HI Market View Commentary 04-17-2023

Please tell me what they are telling us about the economy?

Recession, higher rates to help the overall economy, Chance of recession Q3&4, more bank failures, we can print until the cows come home, debt ceiling will be lifted again,

Was my son’s light red? NO ALL THREE LIGHTS WERE GREEN FOR HIM

Hers was red EVEN though the eyewitness and the experts said it wasn’t

Who are our experts: no experts, they all say the market is going down, TV personalities,

Expert Quotes: 60/40 is now the perfect portfolio for the next generation, The new list of mutual funds will take off for the next decade in a 5% average growth year, Muni, reits and bonds hold all the upside for the next five years

Yes I manage money, my own with yours and I do not know what is going to happen in the future

In real life I am protecting stock ownership when it is most likely to lose 15% or more over a 6 week period

What do we have this week?

We have more uncertainty for the rest of the year

Earnings dates:

AAPL – 5/04 AMC

BA – 4/26 BMO

BAC – 4/18 AMC

BIDU – 5/24

CVS – 5/03 BMO

DIS – 5/10 AMC

F – 5/02 AMC

GE – 4/25 BMO

GOOGL – 5/04

KO – 4/24 BMO

LMT – 4/18 BMO

LUV – 4/27

SQ – 5/04 AMC

UAA – 5/10

V – 4/25 AMC

VZ – 4/24 AMC

https://www.briefing.com/the-big-picture

The Big Picture

Last Updated: 14-Apr-23 14:49 ET | Archive

Inflation (and rate hikes) ain’t over yet

When it comes to inflation, the Federal Reserve concentrates its efforts on fighting core inflation. It has said as much, acknowledging that it doesn’t have the leverage to control volatile food and energy prices.

What it seeks to control, then, is inflation, excluding food and energy. Interest rates are its primary tool for doing that, used either to stimulate aggregate demand when inflation is too low (i.e., cutting rates) or to temper aggregate demand when inflation is too high (i.e., raising rates).

Cutting to the chase, the Fed has raised the target range for the fed funds rate nine times since March 2022 for a cumulative increase of 475 basis points. That is an aggressive course of action because the Fed recognized, albeit too late, that inflation is a problem.

At 5.6% today, core CPI is less of a problem than it was last September when it reached 6.6%. Nonetheless, it is still well above the Fed’s target goal of 2.0% — and that’s a problem.

Take Shelter

The somewhat encouraging consideration is that the shelter index accounted for over 60% of the increase in core CPI. We say encouraging because house price gains, per the S&P Case-Shiller Home 20-City Composite Price Index, have decelerated sharply over the last year. Research done by Fannie Mae indicates house price gains historically lead changes in the CPI shelter cost measures by about five quarters1.

In other words, the shelter index, which is comprised of owners’ equivalent rent and the rent of primary residences, should start factoring into core CPI computations in a more friendly way in coming months. In March 2023, the shelter index was up 0.6% month-over-month and up 8.2% year-over-year.

Take shelter out of the inflation equation, and total CPI, which was up 5.0% year-over-year in March, looks even better at +3.4% year-over-year.

The Fed recognizes this, but here comes the sticking point: Services inflation, which the Fed is watching like a hawk (pun intended), was up 7.2% in March. That is still too high for the Fed’s liking. Excluding shelter, services inflation looks better at +6.1% year-over-year, but, again, that isn’t low enough to calm the Fed’s inflation angst.

If there is one component that makes us think the Fed will press ahead with another rate hike in May, it is this one. Recall that Fed Chair Powell said following the January 31-February 1 FOMC meeting that the Fed was bothered knowing that there had yet to be any discernible disinflation process in core services excluding housing.

The chart above is starting to move the Fed’s way, only it likely hasn’t moved fast enough since that February 1 press conference to convince the Fed that it can pause at this juncture, notwithstanding the regional banking crisis that came to light in the interim.

In fact, several Fed officials have intimated following the March Consumer Price Index that the Fed still has more work to do to bring down inflation. Fed Governor Waller (FOMC voter) was perhaps the most direct, saying in a speech that:

“…despite some encouraging news on a slowing in housing costs, core inflation does not show much improvement and remains far above our 2 percent inflation target. Whether you measure inflation using the CPI or the Fed’s preferred inflation measure of personal consumption expenditures, it is still much too high… I interpret these data as indicating that we haven’t made much progress on our inflation goal… monetary policy needs to be tightened further… Another implication from my outlook and the slow progress lately is that, as of now, monetary policy will need to remain tight for a substantial period of time, and longer than markets anticipate.”

For good measure, JPMorgan Chase CEO Jamie Dimon posited on his bank’s earnings conference call that people need to be prepared for higher rates for longer while BlackRock CEO Larry Fink thinks inflation is going to be stickier for longer.

What It All Means

The idea that that monetary policy will need to remain tight longer than the markets anticipate could very well be the stock and bond market’s albatross as 2023 progresses, assuming the debt ceiling matter gets resolved before any defaults occur.

We haven’t heard a single Fed official suggest the Fed is entertaining a rate cut before the end of the year, though one might concede it is implied given their data-dependent nature. The fed funds futures market, however, has priced in two rate cuts before the end of the year. Notably, that is down from three rate cuts from a week ago, which is to say the third rate cut has been priced out this week after the CPI report.

The CME FedWatch Tool shows a 78.8% probability of a 25-basis points rate hike at the May meeting followed by a 67.0% probability of a pause in June. The first rate cut is projected to happen in September with the second cut coming in December.

A stubborn Fed will force the front end of the Treasury curve and the stock market to recalibrate their more bullish-minded positions. A lot can still happen to validate their current views, yet the signaling from the Fed, and the services inflation that has yet to provide comfort for the Fed, point the way to another rate hike in May.

—Patrick J. O’Hare, Briefing.com

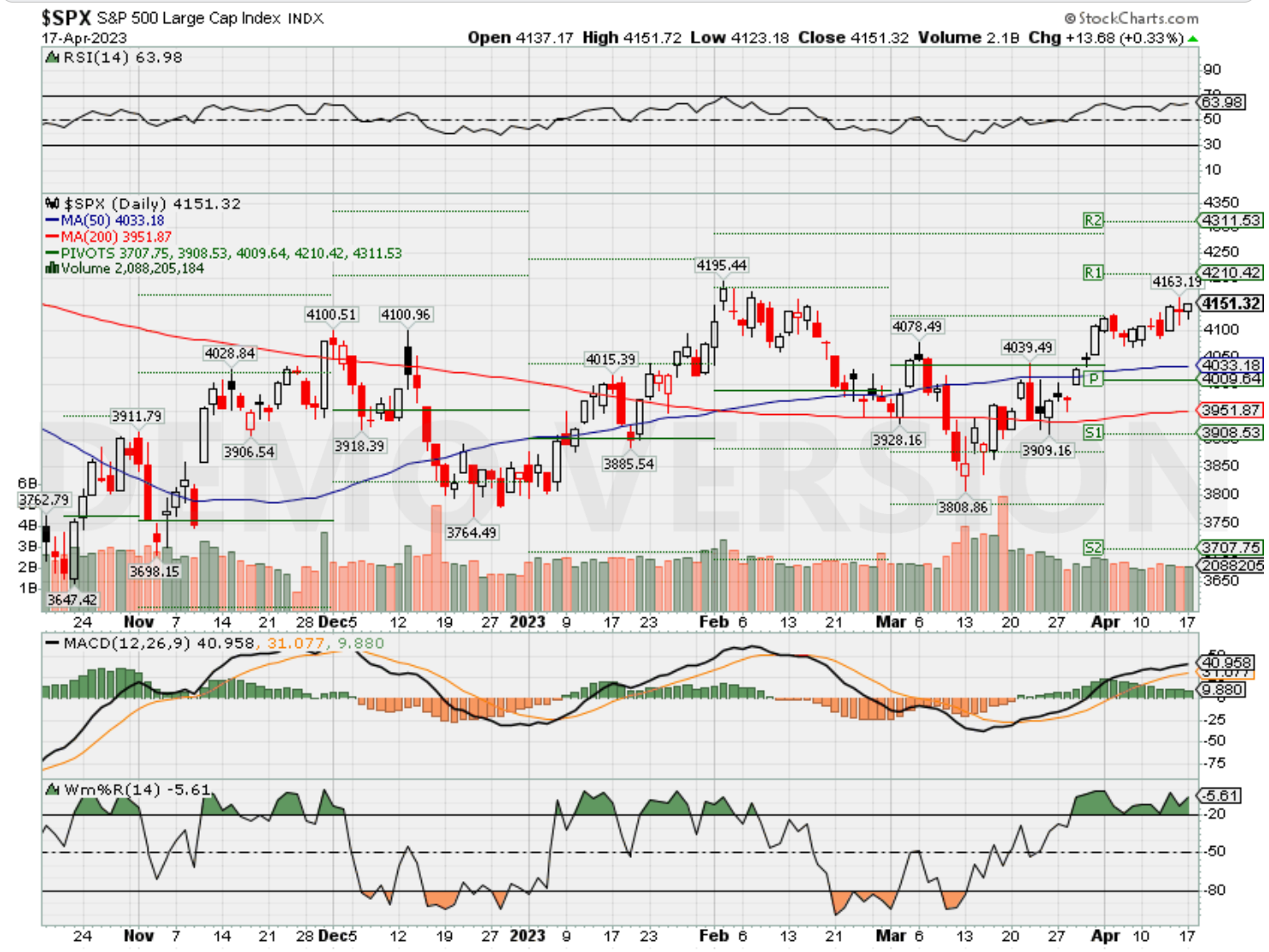

Where will our markets end this week?

Higher

DJIA – Bullish

SPX –Bullish

COMP – Bullish

Where Will the SPX end April 2023?

04-17-2023 -2.0%

04-10-2023 -2.5%

04-03-2023 -2.5%

03-31-2023 -2.0%

Earnings:

Mon: SCHW

Tues: BK, GS, JNJ, FHN, IBKR, ISRG, NFLX, UAL, BAC, LMT

Wed: ABT, LAD, MS, USB, AA, DFS, IBM, KMI, TSLA, ZION

Thur: ALK, AXP, BX, T, DHI, KEY, NOK, NUE, PM, CSX, VMI

Fri: ALV, SLB

Econ Reports:

Mon: Empire, NAHB Housing Market Index

Tue Building Permits, Housing Starts

Wed: MBA, Fed Beige Book

Thur: Initial Claims, Continuing Claims, Phil Fed, Leading Indicators

Fri: MONTHLY OPTIONS EXPIRATION

How am I looking to trade?

www.myhurleyinvestment.com = Blogsite

info@hurleyinvestments.com = Email

Questions???

https://www.investors.com/news/dis-stock-chases-netflix-higher-as-analyst-sees-this-edge-for-disney-vs-its-brand-new-rival-max/

DIS Stock Chases Netflix Higher As Analyst Sees This Edge For Disney+ Vs. Its Brand-New Rival Max

- 04:52 PM ET 04/13/2023

Disney (DIS) beats Warner Bros. Discovery (WBD) with its clearly differentiated video streaming services, a Wall Street analyst said Thursday. Disney stock helped drive the Dow’s advance on Thursday. Meanwhile, Netflix (NFLX) ran near the top of the S&P 500 and Nasdaq 100.

Needham analyst Laura Martin attended Warner Bros.’ Max unveiling event Wednesday and concluded that its execution is lacking.

Warner Bros.’ two streaming services — Discovery+ and the brand-new Max — are not properly differentiated, the analyst said. Max also includes Discovery+ content.

In contrast, Disney has three streaming services — Disney+, Hulu and ESPN+ — but each has a clear target audience, Martin said. Netflix is concentrated into a single streaming service.

Warner Bros. unveiled Max, its enhanced streaming service, Wednesday. Max will launch in the U.S. on May 23.

DIS Stock

Shares of Disney rallied nearly 3% to 100.84 on the stock market today, helping to power the Dow Jones’ advance after another report showed cooling inflation. Shares close a fraction above the 50-day moving average and just below the 200-day.

DIS stock fell 2.5% Wednesday amid the Max unveiling event.

Disney stock lags well below a 118.28 buy point in a cup base that’s part of a larger consolidation.

Netflix rallied 4.6% to 346.19 Thursday, fast approaching a 349.90 entry in a cup-with-handle base.

WBD stock initially rose but closed down 0.1% to 14.04. Shares tumbled 5.8% on Wednesday, falling below the 50-day line. Warner Bros. Discovery is consolidating with a 16.35 buy point, the MarketSmith chart shows. Warner Bros. Discovery debuted last year.

Disney+ Vs. Max

Martin also took issue with other parts of Warner Bros.’ Max streaming video strategy — including the decision to delete “HBO” from the name.

“‘Max’ means nothing (i.e., requires more marketing spending) while ‘HBO’ spent hundreds of millions of dollars over decades to create a brand that meant best-in-class TV,” Martin said.

Overall, the analyst deemed Disney and Amazon (AMZN) Prime Video the winners, beating both Warner Bros. and Netflix.

This is due to the better OTT (over-the-top) strategy, and deeper pockets, of the former two, Martin said.

JPMorgan Chase posts record revenue on higher interest rates; shares jump 7%

PUBLISHED FRI, APR 14 202312:01 AM EDTUPDATED FRI, APR 14 20233:43 PM EDT

KEY POINTS

- Here’s how the bank did: Adjusted earnings of $4.32 per share vs. $3.41 estimate

- Revenue of $39.34 billion vs. $36.19 billion estimate

- The bank also boosted a key piece of guidance: Net interest income will be about $81 billion this year, about $7 billion more than their previous forecast.

JPMorgan Chase posted record first-quarter revenue on Friday that topped analysts’ expectations as net interest income surged almost 50% from a year ago on higher rates.

Here’s what the company reported:

- Adjusted earnings: $4.32 per share vs. $3.41 per share Refinitiv estimate

- Revenue: $39.34 billion, vs. $36.19 billion

15 HOURS AGO

The bank said profit jumped 52% to $12.62 billion, or $4.10 per share, in the first three months of the year. That figure includes $868 million in losses on securities; excluding those losses lifts earnings by 22 cents per share, resulting in adjusted profit of $4.32 per share.

Companywide revenue rose 25% to $39.34 billion, driven by a 49% rise in net interest income to $20.8 billion, thanks to the Federal Reserve’s most aggressive rate-hiking campaign in decades. That topped analysts’ expectations for interest income by more than a billion dollars.

The bank also boosted a key piece of guidance that bodes well for the near future: Net interest income will be about $81 billion this year, about $7 billion more than their previous forecast of $74 billion, CFO Jeremy Barnum said Friday.

The change was mostly driven by expectations that JPMorgan will have to pay less to depositors later this year if the Fed cuts rates, he said.

Shares of the bank rose 7.5%. That is its biggest upside move on an earnings report in more than 20 years, according to Bespoke Investment Group.

“The U.S. economy continues to be on generally healthy footings — consumers are still spending and have strong balance sheets, and businesses are in good shape,” CEO Jamie Dimon said in a release.

“However, the storm clouds that we have been monitoring for the past year remain on the horizon, and the banking industry turmoil adds to these risks,” he said, adding that the industry could rein in lending as banks become more conservative ahead of a possible downturn.

Money in, money out

JPMorgan, the biggest U.S. bank by assets, is watched closely for clues on how the industry fared after the collapse of two regional lenders last month. Analysts had expected JPMorgan to benefit from an influx of deposits after Silicon Valley Bank and Signature Bank experienced fatal bank runs.

Indeed, JPMorgan saw “significant new account opening activity” and deposit inflows in its commercial bank, Barnum said.

The money flows implied “an intra-quarter reversal of the recent outflow trend as a consequence of the March events,” Barnum said. “We estimate that we have retained approximately $50 billion of these deposit inflows at quarter-end.”

That helped cushion a larger trend of customers pulling money out of the regulated banking system as they realize they can earn higher yields in places like money market funds.

JPMorgan saw a 7% decrease in total deposits from a year ago to $2.38 trillion, slightly better than the $2.31 trillion estimate of analysts surveyed by StreetAccount. But, thanks to the recent inflows, deposits actually climbed 2% when compared with the previous quarter.

Slow to act

While commercial clients have been pulling deposits for the past year as rates rose, retail customers have been far slower to act. Now, it looks like Main Street customers have been seeking higher yields; deposits in the bank’s giant retail banking division dropped 4% in the first quarter.

Banks have also begun setting aside more loan loss provisions on expectations for a slowing economy later this year. JPMorgan posted credit costs of $2.3 billion, roughly in line with the StreetAccount estimate, as it built reserves by a net $1.1 billion and booked $1.1 billion in net loan charge-offs.

JPMorgan’s fixed income trading business also helped the bank beat expectations, posting $5.7 billion in revenue, or about $400 million more than expected. Equities trading revenue of $2.7 billion was below the $2.86 billion estimate.

Investment banking remained weak thanks to IPO markets that are still mostly closed, with a 24% decline in revenue to $1.6 billion, just below the $1.67 billion estimate. Barnum said in February that investment banking revenue was headed for a 20% decline from a year earlier.

Dimon’s thoughts

Finally, analysts will want to hear what Dimon has to say about the economy and his expectations for how the regional banking crisis will develop. JPMorgan has played a central role in propping up a client bank, First Republic, which teetered last month, in part by leading efforts to inject it with $30 billion in deposits.

Another key question will be whether JPMorgan and others are tightening lending standards ahead of an expected U.S. recession, which could constrict economic growth this year by making it harder for consumers and businesses to borrow money.

Shares of JPMorgan are down about 4% this year before Friday, outperforming the 31% decline of the KBW Bank Index.

Wells Fargo and Citigroup also topped analyst estimates for revenue Friday. Still ahead are Goldman Sachs and Bank of America results on Tuesday, while Morgan Stanley discloses earnings Wednesday.

‘Gradually, then suddenly.’ Earnings expectations may be about to drop, says Morgan Stanley strategist.

Last Updated: April 17, 2023 at 9:58 a.m. ETFirst Published: April 17, 2023 at 6:50 a.m. ET

By

Barbara Kollmeyer

What did we learn last week? Some big banks are holding up okay after last month’s tremors, thanks to rising rates. That, along with cooling inflation, helped the Dow industrials DJIA close out its longest weekly winning streak since October.

Will optimism hold as earnings season gets fully under way this week and is banking stress done? Our call of the day, from Morgan Stanley’s chief U.S. equity strategist Mike Wilson, warns of a long shadow cast by March stress, despite a mostly upbeat stock market.

“In contrast to what we expected, the S&P 500 SPX and Nasdaq COMP have traded well since SVB [Silicon Valley Bank] first announced it was insolvent. However, small-caps, banks and other highly levered stocks have traded poorly as the market leadership turned more defensive, in line with our sector and style recommendations,” Wilson tells clients in a new note.

The strategist credits “defensive/high-quality characteristics and lower back-end rates” for holding up bigger indexes, but warns against breathing easy here. “On the contrary, the gradual deterioration in the growth outlook continues, which means even these large-cap indexes are at risk of a sudden fall like those we have witnessed in the regional banking index and small-caps,” says Wilson.

He uses a quote from one of Ernest Hemingway’s novels to get his point across. In “The Sun Also Rises,” a character, asked how he went bankrupt, responds: “Two ways…Gradually, then suddenly.” Last month’s bank failures were blamed on a gradual build up of risk from long-duration Treasury holdings and concentrated deposit over the past year that suddenly accelerated, noted Wilson. And as most didn’t see those coming, investors need to stay alert for more fallout, he warns.

One area to watch — earnings and a “gradually, then suddenly,” decline in estimates. Since last June’s peak, the forward 12-month bottom-up consensus earnings per share (EPS) S&P 500 forecast has fallen by around 9% per annum, “which is not severe enough for equity investors to demand the higher equity risk premium we think they should,” says Wilson. And he is neither swayed by consensus earnings forecasts that imply the first quarter will mark an EPS trough — usually a buy signal.

Last week’s bigger-than-inflation drop may also pose trouble for companies, as it hints of sagging demand, as “inflation is the one thing holding up revenue growth for many businesses,” says Wilson.

“The gradually eroding margins to date have been mostly a function of bloated cost structures. If/when revenues begin to disappoint, that margin degradation can be much more sudden, and that’s when the market can suddenly get in front of the earnings decline we are forecasting, too,” he said.

BLOOMBERG, MORGAN STANLEY RESEARCH

How To Invest: 8-Week Hold Rule Helps Latch On To Big Winners

- 08:00 AM ET 04/14/2023

IBD has two main rules for selling a stock: Take your profits at 20% to 25% and cut your losses at 7% to 8%.

If you are buying stocks on breakouts from properly formed bases, following these guidelines will keep your head above water. But there is also a third option, one that can take your 25% profit and turn it into much more. It’s called the eight-week hold rule.

If your stock produces a gain of 20% or more within three weeks of breaking out of a proper base, you may have a true winner on your hands.

IBD research shows that in many cases, stocks that make this quick and powerful move are capable of doubling or tripling in price. Unless your stock shows a clear sell signal, you should sit on your hands for the first eight weeks of such a move.

IBD Founder Discovered Signal

IBD founder William O’Neil conceived this rule in the early 1960’s after being shaken out of Certain-Teed, a winning stock. In a moment of market weakness, O’Neil sold his position for only a two- or three-point gain. Certain-Teed tripled in price without him.

Doing nothing can be a challenge for investors, but your 20% profit cushion helps ease the difficulty.

Unless you are in danger of a complete round trip of gains, hold your stock for those eight weeks. It may appear to wane as it pulls back to or just below the 10-week moving average, but this action is normal.

After the eight weeks lapse, it is time to reassess the stock. It’s likely your stock has returned to or surpassed the area of initial strength, and you can then decide when to sell and take profits.

How To Invest: Shopify’s Monster Run

Shopify (SHOP) broke out of a deep cup base in April 2020. While deep bases normally don’t work out, this was one of many deep patterns that formed during that 2020 bear market and still panned out.

Following the lows of the Covid crash, the stock ran up 24% in three weeks from the 59.49 buy point, triggering the eight-week hold rule (1).

The remaining five weeks saw the price continue to a superb 42% gain, then pull back nearly 19%. But Shopify did not cross below the 10-week moving average, which would have been at least a red flag. The eighth week closed at a split-adjusted 74.26, or 25% above the buy point (2).

Patient investors were quickly rewarded; the very next week ended with Shopify up 48% from the entry (3).

Since the breakout did not cross the 10-week line at any point, it would be logical to use that as your stop. In the week ended Sept. 4, 2020, the stock finally had a close below the 10-week line after notching a 64% gain (4).

The eight-week hold rule is a conditional tool: It is most effective in the first two years of a new bull market.

More wives, husbands have similar earnings. But who’s doing the housework?

By Lois M. Collins, Deseret News | Posted – April 15, 2023 at 12:12 p.m.

SALT LAKE CITY — Though men and women in opposite-sex marriages increasingly earn similar amounts of money, each making between 40% and 60% of the income, women are still doing most of the housework and caregiving, while men spend more time on paid work and leisure activities.

That’s according to a new report from Pew Research Center, released Thursday, that echoes a pattern that’s been seen for some time.

Women are doing more caregiving and household work even when they are the breadwinners, meaning they earn more than 60% of a couple’s income. That remains true when women earn about as much as their husbands. It’s also true when men earn the bulk of or all the marriage’s income.

The only exception is when the woman is the only wage earner. In that case, her husband is likely to do more in terms of caregiving and home chores, making the workload at home more evenly balanced, said Richard Fry, a senior researcher at Pew who co-wrote the report.

Men, however, are still the primary or only breadwinner in 55% of families, down from 85% a half century ago. Men are the sole breadwinner in 23% of marriages, compared to 49% in 1972. That number has been pretty stable since 1992, the researchers said, noting the decline was driven “as women streamed into the labor force.”

Women’s labor force participation went up a lot in the 1970s and 1980s, peaking around 1999. It decreased a bit after that, said Fry. “Married women are not participating in the labor force at greater rates than they were two decades ago,” he noted.

But the share of couples in egalitarian marriages — where both spouses earn roughly the same amount of money — has nearly tripled to 29% from 1972. The share of marriages where the wife is the sole or primary breadwinner has increased from 5% in the past 50 years to 16%. Only 6% of marriages have women as the only wage earner, and women are the primary earner in 10% of marriages today.

Women breadwinners

Among women, those most likely to be the breadwinner in their marriage are Black women, college graduates, women between ages 55 and 64, and those who do not have children at home.

Childless women are more likely to be breadwinners than women actively raising children at home, Fry said.

He said that when a wife has more formal education than her husband, she’s more likely to be the breadwinner. “What’s happening over time, in opposite-sex marriages,” said Fry, “is we have a growing number of marriages where wives are better educated than their husband.”

Fry described as “kind of surprising” the fact that older wives, ages 55 to 64, are “significantly more likely to be the breadwinner compared to younger wives.” Among older wives, it’s 22% compared to 1 in 10 as the breadwinner among young wives 25 to 34.

“There might be a supposition a younger cohort is less likely to have what I will call ‘traditional’ arrangements,” Fry said. “That’s not what’s happening.”

“Having younger children really changes the breadwinning likelihood,” he said, while most women 55 to 64 don’t have young children at home.

“We know that as you age, as you get more years in the labor market and more seniority, wages go up,” Fry said. “It’s clear in this data that a wife who makes $100,000 is more likely to be a breadwinner than one who earns $25,000.”

Richard J. Petts, a sociology professor at Ball State University who was not associated with the Pew report, notes research has shown that for most families, at some point over a woman’s life course, she will be the primary breadwinner. That aligns, he noted, with what Pew found.

Of the differences in the women who are more likely to be breadwinners, he sees few surprises. Black women have a long history of work, often out of necessity. And that the college-educated are more likely to be egalitarian “makes sense to me,” he said.

But Fry emphasizes the report captures a point in time and what the future holds does not lend itself to clear prediction, including whether an imbalance between men and women in education will continue. And while couples’ relative education matters, other factors matter as well, he said.

What we value

As part of the report, the Pew asked 5,152 U.S. adults who are part of its American Trends panel what they believe society values when it comes to earnings and gender roles. The poll was conducted in mid-January.

The survey didn’t ask what men and women value in their own marriage, but rather their assumptions about what society wants.

Most Americans believe society values men’s contributions at work and their earning ability more than what they contribute at home. The report says just 7% believe others value what men do at home more than what they do at work, while just over a third say men’s contributions are valued about equally at work and home.

While it was not part of Pew’s research, Fry said other credible researchers and economists have found that marriages may be less stable and marital satisfaction lower when the wife is the breadwinner, Fry said. “That tends to be particularly true when husbands are less educated. The thinking is it’s an accepted gender norm.”

About half of the adults said women’s contributions at home and work have about equal value. Just over 3 in 10 say women’s contributions at home are more valued, while 20% say their contributions at work are valued more than what they do at home.

Fry said that as couples are making decisions about how much time to devote to the workplace and how best to get their chores done at home, they do what works for them.

Pew’s survey also asked what division of paid work and work at home is best for children.

There, the answer was overwhelmingly a belief that it’s better for kids if both parents are “equally focused on work and home,” at 77%. Just under 1 in 5 said dads should focus on work and moms on home.

The report doesn’t look at a trend on time use, either, but instead provides a snapshot, he said.

Women’s work?

Petts believes people “feel pretty comfortable” with the idea that women need to work and even that their earnings should be more comparable to men’s, but notes the public in general doesn’t seem to support gender equality in the domestic sphere. Research he was part of in recent years “saw a host of more traditional gender attitudes: Moms should be permanently responsible for the house. Moms shouldn’t work when kids are young.” They also found that most believe women do have to work. Otherwise, life is not affordable.

Daniel L. Carlson, an associate professor in family and consumer studies at the University of Utah, has also noted those pervasive perspectives. He wasn’t part of the Pew research, either.

“Those trends in the sense that paid work has become more equal, but unpaid work — child care and housework — remain women’s responsibility tracks pretty well with people’s attitudes,” he said.

Carlson noted a “very ingrained belief that domestic labor, child care especially and also housework, is just a woman’s domain. If they want a career and they want to work for pay, that’s great. But it doesn’t mean they get to give up those contextual responsibilities.”

That belief, he noted, is not male-imposed; a large share of both men and women hold it.

He said research by family sociologist Joanna Pepin, an assistant professor at the University at Buffalo, and others suggests that “people are absolutely fine with women having careers and with equality in the public sphere, but they feel that should not come at the cost of their conventional responsibilities for housework.”

Carlson noted little change in housework division of labor in recent decades — “and even what movement did occur was really women giving up the time they were spending. Things got more equal because women were doing less, not because men were doing more.”

He said working women sometimes skip or outsource tasks. “So you hire cleaning services or eat out more or send out your laundry or buy wrinkle-free Dockers so you don’t have to iron,” he said.

That also tracks with child care, he said. Women who can afford it use it if they work. If they can’t afford it, as the pandemic showed, women quit their jobs. “Child care is seen as a support for mothers, not for the family,” he added.

Petts said he’s a bit perplexed about why, if women are working more, men are not doing more at home to compensate. “I would think it would start to change over time, but change has been slow, incremental,” he said.

There’s no penalty if men don’t do more at home. If women are neglecting family or the house is in disarray, said Petts, they are more likely to be judged and “perceived as bad moms.”

Carlson suspects that what seem to be contradictory attitudes are “also part and parcel of the fact that people are rationalizing the need for women to work. If you’re a couple, you’re really not going to achieve middle class unless you’re in a dual-earner household.”

“Men cannot support their families on their own like they used to, so they have become open to women working, but it also creates an internal contradiction with the belief that women should care for the home,” he said.

“The system is designed around the fact that women provide free care and are the caretakers,” Carlson said. “That’s not just an at-home attitude, but also in the workforce, where businesses operate on the assumption that the ideal worker should always be available to work and does not have other obligations outside the job.”

Carlson said it creates an odd situation when “we penalize women for having care responsibilities we don’t want them to give up.”

He believes policy supports like paid leave and flexible schedules would make it easier for households and both men and women to have the two incomes they need and also take care of their responsibilities at home. The two should not be at war.

All of the questions in the Pew research focused on opposite-sex couples. The earnings data the center used came from the Annual Social and Economic Supplement of the U.S. Census Bureau’s Current Population Survey. Details on how couples use their time came from the American Time Use Survey. Besides Fry, the Pew Research Center report authors are Carolina Aragao, Kiley Hurst and Kim Parker.