fifteen years. I’ve seen them all.

In the illustration above, this was a ten-year contract. Below is a snapshot of the surrender schedule that would be included in the documentation for the illustration above. As you can see, in the first year if you were to liquidate the annuity, there would be a 10% penalty on your interest and principal. This is very important to note.

Sample Surrender Schedule

Oftentimes, bad advisors will sell these to seniors comparing them to CDs while explaining they have security and stability. The one big fundamental difference is that with the CD, if you cash it out early, you just give up your interest. With a fixed-indexed annuity, if you surrender it early, not only do you give up your interest, but you also give up a portion of your principal – and that is a huge difference.

Now keep in mind, most of these annuities do allow for a free withdrawal, meaning that you can withdraw anywhere between 10% to 15% of your principal each year without a surrender charge, but anything over and above that will be subject to the surrender schedule.

Where Equity-Indexed Annuities Really Flourish: Income Riders

Thus far we looked at the cap rates and principal protection that FIAs offer. For some people – especially retirees – that’s enticing, but it might not be enough for them to invest into one. Where many retirees find comfort in FIAs is in their income riders.

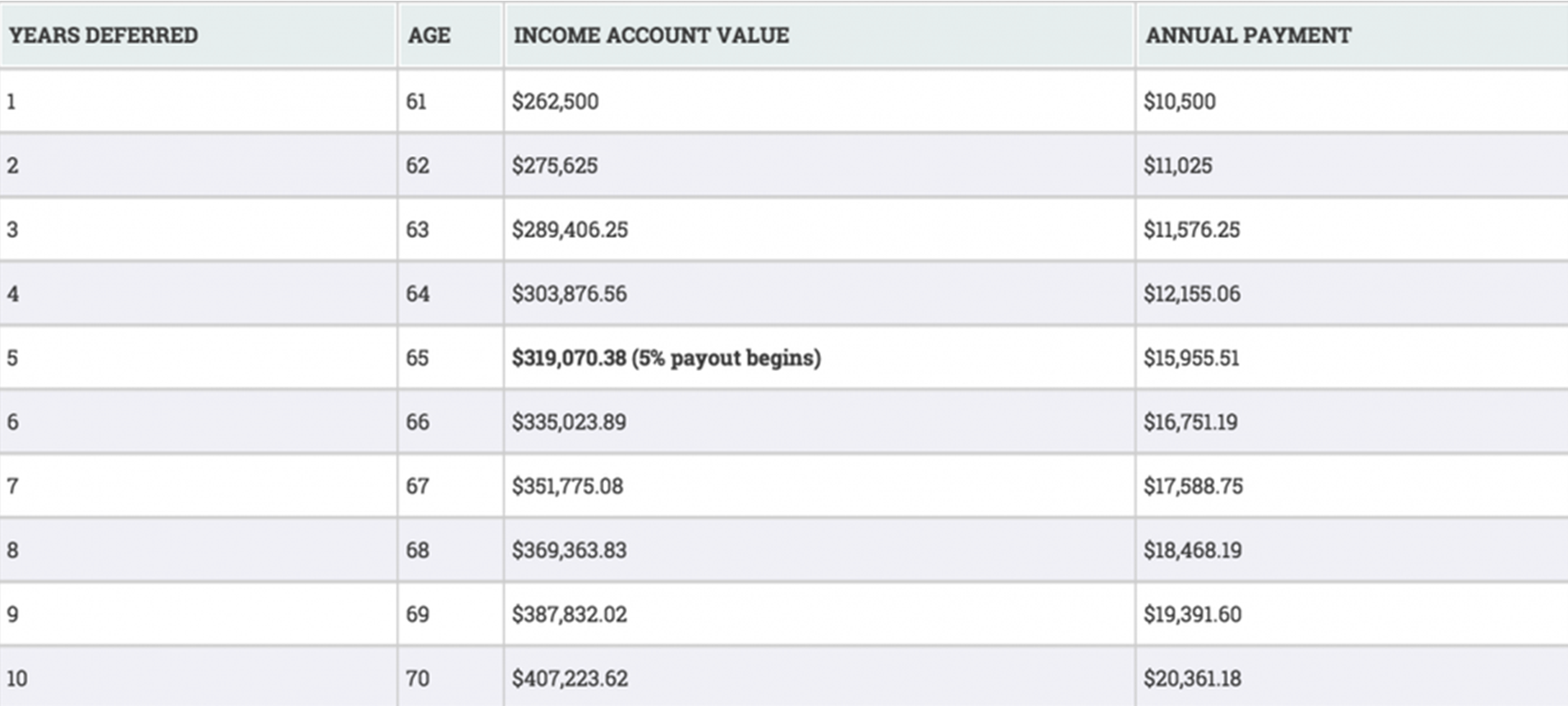

Sticking with our $250,000 example above, I’ll demonstrate how the income rider works.

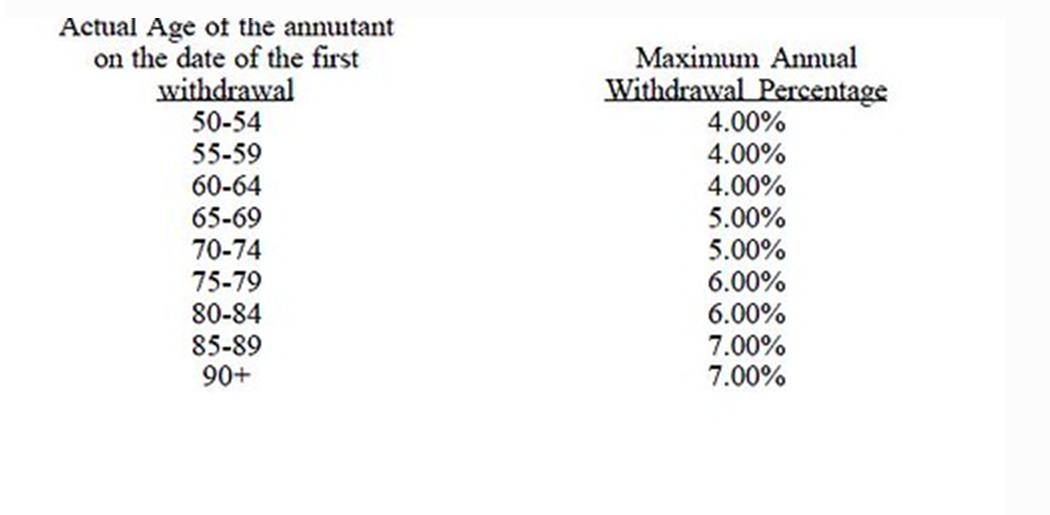

Say that a 60-year-old invests $250,000 into an FIA and wants to start taking a guaranteed monthly benefit, then using the table below, they would have a $10,000 ($250,000 x 4%) guaranteed annual income for life. Even if they end up pulling out more than their principal, they would still continue to receive payments.

A 65-year-old individual with the same amount would get a bit more collecting $12,500 guaranteed per year.

Guarantees for Retirement

If you’re a 60-year-old individual that has $250,000 to invest but doesn’t plan on retiring until 65 or later, then the income benefit riders become that much more attractive. Insurance companies will give an additional credit to the income account that, in turn, gives you a potential higher payout when you need it. Let me explain . . . .

A 60-year-old may get a 5% income credit increase each year up until the day they decide to start taking their money. That means that the insurance company will add 5% a year to original deposit (in this case $250k) each year. Once they start taking their income, the payout will be the amount in their income account multiplied by the withdrawal percentage based on their age.

The table below illustrates this over a 10-year period.

The 5% income credit is for hypothetical purposes. Each insurance company will have their own set interest rate. Recently, I’ve seen anywhere from 5% all the way up to 7%.

Another thing to consider is that the maximum withdrawal percentage is typically lower if you’re looking for a lifetime guarantee for you and your spouse. Typically, it will be about .50% lower.

Beware: The income credit and the maximum withdrawal percentage are used to determine your guaranteed payout. It is not the same thing as “making 5% on a CD.” I’ve encountered many advisors who sell these as investments with a “5% guaranteed return.”

Yes, there is a guarantee but most people associate that return with what a CD or a bond would pay. These are two totally different animals. If an advisor presents this to you as a “CD-like investment,” I would be cautious – very cautious.

Who Should Buy a Fixed- or Equity-Indexed Annuity?

So with all that thorough analysis, you’re probably wondering for whom does it make sense to purchase an equity-indexed annuity. Typically, I think if you meet some of the following criteria, then you might be a good candidate.

- You absolutely hate the stock market.If you’re tired of seeing your investments rise and fall with the Dow Jones, then an equity-indexed annuity might be a good fit.

- If you have five to ten years before you actually need to draw income. Personally I think the income riders are a viable option for those who want to avoid the market and want to have a guaranteed income stream at retirement. With the income account increasing each year for each year that you’re not touching it, this can be a huge benefit for someone who has a big chunk of money that can invest it and sit on it for a few years.

- You want to diversify. You might be a strong believer in the markets, but a little certainty never hurt anyone. Taking some money and locking it up in annuity with a guaranteed income rider could make sense.

Caveats to Consider

It’s also important to note that there are several caveats to consider when you’re thinking about fixed-indexed annuities. These caveats are somewhat serious, so make sure you’re okay with them before you sign on the dotted line.

Please keep in mind while you’re reading these caveats everything I just shared with you . . . there are certainly benefits to FIAs! Some people like FIAs because they offer a lower amount of risk when compared to traditional investing, for example. Make sure to weigh the pros and cons.

Let’s take a look at these caveats.

1. Most equity-indexed annuities don’t offer inflation protection.

Inflation can have devastating effects on the value of money over time. As you probably recall, inflation is an increase in prices which in turn lowers the purchasing value of money. Now, the annual inflation rate is a percentage that reflects how much prices have risen over the year.

Unfortunately, annual inflation rates have significantly changed over time as to make them not so predictable. An annual 4% inflation rate rule of thumb has been suggested, but fluctuations in the actual annual inflation rate results in mathematical properties over time that may make the 4% rule of thumb irrelevant.

So what does all this have to do with equity-indexed annuities? Well, equity-indexed annuities don’t offer inflation protection. If you’re living in a 2% inflation environment and then experience a season of hyperinflation, your equity-indexed annuities might not look as great as they once did in a lower inflation environment.

In high inflation environments, a traditional stock and bond portfolio may look more appealing to you due to their ability to potentially produce higher returns. The higher returns in this environment are desirable as they have a higher likelihood to offset the negative effects of inflation. Makes sense, right?

2. Most income riders cease when you start receiving distributions.

Let’s say that you have a 7% income rider. It’s important to note that you will only receive that increase during the accumulation phase and not when distributions begin.

As an example, you might receive the increase for 10 years, but once the annuity becomes like an immediate annuity, you will have to settle for the same payment every year for the remainder of your life.

Now, that’s really not too bad of a caveat, but it’s an important one to note. If you’re basing your projections on receiving the increase every year even after distributions begin, that could make your math skew higher than it should which could put your retirement plan at risk. Make sure not to make this mistake.

3. Annuities are only backed by insurance companies.

Forget FDIC insurance – you won’t see that with an annuity. That means if the insurance company that holds your fixed-indexed annuity goes under, so does your money. This is why it’s essential to check the ratings – and understand how the ratings work – of the insurance company before you buy one of their financial products. It’s probably a remote chance that they’ll go under, but still, there’s a chance.

4. Surrender charges may discourage you from switching to a better product down the road.

Not everything that sounds like a good deal today will sound like a good deal in three, five, or seven years. Financial products change over time and new ones arrive on the market.

Should you find yourself discovering a new financial product that blows your fixed-indexed annuity out of the water, and should you still be subject to surrender charges, you may find yourself with a difficult decision: losing some of your interest and principal to surrender charges and going with the latest and greatest financial product, or riding it out with the hope that the latest and greatest financial product will still be around once you aren’t subject to surrender charges.

Hindsight is 20/20, but foresight is foggy at best. That’s why I recommend you consider this caveat but don’t let it be the sole reason you choose to forgo FIAs.

Bottom line: Get a Solid Retirement Plan in Place

Sometimes, it’s too easy to focus on the building blocks of a retirement plan (like Roth IRAs, FIAs, mutual funds, bonds, and more) and forget about the big picture. After all, the reason you’re learning about these building blocks should be so that you can build a comfortable retirement for your family.

By understanding the many options available to you – including FIAs – and keeping your retirement goals in mind, you can carefully put together a retirement plan that will last longer than you will survive. If you’re having trouble putting one together or you’d just like some peace of mind, consider finding a competent financial advisor who not only can help you with insurance products, but with investment products as well.

Equity-indexed annuities are nice because they offer access to an index, they have income riders, and they have longevity of benefits, but remember: that doesn’t necessarily mean they’re right for you. There are plenty of reasons why you shouldn’t buy an annuity – but there are also reasons why you should. Simply put, whether you should or shouldn’t depends on your particular situation.

If you would like detailed analysis of an annuity that you own or one you are considering purchasing, head over to AnnuityTested.com. There, you will be able to enter in information regarding the annuity in question and receive prompt feedback so that you can form an educated opinion. This should help you determine if the annuity is right for you; or, for example, if more traditional stock and bond investing represents a better option.

It’s important to note that traditional stock and bond investing is likely to result in higher returns than those offered by FIAs over time – but remember that comes with a higher risk. Consider alternatives like this when you’re thinking about FIAs and consider the differences in fee structures as well.

As always, make sure that you ask plenty of questions of the financial advisor and have a solid understanding before you invest any money. Annuities are long-term investments so don’t use them if you’re looking for a short-term investment solution – I recommend emergency funds before I recommend any investment. Again, seek the advice of a competent financial professional and educate yourself before you pull the trigger.

I am a certified financial planner, author, blogger, and Iraqi combat veteran. I’m best known for my blogs GoodFinancialCents.com

Bad’er Why aren’t people paying attention to their accounts vs just listening to an voice message, email, podcast

Ugly – The position people are in when in one month their whole retirement plan is shot to hell

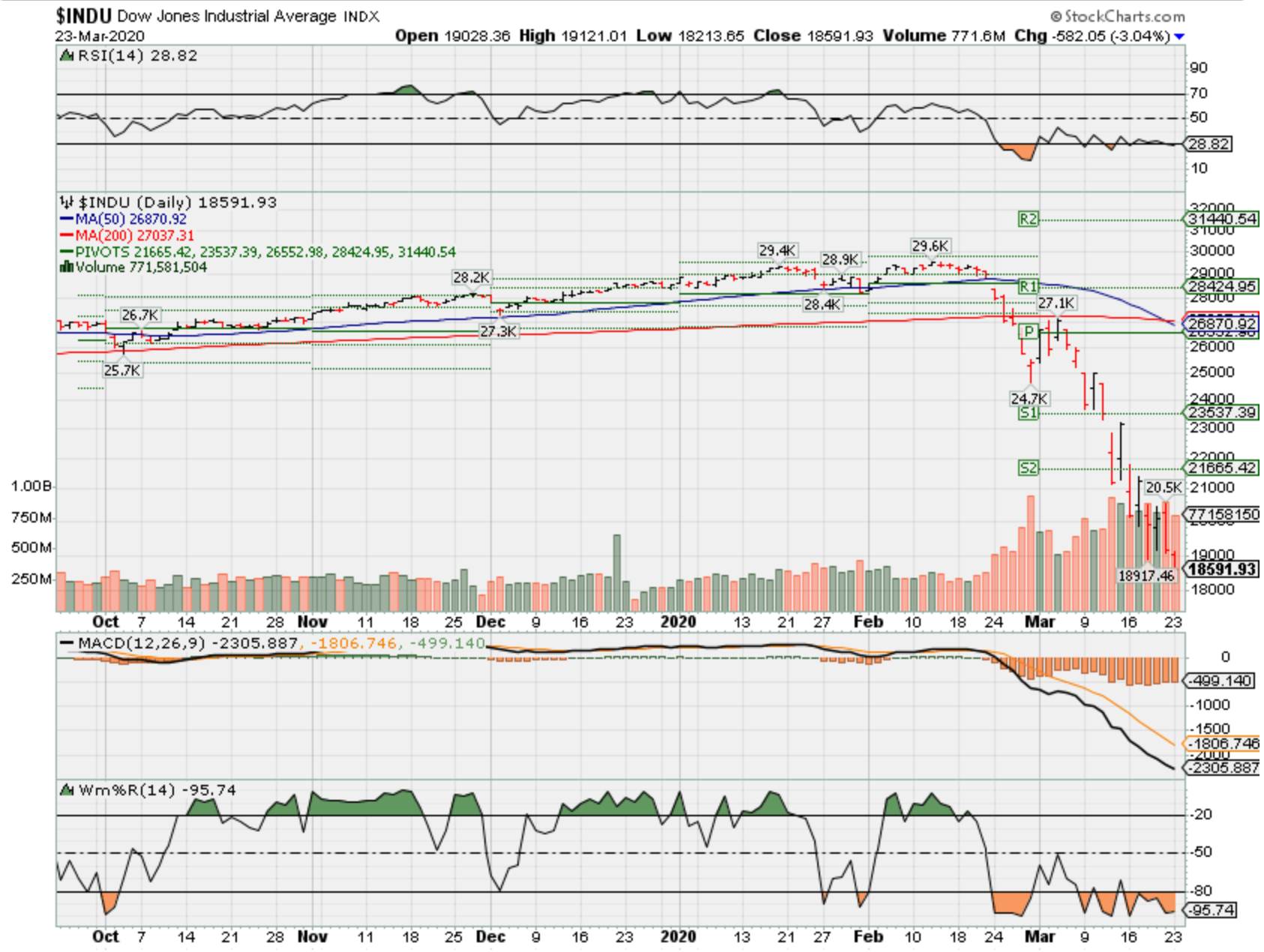

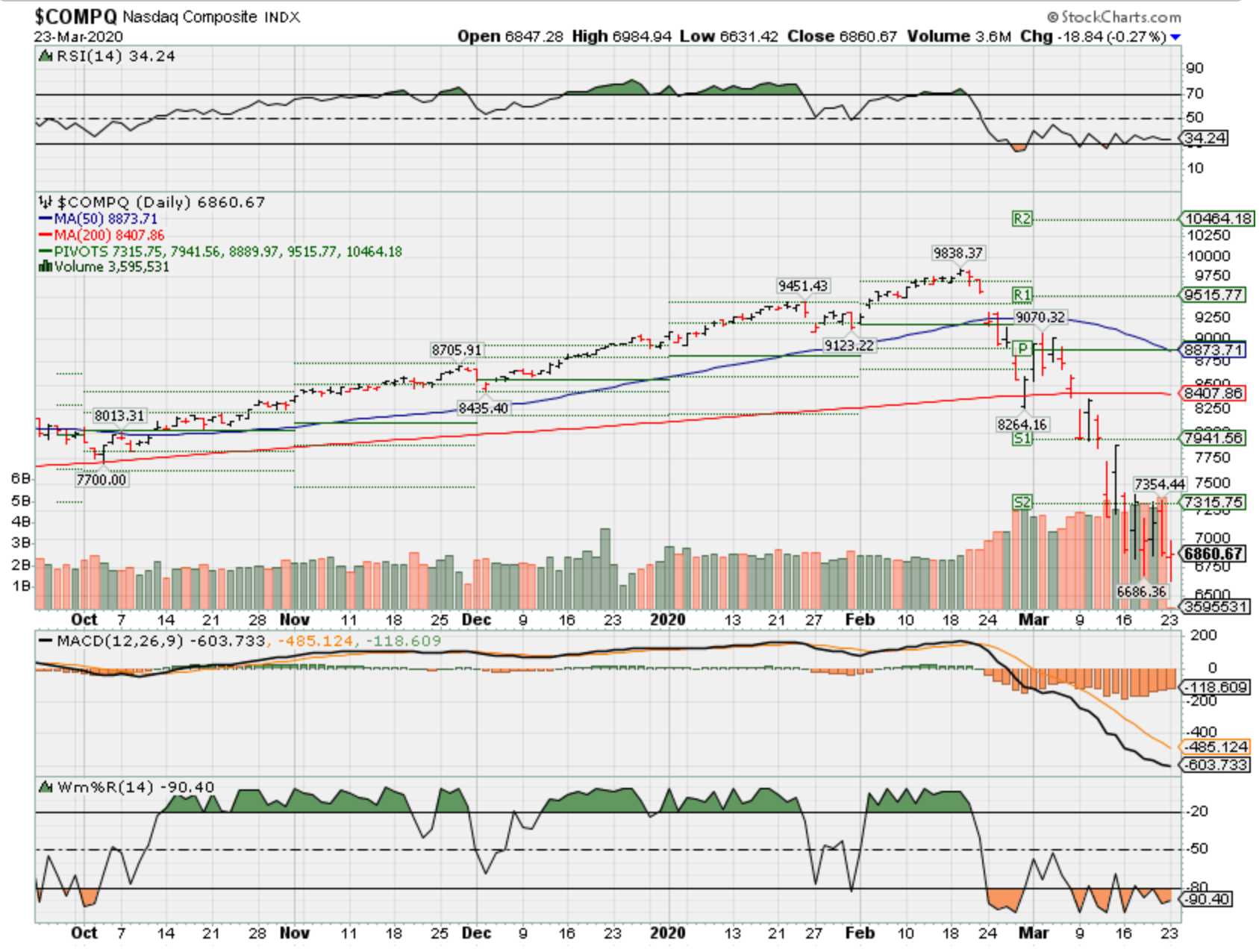

Where will our markets end this week?

Lower

DJIA – Bearish

SPX – Bearish

COMP – Bearish

Where Will the SPX end March 2020?

03-23-2020 -15.0%

03-16-2020 -15.0%

03-07-2020 0.0%

03-02-2020 +5.2 %

Earnings:

Mon:

Tues: CCL, NKE

Wed: FUL

Thur: KBH, LULU, SPWH

Fri:

Econ Reports:

Mon:

Tues: New Home Sales,

Wed: MBA, Durable Goods, Durable ex-trans, FHFA Price Index

Thur: Initial, Continuing, GDP, GDP Deflator,

Fri: PCE Prices, PCE Core, Personal Income, Personal Spending, Michigan Sentiment

Int’l:

Mon –

Tues – EUR: Markit PMI Composite

Wed –

Thursday – GBP: BoE Interest Rate Decision

Friday-

Sunday –

How am I looking to trade?

Protection still on and coming due 3/27/ 04/03, 04/09

When and how to pick up shares and most likely add more protection/Earnings

www.myhurleyinvestment.com = Blogsite

customerservice@hurleyinvestments.com = Email

Questions???

https://news.yahoo.com/us-government-nationalize-boeing-013447260.html

Will the US government nationalize Boeing?

Luc OLINGA

New York (AFP) – About 12 years after the US government bailed out General Motors and Chrysler, Washington policymakers are debating how to throw Boeing a lifeline as it reels from dual crises over the coronavirus and 737 MAX.

The aerospace giant, which manufactures the US presidential jet Air Force One in addition to defense and commercial aircraft, has asked for $60 billion in federal support for the US aerospace industry, but it is not yet clear how such a bailout would function.

“Boeing is on the brink,” prominent hedge fund investor Bill Ackman said this week. “Boeing will not survive without a government bailout.”

Boeing’s financial picture was already under pressure even before the coronavirus.

The 737 MAX, which had been the company’s top-selling plane, has been out of service for more than a year following two deadly crashes. The lengthy grounding has cost the company upwards of $18 billion, a figure that is expected to rise.

The coronavirus has now worsened that picture considerably, obliterating demand for flying and putting Boeing’s airline customers in financial distress.

The situation has pummeled shares of Boeing, leaving its market capitalization Friday at around $54 billion.

Also Friday Boeing announced that it was suspending its dividend until further notice and that Chief Executive Dave Calhoun and Chairman Larry Kellner would forgo pay until the end of the year.

The company, which had previously announced it was suspending share buybacks, said the program would remain paused indefinitely.

Boeing’s dual crises would threaten the survival of other companies, but it still retains considerable support in Washington because of its importance to the US economy, with about 130,000 employees. And that figure does not include a much larger group workers employed by Boeing’s 17,000 suppliers.

President Donald Trump on Tuesday endorsed aggressive measures to assist the companies, telling reporters at a briefing, “we have to protect Boeing and help Boeing.”

– Auto bailout a model? –

In a securities filing Thursday, Boeing said there are a “variety of approaches” currently being discussed to support the US aerospace industry, but the company declined to comment further on the options.

Aid for aerospace is not included in the $1 trillion stimulus package now being crafted on Capitol Hill, although it does including help for airlines.

One option that has been discussed is for the government to take an equity stake in Boeing.

“Taxpayers should receive equity in a company in return for assistance so that the public benefits from its investment when the company is fiscally stable,” said Oregon Democratic Representative Earl Blumenauer.

If Boeing follows the model set by General Motors and Chrysler after the 2008 financial crisis, it would file for bankruptcy protection under Chapter 11 and restructure its finances.

The auto bailout was launched by former president George W. Bush in 2008 under the Troubled Assets Relief Program, and carried through by Barack Obama’s administration.

The federal government injected $81 billion into two of Detroit’s “Big Three” automakers and took equity stakes in the companies, and then sold those shares in December 2013.

GM filed for bankruptcy in June 2009 and received $50 billion in support that allowed the government to take a 61 percent stake in “new GM.” The company was effectively nationalized, although officials avoided that term.

The restructuring cost shareholders $11.2 billion, but saved some 1.5 million jobs, according to the Center for Automotive Research.

Scott Hamilton of Leeham News, which specializes in aviation, said a US takeover of Boeing could pose competitive concerns in the defense industry.

“Boeing is the nation’s number two defense contractor. How would this affect defense contract bids? I imagine Lockheed Martin and Northrop Grumman might have some concerns,” Hamilton said.

“I don’t think there’s much of a rationale for a US stake in Boeing,” said Richard Aboulafia of the Teal Group, a research consultancy focused on aviation and defense.

The government also could make aid conditional on splitting the company into two entities, one focused on commercial planes and the other on defense, experts said.

Another possibility could be a merger of Boeing into one of the other defense giants, experts said.

Lockheed Martin did not respond to queries, while Northrop declined comment.

NYSE to temporarily close floor, move to electronic trading after positive coronavirus tests

PUBLISHED WED, MAR 18 20204:46 PM EDTUPDATED WED, MAR 18 20208:05 PM EDT

KEY POINTS

- The New York Stock Exchange said starting March 23, it will temporarily close its historic trading floor and move fully to electronic trading.

- The move came after two people tested positive for coronavirus infection at screenings it had set up this week.

- The entrants were stopped at the medical screenings at the Big Board.

- This is the first time the physical trading floor of the Big Board has ever shut independently while electronic trading continues.

The New York Stock Exchange said Wednesday it will temporarily close its historic trading floor and move fully to electronic trading after two people tested positive for coronavirus infection at screenings it had set up this week.

All-electronic trading will begin on March 23 at the open, the exchange said. The facilities to be closed are the NYSE equities trading floor and NYSE American Options trading floor in New York, and NYSE Arca Options trading floor in San Francisco.

The closure was in part as a result of positive coronavirus tests of two people, Stacey Cunningham, President of the NYSE, told CNBC. The entrants were stopped at the medical screenings at the Big Board.

The stock market has closed at times over the years, such as during World War II and in the wake of 9/11, but this is the first time the physical trading floor of the Big Board has ever shut independently while electronic trading continues.

“We implemented a number a number of safety precautions over the past couple of weeks, and starting on Monday this week we started pre-emptive testing of employees and screening of anyone who came into the building,” Cunningham said on “Closing Bell.” “If that screening warranted additional testing, we tested people and they were sent home and not given access to the building. A couple of those test cases have come back positive.”

“While those people were not in the building this week and the building had been cleaned and addressed prior to start of trading on Monday, I think it’s reflective we’re seeing things evolve,” Cunningham added.

The NYSE is operated by the electronic trading group Intercontinental Exchange, which acquired it in 2012. The exchange moved into its location at 18 Broad St. in lower Manhattan in 1903. As electronic trading grew on Wall Street, the NYSE adapted, with more and more of its trading being done away from the physical floor.

However, the company has maintained over the years that the floor was still important, especially at the open and closing of trading, and said that it would not be shut even as the number of actual traders in the location dwindled. The other major U.S. stock exchange, Nasdaq, does not have a physical trading floor.

Wall Street has been on an unprecedented volatile ride during the coronavirus crisis. Just this week, a market-wide circuit breaker was triggered twice by the NYSE due to the massive sell-off, resulting in brief trading halts.

On Wednesday, the Dow Jones Industrial Average closed below 20,000 for the first time since February 2017. The S&P 500 was now nearly 30% below a record set last month.

The exchange said in a release that it was implementing its business continuity plan and “trading and regulatory oversight of all NYSE-listed securities will continue without interruption.”

CME Group closed its Chicago trading floor last week in a precautionary move due to the coronavirus outbreak.

As of Wednesday, global cases of the coronavirus have reached more than 212,000 and confirmed cases in the U.S. surged to 7,324 in total, according to data from Johns Hopkins University. The coronavirus has spread to all 50 states and D.C., with the death toll in the U.S. climbing to 115.

— CNBC’s Jesse Pound contributed to this report.

https://the-moneychanger.com/articles/signs_the_credit_bubble_is_bursting

Signs the Credit Bubble Is Bursting

An interview with Daniel Oliver (October 2018)

Daniel Oliver Jr. is President of the Committee for Monetary Research & Education, a non-profit educational organization founded in 1970 to promote greater public understanding of the nature of monetary institutions and of the central role that a healthy monetary system plays in the well-being, indeed, in the very survival of a free society.

In 2009, he founded Myrmikan Capital, an investment firm specializing in micro-capitalized gold mining companies. Previously, he worked for Bearing Capital, LLC, a private equity firm in Buenos Aires focused on Latin American commodities investments.

Mr. Oliver graduated from Columbia Law School with honors in 2001, where he was President of the Federalist Society. After practicing corporate law at Simpson Thatcher & Bartlett and co-founding two venture companies, he attended INSEAD and obtained an MBA in 2005.

His first job was at the International Herald Tribune in Paris, which filled him with a love of writing. He currently publishes commentary on monetary principles in various media outlets, on financial television and radio programs, and speaks at monetary and investment conferences. He is finishing a book on the nature and history of credit bubbles, which stretch back to ancient Greece and beyond.

Visit Myrmikan to sign up for his free monthly commentary, elegantly written and filled with historical understanding and original insights.

Dan is a National Review Institute Fellow and is an alumnus of the Swiss American Foundation’s Young Leadership Conference. He lives in New York City with his wife and two daughters, and kindly made time for this interview on 24 October 2018. He is just finishing a book, Golden Tears: A History of Credit Bubbles which should be published next spring. It is an elegantly written picture of 5,000 years of credit bubble. I have read a draft and can recommend it without reserve or hesitation.

It would help your understanding of this interview to read again the July 2016 Moneychanger article, “Nor a Lender Be,” and our January 2017 interview with Mr. Oliver.

Moneychanger: I’ve got a big question burning a hole in my head. How will we know the bubble is popping?

Oliver: Great question. History shows that bubbles form when the banking system creates credit instead of allocating savings. When it creates credit, a banking system drives interest rates too low, which encourages malinvestment. Since interest rates define the value of future cash flow, when rates are driven too low we get a false picture. Low rates make future cash flows look more valuable than they really are.

How does this play out, practically? Everyone runs out and starts building big capital assets like buildings and ships and airplanes. When they do that based not on consumer demand but simply because the bank system has sent these artificial interest rates signals on money, it creates overcapacity and that drives down rent (income from assets). That drives down price. Once that happens the profit margins of those projects shrink, and they can’t then pay the capital cost.

What are signs of a popping bubble? What’s happening to the pricing power of (especially) capital projects very far from consumers like buildings, power generators, locomotives, or airplanes? Also look at the health of the banking system. When I look out my window, it looks like Shanghai. There are cranes everywhere. Why? Because since 2008 rates have been almost zero and any project becomes profitable at a zero percent interest rate.

It takes a long time to build a building. All around, though, they are going up everywhere. At the same time, I’m reading articles every week saying that real estate is falling. Well, you don’t just stop building your building because of a blip in rent.

All this overcapacity comes on line at the very moment that rents are already falling. Of course, the overcapacity then makes them fall further. Then the question is, how on earth do these projects pay their debt back or get a return for capital investment to their investors?

One thing I’ve been watching is the share prices of the very globally connected banks. [See charts 1, 2, and 3.] Those, of course, did very badly in 2008 as you would expect when a bubble pops. They are doing very badly now which tells you that returns on their investments are very poor.

To answer your question, from my perspective, the bubble is popping right now.

Interest rates are going up. That makes these investments not work. It makes overcapacity lower the rent then the banks get stressed and the whole thing comes tumbling down.

I can’t predict exactly when the Lehman moment will happen. That might still be a ways off. But I think we’ve passed the top of this credit bubble already and now we’re on the way down. My question is – How far do we go down?

Moneychanger: You picked two things that interest me. I’ve been watching the price of real estate. Local bubbles seem to be popping around the country. Also, the bank stock index (BKX) has tanked since September.

Oliver: That’s right. You’re starting to see write offs now, not wholesale but little banks here and there saying, “This mall that should have a return of 100 cents on the dollar is actually giving 20 cents on the dollar.” Things like that.

It’s not the money center banks yet. It usually starts in the fringes, whether subprime housing last cycle or emerging markets this cycle. Problems often begin in emerging markets. You’d expect to see the most thinly capitalized people, the biggest speculators, get stressed first and that’s exactly what you see now.

Overbuilding always concentrates, like in Las Vegas or New York City. When you look at the pockets of frenetic activity, they’re looking very stressed. The bank stocks aren’t doing well because the market is figuring out that in a high interest rate environment the investments banks make don’t make sense.

Bernanke arranged all this. He’s the man who took rates to zero, and he recently quoted Paul Samuelson who said, “At a zero percent interest rate it makes sense to flatten the Rocky Mountains to save on gas driving back and forth across Colorado.” This is an absurd example but he’s right. When you have a zero percent interest rate, you have infinity amount of time to make back your capital. I mean if the cost was actually free and you have forever to make your cash flow, it does make sense to flatten the Rocky Mountains.

It’s extraordinary. When ultra low rates exist for several years, you see huge amounts of craziness not unlike that anecdote. There exist now plenty of real-life examples that cannot survive a high interest rate environment. The end cannot be far off.

Moneychanger: One thing that makes the bank stocks’ plunge potentially more lethal is that they’re falling in the teeth of rising interest rates. Theoretically shouldn’t higher interest rates mean wider margins for banks and greater profits? [See chart 4.]

Oliver: Not really. Victor Sperandeo wrote an article about this a couple months ago where he pointed out that if you’re a bank and you buy a treasury bond and you put it in your hold-to-maturity account, you no longer are required to mark its value to market. This has tremendous implications.

A couple years short term interest rates were zero. Banks were paying zero percent for deposits, and 30-year Treasury bonds were paying 3 or 3-½%. A bank could take deposit money, which cost it zero, buy a 30-year bond, and make a 2-1/2% spread for free!. And, when interest rates go up, driving the bond’s market value down, you don’t need to mark that bond’s value down on your books! Your assets still show the value of that 30-year bond the same as the day you bought it.

Of course, if a bank buys a bond at three and a half percent and 30 year interest rates rise to five percent, they’ve suffered a tremendous loss but they don’t have to report that, either. So today a bank can say, “Our assets are fine,” even though, behind the scenes their cash flow is shrinking. All of a sudden they have to pay one, one and a half, two percent on their deposits. Now their cash margin on that trade is cut in half. And if short term rates then go to three and a half percent, they are now making nothing on that trade and must realize their cash flow is about to go negative. Rising rates are lethal to banks because of the games banks play.

No. An interest rates increase is not good for banks. It is very, very bad, and that’s what the market is telling us. I think it was Paul Singer, a hedge fund guy from Argentina, who said he has 200 investment advisors and analysts that work for him. They tried to decipher the balance sheets for the banks and they couldn’t do it. So if he can’t do it, no one else can do it. In fact, the banks can’t even do it. That’s why they hire these big consulting firms to try and figure out what is going on inside their own bank. Banks don’t even know what’s happening.

Banks are very compartmentalized. The top people have all of these different departments below them that compete with each other to make money. The guys in the tippy top really don’t know a whole lot of what’s happening. Below them is where all these scandals happen. The guys at the top say, “Oh, we had no idea.” They didn’t have an idea because they don’t know, they don’t care -there is a culture of just make money and just don’t get caught.

Moneychanger: I realize that it’s impossible to foretell what the bubble-bursting catalyst will be. You can’t see everything in the market so you don’t know who is in the worst condition. But do you have any idea what that catalyst will look like?

Oliver: I’m writing a book on the history of credit bubbles that goes back 5,000 years. What usually happens is that as rates start rising the weaker players start rolling over, and finally one of them is big enough to bring down the big players.

Go back to 2007. In May a European fund blew up. It was a small fund of just a few million dollars. No one cared. Then a month later two other hedge funds went down. They were maybe a few billion dollars – still not big enough to bring the system down. Still they were symptoms of a big problem. Then a European bank went down and the central bank couldn’t bail it out.

While these little things around the edges were faltering, stocks kept going up. They made new highs that autumn, then started leaking lower. Next you got a bigger collapse of an entire firm. Lehman Brothers (someone big enough to bring down the entire system) didn’t go down until a year later. That’s why I’ve been looking around for those little failures that are not big enough to bring the system down but are symptomatic of stress under the surface.

And there are some. Look at Argentina, at Turkey, at the bank situation in China. I was very intrigued by the failure of the hedge fund GAM, Global Asset Management last summer. They were a big firm of about $150 billion. Apparently the manager of this fund was not following proper due diligence procedure and they simply stopped redemptions; they gated the fund. Nobody could get their money out. It turned out the manager wasn’t just not following policy. He was investing in emerging market debt that got crushed and blew up the fund. So they gated it because they got 10% redemptions and couldn’t liquidate the holdings. There was a run on the fund. I see no news on what’s happened since then. But, again, it started off as internal problem.

There have been little failures like GAM here and there, not really enough for me to think that we’re on the cusp of a major failure but a big bust can happen without them. That’s what happened in 1929.

In 1929 there really weren’t that many failures leading up to the collapse. The market just was so overbalanced, so high, that it simply crashed. It hit a peak in early September 1929, and, within six weeks, it was 40% lower. Two years later a lot more failures piled up. So, there is no rule that you have to have little failures first. It’s certainly possible you could see the stock market crash first, then see other systems blow up in the last big, huge credit cycle. I look for little failures that are symptomatic of stress under the surface that you really can’t see as a retail person looking at wholesale money markets because they can be good signs of what’s to come. [See chart 5.]

One reason stocks are so high now is because companies have been borrowing money to buy back their shares. Company executives like this because they get paid stock options and these purchases help the stock options, but it’s not real. The company is just adding to its debt load. Now, rates are rising. That means they have to refinance that debt and, all of a sudden, it’s more expensive. This has made these companies’ financial structures much more brittle.

Also, if you see any setbacks in your business, equity can get really crushed. IBM is a great example. They’ve been buying shares with borrowed money. They sell their software to companies on credit, so they don’t even get cash for their product. When the music stops, IBM won’t simply sell less software to companies, they won’t even get paid for something they’ve already sold, so they won’t have any money to refinance their debt. Companies like IBM have the potential to go down 90% (That’s not a prediction.).

When you make your capital structure more brittle, the business doesn’t have to go down 90%. The stock will go down a big portion of that. But your equity is highly, highly levered. On the upside this is great, especially for the upper executives. But the down side is very, very lethal. Low interest rates made it logical for all of these companies to play this game in their own self-interest. This game, though, also made the market extremely dangerous and is another reason I expect it to go very, very much lower.

Moneychanger: I remember well a speech Bernanke made in November 2002 long before he was appointed head of the Federal Reserve. It earned him the nickname Helicopter Ben because, if he didn’t say in fact, he certainly implied that in a financial panic he would drop $100 bills out of helicopters.

Oliver: He said he had a technology called a printing press.

Moneychanger: Right — that famous statement. Anyone who read tha had some idea of what Bernanke would do, but the performance in fact astounded me. He doubled the size of the Federal Reserve’s balance sheet in three months. He created that much money and then lowered interest rates to zero and God only knows whatever else he did. He loaned $16 trillion to foreign banks and everywhere else to keep the whole world afloat. If they do that in the green tree, what will they do in the dry?

My imagination falters to think of what they will do to save the banks this time. This is also part of the historical record, that the people who engineer bubbles are usually powerful enough to get the government to rescue them. What in the world will it look like this time?

Oliver: I think that’s the right question. Bernanke didn’t really drop money from helicopters. Remember the Austrian model of a credit bubble is that banks made bad loans to very capital intense industries, then they run out of money because banks fail. And then the Keynesians say, “Look, demand has faltered.” No. Demand hasn’t faltered. You have built over capacity.

Then the Keynesians say, “We need to recapitalize the banks.” So Bernanke didn’t give money to consumers to buy stuff. He gave money to banks to lend it to create more capital and this capital actually has the adverse effect of lowering prices of things that capital produces.

That’s how he created a new bubble. Because of Bernanke’s low interest rates, the banks doubled down on the model and, of course, debt levels are much higher now than then. So it wasn’t the printing press. He created credit reserves at the central bank.

Now the imbalances are much, much greater than they were. And the Fed was not designed to do this. It wasn’t designed to support the government. But that’s what’s happening. It has become a mechanism to finance the state. That is its stated mission at this point.

When markets crash and stocks collapse, government tax revenues dry up. What does the government do? She borrows money so she can keep spending. The Fed’s job is to run in and make sure that the treasury bond market is working. That finances the state.

Yes, when things are bad enough they will run out and support the banks to keep prices rising, as in that two percent inflation target they have. It’s crazy but it’s their target to support the market. To me it wasn’t the fact that they doubled up the monetary base or tripled it.

In autumn of 2008 the Fed issued $6 trillion in guarantees. The guarantees weren’t triggered but if you’re a private company and the guy you lent money to is shaky, and the Fed says, “Hey, don’t worry, if he doesn’t pay you, we will” – well, okay. Now you’re more patient. Also, don’t forget Bernanke’s Fed suspended mark-to-market accounting, which gave the banks more time to recover. Now because the imbalances are so much greater than they were then, to stabilize the system in the next crash we’ll be talking numbers much, much bigger than last time.

I don’t know exactly. No one knows because a lot of the bubble is the shadow bank system and no one can get a handle on how big it is. But it’s going to be enormous. It’s not going to be $6 trillion. It will be $12 trillion – numbers of that magnitude.

The next question is, do the guarantees work? Again, the Fed guarantees these crappy assets in the banks. What happens when the private bank says, “You know what? The bond is dead. We’re calling in the guarantee. Here’s this paper back, we want the money.” Suddenly those bad assets –bad credit — get converted into currency. That’s when you start getting the big [consumer price] inflation that’s been missing from the equation because they didn’t print currency. They printed credit. But when you convert that credit into currency to keep the system afloat, which they will do in extreme situations, then comes the crushing inflation.

This scares me because I think it’s inevitable. It’s inevitable because the alternative is to allow a 1930s style depression where the banks all collapse and close.

Moneychanger: Is hyperinflation really possible in the United States? It’s the largest, strongest economy in the world. Does it make sense to talk about hyperinflation?

Oliver: It’s not that it could happen, it already has happened. Look at the American Revolution. The 1970s aren’t comparable because the private and federal debt levels in the 1970s were not that high. Look at debt as a percent of GDP or in terms of gold. Today the debt levels have gone vastly, vastly, vastly higher.

Hyperinflation is certainly not inevitable. They could take a 1930s outcome, which I think is better, but hyperinflation is not an event, it’s a process. When the treasury bond market complex collapses (which it will) and rates are going crazy and the federal government cannot fund itself and no one else can fund themselves, then the Federal Reserve will buy bonds wholesale everywhere to stabilize interest rates and prices.

When they start buying things above market price, they suddenly become the only buyer and they have to buy all. Then their balance sheet will increase to three times, 20 or 30 times, numbers like that, and that’s when you get a huge inflationary chill. But what will they do next? What if they just stop? Maybe a one-time devaluation that would set the dollar lower by a big number, 70 – 80%. Then the country would move on with a lot less debt and everyone would be happier.

But they never stop and allow something like this to play out because stopping is very, very painful. Everyone says, “Hey, this is great. I’ll take on more dollar debt and I’ll gamble.” Don’t forget. You have an agency problem here, not just people with their own money. They’re running banks, corporations. Say you’re a CEO. You’re not very rich but you say, “If I can get stock options a whole bunch of my debt goes away because I personally made a lot of money. And if it goes wrong it’s not my money. It’s someone else’s. I’ll just keep doing that until the market forces the Feds to end this game because of inflation.”

It’s hard to imagine in our world where more than half the country are direct recipients of government spending. When that stops, would everyone say, “Let’s just go back to free market”? Hard to envision, but possible.

So maybe we see not wide margins hyperinflations but certainly 1970s plus type hyperinflation.

Moneychanger: Weimar Germany’s 1923 hyperinflation just ended in exhaustion. The Rentenmark that replaced the Reichsmark was not particularly strong, but it was accepted because something had to stop the hyperinflation.

More than 50% of the people in the United States take their income from government spending, more than 50%. Hyperinflation would throw those people out on the street – a huge social disruption.

Oliver: It wouldn’t take hyperinflation, just high inflation.

I think if Trump wins the next election, something bad will happen. I think the market will crash. Certainly, two years is a very long time for this market to survive, but does he blame the Fed and everyone believes him, and then he’s elected?

Or does the pendulum swing from Trump to someone hard core left like Cory Booker or Elizabeth Warren? If the pendulum swings way to the left then things like hyperinflation become more realistic because the government would essentially be run for the people getting money from the government. And then the Fed would be mandated to support this type of spending.

Elizabeth Warren proposes that all corporate boards with more than a billion dollars of revenue have labor representatives, Medicare for all, and forgiving student loans. How would all this be financed? Through treasury bonds and who has the treasury bonds? The Federal Reserve. The path to hyperinflation, certainly a very high inflation, would go through a left-wing victory in 2020.

Moneychanger: Right. Looking at what the Fed did already they’ll do anything to keep the system going.

Oliver: It’s crazy but the system is pernicious and evil and should go away. But they’re very powerful and their job is to maintain it as long as they possibly can and they will. Don’t forget the people at the Fed come out of the biggest banks in the world. So the prospect of these guys getting religion and letting big banks go down is fantasy. It will never happen until there are riots in the streets.

Moneychanger: Until that complete exhaustion.

Let me ask about gold. I’ve been in the gold business since 1980 and I’ve never been through a time as weary and disappointing as the last two years. In our January 2017 interview, you said that a low interest rate environment is very bad for gold because gold has no cash flow and hence it goes down. Did you expect it to go down this much?

Oliver: It’s counterintuitive but in a low interest rate environment, economically sensitive assets like buildings and ships become very valuable because cash flow is discounted at a low interest rate — so valuable you want to build it. To build a building you acquire huge amounts of industrial commodities, which pushes up their prices. [See chart 6.]

Gold generates no income, no cash flow. It’s not subject to those forces, so on a relative basis it falls against everything else in a credit boom. History clearly shows that gold does badly during credit booms, and then the opposite happens. When rates shoot higher and no one wants to build buildings the next 30 years because too many have been built, gold shines. All of the pieces that go into construction are now in massive overcapacity up and down the supply chain so the pricing collapses. Gold is relatively immune to this story.

It’s not an expectation that gold would do so badly, it’s a realization that as long as the bubble lives gold will not do well relatively. I now expect that because the bubble is fraying that we are near to a huge reset in the gold price.

Still, there are other issues. When the music really stops you get your Lehman moment and panic for dollars. [See chart 7.] Don’t forget, there’s $4 trillion dollars that exist on that Fed balance sheet, and there’s $90 trillion of dollar denominated debt globally that needs dollars all day long to pay interest. When there aren’t enough dollars to go around a big short squeeze occurs and the dollar becomes really, really valuable. People sell whatever assets they can for dollars to pay their debts. If they don’t pay their debts they lose their collateral.

Is gold one of the things they’ll sell? In 2008 the answer was yes because hedge funds and momentum players had been riding the gold trade up from 2000. They were forced to sell gold to get collateral for their other assets. [See chart 8.] I don’t see that today. Today if anything there’s a short gold position and those shorts will have to buy gold, not sell it.

That’s the western market. In the eastern market, especially in China, some debts are specifically backed by gold collateral, so when they default the lender takes the gold and sells it because he needs cash to pay off his creditors. You saw a big drawdown in the gold price last summer because the Chinese bank system is under pressure. In Turkey the price of gold was a full three dollars less than global market which told you that gold collateral was being liquidated there.

But that’s temporary. I’m not at all certain which way gold will go immediately when the music actually stops. I think higher, but I am sure that when the dust settles gold will be very, very much higher than it is now.

What’s the takeaway? Don’t hold gold on leverage because if it drops for a month you’ll be knocked out of the trade and miss the move to $10,000. But if you have it in an equity position (fully paid for and owned) then you could ride down that volatility and not worry about it.

Moneychanger: Back in 2008 gold tanked before stocks, but not only did it recover faster than stocks, bottoming in November before stocks bottomed in March, for the next three years it also vastly outperformed stocks. Will gold behave the same way this time? Then gold was in a bull market phase, having peaked at $1,000 in March 2008. Today gold is in a completely different world. It has been in a bear phase since 2011 and these last two years have wrung out gold’s price. A massive short overhangs the market. Commitments of Traders short positions are at 15 or 20 year highs. Although there obviously will be a run for dollars when the panic arrives, you just have to wonder if it will look exactly like it did in 2008. And it doesn’t seem to me that it will.

Oliver: I don’t think it will, for the reasons you just stated. I think gold will go straight up. When we’ve seen big down days on the stock market we’ve seen gold have big uptakes and vice versa. The market is signaling us that’s how it will happen.

I think gold stopped at $1,900 in 2011 because the Fed was able to restart a new and bigger credit bubble. When the next big crisis comes can they do it again? Can we get another cycle up out of this super cycle?

I’m not all sure about that. If that is the case, we do expect gold to run to $3,000 plus, after a big crunch when the Fed has to print money to supply lots of dollars to the world so they can pay their debts and not default. Then if they create a bubble I would expect another period of time when gold is very weak. That’s the cycle we’ve been playing now for 40 years at least, for 4,000 years in some form.

But it’s also possible that the Fed’s efforts to re-start don’t work. Maybe we’re tapped out. Maybe there’s just too much capital misallocated, so when the Fed guarantees all the assets, people actually take the guarantees. Then you can see gold prices up at $10,000 plus — completely resetting the system.

As recently as the 1930s the market staged a run on the central bank by presenting paper dollars to be redeemed in gold. You can’t go with dollars to the Federal Reserve to get gold today, but you can go to the coin store and buy gold with dollars. I can’t redeem them but I can convert them into gold.

In 1980 gold peaked over $800. At $600 an ounce the 8,300 tons of gold on the Fed’s balance sheet completely backed their liability, the dollar. We were on a de facto economic gold standard. It represented a run on the Fed. I see the exact same thing happening when the Fed finally loses control of interest rates and people convert dollars to gold – gold will rise to a price that balances the Fed’s balance sheet. That is a very, very big number. I almost don’t want to say it because it sounds so crazy. When the super cycle ends you’re going to see gold over $10,000 for sure.

Moneychanger: You have called this the greatest debt bubble the world has ever seen. If so, then it’s the end of the super cycle.

Oliver: That’s right. And again, these things don’t crash. They’re not just economic, they’re political, too. The debt in France brought on the French Revolution. Think of the Russian Revolution. When the Depression hit we got Franklin Roosevelt who was basically a fascist. The National Recovery Act (NRA) was based on Fascism, but the Supreme Court shut it down. The idea was a government-regimented economy, but we escaped.

It’s never just an economic event, it’s also political. When half your country draws its income from government spending and that all goes away in real terms there will be major political ramifications.

That’s what really scares me. Do we go down the hard Fascism road where government, the guys in charge of banks, and the government just don’t let the system collapse but send tanks out to keep people in line? Or do they let it go down so we can start writing off the debt again and return to a free market? I’d like to think it’s the latter, but I don’t know.

This country was pretty homogenous last time this happened, a Protestant Christian nation for the most part. That’s no longer true. We have multiculturalism, people with different ideas. I don’t know that we have the cohesiveness to survive the political problems that this collapse, the greatest in history, will create.

Moneychanger: People accept Fascism because they have no other hope. It’s certainly foreseeable that when this debt bubble crashes a lot of people will be left with no hope. Anything is preferable to chaos and starvation.

Oliver: In 1935, the Supreme Court said the NRA was unconstitutional after Roosevelt’s court packing tactics. Over the last 70 years they’ve essentially eviscerated the constitution. It’s very scary.

Moneychanger: It is, but there’s also the hope buried in there somewhere that we’ll get rid of the Federal Reserve.

Oliver: That is a hope, too. Absolutely. The American country which has been forgotten is still very solid unlike the elites who run everything. The country is very divided, more and more so all the time between the hard left and people who adhere to traditional American virtues and values.

When the government starts doing crazy things what happens? What does the Texas National Guard do? I don’t know. I would hope that the system is robust enough that states build up power and get the people to say we will not go down this road these elites want to take.

Moneychanger: I think there is a solid core of Americans that sees and knows something is wrong but there’s no direction for them to go. That’s the reason why Trump — good, bad, or indifferent – has been so popular. He offered an alternative to the elites.

Oliver: The last ad he ran he was in some manufacturing plant or hanger with the workers and he had a montage of Janet Yellen and Lloyd Blankfein and the whole crowd. I thought, This is the conflict. This is why he’s going to win. And he did.

Moneychanger: I deeply appreciate the time you have given me.

Originally published October 2018

Revealed: Four senators dumped millions in stocks while Capitol Hill was being briefed on the coronavirus threat but BEFORE markets started tanking

- Richard Burr, head of the Senate Intelligence Committee which was directly briefed on coronavirus, sold up to $1.7m in stock between January and February

- Dianne Feinstein, on the same committee, sold up to $6m in stock in same period

- Kelly Loeffler, on the Senate Health Committee, sold up to $3.1m in stock starting on the day her committee was briefed by the CDC

- James Inhofe sold up to $400k in stocks including real estate all on January 27

- Coronavirus symptoms: what are they and should you see a doctor?

By NIKKI SCHWAB, SENIOR U.S. POLITICAL REPORTER FOR DAILYMAIL.COM and CHRIS PLEASANCE FOR MAILONLINE

PUBLISHED: 17:02 EDT, 19 March 2020 | UPDATED: 10:17 EDT, 20 March 2020

Four senators dumped millions of dollars worth of stock while Capitol Hill was being briefed on the threat of coronavirus but before the markets tanked as infections soared, disclosure records have revealed.

Republicans Richard Burr, Kelly Loeffler and James Inhofe and Democrat Dianne Feinstein collectively offloaded up to $11million in stock between late January and early February, according to records seen by The Daily Beast, New York Times and ProPublica.

Burr, chair of the Senate Intelligence Committee that was directly briefed on coronavirus, sold up to $1.7million in stock including in hotels, according to reporting from ProPublica.

Feinstein, a member of the same committee, sold up to $6million in stock including in a biotech firm.

Loeffler dumped up to $3.1million in investments starting on the day the Senate Health Committee, which she sits on, was briefed by the CDC. Meanwhile James Inhofe sold up to $400,000 in stock including real estate.

Loeffler and Feinstein have defended themselves, saying their stocks are invested in trusts and portfolios that they have no personal control over. Inhofe has not commented.

Burr’s spokeswoman said in a statement to DailyMail.com that Burr filed his financial disclosure form several weeks before the markets showed ‘volatility.’

The Stop Trading on Congressional Knowledge Act prohibits members of Congress from insider trading based on classified information they have received in briefings.

The chairman of the House Intelligence Committee, Sen. Richard Burr, knew of the coming coronavirus crisis three weeks ago and divulged details of the chaos that would ensue to a group of well-heeled constituents

Sen Kelly Loeffler (pictured) reportedly sold $3.1million in stock with the first sale made on January 24, the same day her committee was briefed by the CDC10

Sen. Jim Inhofe, a Republican from Oklahoma, sold up to $400k all on January 27

Dianne Feinstein who sits on the Intelligence Committee which was also briefed on coronavirus, sold up to $6m in stock

According to The Daily Beast, Sen Kelly Loeffler and her husband, Jeffrey Sprecher, the chairman of the New York Stock Exchange, sold $3.1million in stock between late January and early February.

The first sale was in the firm Resideo Technologies worth between $50,001 and $100,000 and made on January 24, the same day her committee – the Senate Health Committee – held a briefing with the CDC.

The stock has since halved in value.

During the same period the couple made just two purchases, one of which was stock in a tele-working company that has seen an increase in price amid office shutdowns.

Meawnhile Richard Burr, Republican chair of the Senate Intelligence Committee which was being briefed on coronavirus, offloaded between $582,029 and $1.56million of his stock holdings in mid-February.

Burr later went on to warn people at a meeting in Washington that coronavirus was likely to cause significant disruption to businesses, even as Donald Trump was playing down the threat.

Dianne Feinstein, a Democratic member of the same committee, and her husband also sold between $1.5 million and $6 million in stock in California biotech company between late January and mid-February.

Elsewhere James Inhofe, Republican of Oklahoma, sold stocks totaling $400,000 on January 27 including shares in PayPal, Apple and Brookfield Asset Management, a real estate company.

Loeffler’s sell-off began the same day the committee she sits on was briefed by the CDC, which she later tweeted about

Loeffler has defended herself, saying her money is invested in a portfolio she has no control over. Feinstein also said her stocks are held in a blind trust, which she does not control

ProPublica reported that on February 13 Burr sold of stock holdings in 29 separate transactions. A week later the stock market started its downward trend, now losing about a third of its value.

Burr dumped $150,000 worth of shares of Wyndham Hotels and Resorts stock and $100,000 worth of shares of Extended Stay America.

The hospitality industry has been one of the worst shattered in this collapse.

Then, on February 27 Burr gave well-heeled constituents from the Tar Heel State a dire warning about the kind of chaos the coronavirus could cause.

The North Carolina Republican is heard on a secret recording obtained by NPR telling members of the Tar Heel Circle on February 27 that the coronavirus was ‘much more aggressive in its transmission than anything that we have seen in recent history.’

‘It is probably more akin to the 1918 pandemic,’ Burr told the group, who pay between $500 and $10,000 for membership of the group, according to NPR’s reporting.

In a series of tweets, Burr pushed back and said he was addressing the membership of the North Carolina State Society. ‘The message I shared with my constituents is the one public health officials urged all of us to heed as coronavirus spread increased,’ he also said.

A spokesman for Feinstein said that all of her stock holdings are in a blind trust, and that she has no involvement in financial decisions made by her husband.

The luncheon that was taped was held at the Capitol Hill Club, a social club for Republicans located steps away from the Capitol Building.

+10

Rep Alexandria Ocasio-Cortez led the calls for the resignations of both Koeffler and Burr shortly after the news broke on Thursday

+10

+10

There, Burr spelled out some of the broad repurcussions of the brewing outbreak.

‘Every company should be cognizant of the fact that you may have to alter your travel. You may have to look at your employees and judge whether the trip they’re making to Europe is essential or whether it can be done on video conference. Why risk it?’ Burr told attendees.

He also previewed school shutdowns.

‘There will be, I’m sure, times that communities, probably some in North Carolina, have a transmission rate where they say, “Let’s close schools for two weeks. Everybody stay home,’ the Republican lawmaker said.

Burr also said the military would be utilized.

‘We’re going to send a military hospital there; it’s going to be in tents and going to be set up on the ground somewhere,’ he said. ‘It’s going to be a decision the president and DOD make. And we’re going to have medical professionals supplemented by local staff to treat the people that need treatment,’ he added.

Burr was not sounding a similar alarm publicly. And the leader of his party, President Trump, was downplaying the risk the same day.

‘It’s going to disappear. One day, it’s like a miracle. It will disappear,’ Trump said. ‘It could get worse before it gets better. It could maybe go away. We’ll see what happens.’

Three weeks later, Burr’s assessment was right on the money.

A week ago Wednesday, Trump announced that travelers from Europe who were not Americans or U.S. residents would be banned.

On Thursday, the State Department told Americans to come home from abroad now – and to not count on government help.

Schools, colleges and universities across the country have been closed down. And the military is doing its part to deal with the outbreak.

Later on Twitter, Burr blasted NPR saying the lunch was sponsored by the North Carolina State Society. ‘They aren’t “secretive: or “high-dollar donor” organizations.

‘Unfortunately, NPR’s journalistic malpractice has raised concerns that Americans weren’t warned about the significant steps we may have to take to stop the coronavirus threat. That’s not true,’ Burr said.

He pointed to comments Trump made on February 26, when the president said ‘every aspect of our society should be prepared.’ Though Trump used the caveat that the preparations should be made ‘just in case.’

‘Purposefully misleading listeners for the sake of a “narrative,” like NPR has done, makes us less safe,’ Burr wrote.

On the ProPublica report, a spokesperson for Burr told DailyMail.com, ‘Senator Burr filed a financial disclosure form for personal transactions made several weeks before the U.S. and financial markets showed signs of volatility due to the growing coronavirus outbreak.’

‘As the situation continues to evolve daily, he has been deeply concerned by the steep and sudden toll this pandemic is taking on our economy,’ the statement continued. ‘He supported Congress’ immediate efforts to provide $7.8 billion for response efforts and this week’s bipartisan bill to provide relief for American business and small families.’

The statement didn’t push back on the allegations found in the reporting outright.

Pointing to the NPR and ProPublica reports, Rep. Alexandria Ocasio-Cortez – one of the most famous House Democrats – called for Burr’s head.

‘As Intel chairman, @SenatorBurr got private briefings about Coronavirus weeks ago. Burr knew how bad it would be. He told the truth to his wealthy donors, while assuring the public that we were fine. THEN he sold off $1.6 million in stock before the fall,’ Ocasio-Cortez tweeted Thursday. ‘He needs to resign.’

The upcoming job losses will be unlike anything the US has ever seen

PUBLISHED FRI, MAR 20 20207:13 AM EDTUPDATED FRI, MAR 20 202011:10 AM EDT

Jeff Cox@JEFF.COX.7528@JEFFCOXCNBCCOM

KEY POINTS

- The coronavirus crisis is likely to result in layoffs on a scale that the U.S. has never seen before.

- Economists expect April to be the first reporting month when the damage starts to show up.

- Forecasts for that month range from 500,000 to 5 million.

- The worst month during the financial crisis saw nonfarm payrolls decrease by 800,000.

- Weekly jobless claims numbers are expected to be so bad that the White House has reportedly asked state officials to delay releasing precise counts.

When the damage the coronavirus inflicts on the U.S. jobs market becomes clearer, it could be unlike anything the country has ever seen.

Judging by numerous forecasts from economists, the avalanche of furloughs will easily break the record for most in a single month.

Upcoming weekly jobless claims will shatter the standards set even during the worst points of the financial crisis and the early-1980s recession, with Bank of America forecasting a total of 3 million when the number is released Thursday. Those figures are expected to be so bad, in fact, that the Trump administration, according to several media reports, has asked state officials to delay releasing precise counts.

While the headline unemployment rate is highly unlikely to approach the 24.9% during the Great Depression, it very well could be the highest in almost 40 years, something unthinkable for a jobs market that had been on fire as recently as February.

Job losses will be counted not in the thousands or even hundreds of thousands, but rather in the millions. Although it’s uncertain whether the total count from this recession ends up breaking previous records, it’s a good bet that April’s number will outpace by a large margin any single month in U.S. history for a drop in nonfarm payrolls.

5 million in April alone?

The worst month for job losses during the financial crisis was 800,00 in March 2009.

Some forecasts see April quintupling that or worse. Forecasts for that month range from 500,000 to 5 million.

“There’s just so much that we don’t know about how long the disruption to economic activity related to the containment of the virus will be. That does make forecasting these things very difficult,” said Jeremy Lawson, chief economist at Aberdeen Standard Investments. “By the time you get to the April payroll number, which may be right at the deepest level of contraction, yes, those numbers are plausible certainly.”

Because of the way the Labor Department conducts its sampling, the March nonfarm payrolls report probably won’t reflect the worst of the layoffs. Where those numbers will show up is in weekly jobless claims figures.

Looking further ahead to April, Lawson said a drop of 500,000 for the month “is not an unreasonable starting point.” Other forecasters, though, see a far gloomier picture.

Ian Shepherdson, chief economist at Pantheon Macroeconomics, sees the possibility of 5 million job losses in that month alone.

“We never imagined we’d write anything like this,” Sheperdson said in a note. “The shock will be so great that it will leave policymakers with no choice but to pass much more stimulus than is currently under discussion.”

When all is said and done, the unemployment rate will be 10.6%, and there will be 17.9 million Americans on the unemployment line, or about 12 million more than in February, according to a projection from Steven Blitz, chief U.S. economist at TS Lombard. The current jobless rate is 3.5%, the lowest in more than 50 years.

If Blitz is right, that would put unemployment at its highest percent level since December 1982.

Elsewhere, the Economic Policy Institute projects 3 million job losses during the summer, while Citigroup economist Veronica Clark said the rise in jobless filings “is just the start of a period of a rapid increase in claims over the next few weeks.”

“If there is not a normalization of activity by mid-April (which looks increasingly unlikely), we would not be surprised to see job losses in the multi-millions next month,” Clark wrote.

One survey released Thursday painted a far gloomier mosaic: SurveyUSA indicated that 14 million people already have experienced temporary layoffs, while 2% of the workers have lost their jobs outright. A bright side: A Towers Watson survey said 52% of employers who experience a shutdown will continue to pay employees.

A call for even more stimulus

The big layoff numbers are not likely to show up until the April data is released in early May. The March report could be somewhere around flat as the sample period the Labor Department will use for its estimate is the week ended March 14, before some of the worst news came about companies cutting workers.

Since then, Marriott International has announced it will cut thousands of workers, and similar moves are expected to be executed throughout the hospitality and food and beverage industries.

One upside to the coronavirus scenario is that most economists still expect the downturn to be brief compared to other recessions, with the worst news front-loaded.