HI Financial Services Commentary 03-13-2018

You Tube Link: https://youtu.be/nXXQ1Q57WTg

What I want to talk about today?

What is the Difference between Institutional & Speculation?

My question is simply this. What makes your institutional advice so dominant?

2116

Blog/Training Tools

Posted Mar 12, 2018 by Martin Armstrong

ANSWER: Interesting question. Institutions CANNOT be flipping their portfolios back and forth. They are not interested in what will the Fed do next week. They cannot react to such short-term swings. Our models are fractal and dynamic. We have the largest database ever assembled and that is what it takes to do accurate long-range forecasting. What you also must understand is how can a guy write a book and describe the feeling it is to give birth. Sure, he can interview women and write down the overview of what they say. But he cannot possibly really know what it feels like.

Look, 99% of all these self-proclaimed analysts have NEVER traded size. They look at the market from a short-term trader perspective and do not even understand how to do strategically position a portfolio of size. Oh sure, they can advocate the standard 60% equities and 40% bonds. Yet what happens when government bonds default? What happens when 10-year rates are 3% or less and you need to make 8% to cover your liabilities moving forward? They are clueless when it comes to actually the problems in size and how you even place orders.

The questions from institutions are strikingly different. They need to know when major trends change and how to adjust their portfolio and when. Our asset allocation is by no means 60-40. They are not concerned about when is the high Tuesday or Wednesday. Therefore, our institutional services are strategically different. You are either long or short. There is no pension fund that can buy even a 10-year government bond paying 3% for they are locking in a 50% loss or more. If you have not played in the big leagues, don’t bother. How you hedge is strikingly different from speculative trading.

We are able to differentiate between short-term changes in trend and long-term. That is the key. Plus, even if someone comes up with a new model and tries to get a meeting with a major institution if they can get 15 minutes that will be a miracle. Why? Nobody is going to take an unproven model for if it fails, that person loses their job.

What happening this week and why?

Headline risk vs news

News is a single one time event that verifies a continued or new trend

Headline risk is a tweet, headline, a news blurb,

Tariff leads to a trade war, which leads to More tariffs that eventual lead to higher prices,

Shock pricing leads higher inflation which leads to the ….

Rapid Federal Reserve Interest rate hikes, which leads to even higher costs and borrowing

Free MARKETS are hard to achieve, NEVER are fair, but over time regulate pricing power to be more equal for everyone

Larry Kudlow as the new Secretary of State

Where will our markets end this week?

Lower

DJIA – Technically Bullish still but passed below the 50 SMA

SPX – Bullish

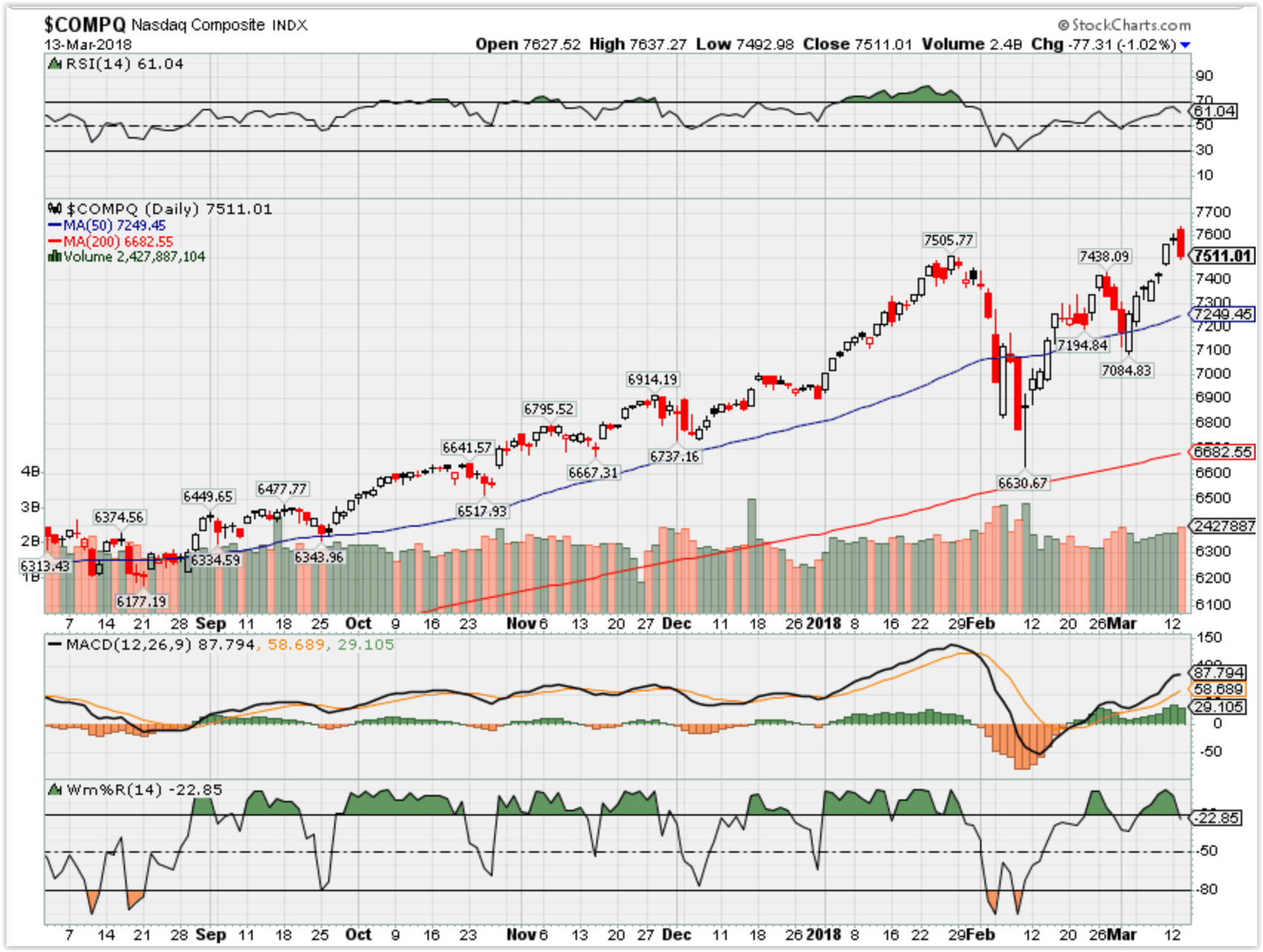

COMP – Bullish

Where Will the SPX end March 2018?

03-13-2018 -2.0%

03-05-2018 -2.0%

02-28-2018 -3.0%

What is on tap for the rest of the week?=

Earnings:

Tues:

Wed: CTRP, DDD

Thur: DG, GCO, SHLD, ADBE, AVGO

Fri: TIF

Econ Reports:

Tues: NFIB Small Business Optimism, CPI, Core CPI

Wed: MBA, Retail Sales, Retail ex-trans, PPI, Core PPI, Business Inventories

Thur: Initial, Continuing Claims, Export, Import, Empire Manu, Phil Fed, NAHB Housing Market Pricing , Net Long term TIC Flows,

Fri: Housing Starts, Building Permits, JOLTS OPTIONS EXPIRATION

Int’l:

Tues –

Wed –

Thursday –

Friday-

Sunday –

Questions???

www.myhurleyinvestment.com = Blogsite

customerservice@hurleyinvestments.com = Email

How am I looking to trade?

Looking to add protection

Trump shaking up market for now, but only trade wars would bring big sell-off: Analysts

- The president’s trade actions and personnel shake-ups are causing turbulence for the market, but for now, analysts do not see a major sell-off unless a full-blown trade war breaks out.

- Trump abruptly let go Secretary of State Rex Tillerson just after agreeing to talks with North Korea, and a few other shoes are expected to drop in coming days.

- The Trump administration is now threatening trade actions against China, after broadly imposing steel and aluminum tariffs.

President Donald Trump has beeninjecting uncertainty into the stock market lately, and the jolts and volatility could continue as long as investors worry about trade wars.

But analysts see market turbulence, for now, not necessarily a deeper sell-off.

“If you look historically, political headlines tend to bother people for about 15 minutes, and the market tends to move on. Even concerning political headlines tend to not roil the markets for sustained periods in general,” said Jonathan Golub, Credit Suisse chief U.S. market strategist.

“I think the same applies to trade concerns,” he said. “If we end up in a full-blown trade war, that would be bad. But at this point in time, we’re far away from that.”

Stocks were rocky Tuesday morning after Secretary of State Rex Tillerson was let go by the White House, just days after the administration agreed to talks with North Korea. The market brushed that off.

But stocks really tumbled when reports started to circulate Tuesday afternoon that the Trump administration could slap tariffs on China on technology, apparel and other imports. Under consideration were also investment and visa restrictions.

The Dow closed off 0.7 percent to 25,007, and the tech-heavy Nasdaq lost 1 percent to 7,511. The S&P 500 was down 0.6 percent at 2,765. It is 3.75 percent away from its high after February’s market sell-off, which was kicked off by interest-rate concerns, not political drama.

Dan Clifton, head of policy research at Strategas, said the Tillerson move will no doubt be followed by other shake-ups but that should not send longer-term shock waves through the market.

“It’s possible that H.R. McMaster goes,” Clifton said. “I think John Bolton might replace him as national security advisor.” Bolton is a former U.N. ambassador who is viewed as hawkish.

“You’re getting a much more Trumpian administration,” Clifton said. “Bolton seems more Trumpian than McMaster. Larry Kudlow seems much more Trumpian than Gary Cohn.” Trump earlier said that Kudlow,CNBC senior contributor, has a good chance at succeeding Cohn as his top economic advisor.

“It seems Trump is putting in his next wave of personnel here,” said Clifton. Those types of moves shouldn’t impact the market “as long as that’s contained and the results of this is just palace intrigue.”

Golub said, “When you’re investing in the S&P and the Dow, you’re not investing in the White House. You’re investing in well-run corporations with global footprints and wonderful products.”

More worrisome were reports about tariffs on China. Politico first reported that U.S. Trade Representative Robert Lighthizer suggested tariffs on $30 billion in Chinese goods but Trump sought even more. Reuters later reported Trump would target $60 billion.

“If you start having a Chinese trade war or greater geopolitical risk, then it starts to become a greater worry for the market overall,” Clifton said. He said the size of the tariffs on Chinese goods was greater than expected and could be a negative for the market.

Trade has been the one big worry hanging over markets since Trump’s election. His other policies have been market positives, particularly tax cuts. But the level of anxiety has risen since Trump imposed tariffs on imported steel and aluminum, and unease remains about the NAFTA negotiations with Canada and Mexico.

“We already have tax cuts and deregulation,” said Edward Keon, portfolio manager at QMA. “That’s on the books. But on trade, the market rightly fears that could easily spin out of control.”

Keon said the trade story depends on how trade partners respond. “It’s complicated from a game-theory point of view of who is going to do what. The market then worries that this is going to be not just one action but a series of actions.”

Keon said he also viewed the administration’s blocking of Broadcom‘s proposed purchase of Qualcomm as a negative undercurrent for the market. Although Broadcom is based in Singapore, a U.S. panel found that it was a competitive concern with China.

“Concerns about the possibility of a trade war and concerns about the shutting down of one tech deal may be a precursor for others and that may imply lower valuations for technology companies,” said Keon.

Keon said the markets weren’t that concerned about the musical chairs in the Trump administration, but the fact that Kudlow was in the running for a White House post was a positive.

“The market is clearly concerned about trade. Having a free trader in the top economic spot is probably good news. If you balance that out over the course of the day, having a globalist like Rex Tillerson out and this new report of tariffs maybe rekindled fears of possible trade wars,” Keon said.

https://www.cnbc.com/2018/03/13/stock-market-nearing-old-highs-but-at-cheaper-prices.html

Stock market nearing old highs, but at ‘cheaper’ prices

- At the late-January high, stocks were at their loftiest valuation of this cycle versus expected earnings and compared to Treasury yields.

- In late January, the S&P traded at 18.5-times forecast earnings for the next 12 months. Now the index is back to 17.4 forward price/earnings multiple.

- And a bit of simple market algebra could be used by the bulls to pencil in a run to 3000 on the S&P 500 – up 8 percent from here.

Michael Santoli | @michaelsantoli

The S&P 500 has worked its way higher in a jagged but estimable 10 percent climb off the low set early on Feb. 9, which for now represents the depths of the market’s first serious correction in two years.

The index now sits about 3 percent from its record high set Jan. 26. That threshold, at 2872, is certainly within sight and reach, and could be revisited with just a bit release of tensions along the trade-policy or interest-rate fronts.

At the late-January high, stocks were at their loftiest valuation of this cycle versus expected earnings and compared to Treasury yields. And as the S&P shot up more than 7 percent from New Year’s to the peak, investor optimism and aggressive risk-taking reached parallel extremes.

The good news is that the swiftest double-digit correction from an all-time high last month skimmed some froth from both valuations and sentiment.

In late January, the S&P traded at 18.5-times forecast earnings for the next twelve months. Now — with profit estimates continuing to rise at a rarely seen pace thanks to tax cuts and global growth — the index is back to 17.4 forward price/earnings multiple. That’s still a bit rich, but investors have already proven they can stomach owning stocks above that valuation, if confident in the growth outlook.

Investor mood was certainly shaken, even if acute panic never quite took hold in the selloff. The CNN/Money Fear-Greed Index reached depths below 20 on a 0-100 scale in recent weeks, down from around 80 in January and is now near 40.

So even if the S&P blipped higher another 3 percent to retake the former highs fairly soon, it’s likely that valuation and sentiment would be less extended this trip — leaving a bit more headroom for a foray into fresh record territory.

And a bit of simple market algebra could be used by the bulls to pencil in a run to 3000 on the S&P 500 – up 8 percent from here. Just slap January’s peak multiple on today’s forward earnings forecast and the index is there – and would mean a 12 percent gain from year-end 2017, which would come with dividends of close to 2 percent and make for another above-average year.

Simple as it seems, any trip to those levels would likely have twists and stops along the way.

Longtime tech investor Paul Meeks warns a correction ‘could happen at any time’

Stephanie Landsman | @stephlandsman

Published 4:46 PM ET Sat, 10 March 2018

The investor known for running the world’s largest technology fund during the dotcom boom is refreshing his call for investors to keep their portfolios light on the tech sector.

Sloy, Dahl & Holst chief investment officer Paul Meeks sees near-term trouble approaching based on frothy stock prices.

“Because they’re so volatile high beta [risk] stocks, when they correct they don’t just go down 2 percent. They go down 20 percent,” he said Friday on CNBC’s “Trading Nation” in an interview this week. “It could happen at any time.”

His latest call comes as Wall Street celebrates the Nasdaq‘s rebound to all-time highs. Since the February correction lows, the index has soared more than 7 percent.

“Valuations are extended for some of the names, and everybody’s favorite names particularly the FANGs,” said Meeks, referring to the widely-held group of tech stocks: Facebook, Amazon, Netflix and Google [the holding company of Alphabet].

But that doesn’t mean the former Merrill Lynch portfolio manager is abandoning his positions. Meeks, who owns Apple shares and has broad exposure to tech stocks, contended the backdrop is strong.

“I’ve been covering the tech sector for a very long time, and I can say in my heart of hearts that the fundamentals relative to the other 10 sectors in the S&P 500 are as good as they’ve ever been,” he noted. “Fundamentally I like it — particularly certain themes for tech spending within the sector.”

A tech swoon would be a major buying opportunity for Meeks, who’s putting together a list. He says he’s planning to pounce if there’s a 10 to 20 percent downdraft, because once it winds down, the Nasdaq could still see a strong year.

Facebook is a FANG stock making his list, as well as some semiconductors.

“Advanced Micro Devices today [Friday] is down 2 or 3 percent when the market is raging. Same thing with Micron. I think some of the semiconductors have fallen and they haven’t gotten back up,” Meeks said. “But I think they’re some good opportunities.”