HI Market View Commentary 04-22-2024

Freaking META – Update

Each share on an average price made roughly $250 per share – 25K per Hundred shares

Don’t forget half of shares we picked up 100% paid for with put profits

Each 100 shares made $910 with the covered call strategy

We still have stock replacement positions in place

We also closed the 240/300 bull calls with 84% of the total potential profit

We also closed the 300/350 bull calls for 72% of the total potential profit

Everything share count is long term capital gains

We still have 360/400, 400/460, 470/540, 500/550, 520/600 in play (leap bull calls)

Bull Call = Right to buy at a lower price than you are obligated to sell

So now we are cash rich in accounts = MU, Some will add shares to current positions, we are looking to introduce two now positions to accounts

EMAILS with profit expectations need to be read VERY CAREFULLY to find the BS !!!!

According to my records, you haven’t activated your 90-day trial of my brand new SPY 15 Trader day trading program yet.

Maybe it’s because you have a question that we haven’t answered yet.

If so, here are some of the top questions we’ve been getting since we released this program:

Q: If I don’t have a lot of time, what’s the bare minimum amount of time I need to place these trades?

A: Trades can be issued as soon as the market opens, and they can also close in less than 30 minutes. On average, they last about 2.5 hours, so that’s a good rule of thumb. However, you don’t need to pay attention for 2.5 hours – you simply need to be available to act when you receive an alert (on your computer, email, phone, or sms/text) to take action. So for a trade that lasts 2.5 hours, your actual time placing trades will probably be less than 5 minutes.

Q: Can I use any broker to place these trades?

A: We use TradingView to issue the alerts, but you can use any broker that allows you to buy basic call and put options.

Q: How do I overcome my broker’s pattern day trading rule?

A: If your trading account is less than $25,000 and you have margin on your account, you can ask your broker to disable margin. Very simple to do.

Q: How quickly can I get started?

A: After you activate your trial, you could be in your first trade as soon as the next trading day.

Q: Can you guarantee this will make me money?

A: Of course not! Don’t be silly. No one can guarantee that. However, we do offer a 90-day money back guarantee so you can prove to yourself that the SPY 15 Trader can work for you.

—

Click here to join my next SPY 15 Trader workshop…

Good Trading,

Bill Poulos

You are receiving this note because you joined us at one of the Profits Run websites.

Our office hours are Monday – Friday 9AM – 5PM EST

28339 Beck Rd Suite F6, Wixom, MI 48393

Phone: (248) 733-4343 / Email: support@profitsrun.com

Privacy Policy | Terms & Conditions | Disclaimer

Copyright © Profits Run, Inc. All rights reserved.

About Profits Run

At Profits Run, our goal is to teach regular people how to become better, smarter, and safer investors and traders in any market. Whether it’s stocks, options, exchange-traded funds (ETFs), or foreign exchange (forex), we have trading programs for everyone at every level of experience.

You won’t see any crazy income claims from us. Instead, our philosophy is more along the lines of protecting your portfolio as much as possible. And that’s why our primary focus with all of our programs is risk management. Once you learn how to properly manage risk, trading can be a lot less stressful.

Profits Run was founded in 2001 by father and son team Bill Poulos and Greg Poulos. It was named after the saying, “cut your losses and let your profits run”, which most traders know well.

Bill Poulos was born and raised in Detroit, Michigan to a lower middle class family, who were first generation Greek immigrants, and he had to work pretty hard to get where he’s at today.

His parents taught him good old fashioned Midwest sensibilities and instilled a strong work ethic in him at a young age. In fact, in 1960, he became the youngest Eagle Scout in the Detroit area at the time.

He went on to get an engineering degree from General Motors Institute and that’s where he ended up working for 36 years before retiring 12 years early in 2001 at age 53. While at General Motors, Bill started out on the assembly line and worked his way up the corporate ladder over his long and successful career, having traveled and lived all over the world, including Japan, Germany, England, Brazil, and other countries.

His hobby, though, was always studying the markets, which he began to seriously put time into in 1974. Because he was trained as an engineer, he found the challenge of trading a lot of fun and he still does, even today.

Long before home computers, Bill had subscriptions to printed market data which would be delivered daily to his home. After returning home from a long day of work, Bill would eat dinner with his family, tuck his kids into bed, and then disappear into his tiny den in the corner of the house. With a pot of black coffee, a straight edge, a magnifying glass, and a calculator, Bill spent hours analyzing price action and market data. These late-night sessions were the seeds of the core trading principles that became the basis for his trading programs that he later developed.

Bill also ended up getting his master’s degree from the University of Michigan with a focus in finance. While it helped with his career at General Motors, it also helped him as a trader because he’s always thought about trading as a business.

They literally started Profits Run from the kitchen table. One night in the year 2000, Greg was visiting his parents for dinner. The company he was working for was about to close their Michigan office, and Bill was less than a year from retiring, so they would both soon be without jobs. Greg had watched his father master the art and science of trading over the years and had always wanted to start a small business of his own. That’s when he asked Bill, “Why don’t we start a business to help others learn what took you years to figure out?” A year later, Profits Run was born.

And now, years later they have a modest office and at last count have helped over 100,000 regular people from all over the world learn how to become safer and smarter traders. The Profits Run headquarters is in Wixom, Michigan, a small town in the suburbs of Detroit.

Today, not only is Bill able to realize his lifelong dream of helping regular people learn how to trade the markets, but he’s able to create jobs locally through the growth of his business, support the community, and mentor his youngest team members as they learn the ropes of becoming traders themselves.

At Profits Run, Bill has a small team of dedicated trading professionals who really want to see you succeed, and they’re passionate about helping you become the best trader you can be.

When Bill isn’t studying the markets, he can be found in Northern Michigan onboard his sail boat, which is also named Profits Run. Some of the concepts behind his most popular and effective trading programs were discovered when he was sailing his boat across the Great Lakes.

Bill has no plans of “retiring” for a second time any time soon. His son, Greg, continues to manage the day-to-day operations at Profits Run which gives Bill time to focus on helping his members and to experiment with new trading ideas.

If you wish to stop receiving our emails or change your subscription options, please Manage Your Subscription

Profits Run, Inc., 28317 Beck Rd Suite E4, Wixom, MI 48393, US

Earnings Season:

AAPL 05/02 AMC

BA 04/24 BMO

BABA 05/16

BAC 04/16 BMO

BIDU 05/16

DG 05/30

DIS 05/07 BMO

F 04/24 AMC

GM 04/23 BMO

GOOGL 04/25 AMC

JCI 05/01 BMO

KO 04/30 BMO

LMT 04/23 BMO

META 04/24 AMC

MU 06/26

MRO 05/01 AMC

O 05/06 AMC

SQ 05/02 AMC

TGT 05/22 BMO

UAA 05/09

V 04/23 AMC

VZ 04/22 BMO

ZION 04/22 BMO

A Standard 60/40 growth portfolio is killing peoples retirement.

https://www.briefing.com/the-big-picture

The Big Picture

Last Updated: 19-Apr-24 14:48 ET | Archive

Existing home market (still) between a rock and a hard place

The Existing Home Sales Report for March was released this past week, and it conveyed a reality that has been existing for some time: sales activity in the existing home market is weak. The other reality in the report is that selling prices are not weak.

It’s a strange disconnect, but not one that is without explanation, so that is what we will aim to do this week.

Come to think of it, we’ve already explained it. No new explanation is necessary, because the old one we provided in July 2023 will still suffice. Accordingly, we are re-posting that same piece this week with updated charts and updated references to the latest report that indicate the existing home market is still stuck between a rock and a hard place.

An Imbalance

Existing home sales in March were down 3.7% year-over-year at a seasonally adjusted annual rate of 4.19 million. It was another disappointing report on the surface; however, the weak year-over-year sales wasn’t a case of weak demand so much as it was a case of weak supply.

That has been the case for some time now — and we don’t just mean over the time the Fed was raising interest rates.

In a more balanced market, there is typically a 4-6 months’ supply of existing homes for sale based on the prevailing sales rate. The last time we saw 6.0 months of available supply in the existing home market was August 2012. Since that time, the supply of existing homes for sale has averaged just 3.9 months, and over the last five years, it has averaged only 3.0 months. In January 2022 it reached an all-time low of 1.6 months.

There is low supply but there is not low demand. In textbook fashion, then, sales prices have increased, and they seem poised to keep rising.

Supply Constraints

The median sales price in March for all housing types was $393,500. That was the highest price ever for the month of March.

It is remarkable that prices have held up as well as they have given the spike in mortgage rates that has coincided with the Fed’s rate hikes and quantitative tightening.

Then again, it is a matter of supply and demand, and demand hasn’t dropped off because the labor market hasn’t dropped off to this point despite the Fed’s rate hikes. The 3.8% unemployment rate in March remained near a 50-year low.

There are various reasons why the supply of existing homes for sale is so low:

- Gainfully employed homeowners and retirees, who took out mortgages or refinanced mortgages at much lower rates in recent years, don’t want to sell their home and face a higher cost of ownership that comes with today’s higher mortgage rates and high-priced homes.

- The newfound ability to work remotely has curtailed the need to move from favored locations when an employee takes a new job, so there is less turnover now in the housing market than in pre-pandemic years past.

- Investment companies (and individual investors) scooped up a lot of available homes for sale during the Great Recession and onward, turning them into rental properties.

- New construction has been constrained by the higher financing costs, higher land costs, permitting restrictions, and difficulties in finding (and keeping) labor to build the homes. In March, single-family starts were down 12.4% month-over-month to a seasonally adjusted annual rate of 1.022 million. They were up 21.2% year-over-year, but down 22% from the peak hit in December 2020.

Then and Now

The jump in mortgage rates, admittedly, has cooled off the rapid home price appreciation seen in the midst of, and in the wake of, the COVID pandemic. We are inclined to think, too, that some prospective buyers have been scared away by the idea of buying into the market at a “top,” cognizant of the material losses incurred by many homeowners needing to sell during the housing crisis or soon thereafter.

One of the key differences between then and now, however, is that homeowners then were also dealing with rising levels of unemployment. That pressure has not pervaded the existing home market in this cycle — not yet anyway, and it may not, but it is a key difference that helps explain why supply is low and selling prices remain high.

Affordability Not What It Used to Be

Stubbornly high prices combined with a spike in mortgage rates have created some increased affordability pressures that have not been seen for some time. The NAR’s Housing Affordability Index stood at 103.00 in March after hitting a 10-year low of 91.4 in October 2023. An index above 100 means a family earning the median income has enough income to qualify for a mortgage loan on a median priced home with a 20% down payment.

This connection between mortgage rates and affordability is why prospective buyers — and existing homeowners wanting to move — are anxious to see a drop in mortgage rates. That would relieve some of the affordability pressures, but it won’t eliminate them if the labor market is still running strong.

The reason being is that there is undoubtedly pent-up demand, and if/when mortgage rates come down, that will unleash the pent-up demand that will be competing for what is still a relatively scarce supply of existing homes for sale. Accordingly, look for median selling prices to remain stubbornly high.

What It All Means

It may not be as much of a seller’s market in the housing market as it was a few years ago, but that doesn’t mean it is entirely a buyer’s market either. The existing home market is between a rock and a hard place, pressured by tight supply and rising — or maybe we should say a normalization in — mortgage rates.

The speed with which mortgage rates rose was a halting factor for existing home sales and price appreciation, but for some perspective, they remain well below mortgage rates that stretched into the mid to high teens back in the early 1980s. Granted they are higher than the average of 5.6% for the last 30 years, but if the Fed succeeds in slaying inflation, they will moderate and prospective buyers will respond accordingly.

Existing homeowners then are in a reasonably good spot even if it is not the exact spot they want to be in physically. The inference is that ongoing demand encouraged by a strong labor market should keep median prices rising and padding their home equity.

The latter will remain a support for consumer spending via the wealth effect.

If there is a risk to the existing home market and pricing there, it would be another spike in mortgage rates or a crack in the labor market that translates into a significant rise in the unemployment rate. Conversely, some relief on mortgage rates and/or continued strength in the labor market will be good for sellers who want to sell and buyers who want to buy, albeit at higher prices.

—Patrick J. O’Hare, Briefing.com

Earnings dates:

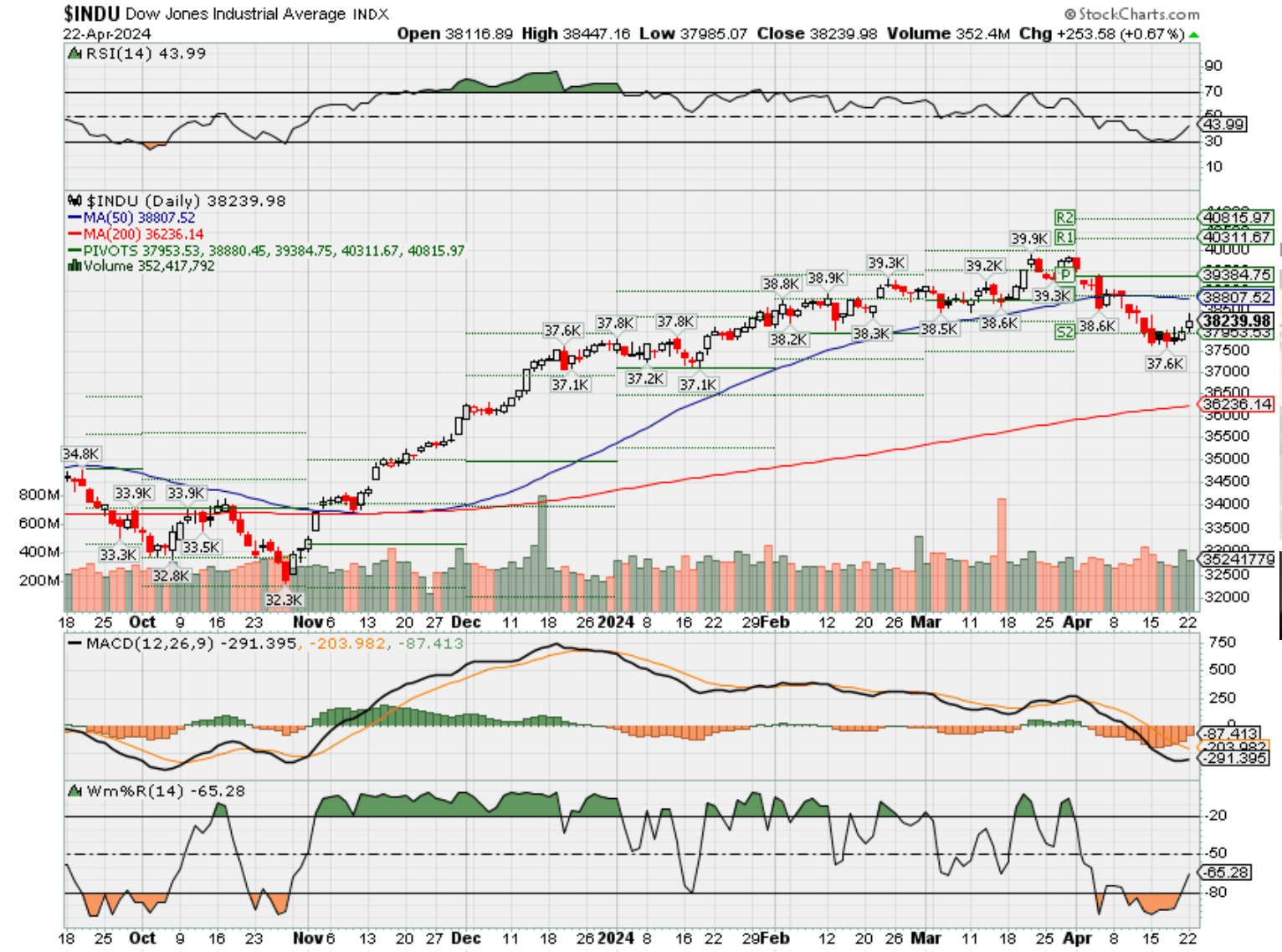

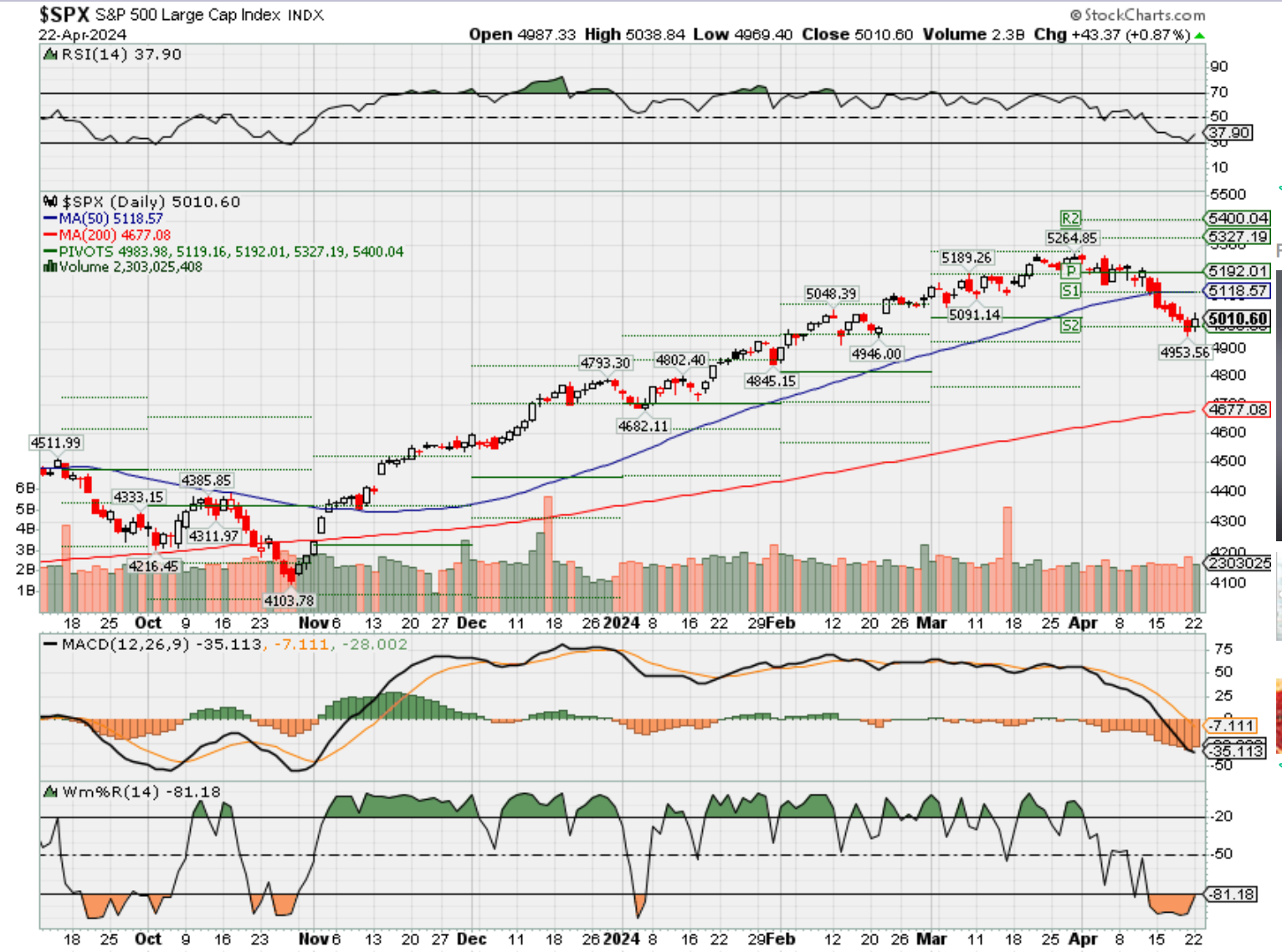

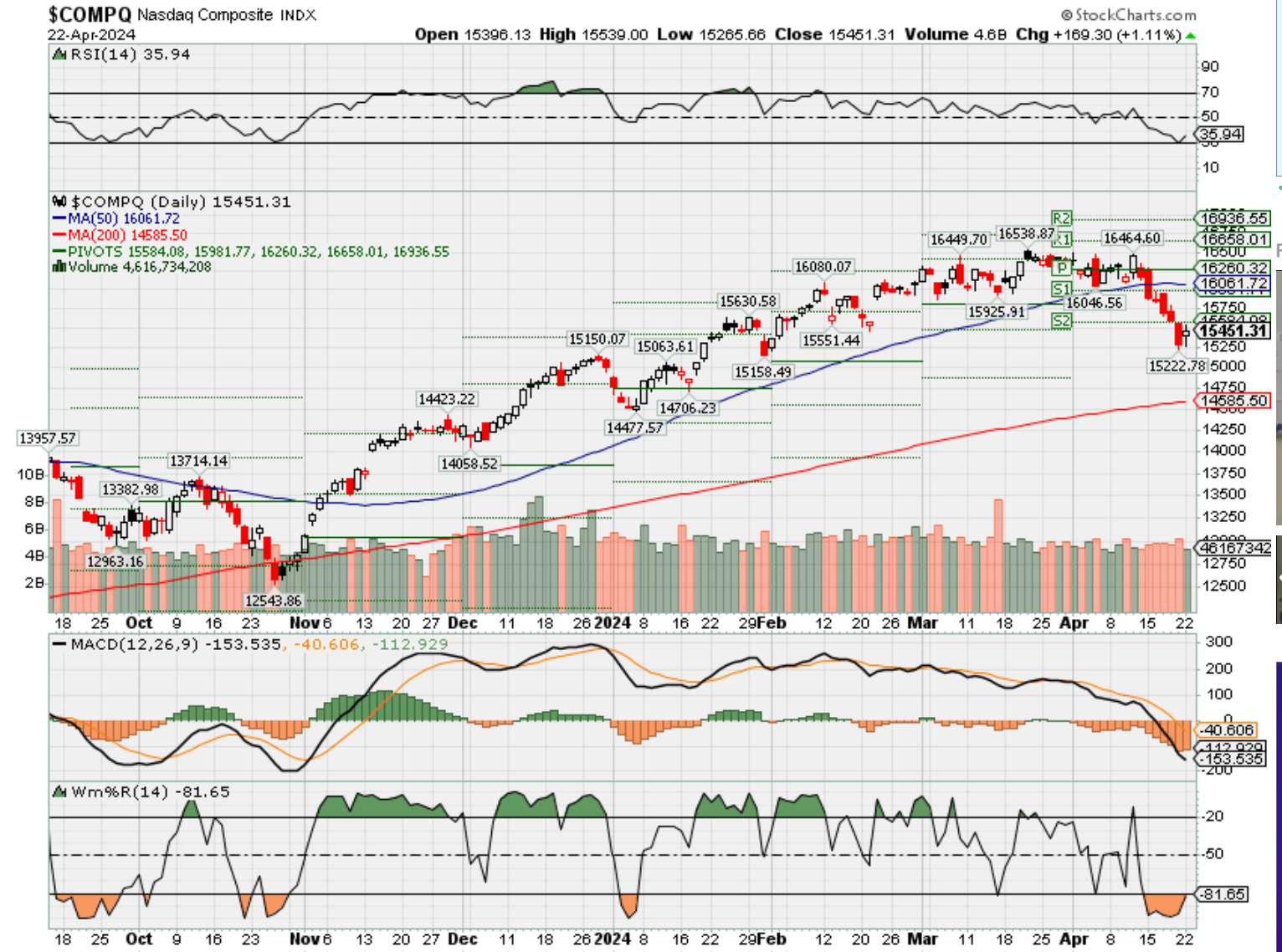

Where will our markets end this week?

Lower

DJIA – Bearish

SPX – Bearish signals and breaking the 50 day SMA usually means more sell orders are

COMP – Bearish signals and breaking the 50 day SMA usually means more sell orders are coming

Where Will the SPX end April 2024?

04-22-2024 -2.0%

04-15-2024 +0.0%

04-08-2024 +2.0%

04-01-2024 +2.0%

Earnings:

Mon: VZ, ZION, CLF, NUE

Tues: HAL, JBLU, KMB, PEP, PHM, UPS, LMT, V, GM, TSLA

Wed: AA, BSX, DFS, KMI, LVS, T, GME, GD, HLTN, LAD, IBM, BA, F, META

Thur: ADT, MO, AAL, BMY, CAT, IMAX, IP, LUV, UNP, COF, JNPR, SNAP, GOOGL, HUBS, MSFT, ROKU

Fri: CVX, XOM

Econ Reports:

Mon:

Tue New Home Sales,

Wed: MBA, Durable Goods, Durable Goods ex-trans

Thur: Initial Claims, Continuing Claims, GDP, GDP Deflator, Pending Home Sales,

Fri: Personal Income, Personal Spending, PCE, Core PCE, Michigan Sentiment

How am I looking to trade?

Mostly protected for earnings

www.myhurleyinvestment.com = Blogsite

info@hurleyinvestments.com = Email

Questions???

Americans think they need almost $1.5 million to retire. Experts say to focus on another number instead

PUBLISHED MON, APR 15 20242:42 PM EDTUPDATED MON, APR 15 20243:48 PM EDT

KEY POINTS

- Americans’ “magic number” savings goal for retirement has increased by over 50% since 2020.

- But experts say the secret to building true wealth is having a high savings rate.

When it comes to retirement, Americans have a new number in mind — $1.46 million — for how much they think they will need to live comfortably, according to new research from Northwestern Mutual.

That estimate is up 53% since 2020, when Americans said they would need $951,000, as the cost of living has surged in recent years. It is also up 15% from last year, when respondents said they would need $1.27 million.

For many savers, that goal may sound daunting, particularly as U.S. adults have an average of $88,400 currently saved toward retirement, the study found. Likewise, a recent CNBC survey showed that 53% of Americans feel like they are behind on their retirement savings.

However, experts say having a “magic number” in mind should not be a priority when planning for your retirement.

“The number isn’t the emphasis,” said John Roland, a certified financial planner and private wealth advisor at Northwestern Mutual’s Beyond Financial Advisors.

“That retirement number is really just a starting point for a broader conversation on how to make clear, competent decisions in that phase of your financial life when you’re distributing money versus when you’re accumulating money,” he said.

Fidelity Investments, the nation’s largest provider of 401(k) savings plans, has moved away from providing broad estimates for what is needed to retire, said Rita Assaf, vice president of retirement products at Fidelity.

“There is no one size fits all,” Assaf said.

She said your income likely differs from other people’s. Other factors — such as how much of your income you hope to replace in retirement, where you plan to live, the lifestyle you plan to have, your health-care costs, and longevity — will all impact the actual number you will need.

“It really depends on your personal situation,” Assaf said. “We do think having a retirement plan helps with that, but it’s got to be a personal retirement plan.”

The number experts say to focus on

Financial advisors agree that having a high savings rate, along with appropriate asset allocations, is one of the most significant components of building wealth. That’s the number to focus on, they say.

Fidelity provides a framework for evaluating your retirement savings progress based on your age.

The framework includes saving your salary by age 30, which then increases to twice your salary by age 35, three times by 40 and continues to go up until the goal of 10 times by age 67.

“That may or may not be feasible depending on where you’re at,” Assaf said of the savings goals. “But it just gives an easier view of what to do.”

The framework assumes that the investor will start saving at age 25 and save 15% annually.

Recent retirement research from Vanguard recommends that workers ramp up their annual retirement savings rate to 12% to 15% of their incomes and invest in an appropriate asset mix for their ages. Doing so can help improve their sustainable investment rate — the highest level of pre-retirement income they can replace.

“I would much rather have clients that save 15% of their income and get a 5% rate of return than save 1% of their income and get a 15% rate of return,” Roland said.

He said that to save money, you need not spend it, a concept emphasized in the book “The Millionaire Next Door.”

“Many people who have significant wealth, you would never know because they don’t look visibly wealthy,” Roland said.

“Those are the people that, as they save and accumulate wealth, oftentimes have accumulated more than they ever anticipated,” he said.

If setting your retirement savings deferral rate to 15% now feels like too much of a financial stretch, you may instead try to boost your contributions by 1% per year. Experts say incremental increases can make a big difference in the long run.

Google terminates 28 employees after multicity protests: Read the full memo

PUBLISHED THU, APR 18 202412:04 AM EDTUPDATED THU, APR 18 20242:07 PM EDT

KEY POINTS

- Google terminated 28 employees Wednesday, according to an internal memo viewed by CNBC, after a series of protests against labor conditions and the company’s contract to provide the Israeli government and military with cloud computing and artificial intelligence services.

- The news comes one day after nine Google workers were arrested on trespassing charges Tuesday night after staging a sit-in at the company’s offices in New York and Sunnyvale, California, including a protest in Google Cloud CEO Thomas Kurian’s office.

- On Wednesday evening, a memo sent by Chris Rackow, Google’s vice president of global security, told Googlers that “following investigation, today we terminated the employment of twenty-eight employees found to be involved. We will continue to investigate and take action as Googleterminated 28 employees Wednesday, according to an internal memo viewed by CNBC, after a series of protests against labor conditions and the company’s contract to provide the Israeli government and military with cloud computing and artificial intelligence services.

The news comes one day after nine Google workers were arrested on trespassing charges Tuesday night after staging a sit-in at the company’s offices in New York and Sunnyvale, California, including a protest in Google Cloud CEO Thomas Kurian’s office.

Some of the arrested workers in New York and Sunnyvale, who spoke with CNBC earlier Wednesday, said that during the protest they were locked out of their work accounts and offices, placed on administrative leave and told to wait to return to work until being contacted by human resources.

On Wednesday evening, a memo sent by Chris Rackow, Google’s vice president of global security, told Googlers that “following investigation, today we terminated the employment of twenty-eight employees found to be involved. We will continue to investigate and take action as needed.”

The arrests, which were livestreamed on Twitch by participants, follow rallies outside Google offices in New York, Sunnyvale and Seattle, which attracted hundreds of attendees, according to workers involved. The protests were led by the “No Tech For Apartheid” organization, focused on Project Nimbus — Google and Amazon’s joint $1.2 billion contract to provide the Israeli government and military with cloud computing services, including AI tools, data centers and other cloud infrastructure.

“This evening, Google indiscriminately fired over two dozen workers, including those among us who did not directly participate in yesterday’s historic, bicoastal 10-hour sit-in protests,” No Tech For Apartheid said in a statement, adding, “In the three years that we have been organizing against Project Nimbus, we have yet to hear from a single executive about our concerns. Google workers have the right to peacefully protest about terms and conditions of our labor. These firings were clearly retaliatory.”

Protesters in Sunnyvale sat in Kurian’s office for more than nine hours until their arrests, writing demands on Kurian’s whiteboard and wearing shirts that read “Googler against genocide.” In New York, protesters sat in a three-floor common space. Five workers from Sunnyvale and four from New York were arrested.

“On a personal level, I am opposed to Google taking any military contracts — no matter which government they’re with or what exactly the contract is about,” Cheyne Anderson, a Google Cloud software engineer based in Washington, told CNBC earlier Wednesday. “And I hold that opinion because Google is an international company and no matter which military it’s with, there are always going to be people on the receiving end … represented in Google’s employee base and also our user base.” Anderson had flown to Sunnyvale for the protest in Kurian’s office and was one of the workers arrested Tuesday.

“Google Cloud supports numerous governments around the world in countries where we operate, including the Israeli government, with our generally available cloud computing services,” a Google spokesperson told CNBC on Wednesday evening, adding, “This work is not directed at highly sensitive, classified, or military workloads relevant to weapons or intelligence services.”

The demonstrations show Google’s increased pressure from workers who oppose military use of its AI and cloud technology. Last month, Google Cloud engineer Eddie Hatfield interrupted a keynote speech from the managing director of Google’s Israel business stating, “I refuse to build technology that powers genocide.” Hatfield was subsequently fired. That same week, an internal Google employee message board was shut down after staffers posted comments about the company’s Israeli military contracts. A spokesperson at the time described the posts as “divisive content that is disruptive to our workplace.”

On Oct. 7, Hamas carried out deadly attacks on Israel, killing 1,200 and taking more than 240 hostages. The following day, Israel declared war and began implementing a siege of Gaza, cutting off access to power, food, water and fuel. At least 33,899 people have been killed in the Gaza Strip since that date, the enclave’s Health Ministry said Wednesday in a statement on Telegram. In January at the U.N.’s top court, Israel rejected genocide charges brought by South Africa.

The Israeli Ministry of Defense reportedly sought consulting services from Google to expand its access to Google Cloud services. Google Photos is one platform used by the Israeli government to conduct surveillance in Gaza, according to The New York Times.

“I think what happened yesterday is evidence that Google’s attempts to suppress all of the voices of opposition to this contract are not only not working but actually having the opposite effect,” Ariel Koren, a former Google employee who resigned in 2022 after leading efforts to oppose the Project Nimbus contract, told CNBC earlier Wednesday. “It’s really just creating more agitation, more anger and more commitment.”

The New York sit-in started at noon ET and ended around 9:30 p.m. ET. Security asked workers to remove their banner, which spanned two floors, about an hour into the protest, according to Hasan Ibraheem, a Google software engineer based in New York City and one of the arrested workers.

“I realized, ‘Oh, the place that I work at is very complicit and aiding in this genocide — I have a responsibility to act against it,’” Ibraheem told CNBC earlier Wednesday. Ibraheem added, “The fact that I am receiving money from Google and Israel is paying Google — I am receiving part of that money, and that weighed very heavily on me.”

The New York workers were released from the police station after about four hours.

The workers were also protesting their labor conditions — namely “that the company stop the harassment, intimidation, bullying, silencing, and censorship of Palestinian, Arab, Muslim Googlers — and that the company address the health and safety crisis workers, especially those in Google Cloud, are facing due to the potential impacts of their work,” according to a release by the campaign.

“A small number of employee protesters entered and disrupted a few of our locations,” a Google spokesperson told CNBC Wednesday evening. “Physically impeding other employees’ work and preventing them from accessing our facilities is a clear violation of our policies, and completely unacceptable behavior. After refusing multiple requests to leave the premises, law enforcement was engaged to remove them to ensure office safety. We have so far concluded individual investigations that resulted in the termination of employment for 28 employees, and will continue to investigate and take action as needed.”

Read the full memo below.

Googlers,

You may have seen reports of protests at some of our offices yesterday. Unfortunately, a number of employees brought the event into our buildings in New York and Sunnyvale. They took over office spaces, defaced our property, and physically impeded the work of other Googlers. Their behavior was unacceptable, extremely disruptive, and made co-workers feel threatened. We placed employees involved under investigation and cut their access to our systems. Those who refused to leave were arrested by law enforcement and removed from our offices.

Following investigation, today we terminated the employment of twenty-eight employees found to be involved. We will continue to investigate and take action as needed.

Behavior like this has no place in our workplace and we will not tolerate it. It clearly violates multiple policies that all employees must adhere to — including our Code of Conduct and Policy on Harassment, Discrimination, Retaliation, Standards of Conduct, and Workplace Concerns.

We are a place of business and every Googler is expected to read our policies and apply them to how they conduct themselves and communicate in our workplace. The overwhelming majority of our employees do the right thing. If you’re one of the few who are tempted to think we’re going to overlook conduct that violates our policies, think again. The company takes this extremely seriously, and we will continue to apply our longstanding policies to take action against disruptive behavior — up to and including termination.

You should expect to hear more from leaders about standards of behavior and discourse in the workplace.

Chris

Breaking down the market sell-off and odds this 5% pullback turns into a 10% correction

PUBLISHED SAT, APR 20 20248:03 AM EDT

Michael Santoli@MICHAELSANTOLI

From relentless rally to persistent pullback, five straight winning months without a 2% decline were then followed by three straight down weeks, featuring a rare six-day S&P 500 losing streak and five successive sessions last week of failed intraday rallies.

As with all market retrenchments from a record high, the current 5.5% setback in the S&P 500 is accompanied by a litany of proximate causes, ready excuses and plausible cover stories — in addition to the simple “we were due” catch-all.

The sticky-inflation and patient-Fed theme has carried the 10-year Treasury yield from 4.2% to above 4.6% in three weeks while expectations of a potential Federal Reserve rate cut have been shoved to the outer edge of traders’ time horizon. Typical seasonal headwinds starting in April of election years and after a strong first quarter apparently arrived on time. Hard-to-handicap geopolitical conflict never helps, even if it rarely serves as the key swing factor in a market trend.

And then there was simply the elevated valuation and over-optimistic sentiment that had built up over that five-month, 28% rally that culminated at the end of March. The dominant momentum leadership that broke stride a few weeks ago (and was previewed here as it peaked) has continued to unwind, a self-reinforcing process in the short term.

Friday’s treacherous rotation out of big-tech winners and into less-loved value sectors (semis down 4%, regional banks up 3%) was particularly stark and seemingly part of an ongoing reversal of extreme positioning among systematic trend-following strategies. We entered 2024 with a market whose most crowded stocks also happened to be some of the largest and most expensive in the world, granted a hefty premium for perceived predictability and the scarcity value of powerful secular-growth plays.

Which takes us to the moment that’s featured in all pullbacks, when the question becomes whether the tape is stretched enough to the downside to expect at least a forceful rebound attempt.

Bounce coming?

Things are at least starting to line up in that direction. The Nasdaq Composite is doubled over in a grueling gut check, dropping nearly 8% from its recent high, cutting back below its old November 2021 peak, slicing below its 100-day average. In the process, it’s grown pretty oversold, with its 14-day relative strength reading (a measure of price relative to a longer-term trend) pretty close to levels seen in the vicinity of past trading lows.

Some market-breadth readings (the low percentage of S&P 500 stocks above a 20-day average, say), elevated put-option volumes and the inversion of the Volatility Index (VIX) relative to VIX futures prices are all similarly hinting at a tightly coiled market susceptible to a high-velocity snapback attempt before long.

This is where the caveats must be noted: Extremes can always grow more extreme and severe liquidation-type selloffs tend to start with oversold readings, with the ever-present chance that stressed trading mechanics among quantitative players can exacerbate pullbacks when they get into risk-reduction mode. Nothing works every time, nor are such oversold indicators always timely when they are prescient. Arguably the decline so far has been a touch too orderly, at least until Friday’s ferocious purge in semis.

And while indicators of traders’ mood have shown increasing caution, most sentiment indicators are merely coming off excessive bullishness and not yet in outright fear mode.

Over the long span of time, about 40% of all 5% market pullbacks deepened into full 10% corrections.

According to Warren Pies, co-founder of 3Fourteen Research, after the Global Financial Crisis, “the 5% dip-buying odds…improved.” From 2009 through 2021, buying 5% dips was “a consistent winner.” On average, the market recovered to new highs within three months of any 5% dip and “only 35% of cases went on to become 10% corrections.”

And yet, Pies stepped back from his previous bullish market view last Thursday, noting that the pattern may have shifted again since 2022, with the upward trend in Treasury yields helping to drive stock corrections rather than the former pattern of yields declining and acting as a buffer as stocks fell, leading most 5% drops to worsen into a 10% haircut.

While observably true, it’s crucial to note that yields haven’t had to retrace all the way back to their levels from before the equity correction in order for stocks to get relief. They have simply needed to stop rising and settle back somewhat. Remember, since 2022, stock investors have successively fretted that 3%, 3.5%, 4% and now perhaps 4.6% 10-year Treasury yields would be kryptonite to stocks. Yet under the right conditions, once the economy shows it can absorb such yields, equities have been able to make a tentative peace with them.

A 10%-ish correction from the S&P 500 high of 5254 would pull the index down below 4800, the former record high from early 2022, and so would be a test of the first-quarter breakout. (In 2013, after the S&P 500 had made its first record high in over five years, it doubled back to briefly test the former record level within a few months before resuming its advance.)

It’s useful to keep in mind that when stocks go down in price they also go back in time, returning to some prior point against which we can assess current fundamentals and ask whether anything substantive has changed.

A week ago, I noted the S&P had closed at the exact level from March 8 – the moment of peak “We can have it all” sentiment, with Fed Chair Jerome Powell implying rate cuts soon on the 7th and a just-strong-enough jobs report that day underscoring economic resilience, and with an AI-stock buying crescendo as a sweetener.

Last week’s 3% decline took the index back to Feb 21 and thereby closed the “Nvidia gap,” the 100-point S&P 500 pop the day after Nvidia’s blowout fourth-quarter earnings report. Nvidia shares themselves closed just above its Feb. 22 level, though are a couple of P/E points lower (29-times forward earnings now versus 31.5 then) thanks to rising profit forecasts.

Valuation check

As for the broader market, the S&P 500′s forward multiple is down from 21 a month ago to 20, no one’s definition of cheap, though as ever the equal-weighted index sits at a glaring discount to the marquee version.

Betting on the wider field of stocks to do well relative to the dominant trillion-dollar-and-up market-cap has been tricky due in part to those rising bond yields, which in recent times have smothered any broadening action.

Not only are cash-rich, secular-growth mega-caps inured to higher financing costs, they are deemed generally defensive against macro flux. Not to mention the fact that Big Tech dominates the earnings-momentum scoreboard, with significant upward profit revisions in recent quarters.

Barclays

With Treasury yields taking a breather on Friday from their recent project of probing for the economy’s pain threshold, energy and traditional defensive groups were the main leaders, along with financials. Whether this reflects healthy rotation in response to economic resilience or more the erratic flight from crowded bets by fast professional players is a question to hold in mind into next week.

Regional banks, up 3% Friday, are now four quarters removed from the mini-crisis around Silicon Valley Bank, with credit and deposit pressures looking manageable for now, and the stocks as a group trading at just 90% of book value in what most are now arguing is a briskly growing economy.

Next week brings the PCE report which will mark inflation to market relative to the Fed’s target, leaving open the prospect of another narrative shift in a less-hawkish direction now that the market has migrated to assumptions of an indomitable consumer and a higher-for-longer rate assumption.

On a trading basis, aside from the oversold readings starting to accumulate, it would seem the pullback has helped at least to clean up aggressive positioning and cool off investor expectations just in time for the heaviest week of big-cap earnings reports.

You could claim up to $500 from Walmart as a part of a $45 million class action lawsuit—here’s how to check

Published Fri, Apr 19 202412:02 PM EDT

Attention shoppers, you may be eligible to receive up to $500 from Walmart if you purchased certain groceries from the big box retailer over the past six years. But the June 5 deadline to file a claim is quickly approaching.

A class action lawsuit filed in Florida claims that “Walmart uses unfair and deceptive business practices to deceivingly, misleadingly, and unjustly pilfer, to Walmart’s financial benefit, its customers’ hard-earned grocery dollars.”

The lawsuit specifically alleges Walmart “falsely inflates the product weight” and overcharged shoppers for certain “weighted goods” and “bagged citrus.” This includes meat, poultry, pork and seafood products that are sold by weight and organic oranges, grapefruit, tangerines and navel oranges sold in Walmart stores that were sold in bulk in mesh or plastic bags, per the settlement’s website.

“We will continue providing our customers everyday low prices to help them save money on the products they want and need. We still deny the allegations, however we believe a settlement is in the best interest of both parties,” a Walmart spokesperson told CNBC Make It.

Here’s how to see if you’re eligible for a cash payment and how to file a claim.

Who is eligible for a cash payment from Walmart’s settlement

As a part of the $45 million settlement, some Walmart customers may qualify to receive up to $500 cash payments.

You may be eligible if you purchased weighted goods and/or bagged citrus in-person from Walmart, Walmart Supercenter or Walmart Neighborhood Market in the U.S. or Puerto Rico between Oct. 19, 2018 and Jan. 19, 2024, according to the settlement’s website.

The amount you receive will depend on how much you spent on those items at a Walmart store during that time period. Here are the potential payouts, per the settlement website.

- $10: If you’re approved and don’t have receipts, proof of purchase, or other documentation but attest to Purchasing up to 50 Weighted Goods and/or Bagged Citrus

- $15: If you’re approved and don’t have receipts, proof of purchase, or other documentation but attest to Purchasing 51 up to 75 Weighted Goods and/or Bagged Citrus in-person

- $20: If you’re approved and don’t not have receipts, proof of purchase, or other documentation but attest to Purchasing 76 up to 100 Weighted Goods and/or Bagged Citrus in-person

- $25: If you’re approved and don’t have receipts, proof of purchase, or other documentation but attest to Purchasing 101 or more Weighted Goods and/or Bagged Citrus

- Up to $500: If you’re approved and have receipts, proof of purchase, or other documentation that substantiates (a) each Weighted Good and/or Bagged Citrus Purchased in-person in a Walmart Store during the Settlement Class Period, and (b) the amount paid for each Weighted Good and/or Bagged Citrus Purchased, then that Approved Claimant will be entitled to receive 2% of the total cost of the substantiated Weighted Goods and Bagged Citrus Purchased, capped at five hundred dollars ($500)

The deadline to submit a claim online or via mail is June 5, 2024. The form will ask you for your name, address, contact information and whether you have receipts for your purchases or not.

If you’re approved for a cash payout, you’ll receive your payment in the form a a prepaid Mastercard, direct deposit, Zelle transfer or Venmo transfer, per the settlement’s website.

Want to make extra money outside of your day job? Sign up for CNBC’s new online course How to Earn Passive Income Online to learn about common passive income streams, tips to get started and real-life success stories. Register today and save 50% with discount code EARLYBIRD.

Plus, sign up for CNBC Make It’s newsletter to get tips and tricks for success at work, with money and in life.

If you’re investing in the AI theme for the long haul, here’s how to pick the winners

PUBLISHED SAT, APR 20 20247:51 AM EDT

KEY POINTS

- Excitement around artificial intelligence lifted a slate of tech stocks to astronomical heights, contributing to the rise of the Magnificent Seven in 2023.

- But these names can see plenty of volatility. On Friday, the tech-heavy Nasdaq Composite slid more than 2% as Nvidia plummeted 10%.

- Investors examining the AI space should look into names with staying power and remain diversified. Selecting ETFs that incorporate dozens of names can be a lower-risk way to diversify, one expert said.

Artificial intelligence has shaken up the investing landscape since the groundbreaking launch of ChatGPT in November 2022.

Since then, investors have poured money into all things related to AI as they hunt for the next big winners. In 2023, a group of major technology players dubbed the Magnificent Seven — Tesla, Amazon, Meta Platforms, Apple, Microsoft, Alphabet and Nvidia — contributed to a large chunk of the market’s rally.

Those tail winds continued into 2024, but even the winners eventually reach their limit. Indeed, some of this year’s highest fliers came down to earth on Friday, with Big Tech names dragging down the Nasdaq Composite by more than 2%.

“You have to do your work,” said Jay Woods, chief global strategist at Freedom Capital Markets. “You want to do the research, you want to know what you’re buying, you want to know the risks involved. In AI right now, there are a lot of unknowns.”

AI is poised to be a central theme as the technology transitions from early-stage winners to second-stage adopters. Portfolio and wealth managers say investors may want to undertake certain strategies if they’re looking for long-term plays in the space.

What to look for

There’s no secret formula to investing and picking artificial intelligence stocks, but investors can keep an eye on certain metrics and trends when weeding out the winners from the duds.

When investing in any new industry, Carol Schleif, chief investment officer at BMO Family Office, recommends that investors keep an eye on companies’ cash burn and how they are spending their money. Be attentive to the fine details, including how a company works through a backlog and how much money it devotes toward infrastructure.

When it comes to chip stocks, Schleif also recommends taking a look at government grants. The industry won big in 2022 when President Joe Biden signed the CHIPS Act into law. The measure allocated funds toward building out semiconductor production on U.S. soil.

Samsung Electronics is in line to receive funding from CHIPS for making semiconductors in Texas, while Intel has been awarded up to $8.5 billion from the measure.

“Focus on the underlying fundamentals, and are they moving in the right direction, [rather] than just last quarter’s earnings,” Schleif advised.

Investors should also avoid blindly chasing the hot winners that have benefited from AI enthusiasm. For Laffer Tengler Investments CEO and CIO Nancy Tengler, that means looking at some of the old-economy stocks embracing the new digital wave. She likes Microsoft and IBM, a pair of tech industry veterans.

When building any portfolio, financial advisors and portfolio managers stress the importance of diversification — and the same applies to AI.

An exchange-traded fund might be a good way to get that diversified exposure to a basket of stocks that could benefit from the AI theme, rather than sticking with one or two promising names.

Consider diversifying through ETFs

Selecting ETFs that incorporate dozens of names can be a lower-risk way to diversify, said Marguerita Cheng, a certified financial planner and CEO of Blue Ocean Global Wealth in Gaithersburg, Maryland.

She highlighted the Global X Robotics and Artificial Intelligence ETF (BOTZ), the First Trust Nasdaq AI and Robotics ETF (ROBT) and the Global X Artificial Intelligence & Technology ETF (AIQ).

“That’s one way to get some exposure without putting the proverbial all the eggs in that one basket,” said BMO’s Schleif. “You want to be able to focus on a few different avenues such that you can withstand the volatility.”

AI ETFS AND THEIR PERFORMANCE IN 2024

| TICKER | NAME | EXPENSE RATIO | %CHG YTD |

| BOTZ | Global X Robotics and Artificial Intelligence ETF | 0.68% | 0.53% |

| ROBT | First Trust Nasdaq AI and Robotics ETF | 0.65% | -10.34% |

| AIQ | Global X Artificial Intellligence & Technology ETF | 0.68% | 0.90% |

| CHAT | Roundhill Generative AI and Technology ETF | 0.75% | 3.20% |

Source: fund websites, FactSet

Volatility can be a bitter pill, particularly for newer investors. Stocks tend to rise at first when a new theme hits the mainstream, but often suffer at some point from volatility and pullbacks, said Helen Dietz, a CFP and managing director at Aspiriant.

“The newer the trend, the more volatile the trend,” she said. “The corrections of those individual stocks, or those sectors, can be quite violent at times, which is not unusual, and the investing public gets scared out of that.”

To that effect, Nvidia’s shares suffered a setback on Friday when they tumbled 10% and posted their worst day since March 2020. The decline put a sizable dent into the chip stock’s year-to-date gains, but it remains up nearly 54% in 2024. Fellow AI play Super Micro Computer also took a nosedive that day, dropping 23%.

ETFs typically include a range of names and can vary in weighting. Though the BOTZ ETF and the Roundhill Generative AI and Technology ETF (CHAT), both currently lag some of this year’s popular AI winners. However, the underlying names are varied: BOTZ holds Nvidia and robotics play Intuitive Surgical, while CHAT’s top holdings include Microsoft, Meta and ServiceNow.

Schleif recommends looking for ETFs with high trading volume and backed by reputable companies. Investors should also be mindful of fees, which can take a bite out of returns if they are too high.

While the gains may fall short of the surge seen in stocks such as Nvidia and Meta, ETFs allow investors to obtain lower-risk exposure to the sector, Woods said. Longer term, investors can also use the leadership in these funds to consider picking out individual names further down the road.

“The old cliché is timing the market and then hoping you find that individual stock that can really be the big performer,” Woods said. “If you want to be involved, you want to be diversified and I think an ETF is the best way to do that.”