HI Market View Commentary 04-29-2024

META on Last Monday we sold around $481 and change Booking a 220% ROI or more

Why did we sell META?= Because it was fully valued, your investing methodology has to be always taking a profit somewhere in your process.

If you are going directional you have no “real adjustments” you are just reacting and trading as an event.

We NEED to talk about investing as a process vs an event :

HI currently has leap bull calls in place

![]()

What is our next step for Leap bull calls placed 2 months ago?

Make money on the short side while the stock falls down to then book that profit and let the long side run back up = Make money coming and going

Earnings Season:

AAPL 05/02 AMC

BABA 05/16

BIDU 05/16

DG 05/30

DIS 05/07 BMO

JCI 05/01 BMO

KO 04/30 BMO

MU 06/26

MRO 05/01 AMC

O 05/06 AMC

SQ 05/02 AMC

TGT 05/22 BMO

UAA 05/09

https://www.briefing.com/the-big-picture

The Big Picture

Last Updated: 26-Apr-24 15:06 ET | Archive

Inflation stuck in time

A photograph captures a very specific moment in time. Thanks to the smartphone, we all have ample capacity for “do-overs” now when that moment doesn’t capture us just right. It didn’t used to be that way. What you got on your Kodak film is what you got after that film was processed a week or two later.

You might not have been smiling in a photo that was taken, but only a few seconds later you were. Too bad. History recorded your frown, and it was pasted into a scrapbook. Of course, nowadays you can take a hundred pictures, pick the one with your perfect smile, and post it to Facebook.

We point this out, because the government doesn’t have that filtering capability with economic data. Sure, there are revisions that get posted a month — or even years — later, but never in the moment. The actuals are the actuals until the revisions are released.

The PCE price data released in the March Personal Income and Spending Report can be thought of as the equivalent of a frown in economic terms, only one can’t be sure (and that “one” is the Fed) if that frown will be quickly replaced with a smile.

Out of the Wild

The hope of course is that the economy will be smiling ear-to-ear soon with tame inflation. What is tame?

Well, the Fed has led everyone to believe that 2.0% is tame. It has also put everyone on notice that its preferred gauge for measuring inflation is the core-PCE Price Index, which excludes food and energy. That gauge isn’t as wild as it used to be, but by the Fed’s thinking, it isn’t tame yet either.

In March, the core-PCE Price Index was up 2.8% year-over-year, unchanged from February. That’s much better than core-CPI for March, which was up 3.8% year-over-year, also unchanged from February.

The differences between the two inflation reports boil down to four main reasons:1

- Different formulas for computations

- Different weights for consumption categories (e.g., shelter is assigned a much higher weight in CPI vs PCE)

- Scope of consumer items being measured

- Other reasons like using different price data for the same product

Interestingly, cost-of-living adjustments for Social Security recipients are tied to CPI; and the CPI is typically used as the main inflation gauge in wage negotiations.

When it comes to monetary policy decisions, though, the core-PCE Price Index is at the top of the Fed’s list of inflation gauges. It is not the only gauge. Fed Chair Powell has said often that the Fed looks at a wide range of inflation data, including inflation expectations, as it contemplates the right setting for monetary policy.

What It All Means

What the Fed is looking at these days is a moment in time that suggests inflation and inflation expectations are struggling to bring a smile to everyone’s face. That is particularly true on the services side of the economy, which comprises the largest swath of economic activity. Prices for services were up 4.0% year-over-year in March while prices for goods were up just 0.1%.

Both inflation and inflation expectations are sticking around at higher levels that are failing to engender confidence at the Fed that the time is right to cut rates. The fed funds futures market is thinking along the same frown lines, too.

The probability of a rate cut to 5.00-5.25% at the June FOMC meeting is just 11.6% now versus 70.2% a month ago, according to the CME FedWatch Tool. The probability of a rate cut to 5.00-5.25% at the July FOMC meeting is only 31.7% now versus 83.2% a month ago.

At the moment, it looks like the September FOMC meeting will usher in the first rate cut, but that’s no sure thing. The CME FedWatch Tool shows there is a 60.9% probability of a rate cut to 5.00-5.25% versus 95.5% a month ago.

There are many more inflation reports to be seen between now and then (and between now and June for that matter). They all present an opportunity for a “do-over” and getting the inflation frown to turn upside down.

For now, the snapshot of inflation at this moment in time shows it is stuck at a level that will keep the Fed stuck on its restrictive policy and interest rates stuck on higher ground.

—Patrick J. O’Hare, Briefing.com

Earnings dates:

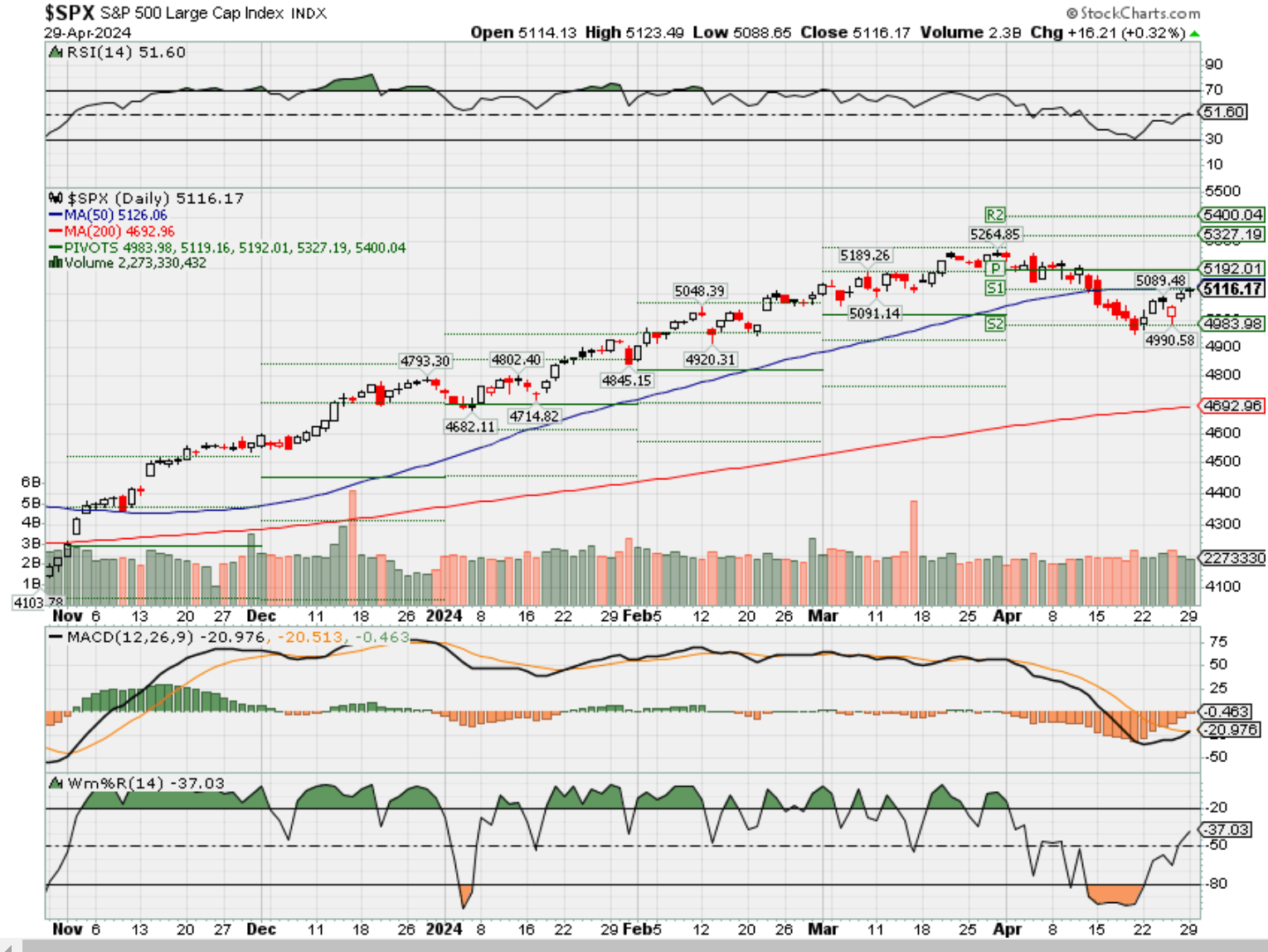

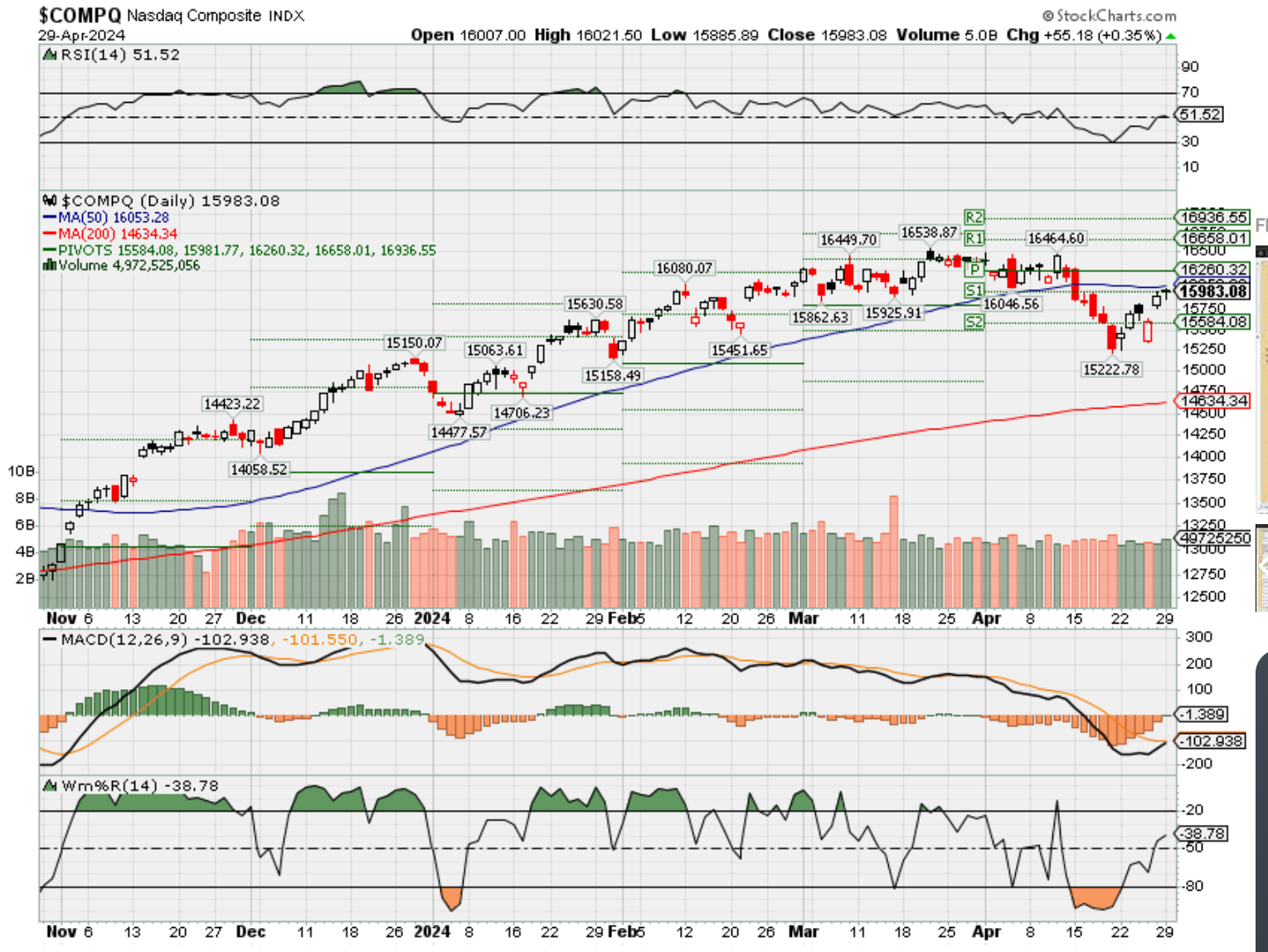

Where will our markets end this week?

Lower

DJIA – Bearish

SPX – Bearish signals and breaking the 50 day SMA usually means more sell orders are

COMP – Bearish signals and breaking the 50 day SMA usually means more sell orders are coming

Where Will the SPX end May 2024?

04-29-2024 -2.0%

Earnings:

Mon: DPZ, FLS

Tues: MMM, KO, GLW, LLY, MCD, TAP, PYPL, SIRI, AMD, CLX, DENN, SBUX

Wed: CVS, DD, EL, GRMN, JCI, KHC, MAR, YUM, BZH, EBAY, FSLR, MOS, VMI, PFE, MRO

Thur: COP, MUR, SHAK, WFN, DKNG, MNST, X, D, AAPL, SQ

Fri: LNG, FLR

Econ Reports:

Mon:

Tue Employment Cost Index, FHFA Housing Price Index, Case-Shiller Index, Consumer Credit

Wed: MBA, Construction Spending, ISM Manufacturing, ADP Employment, FOMC Rate Decision,

Thur: Initial Claims, Continuing Claims, Productivity, Trade Balance, Unit Labor Costs, Factory Orders,

Fri: Average Workweek, Non-Farm Payroll, Private Payroll, Hourly Earnings, Unemployment Rate, ISM Services

How am I looking to trade?

Mostly protected for earnings

www.myhurleyinvestment.com = Blogsite

info@hurleyinvestments.com = Email

Questions???

New positions: GOOGL Tech or VZ for Tech/dividend 6.68 % Yield , SQ for financial

Why the Fed keeping rates higher for longer may not be such a bad thing

PUBLISHED WED, APR 24 202410:42 AM EDTUPDATED WED, APR 24 20243:00 PM EDT

Jeff Cox@JEFF.COX.7528@JEFFCOXCNBCCOM

KEY POINTS

- It’s a tough case to make that higher interest rates are having a substantially negative impact on the economy.

- There are big questions over when exactly monetary policy easing will come, and what the central bank’s position to remain on hold will do to both financial markets and economic performance.

- There is little precedent for the Fed to cut rates in robust growth periods such as the present, except for the early 1980s, when the central bank stamped out runaway inflation.

- That leaves expectations for Fed policy tilting toward cutting rates somewhat but not going back to the near-zero rates that prevailed in the years after the financial crisis.

With the economy humming along and the stock market, despite some recent twists and turns, hanging in there pretty well, it’s a tough case to sell that higher interest rates are having a substantially negative impact on the economy.

So what if policymakers just decide to keep rates where they are for even longer, and go through all of 2024 without cutting?

It’s a question that, despite the current conditions, makes Wall Street shudder and Main Street queasy as well.

“When rates start climbing higher, there has to be an adjustment,” said Quincy Krosby, chief global strategist at LPL Financial. “The calculus has changed. So the question is, are we going to have issues if rates remain higher for longer?”

The higher-for-longer stance was not what investors were expecting at the beginning of 2024, but it’s what they have to deal with now as inflation has proven stickier than expected, hovering around 3% compared with the Federal Reserve’s 2% target.

Recent statements by Fed Chair Jerome Powell and other policymakers have cemented the notion that rate cuts aren’t coming in the next several months. In fact, there even has been talk about the potential for an additional hike or two ahead if inflation doesn’t ease further.

That leaves big questions over when exactly monetary policy easing will come, and what the central bank’s position to remain on hold will do to both financial markets and the broader economy.

Krosby said some of those answers will come soon as the current earnings season heats up. Corporate officers will provide key details beyond sales and profits, including the impact that interest rates are having on profit margins and consumer behavior.

“If there’s any sense that companies have to start cutting back costs and that leads to labor market trouble, this is the path of a potential problem with rates this high,” Krosby said.

But financial markets, despite a recent 5.5% sell-off for the S&P 500, have largely held up amid the higher-rate landscape. The broad market, large-cap index is still up 6.3% year to date in the face of a Fed on hold, and 23% above the late October 2023 low.

Higher rates can be a good sign

History tells differing stories about the consequences of a hawkish Fed, both for markets and the economy.

Higher rates are generally a good thing so long as they’re associated with growth. The last period when that wasn’t true was when then-Fed Chair Paul Volcker strangled inflation with aggressive hikes that ultimately and purposely tipped the economy into recession.

There is little precedent for the Fed to cut rates in robust growth periods such as the present, with gross domestic product expected to accelerate at a 2.4% annualized pace in the first quarter of 2024, which would mark the seventh consecutive quarter of growth better than 2%. Preliminary first-quarter GDP numbers are due to be reported Thursday.

For the past several decades, higher rates have not been linked to recessions.

On the contrary, Fed chairs have often been faulted for keeping rates too low for too long, leading to the dot-com bubble and subprime market implosions that triggered two of the three recessions this century. In the other one, the Fed’s benchmark funds rate was at just 1% when the Covid-induced downturn occurred.

In fact, there are arguments that too much is made of Fed policy and its broader impact on the $27.4 trillion U.S. economy.

“I don’t think that active monetary policy really moves the economy nearly as much as the Federal Reserve thinks it does,” said David Kelly, chief global strategist at J.P. Morgan Asset Management.

Kelly points out that the Fed, in the 11-year run between the financial crisis and the Covid pandemic, tried to bring inflation up to 2% using monetary policy and mostly failed. Over the past year, the pullback in the inflation rate has coincided with tighter monetary policy, but Kelly doubts the Fed had much to do with it.

Other economists have made a similar case, namely that the main issue that monetary policy influences — demand — has remained robust, while the supply issue that largely operates outside the reach of interest rates has been the principle driver behind decelerating inflation.

Where rates do matter, Kelly said, is in financial markets, which in turn can affect economic conditions.

“Rates too high or too low distort financial markets. That ultimately undermines the productive capacity of the economy in the long run and can lead to bubbles, which destabilizes the economy,” he said.

“It’s not that I think they’ve set rates at the wrong level for the economy,” he added. “I do think the rates are too high for financial markets, and they ought to try to get back to normal levels — not low levels, normal levels — and keep them there.”

Higher-for-longer the likely path

As a matter of policy, Kelly said that would translate into three quarter-percentage point rate cuts this year and next, taking the fed funds rate down to a range of 3.75%-4%. That’s about in line with the 3.9% rate at the end of 2025 that Federal Open Market Committee members penciled in last month as part of their “dot-plot” projections.

Futures market pricing implies a fed funds rate of 4.32% by December 2025, indicating a higher rate trajectory.

While Kelly is advocating for “a gradual normalization of policy,” he does think the economy and markets can withstand a permanently higher level of rates.

In fact, he expects the Fed’s current projection of a “neutral” rate at 2.6% is unrealistic, an idea that is gaining traction on Wall Street. Goldman Sachs, for instance, recently has opined that the neutral rate — neither stimulative nor restrictive — could be as high as 3.5%. Cleveland Fed President Loretta Mester also recently said it’s possible that the long-run neutral rate is higher.

That leaves expectations for Fed policy tilting toward cutting rates somewhat but not going back to the near-zero rates that prevailed in the years after the financial crisis.

In fact, over the long run, the fed funds rate going back to 1954 has averaged 4.6%, even given the extended seven-year run of near-zero rates after the 2008 crisis until 2015.

Government spending issues

One thing that has changed dramatically, though, over the decades has been the state of public finances.

The $34.6 trillion national debt has exploded since Covid hit in March 2020, rising by nearly 50%. The federal government is on track to run a $2 trillion budget deficit in fiscal 2024, with net interest payments thanks to those higher interest rates on pace to surpass $800 billion.

The deficit as a share of GDP in 2023 was 6.2%; by comparison, the European Union allows its members only 3%.

The fiscal largesse has juiced the economy enough to make the Fed’s higher rates less noticeable, a condition that could change in the days ahead if benchmark rates hold high, said Troy Ludtka, senior U.S. economist at SMBC Nikko Securities America.

“One of the reasons why we haven’t noticed this monetary tightening is simply a reflection of the fact that the U.S. government is running its most irresponsible fiscal policy in a generation,” Ludtka said. “We’re running massive deficits into a full-employment economy, and that’s really keeping things afloat.”

However, the higher rates have begun to take their toll on consumers, even if sales remain solid.

Credit card delinquency rates climbed to 3.1% at the end of 2023, the highest level in 12 years, according to Fed data. Ludtka said the higher rates are likely to result in a “retrenchment” for consumers and ultimately a “cliff effect” where the Fed ultimately will have to concede and lower rates.

“So, I don’t think they should be cutting anytime in the immediate future. But at some point that’s going to have to happen, because these interest rates are simply crushing particularly low-income-earning Americans,” he said. “That is a big portion of the population.”

Meta loses $200 billion in value as Zuckerberg focuses earnings call on all the ways company bleeds cash

PUBLISHED WED, APR 24 20247:40 PM EDTUPDATED THU, APR 25 20241:15 PM EDT

Ashley Capoot@IN/ASHLEY-CAPOOT-02496B173/

KEY POINTS

- Meta CEO Mark Zuckerberg unnerved investors on the company’s quarterly earnings call Wednesday by focusing on its long-term investments in AI and the metaverse.

- Shares of Meta tumbled as much as 19% in extended trading Wednesday.

- “We’ve historically seen a lot of volatility in our stock during this phase of our product playbook,” Zuckerberg said.

Mark Zuckerberg started Meta’s earnings call by talking about artificial intelligence. Then he moved onto the metaverse, touting his company’s headsets, glasses and operating system. He spent almost the entirety of his opening remarks focused on the many ways Meta loses money.

Investors weren’t into it. Meta shares tumbled as much as 19% in extended trading on Wednesday, wiping out more than $200 billion in market cap. The drop came despite Meta reporting better-than-expected profit and revenue for the first quarter.

Zuckerberg appeared ready for the sell-off.

“I think it’s worth calling that out, that we’ve historically seen a lot of volatility in our stock during this phase of our product playbook where we’re investing in scaling a new product but aren’t yet monetizing it,” Zuckerberg said. He cited past efforts like short-video service Reels, Stories and the transition to mobile.

Meta generates 98% of its revenue from digital advertising. But to the extent Zuckerberg talked about ads, he was looking to the future and the ways the company could potentially turn its current investments into ad dollars. In discussing Meta’s effort to build a “leading AI,” he said, “There are several ways to build a massive business here including scaling business messaging, introducing ads or paid content into AI interactions.”

He spent time talking about Meta Llama 3, the company’s newest large language model, and the recent rollout of Meta AI, the company’s answer to OpenAI’s ChatGPT.

Zuckerberg then moved onto potential opportunities for expansion within the mixed reality headset market, like a headset for work or fitness. Meta opened up access to the operating system that powers its Quest headsets on Monday, which Zuckerberg said will help the mixed reality ecosystem grow faster.

He also talked up Meta’s AR glasses, which he called “the ideal device for an AI assistant because you can let them see what you see and hear what you hear.”

In the meantime, Meta’s Reality Labs unit, which houses the company’s hardware and software for development of the nascent metaverse, continues to bleed cash. Reality Labs reported sales of $440 million for the first quarter and $3.85 billion in losses. The division’s cumulative losses since the end of 2020 have topped $45 billion.

Zuckerberg has bought himself some time.

Meta’s stock price almost tripled last year and, as of Wednesday’s close, was up 40% in 2024. It reached a record $527.34 in early April.

After a brutal 2022, during which the company lost about two-thirds of its value, Zuckerberg appears to have regained the confidence of Wall Street.

The driver for the rally has been a cost-cutting plan that the Meta CEO put in place early last year, when he told investors that 2023 would be the “year of efficiency.” The company slashed headcount and eliminated unnecessary projects in an effort to become a “stronger and more nimble organization.”

Zuckerberg said Wednesday that Meta will continue to operate efficiently, but that shifting existing resources to investments in AI will “grow our investment envelope meaningfully.”

Capital expenditures for 2024 are anticipated to be in the $35 billion to $40 billion range, an increase from a prior forecast of $30 billion to $37 billion “as we continue to accelerate our infrastructure investments to support our artificial intelligence (AI) roadmap,” Meta said.

Zuckerberg said he expects to see a “multiyear investment cycle” before Meta’s AI products will scale into profitable services, but noted that the company has a “strong track record” in that department.

Meta finance chief Susan Li echoed Zuckerberg’s remarks, saying the company needs to develop advanced models and scale products before they will drive meaningful revenue.

“While there is tremendous long-term potential, we’re just much earlier on the return curve,” Li said.

Even before the call began, investors were trimming their holdings. That’s because Meta issued a light revenue forecast for the second quarter, overshadowing the first-quarter beat.

As the stock plunge intensified, Zuckerberg told investors that if they’re willing to come along for the ride, they may well be rewarded.

“Historically, investing to build these new scaled experiences in our apps has been a very good long-term investment for us and for investors who stuck with us and the initial signs are quite positive here too,” Zuckerberg said. “But building a leading AI will also be a larger undertaking than the other experiences we’ve added to our apps and this is likely going to take several years.”

China is still years behind the U.S. despite Huawei’s breakthrough chips, Raimondo tells ’60 Minutes’

PUBLISHED MON, APR 22 20244:02 AM EDTUPDATED MON, APR 22 202410:36 AM EDT

Dylan Butts@IN/DYLAN-B-7A451A107

KEY POINTS

- Despite a chip breakthrough by China’s Huawei, the country remains years behind the U.S. in the critical technology, Commerce Secretary Gina Raimondo said.

- According to Raimondo, the Biden administration’s chip export policies are working and the U.S. will continue to protect its national security regarding semiconductors.

Commerce Secretary Gina Raimondo on Sunday downplayed Huawei Technologies’ latest microchip breakthrough, arguing that the U.S. remains far ahead of China in the critical technology.

The comments, which were delivered on CBS News’ “60 Minutes,” align with her stance that the Biden administration’s restrictions on chip sales to China are working, despite an advanced made-in-China chip surfacing in a Huawei phone last year.

“It’s years behind what we have in the United States. We have the most sophisticated semiconductors in the world. China doesn’t. We’ve out-innovated China,” Raimondo said during the interview, which aired Sunday evening in the U.S.

U.S.-blacklisted Huawei released the Mate 60 Pro smartphone in August, which sported a 5G-capable chip — a feat thought to have been made difficult by a series of U.S. export controls in late 2022. The phone launched while Raimondo was on a visit to China.

Ahead of the trip, it was reported that Chinese-linked hackers accessed Raimondo’s email.

“I have their attention, clearly,” she said, adding that the U.S. would continue to pursue actions to protect U.S. national security and businesses.

According to a senior Commerce Department official, Huawei’s chipmaking partner SMIC “potentially” violated U.S. law by providing an advanced chip to the Chinese phone maker.

Since the release of the Mate 60 Pro, the U.S. has further tightened restrictions on sales of advanced semiconductor tech to China.

Chinese officials have repeatedly denounced the policies, which require licenses for any company worldwide to sell products with advanced U.S.-designed chip technology to countries seen as adversaries.

Many U.S. chip companies, which largely rely on China for business, have also expressed concerns about losing market access.

“We want to trade with China on the vast majority of goods and services,” Raimondo said. “But on those technologies that affect our national security, no.”

The global chip race ramped up after Russia invaded Ukraine in 2022, triggering the U.S. and allies such as the Netherlands and Japan to tighten advanced tech export controls. CNBC previously reported that Russia acquired advanced Western technology through intermediary countries like China.

“It’s absolutely the case that our export controls have hurt [Russia’s] ability to conduct the war, made it harder,” Raimondo said. She added that Russia has found some alternative sources of chips.

The Commerce Department has also overseen the allocation of the Biden administration’s almost $53 billion CHIPS and Science Act, aimed at building the U.S. domestic semiconductor industry and undercutting rivals like China.

In recent weeks, billions in grants and loans have been earmarked for chipmakers Taiwan Semiconductor Manufacturing Co., Samsung Electronics and Micron Technology, which are all increasing production capacity in the U.S.

Raimondo told CNBC earlier this month that all of the grant money allocated for the CHIPS and Science Act will be sent out by year-end.

Key Fed inflation measure rose 2.8% in March from a year ago, more than expected

PUBLISHED FRI, APR 26 20248:31 AM EDTUPDATED FRI, APR 26 202412:10 PM EDT

Jeff Cox@JEFF.COX.7528@JEFFCOXCNBCCOM

KEY POINTS

- The core personal consumption expenditures price index excluding food and energy increased 2.8% from a year ago in March, unchanged from February and slightly higher than expected.

- Personal spending rose 0.8% on the month, more than the personal income increase of 0.5%.

- The personal saving rate fell to 3.2%, down 0.4 percentage points from February and 2 full percentage points from a year ago.

Inflation showed few signs of letting up in March, with a key barometer the Federal Reserve watches closely showing that price pressures remain elevated.

The personal consumption expenditures price index excluding food and energy increased 2.8% from a year ago in March, the same as in February, the Commerce Department reported Friday. That was above the 2.7% estimate from the Dow Jones consensus.

Including food and energy, the all-items PCE price gauge increased 2.7%, compared with the 2.6% estimate.

On a monthly basis, both measures increased 0.3%, as expected and equaling the increase from February.

Markets showed little reaction to the data, with Wall Street poised to open higher. Treasury yields fell, with the benchmark 10-year note at 4.67%, down about 0.4 percentage points on the session. Futures traders grew slightly more optimistic about two potential rate cuts this year, raising the probability to 44%, according to the CME Group’s FedWatch gauge.

“Inflation reports released this morning were not as a hot as feared, but investors should not get overly anchored to the idea that inflation has been completely cured and the Fed will be cutting interest rates in the near-term,” said George Mateyo, chief investment officer at Key Wealth. “The prospects of rate cuts remain, but they are not assured, and the Fed will likely need weakness in the labor market before they have the confidence to cut.”

Consumers showed that they are still spending despite the elevated price levels. Personal spending rose 0.8% on the month, a touch higher even than the 0.7% estimate though the same as February. Personal income increased 0.5%, in line with expectations and higher than the 0.3% increase the previous month.

The personal saving rate fell to 3.2%, down 0.4 percentage points from February and 2 full percentage points from a year ago as households dipped into savings to keep spending afloat.

The report follows bad inflation news from Thursday and likely locks the Fed into holding the line on interest rates through at least the summer unless there is some substantial change in the data. The Commerce Department reported Thursday that PCE in the first quarter accelerated at a 3.4% annualized rate while gross domestic product increased just 1.6%, well below Wall Street expectations.

With inflation still percolating two years after it began its initial ascent to the highest level in more than 40 years, central bank policymakers are watching the data even more intently as they contemplate the next moves for monetary policy.

The Fed targets 2% inflation, a level that the core PCE has been above for the past three years.

The Fed watches the PCE in particular because it adjusts for changes in consumer behavior and places less weight on housing costs than the more widely circulated consumer price index from the Labor Department.

While they watch both headline and core measures, Fed officials believe the index excluding food and energy provides a better look at longer-run trends as those two categories tend to be more volatile.

Services prices increased 0.4% on the month while goods were up 0.1%, reflecting a swing in consumer prices as goods inflation dominated since the early days of the Covid pandemic. Food prices showed a 0.1% decline on the month while energy rose 1.2%.

On a 12-month basis, services prices are up 4% while goods have barely moved, increasing just 0.1%. Food is up 1.5% while energy has gained 2.6%.

Intel used to dominate the U.S. chip industry. Now it’s struggling to stay relevant

PUBLISHED FRI, APR 26 202412:43 PM EDTUPDATED AN HOUR AGO

KEY POINTS

- Intel, once the biggest and most valuable U.S. chip company, has been surpassed by numerous rivals in recent years due to a series of missteps.

- The shares plummeted further on Friday following disappointing earnings.

- Intel is now the worst-performing tech stock in the S&P 500 this year, while rival chipmaker Nvidia is the second-best performer in the index.

Intel’s long-awaited turnaround looks farther away than ever after the company reported dismal first-quarter earnings. Investors pushed the shares down 9% on Friday to their lowest level of the year.

Although Intel’s revenue is no longer shrinking and the company remains the biggest maker of processors that power PCs and laptops, sales in the first quarter trailed estimates. Intel also gave a soft forecast for the second quarter, suggesting weak demand.

It was a tough showing for CEO Pat Gelsinger, who’s early in his fourth year at the helm.

But Intel’s problems are decades in the making.

Before Gelsinger returned to the company in 2021, the company, once synonymous with “Silicon Valley,” had lost its edge in semiconductor manufacturing to overseas rivals like Taiwan Semiconductor Manufacturing Co. Now, in a high-risk quest, it’s spending billions per quarter to regain ground.

“Job number one was to accelerate our efforts to close the technology gap that was created by over a decade of underinvestment,” Gelsinger told investors on Thursday. He said the company is still on track to catch up by 2026.

Investors remain skeptical. Intel is the worst-performing tech stock in the S&P 500 this year, down 37%. Meanwhile, the two best-performing stocks in the index are chipmaker Nvidia and Super Micro Computer, which has been boosted by surging demand for Nvidia-based artificial intelligence servers.

Intel, long the most valuable U.S. chipmaker, is now one-sixteenth the size of Nvidia by market cap. It’s also smaller than Qualcomm, Broadcom, Texas Instruments, and AMD. For decades, it was the largest semiconductor company in the world by sales, but suffered seven straight quarters of revenue declines recently, and was passed by Nvidia last year.

Gelsinger is betting on a risky business model change. Not only will Intel make its own branded processors, but it will act as a factory for other chip companies that outsource their manufacturing — a group of companies that includes Nvidia, Apple, and Qualcomm. Its success acquiring customers will depend on Intel regaining “process leadership,” as the company calls it.

Other semiconductor companies would like an alternative to TSMC so they don’t have to rely on a single supplier. U.S. political leaders including President Biden call Intel an American chip champion and say the company is strategically an important part of the U.S. processor supply chain.

“Intel is a big, iconic semiconductor company which has been the leader for many years,” said Nicholas Brathwaite, managing partner at Celesta Capital, which invests in semiconductor companies. “And I think it’s a company that is worth trying to save, and they have to come back to competitiveness.”

But the chipmaker isn’t doing itself any favors.

“I think everyone has been hearing them say the next quarter will be better for two, three years now,” said Counterpoint analyst Akshara Bassi.

Intel has fumbled the ball for years. It missed the mobile chip boom with the unveiling of the iPhone in 2007. It’s also been largely on the sidelines of the AI craze while companies like Meta, Microsoft and Google order as many Nvidia chips as they can.

Here’s how Intel ended up where it is today.

Missed out on the iPhone

The iPhone could have had an Intel chip inside. When Apple developed the first iPhone, then-CEO Steve Jobs visited former Intel CEO Paul Otellini, according to Walter Isaacson’s 2011 biography “Steve Jobs.”

They discussed whether Intel should power the iPhone, which had not been released yet, Jobs and Otellini told Isaacson. When the iPhone was first revealed, it was marketed as a phone that ran the Apple Mac operating system. It would’ve made sense to use Intel chips, which ran on the best desktops at the time, including Apple’s Macs.

Jobs said that Apple passed on Intel’s chips because the company was “slow” and Apple didn’t want the same chips to be sold to its competitors. Otellini said that while the tie-up would have made sense, the two companies couldn’t agree on a price or who owned the intellectual property, according to Isaacson.

The deal never happened. Instead, Apple went with Samsung chips when the iPhone launched in 2007. Apple bought PA Semi in 2008 and introduced its first homegrown iPhone chip in 2010.

Within five years, Apple started shipping hundreds of millions of iPhones. Overall smartphone shipments — including Android phones designed to compete with Apple — surpassed PC shipments in 2010.

Nearly every modern smartphone uses an Arm-based chip instead of Intel’s x86 technology which was created for PCs in 1981 and is still in use.

Arm chips built by Apple and Qualcomm consume less power than Intel’s processors, making them more desirable for small devices like smartphones that run on batteries.

Arm-based chips quickly improved due to the enormous manufacturing volumes and the demands of an industry that needs new chips every year with faster performance and fresh features. Apple started placing huge orders with TSMC to build its iPhone chips, starting with the A8 in 2014. The tech giant’s orders provided the cash to annually upgrade the manufacturing equipment at TSMC, which eventually surpassed Intel.

By the end of the decade, some benchmarks had the fastest phone processors rivaling Intel’s PC chips for some tasks while consuming far less power. Around 2017, mobile chips from Apple and Qualcomm started adding AI parts to their chips called neural processing units, another advancement over Intel’s PC processors. The first Intel-based laptop with an NPU shipped late last year.

Intel has since lost share in its core PC chip business to chips that grew out of the mobile revolution.

Apple stopped using Intel in its PCs in 2020. Macs now use Arm-based chips, and some of the first mainstream Windows laptops with Arm-based chips are coming out later this year. Low-cost laptops running Google ChromeOS are increasingly using Arm, too.

“Intel lost a big chunk of their market share because of Apple, which is about 10% of the market,” Gartner analyst Mikako Kitagawa said.

Intel made efforts to break into smartphones. It released an x86-based mobile chip called Atom that was used in the 2012 Asus Zenphone. But it never sold well and the product line was dead by 2015.

Intel’s mobile stumble set the stage for a lost decade.

All about transistors

Processors get faster with more transistors. Each one allows them to do more calculations. The original Intel microprocessor from 1971, the 4004, had about 2,000 transistors. Now Intel’s chips have billions of transistors.

Semiconductor companies fit more transistors on chips by shrinking them. The size of the transistor represents the “process node.” Smaller numbers are better.

The original 4004 used a 10-micrometer process. Now, TSMC’s best chips use a 3-nanometer process. Intel is currently at 7-nanometers. Nanometers are 1,000 times smaller than micrometers.

Engineers, especially at Intel, took pride in regularly delivering smaller transistors. Brathwaite, who worked at Intel in the 1980s, said Intel’s process engineers were the company’s “crown jewels.” People in the technology industry relied on “Moore’s Law,” coined by Intel co-founder Gordon Moore, that said the amount of computing power would double and become cheaper at predictable intervals, roughly every two years.

Moore’s Law meant that Intel’s software partners, like Microsoft, could count on the next generation of PCs or servers being more powerful than the current generation.

The expectation of continuous improvement at Intel was so strong that it even had a nickname: “tick-tock development.” Every two years, Intel would release a chip on a new process (tick) and in the subsequent year, it would refine its design and technology (tock).

In 2015, under CEO Brian Krzanich, it became clear that Intel’s 10nm process was delayed, and that the company would continue shipping its most important PC and server processors using its 14nm process for longer than the normal two years. The tick-tock process had added an extra tock by the time the 14nm chips shipped in 2017. Intel officials today say that the issue was underinvestment, specifically on EUV lithography machines made by ASML, which TSMC enthusiastically embraced.

The delays compounded at Intel. The company missed its deadlines for the next process, 7nm — eventually revealing the issue in a bullet point in the small print in a 2020 earnings release, causing the stock to plunge, and clearing the way for Gelsinger, a former Intel engineer, to take over.

While Intel was struggling to keep its legendary pace, Advanced Micro Devices, Intel’s historic rival for server and PC chips, took advantage.

AMD is a “fabless” chip designer. It designs its chips in California, and has TSMC or GlobalFoundries manufacture them. TSMC didn’t have the same issues with 10nm or 7nm, and that meant that AMD’s chips were competitive or better than Intel’s in the latter half of the decade, especially for certain tasks.

AMD, which barely had market share in server CPUs a decade ago, started taking Intel’s business in that area. AMD made over 20% of server CPUs sold in 2022, and shipments grew 62% that year, according to an estimate from Counterpoint Research last year. AMD surpassed Intel’s market cap the same year.

Missing on the AI boom

Graphics processor units, or GPUs, were originally designed to play sophisticated computer games. But computer scientists knew they were also ideal for running the kind of parallel calculations that AI algorithms require.

The broader business community caught on after OpenAI released ChatGPT in 2022, helping Nvidia triple sales over the past year. Companies are spending money on pricey servers again.

AI-oriented GPU-based servers sometimes pair as many as eight Nvidia GPUs to one Intel CPU. In older servers, the Intel CPU was almost always the most expensive and important part. In a GPU-based server, it’s Nvidia’s chips.

Nvidia recently announced a version of its latest “Blackwell” GPU that cuts Intel out entirely. Two Nvidia B100 GPUs are paired with one Arm-based processor.

Almost all Nvidia GPUs used for AI are made by TSMC in Taiwan, using leading-edge techniques to produce the most advanced chip.

Intel doesn’t have a GPU competitor to Nvidia’s AI accelerators, but it has an AI chip called Gaudi 3. Intel started focusing on AI for servers in 2018 when it bought Habana Labs, whose technology became the basis for the Gaudi chips. The chip is manufactured on a 5nm process, which Intel doesn’t have, so the company relies on an external foundry.

Intel says it expects $500 million in Gaudi 3 sales this year, mostly in the second half. For comparison, AMD expects about $3.5 billion in annual AI chip revenue. Meanwhile, analysts polled by FactSet expect Nvidia’s data center business — its AI GPUs — to account for $57 billion in sales during the second half of the year.

Still, Intel sees an opportunity and has recently been talking up a different AI story — that it could eventually be the American producer of AI chips, maybe even for Nvidia.

The U.S. government is subsidizing a massive Intel fab outside of Columbus, Ohio, as part of $8.5 billion in loans and grants toward U.S. chipmaking. Gelsinger said last month that the plant will offer leading-edge manufacturing when it comes online in 2028, and will make AI chips — perhaps those of Intel’s rivals, Gelsinger said on a call with reporters in March.

Intel’s ‘death march’

Intel has faced its old failures since Gelsinger took the helm in 2021, and is actively trying to catch up to TSMC through a process that Intel calls “four nodes in five years.”

It hasn’t been easy. Gelsinger referred to its goal to regain leadership as a “death march” in 2022.

Now, the march is starting to reach its destination, and Intel said on Thursday that it’s still on track to catch up by 2026. At that point, TSMC will be shipping 2nm chips. Intel said it will begin producing its “18A” process, equivalent to 2nm, by 2025.

It hasn’t been cheap, either. Intel reported a $2.5 billion operating loss in its foundry division on $4.4 billion in mostly internal sales. The sums represent the vast investments Intel is making in facilities and tools to make more advanced chips.

“Setup costs are high and that’s why there’s so much cash burn,” said Bassi, the Counterpoint analyst. “Running a foundry is a capital-intensive business. That’s why most of the competitors are fabless, they are more than happy to outsource it to TSMC.”

Intel last month reported a $7 billion operating loss in its foundry in 2023.

“We have a lot of these investments to catch up flowing through the P&L,” Gelsinger told CNBC’s Jon Fortt on Thursday. “But basically, what we expect in ’24 is the trough.”

Not many companies have officially signed up to use Intel’s fabs. Microsoft has said it will use them to manufacture its server chips. Intel says it’s already booked $15 billion in contracts with external companies for the service.

Intel will help its own business and enable better performance in its products if it regains the lead in making the smallest transistors. If that happens, Intel will be back, as Gelsinger is fond of saying.

On Thursday, Gelsinger said demand was high for this year’s forthcoming server chips using Intel 3, or its 3nm process, and that it could win customers who had defected to competitors.

“We’re rebuilding customer trust,” the CEO said on Thursday. “They’re looking at us now saying ‘Oh, Intel is back.’”