HI Market View Commentary 03-23-2026

OK LET’S Go Over three rules of trading

#1 – IF you are short YOU PAY the dividend

March 17, 2026

SPY Quarterly Dividend: Ex-Date (March 20, 2026)

As a courtesy reminder, please note that SPY (S&P 500 ETF) will go ex-dividend on Friday, March 20, 2026.

Please be cautious of all short SPY call options that are in-the-money or near-the-money. Also keep in mind that accounts can always be assigned prior to the option expiration date.

If an account is assigned early on any SPY options on Thursday evening (March 19th) that result in a short position of the SPY underlying for the open of Friday’s trading session (March 20th), the account will be responsible for paying the per-share dividend amount.

The dividend is estimated to be between $1.44 – $1.65 per share and is payable on April 30, 2026.

If you have any questions regarding this matter, please contact MoneyBlock Customer Service at service@moneyblock.com or 1-800-591-8243.

#2 – YOU DON’T have a profit until you take a profit !!!!

Gold drops nearly 10% in worst weekly rout since 2011

Gold drops nearly 10% in worst weekly rout since 2011

Published Fri, Mar 20 20266:38 AM EDTUpdated Fri, Mar 20 20264:44 PM EDT

- Gold dropped nearly 10% this week, its worst performance since 2011.

- While gold is on pace for its worst month since 2008, it’s still up year to date

Gold prices sank further on Friday, capping their worst week in 15 years as investors fretted about the economic implications of the U.S.-Iran War.

Futures tied to the yellow metal dropped 0.7% to $4,574.90 an ounce, pulling back from gains earlier in the morning. The metal plunged 9.6% this week, its biggest weekly loss since since September of 2011.

Gold is on track for its worst month since October 2008. But the metal is still up more than 5% in 2026, underscoring its big run before the Persian Gulf conflict.

Silver futures tumbled more than 2% to $69.66, its lowest closing level since December. The metal recorded its third straight losing week with a decline of more than 14%.

Silver is now down more than 1% for 2026.

Friday’s declines extended a tough session for precious metals Thursday, with spot prices dropping around 3% after suffering deeper losses earlier in the day amid rising fears about the economic fallout from the Iran war.

Volatility in the oil market has been influencing global investor sentiment since the beginning of the U.S.-Israel war with Iran. Oil prices topped $112 in Friday’s session.

U.S. stocks tumbled Friday’s, dragging the Dow Jones Industrial Average and Nasdaq Composite near a decline of 10% from their recent highs, which Wall Street defines as a correction. President Trump said Friday that he didn’t want a ceasefire in the war with Iran.

Arthur Parish, a metals and mining equity analyst at SP Angel, told CNBC’s “Squawk Box Europe” on Friday that some of the extreme volatility in gold in recent weeks came after an extended rally in the build up to the U.S.-Israel strikes on Iran on Feb. 28.

“That’s pretty much unwound completely and actually moved quite a lot lower,” he said. “A lot of that is momentum trades coming unwound.”

Gold and silver both enjoyed record-setting rallies in 2025, when they surged 66% and 135%, respectively. They have continued to be volatile in 2026, with silver futures suffering their biggest one-day rout since the 1980s at the end of January.

During the 2025 bull run on gold, Parish noted that there had been “a lot of generalists coming to the space, a lot of systematic hedge funds and a lot of retail as well.”

“That money is not wedded to long term gold positioning,” he said. “Ever since the Ukraine-Russia war and the freezing of Russian assets, you’ve seen central banks accumulate gold. I think they drove the first leg higher in this multi-year gold bull run, and then the tourists and retail investors came in to take advantage of that momentum. They’re leaving the space now, which is probably what’s needed for gold to then take another leg higher.”

Toni Meadows, head of investment at BRI Wealth Management, told CNBC that gold and silver prices are dependent on daily demand as well as “a fear mark-up.”

“I wouldn’t view [the gold price] as a daily hedge to every move in risk assets,” he said. “It is driven by longer-term trends rather than short-term fear trading.”

#3 – YES, The market also almost broke me BUT I FOLLOW A METHODLOOGY

6 out 7 weeks the market has been down, and 4 consecutive down weeks

ADD PUTS, We can add Index puts, We can get frustrated like there is no tomorrow and then I prefer to use highly technical four letter words like I do on the golf course !!!

What the heck is going on?

Trump TACO trade

Are we speaking the dictator’s son or not? WHO’s telling the lie?

I think it’s a game and Trump bought us one week to hunt down the son and “bomb the shit out of them!”

We don’t get oil out of the straight, I think it would be funny to leave the region and have the countries who receive this oil go about protecting the straight

Earnings

https://www.briefing.com/the-big-picture

The Big Picture

Last Updated: 20-Mar-26 12:06 ET | Archive

A salt and pepper view of the interest rate outlook

Briefing.com Summary:

*There is a disconnect between the Fed’s projections and market pricing.

*Rate cuts have been pushed out, and the risk of a rate hike is rising, driven by persistent inflation and the energy price shock.

*Rising global yields and weaker Treasury demand tighten financial conditions, threatening growth, valuations, and fiscal stability.

“Take the SEP forecasts now with a grain of salt. They are subject to a very high level of uncertainty.”

That is what Fed Chair Powell said during his press conference following the March FOMC meeting. It was a nod to the uncertainty surrounding the war with Iran. It is fair to take the forecasts with a grain of salt, but if we are going to do that, then we feel compelled to add in a dash of cayenne pepper.

The median estimate for PCE inflation this year was raised to 2.7% from 2.4%, the median estimate for core PCE inflation was raised to 2.7% from 2.5%, and the median estimate for the change in real GDP was bumped up to 2.4% from 2.3%. Remarkably—or maybe we should say inexplicably—there was no change in the median estimate for one rate cut this year.

That makes no sense. The fed funds futures market and Treasury market know it, and the stock market is begrudgingly accepting it.

Shifting Expectations

In early December, the fed funds futures market was expecting two rate cuts in 2026: one in April and another in September. That expectation is no longer with us.

According to the CME FedWatch Tool, the Fed isn’t expected to cut rates at all this year. The real kicker is that the expectation for another 25-basis-point cut has been pushed out to October 2027!

Things started to slip with the recognition that inflation was remaining stubbornly above the Fed’s 2.0% target, but the real push came from the spike in energy prices that coincided with the attack on Iran, its subsequent weaponization of the Strait of Hormuz, and its retaliatory strikes on other Middle East countries.

It became apparent to market participants that the hoped-for rate cut is going to be later rather than sooner, assuming there isn’t a rate hike first. It’s worth noting that the CME FedWatch Tool shows at least a 40% probability of a 25-basis-point hike at the October 2026 FOMC meeting.

Foreign Exchange

The energy price shock isn’t a unique management problem for the Fed. Every central bank needs to grapple with it, and sovereign bond markets are recognizing that. Bond yields have risen appreciably here and elsewhere, as participants are pricing out rate cuts, and in some cases, like the BOJ, Bank of England, Reserve Bank of Australia, and ECB, pricing in rate hikes.

The 2-yr note yield, for instance, has spiked 52 basis points this month to 3.91%, with rate cut expectations getting swept away. The 10-yr note yield is up 42 basis points to 4.38%, with inflation concerns escalating. This is known as a bear flattener trade in the Treasury market, where short-term rates rise faster than long-term rates, and it isn’t the stock market’s friend.

These higher yields will be an impediment, certainly for the housing market and equity valuations, and they will simply worsen an already bad fiscal situation for the U.S., as the interest expense that comes with financing and refinancing our massive debt is rising.

The added problem is that, as yields rise elsewhere, U.S. Treasuries become relatively less attractive to foreign buyers, who can take advantage of higher yields again in their domestic markets while avoiding currency risk.

The 10-yr U.K. Gilt yield hit 5.00% for the first time since 2008, while Australia’s 10-yr note yield topped 5.00% for the first time since mid-2011. Therefore, it might take even higher yields here to entice foreign buyers to step up their purchases of U.S. Treasuries.

The Iran war, then, which unleashed oil prices, may just end up haphazardly unleashing bond vigilantes if current trends persist. That is a battle the U.S. government doesn’t want to be fighting.

Briefing.com Analyst Insight

Ultimately, the issue isn’t just uncertainty—it’s inconsistency. The Fed’s updated projections acknowledge firmer inflation and resilient growth, yet its rate outlook hasn’t adjusted accordingly, creating a disconnect that markets are rapidly correcting on their own.

With energy prices injecting fresh inflation pressure and global yields moving higher, financial conditions are tightening whether the Fed intends them to or not. That leaves policymakers in a reactive position, while investors are forced to recalibrate for a higher-for-longer reality.

In that sense, investors are taking the SEP with a grain of salt, but they are rightfully concerned about the cayenne pepper that is rising inflation and rising bond yields.

—Patrick J. O’Hare, Briefing.com

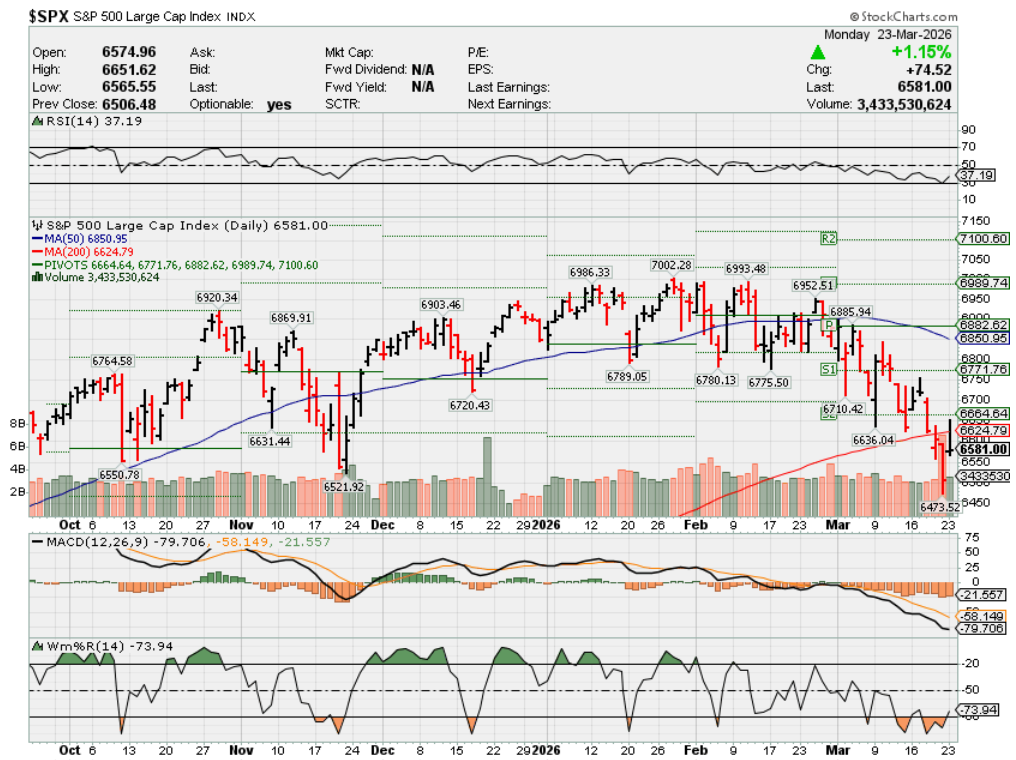

Where will our markets end this week?

HIGHER

DJIA – Bearish

SPX – Bearish

COMP – Bearish

Where Will the SPX end March 2026?

03-23.2026 -4.0%

03-09-2026 -2.0%

03-02-2026 -2.0%

Earnings:

Mon:

Tues: GME, KBH

Wed: FUL

Thur:

Fri:

Econ Reports:

Mon: Construction Spending

Tue Productivity, Unit Labor Costs

Wed: MBA, Current Account Balance

Thur: Initial Claims, Continuing Claims,

Fri: Michigan Sentiment

How am I looking to trade?

Protection and still holding onto cash we raised end of last year/beginning of this year

Looking to protect Friday for when nothing gets resolved or we bomb him!!!

www.myhurleyinvestment.com = Blogsite

info@hurleyinvestments.com = Email

Questions???

https://www.cnbc.com/2026/03/03/blackstone-private-credit-fund.html

Blackstone’s Gray: Market ‘noise’ fueled record redemptions from world’s largest private credit fund

Published Tue, Mar 3 202611:29 AM ESTUpdated Tue, Mar 3 20261:55 PM EST

Key Points

- Blackstone president Jon Gray defended the quality of loans within the firm’s flagship private credit fund after investors as concerns in the sector are growing.

Blackstone president Jon Gray on Tuesday defended the quality of loans within the firm’s flagship private credit fund after investors pulled nearly 8% from it in the last quarter.

The alternative asset management giant said in a late Monday filing that it allowed investors to withdraw 7.9% of BCRED, which it calls the largest private credit fund in the world, with about $82 billion invested. Blackstone did so in part by allowing the firm’s own investors to plow $150 million into the fund.

The move sparked a sell-off in Blackstone shares, which fell as much as about 8.5% in morning trading Tuesday, as well as in other private credit peers.

“When you think about credit quality, the 400-plus borrowers here, they had 10% EBITDA growth last year,” Gray told CNBC’s David Faber, using a term referring to a company’s financial performance. “So when we look at this, we feel pretty darn good.”

Instead of calming markets, recent moves by alternative asset managers to allow investors to cash out of funds have only added to jitters around private credit and loans to the software industry. Last month, the storm intensified when Blue Owl said it found buyers for $1.4 billion of its loans, in part to help cash out 30% of an embattled credit fund.

Blackstone President Jon Gray on private credit fund redemptions

Now, with the far larger asset manager Blackstone being swept up in it, concerns around private credit seem to be broadening.

A Blackstone spokesman said the firm and its employees’ investment in BCRED was “about meeting 100% of requests for the quarter with certainty and timeliness.”

The fund delivered 9.8% annualized returns since inception for Class I shares, the spokesman said.

“We’ve had a ton of noise,” Gray told CNBC. “As you guys know better than anybody in the press, this has become a story.”

‘Spin cycle’

Concerns were first triggered last fall with the collapse of Tricolor and First Brands, firms that also received funding from banks, the Blackstone executive noted.

“There’s a constant spin cycle, and so when that’s happening, it’s not a surprise that investors can get nervous,” Gray said. “Financial advisors can say, ‘Hey, I want to redeem.’”

Still, loans to software firms make up the single biggest exposure for BCRED, at roughly 25% of the fund, per disclosures.

While Gray acknowledged that “there are software companies that will be disrupted” by AI in the coming years, he also noted that debt lenders are senior to equity holders and that many software companies will be difficult to dislodge.

“There’s this disjointed environment now between what’s happening on the ground with underlying portfolios and what’s happening in the news cycle,” Gray said. “Ultimately, these things will resolve themselves.”

The economy has a Strait of Hormuz deadline for Trump: Two weeks

Published Sun, Mar 22 202611:48 AM EDT

Updated Sun, Mar 22 20262:44 PM EDT

Key Points

- Corporate executives on a recent CNBC CFO Council call expressed concern about the risk of a sustained rise in oil prices if the Strait of Hormuz closure is not soon resolved.

- President Trump issued a deadline for Iran to reopen the strait over the weekend, and the military has intensified attacks related to the closure, but the C-suite has set its own deadline for a reopening: about two weeks.

- Oil and energy market expert John Kilduff of Again Capital told CFOs on the call that traders see the situation in much the same way: a roughly two-week deadline for a resolution before oil prices spike even more sharply and the global economy has to start preparing for energy shortages in Asia and the reining in of industrial activity.

In this article

With oil prices at levels not seen in years and global business supply chains across sectors of the economy shut down by the de facto closure of the Strait of Hormuz, faith in the C-suite that the worst isn’t yet to come is being tested. On Friday, United Airlines CEO Scott Kirby said he is planning for $175 oil, and for an oil price that remains above $100 through 2027. This forecast, he said, may not come to pass, but the airline CEO added that there is every reason to at least start planning for it as a potential reality.

Corporate executives have become accustomed in recent years to a world in which it is one new form of uncertainty after another. But the potential ramifications of the U.S.-Iran war, for which President Donald Trump has continued to offer uncertain timelines for ending, has the market and many inside the C-suite on edge. The Nasdaq entered a correction on Friday, a fourth consecutive negative week for the stock market, and it is not just risk-on assets but safe havens such as gold and bonds that are falling.

The administration and military are responding. By Thursday, the Chairman of the Joint Chiefs of Staff said the military was “hunting and killing” watercraft used by Iran to choke traffic in the strait. President Trump’s threats about the Strait of Hormuz have intensified, with Trump saying on Saturday that Iran had 48 hours to reopen the Strait or the U.S. would take out power plants in the country. Meanwhile, more allies of the U.S. have indicated a willingness to support efforts to secure safe passage for ships, though no specific plan has been implemented. Trump also said on Friday that the Strait of Hormuz “will have to be guarded and policed, as necessary, by other Nations who use it — The United States does not!”

Iran said on Sunday that the strait would be “completely closed” if its power infrastructure was targeted.

For now, the C-suite has its own view of the matter: it’s roughly two weeks and counting for the Trump administration and any allies that join the effort to reopen the Strait of Hormuz, or corporate executives have to assume that the conflict will drag on until at least mid-year, with all of the negative consequences that come with that for the global economy. That was the conclusion on a call among members of the CNBC CFO Council earlier this week with energy and commodities market expert John Kilduff of Again Capital, who joined CFOs to share his view of the oil price outlook from inside the trader and investor community.

Among sectors, it is energy that can be said to be truly in the war, and an energy CFO on the Tuesday morning call — CFOs are granted anonymity on the call to speak freely about the discussions inside their firms — said their company is scenario planning for the future with three distinct potentials: a reopening of the Strait of Hormuz by the end of March, one that is closer to the middle of the year, or in the worst-case scenario, a closure that extends through the end of the year. But the energy CFO conceded that it is difficult at this point to have a good sense as to which scenario is more likely, and that leaves the executive team with no choice but to be “worried about what’s the worst thing that can happen here.”

Those concerns about the ticking clock were echoed by CFOs on the call from outside the energy sector. A tech sector CFO on the call said that not having to worry about the price of oil does not mean his company doesn’t worry about the indirect impact, and for a global business, that means pressure around the world, including the Middle East specifically, and booming economies like Saudi Arabia and Dubai and the rest of the UAE. Even though the tech sector CFO noted his business is enterprise-sales focused, “consumer demand ultimately impacts business demand, which would directly impact our business.”

“How long can this go on?” he asked.

Iran war, oil headed into ‘critical stage,’ says Again Capital’s Kilduff

Kilduff said the scenario planning inside the energy company boardroom matches what traders in the market are working with, too. “The [end of] March reopening that you talk about; that’s about two weeks from now; that’s what I’ve been talking about,” he told the energy CFO. “This is a huge window that we’re living in right now, partly because the military folks are now telling us they’re turning their attention to the Strait,” Kilduff said. “Where that goes, we don’t know, but certainly after April 1, if we’re looking at this as something that’s going to drag on into mid-year, that’s when you get the next phase of the repricing, in my opinion, where we get well above $100 for WTI, where we start to be concerned about shortages, particularly out in Asia,” he said.

Measures to shore up, conserve oil supply can’t do enough

Strategic petroleum reserve announcements from Japan to the U.S., and the ability of the U.S. to release over a million barrels a day — which just a few years ago may have been doubted — will help quell the supply fears that occurred as recently as in the aftermath of the Russian-Ukraine war. But Kilduff said “the numbers are just too big” for that solution to be effective for long. “This is a 10 to 12 million barrel per day deficit. … really just insurmountable. There’s no policy measure that can be taken. There’s no lever that can be pulled to offset this,” he said.

That is why he thinks the timeframe to be focused on is that post-April 1 date. “If there’s no resolution, if there’s no plan, if there’s no sort of even hopefulness that we can get the Strait reopened, with amassing troops or doing whatever the military has to do to do that,” that is when this becomes an energy crisis, Kilduff said. “By mid-year, you will see shortages in places like India, Japan, and South Korea. They will start to rein in industrial production. They’re going to have to conserve to keep the lights on, literally,” he said. If the military and government do not have good answers by April 1, “The crunch is coming.”

If there’s good news, Kilduff said, it’s that there is less reason to be worried about the U.S. right now.

While there is already scrambling in the diesel market, and diesel prices have reacted even more violently as compared to crude and even gasoline to the upside, the market is still relatively well supplied for the short-term. But by the end of the year, even in the U.S., “We’re going to have a major energy crisis on our hands. … I think the shortages would certainly have come to California by then,” Kilduff said.

To date, he noted, policy measures being talked about to keep the prices down at the pump, such as no-tax holidays, are in a sense almost perverse measures because they seek to support demand. “In a situation like this, we kind of want demand destruction to allow the price to stay stable, or maybe even go back down, because of how problematic this is for the consumer,” he said.

WTI crude oil futures pricing 2026.

Oil market responses can’t do enough either, he said, with the roughly 20 million barrels a day that would flow through the Strait of Hormuz on a normal basis impossible to redirect through infrastructure such as the Saudi East-West Pipeline. Even with up to 2 million barrels total daily, and 1 million to 1.5 million barrels a day able to get to ships through the pipeline, “none of these policy measures that we have been talking about really can address this situation,” Kilduff said.

In Kilduff’s view, there’s one reason WTI has had a ceiling around $100 and Brent crude has been “fairly well behaved” in the range of $105-$110 on the upside. “That’s because this situation could resolve itself fairly quickly. … we’re just waiting here on the precipice to see if we take another leg higher. Because if this goes on much more than two weeks or so, we’re going to reprice the barrels of oil here considerably higher,” he said.

Kilduff told CFOs there is some truth to the argument that higher oil prices don’t do as much damage to the U.S. economy as crude did back in the 1970s, because of our strong production position and because of how less energy-intensive the economy has become. The U.S. position is aided by the fact that most of the oil imported comes from Canada, and the U.S. now has the newly “rediscovered” resource from Venezuela, which in contrast to U.S. shale oil, is well-suited to the operations of Gulf Coast refiners. “These prices in the global market would be much, much higher if it wasn’t for the U.S. production position. There’s no two two ways about that,” Kilduff said.

There also remains plenty of floating storage, and other oil storage, in the world. In fact, when 2026 began there was an oil glut that had begun developing, which now is still being worked off, and that may sync up in a positive way with the military approach in terms of not prioritizing the strait first. But Kilduff added, “I also think this misses the boat on what the inflation pulse will be throughout the supply chain, and also what it does to consumer confidence.”

$100 WTI oil price ‘floor’ may soon be set

Even if the Strait of Hormuz situation is resolved, there is every expectation in the market that an enhanced risk premium is here to stay in oil prices as other Mideast nations have shut in production, facilities across the Mideast are damaged, and it will take some time to restore production to previous levels. That timeline gets extended the more damage that is done to oil and gas operations. An Iranian attack that took out 17% of Qatar’s liquefied natural gas export capacity could take three to five years to be fully repaired, QatarEnergy’s CEO told Reuters on Thursday.

If the U.S. or Israel hit more Iranian oil export facilities, “I would expect them, with whatever they have left, to asymmetrically go after oil production facilities in all the surrounding countries,” Kilduff said. “The UAE is sort of the closest and easiest to hit. So that’s why they’re doing that.”

“This was one of the unknowns. What would Iran do in response? Would they go after their neighbors? Would they be like what I call ‘the drowning man syndrome,’ where you go to save somebody and they take you down with them? It looks like that for the Iranians. They are looking, in fact, to take everyone down with them,” Kilduff said. “It’s clear that the Iranians are looking to spread the pain, and they’ve turned out to be fairly good at it,” he added. “If you were to hear about a successful Iranian attack on meaningful Saudi or Kuwait or Iraq infrastructure, then this price jumps up $20 a barrel in no time. It’s ‘buy now, ask questions later’ mode for traders in the market.”

Even if the situation deescalates, “It’s going to be a very careful, slow step process,” Kilduff said. “Coming back down to the $70s or $60s becomes a harder trip because of the fundamentals and what may still be a very enhanced risk environment,” he said.

But the next two weeks come first. “We’re on the precipice of $100 being the new floor here over the next week or two. If there’s not meaningful progress in terms of securing the Strait, the benefit of the doubt will go out of this market,” Kilduff said. “The loss of supply will start to grip, will start to bite,” he added.

With the recent focus on the strait from Trump and the military, “now the test will be for the market, do we get out of this within the next two weeks? We are holding our breath,” Kilduff said. “Pick your analogy, your metaphor. Are we like the people in one of those disaster movies, looking at that big wave coming at us as before it all ends badly?”

Top Wall Street analysts are confident about the long-term prospects of these 3 stocks

Published Sun, Mar 22 20267:29 AM EDT

TipRanks.com Staff

Escalating geopolitical tensions in the Middle East and elevated oil prices continue to weigh on global stock markets.

Investors aiming to invest in stocks for the long term, despite the ongoing volatility, can consider the recommendations of top Wall Street analysts. These experts assess macroeconomic factors and sector and company-specific drivers before assigning their ratings.

Here are three stocks favored by some of Wall Street’s top pros, according to TipRanks, a platform that ranks analysts based on their past performance.

Netflix

Streaming giant Netflix (NFLX) is this week’s first stock. After recently upgrading his rating for Netflix stock, JPMorgan analyst Douglas Anmuth reiterated a buy rating with a price target of $120, calling NFLX one of his top picks along with Alphabet (GOOGL) Amazon (AMZN), Spotify (SPOT), and DoorDash (DASH).

Anmuth noted that there are concerns about the necessity, or lack thereof, of large-scale media mergers and acquisitions, Netflix’s engagement growth and valuation. Despite these concerns, the five-star analyst believes that Netflix remains a “healthy organic growth story, driven by a combination of strong content, global subscriber growth, continued pricing power, & an early-stage/under-monetized Ad tier.”

Additionally, Anmuth is confident about Netflix delivering improved margins and solid free cash flows. He expects the company to make higher share repurchases this year, driven by the stock’s favorable share price and the $2.8 billion termination fee received from Paramount Skydance (PSKY) after the streaming platform abandoned a merger deal with Warner Bros. Discovery.

The analyst expects Netflix to deliver a 2025 to 2028 compound annual growth rate of more than 12% for forex-neutral revenue, 21% for operating income, 24% for GAAP earnings per share, and 22% for free cash flow.

Amid worries over elevated AI spending by mega-caps and AI disruption, Anmuth expects Netflix to leverage the technology to enhance content discovery and personalization, improve advertising solutions and measurement, and bring down content production costs.

Anmuth ranks No. 352 among more than 12,100 analysts tracked by TipRanks. His ratings have been profitable 57% of the time, delivering an average return of 15.3%. See Netflix Ownership Structure on TipRanks.

DoorDash

Anmuth is also bullish on delivery platform DoorDash (DASH). He reiterated a buy rating on the stock with a price target of $272. The top-rated analyst is confident about DoorDash’s long-term growth and expects U.S. marketplace gross order value (GOV) to increase at a CAGR of 18% over 2025 to 2028, driven by both a rise in monthly active users (MAUs) and frequency of orders.

Anmuth also expects unit economics to improve for U.S. restaurants in 2026. He is optimistic about the U.S. grocery and retail business delivering positive unit economics and international business posting positive contribution profit in the second half of this year.

Also, the analyst expects DoorDash’s recent acquisitions to expand its total addressable market and support long-term profitable growth. Specifically, Anmuth expects DoorDash to gain market share in Deliveroo’s markets, while expanding SevenRooms products across its merchant base.

Furthermore, Anmuth sees significant monetization prospects. He noted that while the company is one of the most rapidly growing retail media networks, its ad monetization is less than 2% of GOV, compared to Uber at more than 2% and Instacart at about 3%.

Finally, Anmuth expects DoorDash’s EBITDA (earnings before interest, taxes, depreciation, and amortization) to compound at about 28% from 2025 to 2030, supporting a higher valuation for the stock. “Overall, we are positive on DASH’s value proposition and execution and see it as the leader in global local commerce,” concluded the analyst. See DoorDash Financials on TipRanks.

Oracle

Enterprise software and cloud company Oracle (ORCL) recently announced solid fiscal third-quarter results, driven by AI-led demand. Moreover, the company assured investors that it doesn’t intend to raise any further debt this year beyond what it has already announced.

Reacting to the third-quarter print, Guggenheim analyst John Difucci reiterated a buy rating on Oracle stock with a price target of $400. The analyst noted that the company delivered solid third-quarter results.

The five-star analyst emphasized the company’s overall revenue growth of 22% in the third quarter and strength across segments. He contends that Oracle’s growth story is not based on marketing or accounting manipulation or “pricing calisthenics,” but is backed by technology and economics. He attributed Oracle’s growth to its superior technology that ensures better performance at a lower price.

Difucci highlighted AI infrastructure and strength in Oracle’s traditional cloud workloads. The analyst anticipates this, along with ORCL’s leading database technology and an accelerating applications business, could ensure continued growth in the years ahead.

The analyst thinks that while the noise around Oracle stock is not in management’s control, delivering on their commitments to customers could reassure investors.

Difucci ranks No. 300 among more than 12,100 analysts tracked by TipRanks. His ratings have been profitable 60% of the time, delivering an average return of 15.7%. See Oracle Statistics on TipRanks.

‘Tax resistance’ gains attention amid ICE protests, Iran war — and IRS penalties could follow

Published Sat, Mar 21 20269:30 AM EDT

Kate Dore, CFP®, EA@in/katedore/

Key Points

- Amid the Iran war, some “tax protesters” are planning to withhold some or all of their federal income taxes owed.

- However, the IRS has said repeatedly that moral or religious beliefs don’t exempt filers from their tax responsibility.

- What’s more, failing to file returns or underpaying taxes can trigger hefty IRS penalties and other consequences, experts say.

Chicago attorney Rachel Cohen owes more than $8,000 in federal income taxes — but has intentionally left that balance unpaid.

“I’m not paying my federal income tax this year,” Cohen said in a widely viewed TikTok video from March 2 about her decision.

The 31-year-old community organizer filed her federal tax return, which shows a balance due of $8,830, according to a tax document reviewed by CNBC. But Cohen said she deliberately chose to withhold payment of that bill as a protest against immigration detention, including ICE facilities, and U.S. strikes on Iran launched without congressional approval.

While voicing resistance to taxes is legal, refusing to pay taxes owed can violate federal law and lead to serious penalties.

“It’s completely OK to be unhappy and be dissatisfied with our government,” said Josh Youngblood, owner of The Youngblood Group, a Dallas-based tax firm. “But not paying taxes, or engaging in tax fraud or evasion, is not the answer.”

In addition to penalties and interest that start accruing immediately on their past-due balances, tax protesters can face “long-term consequences,” such as wage garnishment, a tax lien on property or even jail time, according to Michele Frank, associate professor of accountancy at Miami University. Federal courts have a long track record of siding with the Internal Revenue Service in cases involving tax resistance, routinely dismissing these claims as frivolous and, in some instances, imposing additional penalties.

Cohen told CNBC she is fully aware of the potential risks and that speaking openly about the decision could attract additional scrutiny from federal authorities.

Her protest is directed at federal spending priorities, not taxation itself, Cohen said. She paid about $3,000 in Illinois state taxes, according to a tax document reviewed by CNBC, and said she sees value in how those dollars support state and local services.

Cohen said her decision is personal and not something she is encouraging others to do, but hopes it pushes people to reflect on whether their actions match their beliefs.

Renewed interest in tax resistance

Cohen’s protest follows a long tradition of so-called war tax resistance, in which people withhold some or all of their federal taxes to oppose government policies.

“It’s been going on pretty much as long as we’ve been a country,” Frank said.

Typically, there’s an uptick in tax protesting — with filers holding back some or all of their tax payments — when the U.S. government engages in a war or other “controversial” activities, she said.

That appears to be happening again, according to the National War Tax Resistance Coordinating Committee, an educational nonprofit founded in the early 1980s by activists connected to the anti-Vietnam War movement.

The group’s website had averaged about 40,000 unique visitors a year until the war in Gaza began in 2023, according to Lincoln Rice, the organization’s coordinator. In January 2026 alone, traffic surged to more than 110,000 visitors.

“I don’t think anyone’s making the decision to practice war tax resistance based on one single action,” Rice told CNBC. Instead, major political events can become the “final straw” that prompts some people to explore the tactic.

Sign Up for Our NewsletterYour Wealth

Weekly advice on managing your money

Get this delivered to your inbox, and more info about our products and services.

By signing up for newsletters, you are agreeing to our Terms of Use and Privacy Policy.

Rice said the organization does not encourage people to refuse to pay taxes but instead provides information about how the practice works and its legal risks.

Those approaches vary. Some protesters file their tax returns but refuse to pay the balance owed, while others deliberately pay less than they owe, Rice said. Some also choose not to file at all, which can expose them to steeper penalties.

Ruth Benn, a longtime war tax protester and volunteer counselor with the National War Tax Resistance Coordinating Committee, said she has followed one of the more common approaches: filing her tax returns but refusing to pay the federal income tax she owes. She currently owes about $27,000 in federal taxes, including interest and penalties accumulated over multiple years, according to a summary of her IRS account reviewed by CNBC.

Benn said over the years she has regularly received IRS letters “with interest and penalties adding up” and met with the agency in 2009 related to her tax debt.

She said she has had small state refunds seized and some government rebates withheld. “I think around 1990 they took $800 from a bank account,” she said. “Otherwise, I don’t recall more bank account seizures, and I never had money taken from a paycheck.”

Benn said she began withholding payment decades ago after becoming involved in anti-war activism, and that she sends the IRS a letter each year explaining why she is withholding payment. She said she is open with the IRS about not paying, rather than trying to hide income.

However, failing to pay federal income taxes is still illegal. Those who don’t pay could still face penalties, interest and collection actions, and in some cases, willful failure to pay taxes can be charged as a criminal offense.

Separately, certain tax positions can trigger more severe penalties. The IRS warned in a 2022 brief that taxpayers relying on “frivolous” arguments to avoid taxes — such as claiming tax returns are voluntary, or disputing what counts as income, among others — can face additional civil penalties and, in more serious cases, criminal prosecution, including felony charges tied to tax evasion or false filings. The agency cites multiple cases in which courts have ruled against tax protesters.

Benn said people considering tax resistance should understand that the consequences can be unexpected, with the IRS sometimes pursuing collection years later.

“It’s unpredictable,” she said. “That’s the hard part of this particular anti-war protest. You don’t know what’s going to happen when.”

Consequences for tax protesters

While some Americans object to funding certain government programs, moral or religious beliefs don’t exempt taxpayers from paying federal income taxes, according to the IRS.

When you don’t file a return, there’s a “failure to file” penalty, levied at 5% of your taxes due for each month or partial month the filing is late and capped at 25%. The agency also charges interest on penalties.

Eventually, the IRS can prepare a “substitute for return” on your behalf, without the credits and deductions you’re owed, said Youngblood, who is also an enrolled agent, which is a tax license to practice before the IRS.

After that, you can expect a “90-day letter” with the agency’s proposed assessment of your balance before they start collections. This could include refund offsets, garnishing wages, seizing property and other activities.

How to keep your money safe amid this economic and political uncertainty

There’s also a “failure to pay” penalty — 0.5% of your balance for each month or partial month the filing is late, capped at 25% — but other penalties can be substantially higher, Youngblood said.

For example, if you file a return without enough information to calculate the correct tax liability, you could be subject to a $5,000 civil penalty for what’s known as a “frivolous tax return,” according to the Internal Revenue Code.

Alternatively, some filers could see a 75% civil fraud penalty if the agency believes the underpayment is due to fraud rather than negligence.

There’s also no statute of limitations for a “false or fraudulent return,” according to the Internal Revenue Code. For those cases, the IRS could pursue filers indefinitely.

In some cases, failure to pay taxes could result in jail time. During fiscal year 2024, the U.S. Sentencing Commission reported original sentencing for some 360 federal criminal cases involving tax fraud, up 11% from fiscal year 2020. The 2024 cases included tax evasion and willful failure to file a return, supply information or pay tax, among other issues.

Odds of a Fed rate hike by June are now higher than the chances for a rate cut

Published Wed, Mar 18 20264:03 PM EDTUpdated Wed, Mar 18 20264:59 PM EDT

Something unusual is happening: The Federal Reserve is now more likely to raise rates by this summer than it is to cut them.

The Atlanta Fed’s Market Probability Tracker now shows the odds of a rate hike stand at 19.2%, while the chances of a rate cut sit at 17.3%. This is a sharp reversal from where these probabilities stood in late February — before the U.S.-Iran war began.

In Feb. 27, the likelihood of an interest rate cut stood at 39.7%, while odds of a rate hike were in the single digits, the tracker showed.

“A month ago, no one would have believed this,” Ryan Detrick, chief market strategist at Carson Group, wrote in an X post on Tuesday.

Detrick told CNBC on Wednesday that “the war and the spike in commodities across the board has pushed the rate hike percentages higher. At the same time, we’ve been seeing inflation concerns even before the war started.”

Oil prices have spiked higher since the war began, raising concern among some economists about stagflation. This takes place when an economy is marked by high inflation and weak growth. Data released Wednesday added to those fears.

The producer price index, which measures a broad basket of wholesale prices, rose in February by 0.7%. PPI also rose 3.4% on an annual basis. Inflationary pressures compounded with a weak job market and rising oil prices could push the Fed to hike interest rates.

The Fed last raised interest rates in its July 2023 meeting, with the hopes of slowing inflation down in the aftermath of Covid.

The FOMC cut interest rates three times by 25 basis points each in 2025, and the year ended with interest rates in the range of 3.5%-3.75%. The Fed opted to keep rates steady in January as well as on Wednesday, with some comments raising worries about inflation.

“In the near term, higher energy prices will push up overall inflation, but it is too soon to know the scope and duration of the potential effects on the economy,” Chair Jerome Powell said in a news briefing Wednesday.

“We are balancing these two goals in a situation where the risks to the labor market are to the downside, which would call for lower rates, and the risks to inflation are to the upside, should call for higher rates or not cutting anyway,” Powell added. “So we’re in a difficult situation, and we feel like our framework calls on us to balance the risks, and we feel like where we are now is just kind of on that borderline, the higher borderline of restrictive versus non-restrictive.”

Gold in trouble?

A Fed hike, while often opportune for stocks, could pose risks to commodities.

Wall Street expected the U.S.-Iran war to drive gold prices up, inflation and Fed rate hikes as a result of the conflict would offset any gains, said Goldman Sachs analyst Amy Gower.

″[I]f the Fed is not able to look through rising oil prices and we see a pause in cuts or even hikes, the set-up for gold may look more challenging.” Gower noted.

Still, Gower and Detrick are still bullish on gold and expect prices to push comfortably past $5,000 in the second half of 2026. As for sectors to watch, Detrick said technology, industrials, materials and “parts of energy” will perform better on the economic acceleration triggered by rate hikes.

Amazon convenes ‘deep dive’ internal meeting to address outages

Published Tue, Mar 10 202611:28 AM EDT

Updated Tue, Mar 10 20266:56 PM EDT

Key Points

- Amazon’s top retail technology convened a “deep dive” meeting on Tuesday to discuss a string of recent site outages, including one tied to AI-assisted coding errors

- An internal document viewed by CNBC originally said generative AI-assisted production changes were partly to blame for the issues, but the reference to GenAI was subsequently deleted.

- Amazon’s website and app suffered technical glitches last week, which the company said were triggered by a “software code deployment.”

Amazon convened an internal meeting on Tuesday to address a string of recent outages, including one tied to AI-assisted coding errors, CNBC has confirmed.

Dave Treadwell, a top executive overseeing the technical foundations of Amazon’s website, told employees that the company’s “This Week in Stores Tech,” or TWiST, meeting would be a “deep dive” on “some of the issues that got us here.” The meeting was scheduled to begin at 12:30 p.m. ET.

“Folks – as you likely know, the availability of the site and related infrastructure has not been good recently,” Treadwell, senior vice president of eCommerce Foundation, wrote in a note to employees viewed by CNBC. He added that he was shifting the focus of the meeting “given the incidence of Sev 1s,” referring to high-severity incidents that cause outages or degraded performance of critical systems.

Amazon experienced four such incidents in a week, Treadwell said and noted the deep dive is necessary to “regain our strong availability posture.”

The Financial Times was first to report on the memos. An Amazon spokesperson said TWiST is a regular weekly meeting where retail tech leaders review the performance of store operations.

“As part of normal business, the meeting will include a review of the availability of our website and app as we focus on continual improvement,” the spokesperson said in a statement.

Earlier on Tuesday, an internal document indicated that “GenAI-assisted changes” involving “GenAI tools” were a factor in a “trend of incidents” since the third quarter. However, the bullet point referencing GenAI was deleted before the meeting, according to an updated version of the document viewed by CNBC and a person familiar with the matter who asked not to be named because of confidentiality.

After initial publication of this story, an Amazon spokesperson said a single incident was related to AI and none of the incidents involved AI-written code.

The meeting comes after Amazon’s online store malfunctioned for some users last week. For roughly six hours on Thursday, website and app users were unable to check out, access account information or view product prices. Amazon said in a statement that the issues were related to a “software code deployment.”

Amazon and its hyperscaler rivals are ramping up spending on infrastructure to manage soaring demand for artificial intelligence services, which require increasing amounts of computing power. In its earnings report last month, Amazon said it expects $200 billion in capital expenditures this year, more than any of its tech peers.

As it boosts AI spending, Amazon is simultaneously continuing to slash jobs. The company in January laid off about 16,000 corporate workers, after a prior round of mass job cuts in October, when roughly 14,000 roles were eliminated. Amazon also laid off more than 27,000 employees between 2022 and 2023.

Amazon layoffs hit engineers, gaming division, ad business

Treadwell acknowledged that “best practices and safeguards” around generative AI usage haven’t been fully established yet.

Amazon plans to “reinforce” various safeguards to prevent further issues, including requiring additional review of “GenAI-assisted” production changes, according to the memo.

“We are implementing temporary safety practices which will introduce controlled friction to changes in the most important parts of the Retail experience, in parallel we will invest in more durable solutions including both deterministic and agentic safeguards,” Treadwell wrote.

Amazon Web Services has also been hit with several outages in recent months, though the company said Tuesday that the cloud group is not involved in the incidents referenced by Treadwell.

AWS was hit in December in an incident that took down a cost management feature for an extended period of time, according to several reports. The FT reported the issue occurred after engineers allowed its Kiro AI coding tool to make changes.

Amazon said in a statement at the time that the outage was the result of “user error” and not AI.

Update: This story has been updated to reflect changes Amazon made in an internal document after initial news reports were published.

Even a $1 trillion forecast can’t break Nvidia out of a 2026 funk. A theory on what’s wrong with stock

Published Tue, Mar 17 202612:21 PM EDT

Updated Tue, Mar 17 20261:47 PM EDT

Even Nvidia’s trillion-dollar growth narrative isn’t enough to jolt its stock out of a six-month rut, one sign that the chipmaker’s biggest challenge may now be its own size.

Despite dominating the artificial intelligence boom and touting long-term revenue potential that could exceed $1 trillion, Nvidia’s stock has lagged peers and failed to respond meaningfully to bullish updates. The stock is down about 2% in 2026, a little bit more than the S&P 500 decline.

The muted reaction underscores a theory on Wall Street that Nvidia may have crossed a threshold where traditional equity dynamics no longer apply.

“The market cap has gotten so large that Nvidia no longer trades like other stocks,” TD Cowen analysts wrote in a note Monday. “The reality is there are trading and fund-flow dynamics at play with a >$4T company that we, and investors, are not used to. We think this is driving a few factors that are capping the stock for now.”

Nvidia’s market capitalization early Tuesday came to some $4.45 trillion, according to FactSet data, more than any other U.S. company, even Apple or Microsoft.

Nvidia year to date

Nvidia is no longer trading like a typical semiconductor company, and its size alone is introducing new constraints — from fund flows to portfolio construction — that are capping the stock’s potential upside, even as the business fundamentals remain strong, TD Cowen said.

To double from current levels, Nvidia would need to approach a $9 trillion valuation — equivalent to the combined economic output of Germany and India, TD Cowen noted. That kind of upside is increasingly difficult to achieve, particularly for growth-oriented investors seeking asymmetric returns.

Among the factors capping Nvidia, “the simplest one we’ve observed is it’s a lot harder to add the next $2T in market cap than the last $2T. Many investors, at least the ones that talk to semis analysts, want to pick stocks that they can at least create scenarios of them doubling,” the investment bank said.

As a result, some portfolio managers are looking elsewhere in the AI ecosystem, particularly among suppliers and infrastructure plays tied to Nvidia, where the potential for outsized gains appears greater, TD Cowen said.

“To put it bluntly, the generalist community needs more convincing on the durability of Nvidia’s position, and more importantly AI spending, than do semis and tech investors,” the analysts said.

Goldman sees risks of market correction rising — and bonds won’t help weather it

Published Thu, Mar 19 20264:07 PM EDT

Goldman Sachs is warning investors to brace for a possible stock correction that won’t necessarily be buffered by bonds.

While the markets started the year risk on, concerns about the spike in oil prices, Iran war and artificial-intelligence disruption have dragged equities down. The Dow Jones Industrial Average, S&P 500 and Nasdaq Composite are all in the red so far in 2026.

That sell-off could deepen, Christian Mueller-Glissmann, head of Goldman’s asset allocation research, said in a note Thursday.

“While geopolitical shocks and their market impact are difficult to time, we think equities have not priced in enough risk premium for the risk of a more lasting shock — based on the disruptions so far our economists have already reflected a worsening,” he wrote.

In addition, the buffer from bonds, which traditionally have served as a ballast in portfolios, will be limited, he said.

Therefore, “the risk of a larger 60/40 portfolio drawdown … has increased,” Mueller-Glissmann cautioned.

Shifting portfolios

Goldman has shifted more defensively in its asset allocation for the next three months and is overweight cash, underweight on credit and neutral on equities, bonds and commodities. For allocations over the next six months, it bumps up its risk to overweight equities and moves cash to neutral.

The firm’s long-term world portfolio proxy, which spans global equities and bonds, as well as gold, has lost about 4% since the start of the Iran war — a “small drawdown in a long-run context,” Mueller-Glissmann said.

However, while the risk of a sustained, large 60/40 loss is still limited, investors should consider mitigating continued stagflationary risks by beefing up their multi-asset portfolios, he said.

″[W]e believe investors can look at a combination of up-in-quality trades in equity/credit/FX, allocations to alternatives, dynamic risk allocation, and option overlays in equities and across assets,” Mueller-Glissmann said.

Since the start of the year, exposure to defensive, quality equities, allocations to commodity trading advisors (CTAs), gold and Treasury inflation-protected securities, as well as an options strategy of put spreads on the S&P 500 would have helped performances versus a 60/40 portfolio on a risk-neutral basis, he noted.

“We continue to like those strategies to manage 60/40 drawdown risk into Q2,” he said.

At 25, she owned 5 rental properties, but says investing in real estate was her No. 1 money mistake: ‘I was really naive’

Published Wed, Mar 18 20269:00 AM EDT

Valentina Duarte@in/valentina-duarte-38a241178@TheValDuarte

44-year-old brings in $251,000 a year with 3 jobs in the Bay Area

When Naseema McElroy was 25, she owned five rental properties. It was how she thought she was going to build her wealth.

By taking advantage of subprime lending practices that allowed borrowers with weak credit histories to easily obtain high-interest mortgages in the early 2000s, McElroy figured she would borrow as much as she could to purchase multiple properties and it would all work out in the end, she tells CNBC Make It.

Then about a year later, in 2008, the housing market crashed.

“I was really naive,” McElroy says. Suddenly, she owed lenders more than what her properties were worth. To avoid foreclosure, she says she was forced to sell two of the investments for less than what was left on their mortgages. Two other properties were foreclosed on, and eventually she says she had to declare bankruptcy.

Since then, the now 44-year-old labor and delivery nurse has grown her net worth to over $1 million, according to documents reviewed by CNBC Make It. She owns her primary home, but the majority of her wealth comes from investing in the stock market through broad-based index funds, documents show.

The biggest lesson she says she’s learned from the experience: “Real estate is one form of investing, but it’s not the only form.”

Don’t underestimate the amount of work it will take

While there can be upsides to investing in real estate, it’s significantly riskier than investing in the stock market and can require a lot more work than many investors anticipate, says Alex Caswell, a certified financial planner and founder of Wealth Script Advisors in San Francisco, California.

On social media, “there’s been a popularization of the idea that real estate is somehow a silver bullet in terms of building wealth,” Caswell says. However, in reality, becoming a successful real estate investor requires extensive research and dedication, he says.

Before purchasing a property, Caswell says investors should consider a swath of variables, including how much it could appreciate, property taxes, maintenance costs, insurance expenses and the best way to finance the purchase.

All of these variables rely on assumptions, and adding all of your assumptions together can create “a lot more of an unpredictable investment experience,” Caswell says.

Being a landlord can be challenging

Additionally, becoming a landlord like McElroy may not be as easy as collecting a monthly check, Caswell says.

“I just remember how hard it was to be a landlord,” says McElroy, who was also working full time as a health-care administrator at the time.

On top of constant costs associated with maintaining her homes, she says collecting rent and dealing with tenants became a constant struggle.

McElroy says she never generated as much revenue from the venture as she expected, and looking back, McElroy says her failure to understand the true costs associated with real estate before taking on so much debt became the biggest money-related mistake she has ever made.

Save for retirement first

If you’re not looking to commit to becoming a full-time real estate investor, Caswell says you’re probably better off prioritizing financial security by investing in the stock market through retirement and traditional brokerage accounts.

If you want to “dabble” in purchasing property, only do so once you’ve saved enough to retire comfortably, he says.

“The risk and the level of dedication to succeed in a real estate venture is going to be so great that if you fail at it, it could really set you back financially,” Caswell says.

Want to lead with confidence and bring out the best in your team? Take CNBC’s new online course, How To Be A Standout Leader. Expert instructors share practical strategies to help you build trust, communicate clearly and motivate other people to do their best work. Sign up now and use coupon code EARLYBIRD for an introductory discount of 25% off the regular course price of $127 (plus tax). Offer valid March 16 through March 30, 2026. Terms apply.

The Real Reason That Vanguard Settled

Stephen Soukup | Allen Mendenhall | March 20, 2026

Stephen R. Soukup is a Visiting Fellow in the Free Enterprise Initiative at the Heritage Foundation.

Allen Mendenhall@allenmendenhall

Allen Mendenhall is a Research Fellow in the Thomas A. Roe Institute for Economic Policy Studies and Senior Advisor for the Free Enterprise Initiative at The Heritage Foundation.

When Vanguard Group announced that it would settle its portion of a lawsuit brought by 13 state attorneys general, opponents of “Environmental, Social, and Governance” (ESG) declared victory. And they weren’t wrong.

The suit, led by Texas AG Ken Paxton, accused Vanguard, BlackRock, and State Street of conspiring to push green-energy initiatives through their coal-company holdings, allegedly raising electricity prices for consumers.

“A huge win in the fight to stop … ESG,” “incredible news”—the celebrations came quickly.

The Daily Signal depends on the support of readers like you. Donate now

The damage done to the ESG cause is significant, and the celebration is justified. But it may also be premature—and for reasons that have nothing to do with ESG. The more important question is one that almost nobody is asking: Why, exactly, did Vanguard settle?

The firm says it settled “solely for the purpose of avoiding the burden and expense of litigation”—standard lawyer-speak for “we want you to leave us alone, but we can’t admit wrongdoing.” While it’s almost certainly the case that Vanguard wanted to avoid extended legal action and the associated expenses, the idea that the settlement was reached “solely” for that purpose strains credulity.

After all, the firm agreed not only to pay almost $30 million in fines but also to turn over communications related to its ESG activities—a massive, potentially embarrassing and costly concession. The true “costs” of letting this case reach trial, in other words, must have far exceeded the mere “burden and expense of litigation.”

Vanguard is not the same as the other two members of the Big Three and is profoundly different from BlackRock in particular. BlackRock may be the biggest asset manager in the world, with more than $14 trillion in assets under management, but Vanguard is, by far, the biggest manager of passive assets. Of its total of $12 trillion in AUM, almost all is passively managed. By comparison, only 35%-40% ($5-$6 trillion) of BlackRock’s assets are passively managed.

While State Street is far more passive-focused than BlackRock, it is much smaller than Vanguard and is not entirely passive.

Vanguard is, put bluntly, the undisputed king of passive investing, controlling roughly half of the entire passive investment market that has been growing at a staggering clip. According to Morningstar, passive funds saw nearly 250% growth in AUM between 2014 and 2023, compared to 36% growth for active funds. In the United States, passive AUM surpassed active AUM last year, and growth continues apace.

Passive investing isn’t just Vanguard’s business model. It is Vanguard. That’s what was at stake.

About a year ago, Denise Hearn and Cynthia Hanawalt, two climate investment researchers at Columbia University, published a paper noting that a trial in this case would provide the first legal test of the “common ownership theory,” which posits that index investing—in which managers hold multiple companies in the same sector—creates incentives to reduce or eliminate competition between the companies, resulting in a slowdown or stoppage in innovation, artificially inflated prices, reduced output, etc. Hearn and Hanawalt argued that the case against the Big Three was flawed but could, at trial, produce unexpected results that would profoundly disrupt the asset management business.

Historically, the common ownership theory has been dismissed as ideologically tinged and is refuted specifically by an appeal to “passivity.” Managers take no advantage of the competition-deadening incentives; they are mere inert observers. But that defense may be weaker than it appears, and this is where the story gets genuinely interesting.

We would argue that passivity actually has the opposite effect. Because it dulls the price-discovery mechanism, which traditionally enforces competitive behavior on corporations, passive investing creates the circumstances in which the structural incentives of common ownership—the dampening of competition in the interest of industry-wide profitability—can function without check or intent.

Active collusion between managers becomes unnecessary because the competitive dampening happens by default. As a result, passivity doesn’t refute common ownership theory; it operationalizes it.

The implications are potentially staggering. Together, the common ownership theory and the theory that passivity operationalizes competitive dampening could undermine the last quarter-century of capital market growth and consolidation—and destroy the very idea that passive investing is an appropriate process for capitalizing business at all.

No single development in this case would have guaranteed that outcome. But none could have ruled it out, either. And if you happen to run a firm with $12 trillion in assets under management—virtually all of it passive, in a market still growing at breakneck speed—is that a chance you could afford to take?

That, likely, is why Vanguard settled.