HI Market View Commentary 09-05-2023

![]()

![]()

META 17Jan25 240 Long call means on Jan17, 2025 we have the right to buy META @ $240

This is our profit side of the equation +1137.73

BUT WE HAVE ANOTHER SIDE OF THE TRADE

META 17Jan25 300 Short call means on Jan 17, 2025 we are obligated to sell META @ $300

Thought behind the trade Buy $240 Sell @ $300 and make $60 per contract x 100 = $6000 profit

Cost = 8,657.22-5,590.22 = 3067

NET profit 6000-3067=$2,933

Profit right now +1,137.78 – 819.78 = $318 or 10.8% on the trade

Earnings dates:

MU – 9/27

https://www.briefing.com/the-big-picture

The Big Picture

Last Updated: 01-Sep-23 14:51 ET | Archive

Bring on the less good economic news

Anyone who has looked at a map directory knows where they are, as the directory aptly points out “You are here.” Those words are your orientation point, enabling you to surmise by looking at the directory where you should turn to get to your intended location.

For right-brained people, map reading comes easily. For left-brained people, it is a different story. Even though they know where “here” is, it is a more challenging exercise looking at the directory to get “there.”

We point this out, because we are all wondering how the U.S. economy is going to get from here to there in the wake of the Fed’s rate hikes and what “there” will look like.

A String of Less Good News

We learned this past week that we are here:

- The Consumer Confidence Index dropped to 106.1 in August from 114.0 in July.

- JOLTS – Job Openings were 8.827 million in July versus 9.165 million in June.

- The ADP Employment Change Report estimated 177,000 jobs were added to private-sector payrolls in August versus 371,000 in July.

- Real GDP growth in the second quarter was 2.1% versus 2.4% in the advance estimate.

- The PCE Price Index was up 3.3% year-over-year in July, versus 3.0% in June, and the core-PCE Price Index was up 4.2% year-over-year in July, versus 4.1% in June.

- The unemployment rate was 3.8% in August versus 3.5% in July.

- The 3-month moving average for nonfarm payrolls was 150,000 versus 181,000 in July.

- The ISM Manufacturing Index was 47.6% in August versus 46.4% in July, sticking below the 50.0% dividing line between expansion and contraction for the tenth straight month.

In aggregate it wasn’t the best of economic news this past week, but to be fair, the economic news heard this past week wasn’t bad news either. It was simply less good…. and that was good in the eyes of the stock and bond markets, which are anxious to be convinced that the Federal Reserve is done raising rates.

How do we know these markets liked what they heard? The Russell 2000 was up 3.8%, and the S&P 500 was up 2.3%, for the week as of this writing, the 2-yr note yield was down 20 basis points for the week to 4.87%, and the 10-yr note yield was down six basis points to 4.17%.

Less Good Is Better than Bad

There is an axiom that makes its way into the market narrative occasionally. You may have heard it: “Bad economic news is good news for the market.”

This axiom gets trotted out when interest rates have been rising and there is a fear that they could keep rising because the economy is performing stronger than expected and/or inflation is higher than expected.

The gist of why “bad economic news is good news for the market” is that it should ultimately invite lower interest rates. Stocks like lower interest rates. Bonds, meanwhile, like the thought that bad economic news will give way to friendlier monetary policy and lower inflation.

It is a clever-sounding axiom, but the stock market doesn’t like bad economic news so much as it likes less good news.

Truly bad economic news is going to translate into bad earnings news. Consequently, investors will be less willing to pay up for earnings growth that is in doubt because of the bad economic news.

At this time, too, one wouldn’t want to see truly bad economic news so much as one would want to see less good economic news. The reason being is that the market has embraced the soft landing/no landing scenario, so the arrival of a stream of truly bad economic news will inevitably stoke renewed fears of the Fed having made a policy mistake by tightening too much, too quickly, and cultivating a hard landing for the U.S. economy.

Nobody wants the latter, particularly at a time when China’s economy is struggling, as it would have a cascading effect on the global economy. Granted that might invite lower rates, but it would also invite downward earnings revisions that are not in today’s mix, either in terms of the estimates themselves, which are being revised higher, or in the market’s above-average valuation.

What It All Means

The economic data thus far don’t support the hard landing view. That includes this past week’s data — and it is a comforting thought.

The important thing now is for the economic data to remain, at worst, on a lower and slower glide path. That would keep the soft-landing view en vogue and presumably keep the Fed on hold, which is what the market desires knowing that a rate cut isn’t in the offing because the core-PCE inflation rate is still well above the 2.0% target. It would also keep policy mistake concerns at bay.

It is enough for now to think the Fed is done raising rates, because we are “here” and here is as good a spot as any right-brained or left-brained person could have hoped to be when looking at a map directory in March 2022 that indicated there would be 11 rate-hike turns before we got here.

We can’t be sure, however, that we have reached our destination because the Fed is not sure yet that it has reached its ultimate policy rate destination.

Many people see a path now to a soft landing or no landing at all. Others, though, are still mapping out a hard landing for the U.S. economy. Time will tell which view is right and which view is, er, left when we finally get “there.”

—Patrick J. O’Hare, Briefing.com

(Editor’s Note: The next installment of The Big Picture will be published the week of September 11)

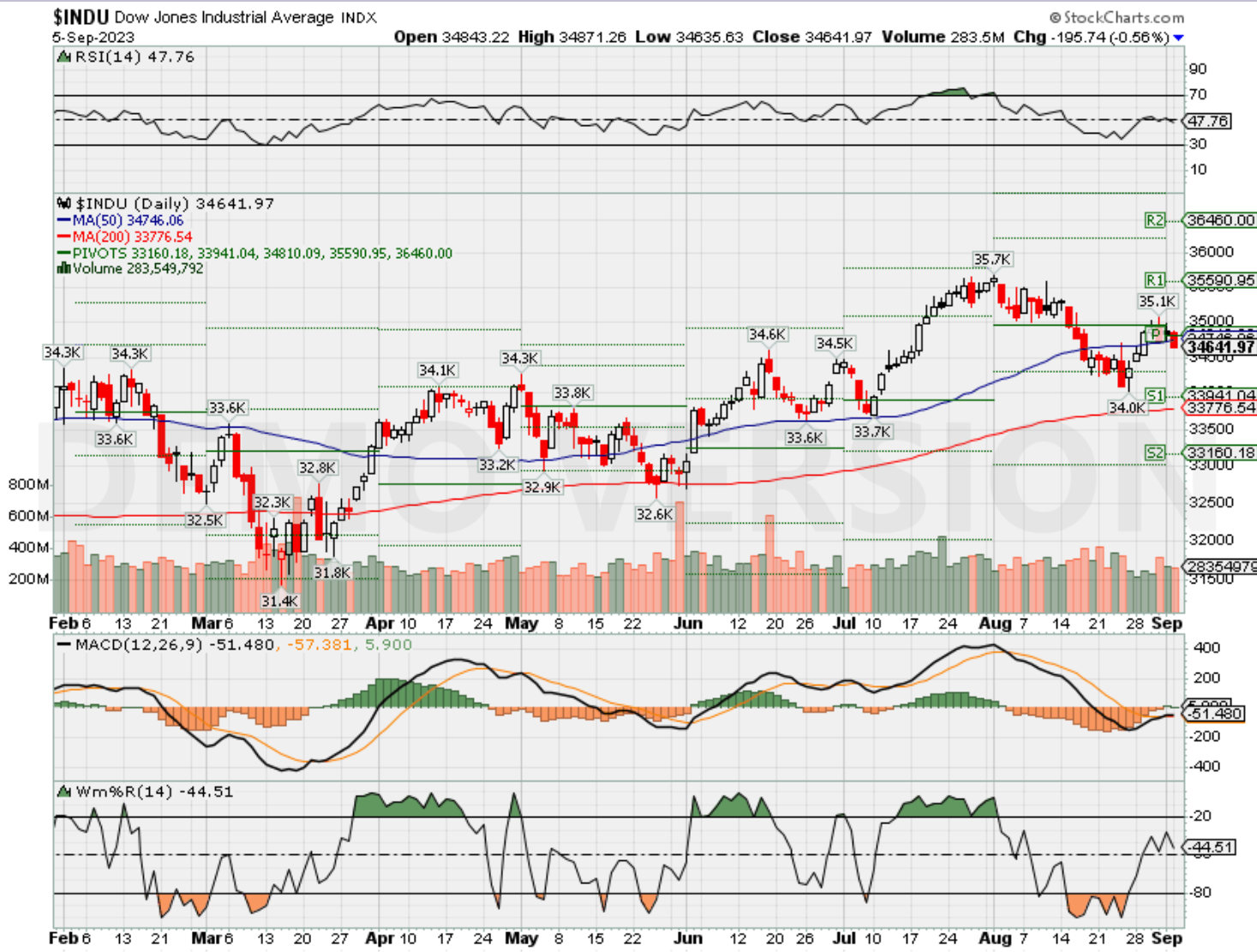

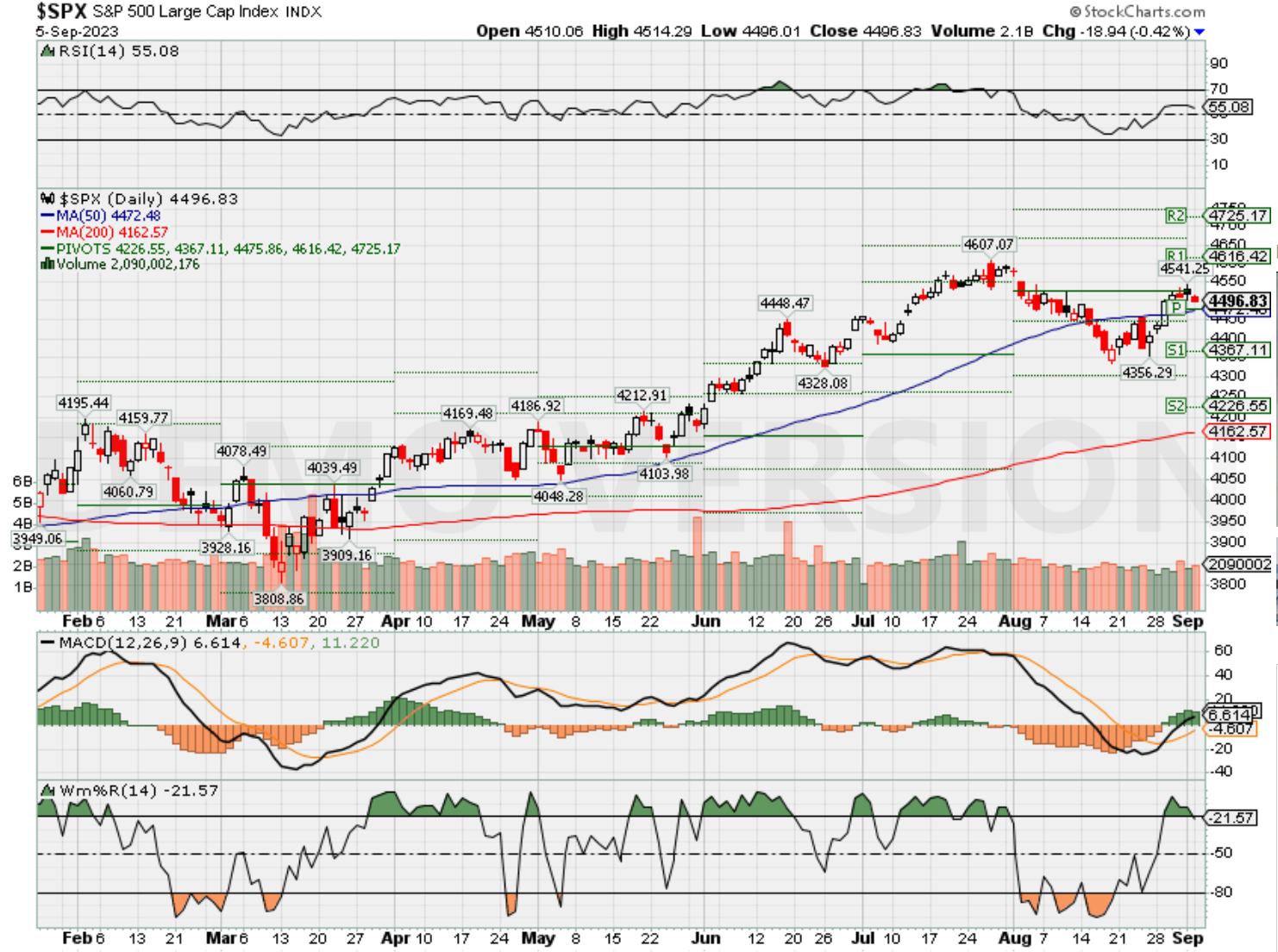

Where will our markets end this week?

Lower

DJIA – Bearish

SPX –Bullish

COMP – Bullish

Where Will the SPX end September 2023?

09-05-2023 -1.5%

08-28-2023 -1.5%

Earnings:

Mon:

Tues:

Wed: GME,

Thur: DOCU,

Fri: KR,

Econ Reports:

Mon:

Tue Factory Orders,

Wed: MBA, Trade Balance, ISM Services, Fed Beige Book

Thur: Initial Claims, Continuing Claims, Productivity, Unit Labor Costs

Fri: Wholesale Inventories, Consumer Credit

How am I looking to trade?

We took some great profits on core holdings and ready to add protection back on for September

www.myhurleyinvestment.com = Blogsite

info@hurleyinvestments.com = Email

Questions???

Hedge funds have made a huge push into risky assets. Here’s what that means.

Last Updated: Aug. 30, 2023 at 10:03 a.m. ETFirst Published: Aug. 30, 2023 at 6:56 a.m. ET

By

Barbara Kollmeyer

Critical information for the U.S. trading day

Tuesday’s pop for stocks after some grim job opening data helped the S&P 500 and other indexes trim August losses, though landing in the green for the month may be still be a long shot.

For those investors who have found this summer tough going, a team at UBS led by chief investment officer Mark Haefele offer validation. They say markets have being pulled in opposing directions “netting to no clear direction overall.” That’s as lots of big simple questions have no answers right now, such as how strong is the consumer and are investors selling rallies or buying dips?

Haefele says positioning suggests investors are only back to neutral on stocks, and with the S&P 500 only off 3.4% from its recent peak, there’s “hardly a large dip to buy after a strong rally.”

Onto our call of the day from Société Générale, which flags a risk indicator tracking hedge funds that is “increasingly risk-on.”

As SG’s strategist Arthur van Slooten and head of global asset allocation Alain Bokobza note, hedge fund positions, whether long or short, are worth watching as they can shed light on financial market trends.

“After a nice summer break, we discover that hedge funds have continued to adjust positions upward and are now clearly risk-on,” they say.

They illustrate that via their Multi Asset Risk Indicator — SG MARI, which qualifies hedge fund positions as risk on or risk off — now at its highest level of 1.52 since summer 2018, when it saw a peak of 2.76. “The current peak has been almost 13 months in the making. During this period, SG Mari has increased by 2.7 points, ranking the episode among the top four strongest recoveries since 2005,” say the strategists, offering the below chart:

Van Slooten and Bokobza say fortunately, the current level of their risk indicator MARI is “still comfortably below the zone that indicates investor exuberance,” which would be a level of 2 or above.

“That said, even though it is still some way from that danger zone, most surges in SG MARI (see shaded areas on the above chart) have been followed by significant drops (see arrows on the chart) in the indicator,” they say. So, think hedge funds having piled into stocks and other assets, backing out in a big way.

In May, the strategists noted inconsistency of hedge fund positioning in bonds and equity. Since that time, shorts on stocks to hedge against a recession have largely been neutralized.

“So, recession fears seem to have been ditched for now, potentially at a rather unfortunate moment,” say the pair.

Last word goes to wish a happy 93rd birthday to Warren Buffett. Long may one of the world’s most followed investors reign.

Baidu’s Ernie bot jumps to the top of Apple’s app store in China

PUBLISHED WED, AUG 30 20239:49 PM EDTUPDATED THU, AUG 31 20231:01 AM EDT

KEY POINTS

- Chinese tech giant Baidu announced Thursday its ChatGPT-like Ernie bot was now open to the public.

- That signaled a green light from Beijing, and another indication of a more relaxed policy stance on artificial intelligence.

- During an earnings call last week, Baidu CEO Robin Li called new AI rules “more pro-innovation than regulation” and said the company was “quite optimistic about the future for a better regulatory environment.”

BEIJING — Baidu’s Ernie bot ranked first in popularity on Apple’s app store in China after the Chinese tech giant said Thursday it was releasing its ChatGPT-like chatbot to the public.

Baidu’s Hong Kong-listed shares rose by more than 3% in morning trade.

The news signaled a green light from Beijing, and another indication of a more relaxed policy stance on artificial intelligence.

Baidu released Ernie bot on March 16. Initial access was limited to the company’s business partners and people who had first joined a waitlist — whose numbers swelled to more than 1.2 million before Baidu stopped disclosing them.

As of Wednesday, CNBC was able to access Ernie bot without the prior restriction of having to enter a Chinese ID number.

Chinese companies have rushed to announce generative AI projects since OpenAI’s ChatGPT surged in popularity worldwide earlier this year. ChatGPT isn’t officially allowed in China, where access to Google and Facebook is blocked.

Despite that level of control, China’s top leaders have made high-profile comments about the need to develop domestic technology, with specific mention of artificial intelligence.

On Aug. 15, China’s “interim regulation” for the management of generative AI services took effect.

The rules said they would not apply to companies developing the AI tech as long as the product was not available to the mass public. That’s more relaxed than a draft released in April that said forthcoming rules would apply even at the research stage.

The latest version of the rules also did not include a blanket license requirement, only saying that one was needed if stipulated by law and regulations. It did not specify which ones.

China has generally increased regulation on personal data protection and network security.

During an earnings call last week, Baidu CEO Robin Li called the new rules “more pro-innovation than regulation” and said the company was “quite optimistic about the future for a better regulatory environment.”

At the time, Li said the company was “still waiting for the green light for large-scale rollout of Ernie bot for use in consumer facing apps.”

Other Chinese companies, including Alibaba, have been releasing a slew of generative AI products.

Last week, Opera web browser parent Kunlun Tech released to the public an AI-powered chatbot and search engine called Tiangong AI search. The company compared it to Microsoft Bing’s integration with OpenAI, since Tiangong also provides internet links with its results.

Previously, the majority of such AI products in China were only available for corporate partners’ internal use.

It is not clear how the chatbots’ underlying technology compare with ChatGPT’s. Basic functionality is generally the same, although Ernie bot and Tiangong primarily operate in Chinese. Both have standalone iPhone apps.

ChatGPT’s popularity started to wane in June, despite the launch of an iPhone app in May, according to a Bank of America report.

— CNBC’s Kif Leswing contributed to this report.

https://www.aier.org/article/against-a-3-percent-inflation-target/

Against a 3 Percent Inflation Target

The aimless drift of economic policy continues, as otherwise sensible economists push for the Federal Reserve to raise its inflation target to 3 percent. This will supposedly provide all the benefits of the Fed’s current 2 percent target without incurring the costs (reduced growth, higher unemployment) of driving inflation down further. Even apart from the naive Keynesianism implied in this view, there are still several problems, any one of which sinks the argument for a higher target.

There are welfare costs to higher inflation. When the dollar depreciates faster, people try to reduce their cash holdings. But economizing on liquidity is itself costly. As Milton Friedman argued, it results in fewer transactions and, correspondingly, fewer gains from trade. The cost incurred by each of us is very small. Multiply it by 330 million, however, and it doesn’t look so trivial.

The second cost, related to the first, stems from the redistributive nature of the policy change. Think about the millions of people with long-term debt contracts, such as banks and mortgage-holders. Raising the inflation target redistributes wealth from creditors to debtors. The longer the duration of the debt contract, the greater the transfer. By itself, a transfer of resources is neither a cost nor a benefit to society. The problem is all the resources people would use up to minimize the damage to their own net worths, as well as precautionary actions taken to avoid similar redistributions in the future. We already spend far too much time, money, and effort watching the Fed. Raising the inflation target would waste even more.

The third cost is significantly larger than the first two. Many tax rates are not indexed to inflation. Capital gains taxes, for example, are denominated in nominal dollars. Higher inflation means higher asset values, which will push owners of capital into higher tax brackets. Even if real asset values are decreasing, owners of capital will have to pay greater taxes on nominal price increases. This creates strong disincentives to invest, and hence create additional wealth. Furthermore, since it means Uncle Sam’s share of the economic pie will increase in real (inflation-adjusted) terms, more wealth will be allocated to fundamentally unproductive uses. This is a needless drag on growth.

But the largest cost to a 3 percent inflation target is diminished Fed credibility. The central bank would essentially admit to markets that it is unwilling to do the hard work to return inflation to its previously adopted target. That would tarnish the Fed’s reputation. If the central bank can’t be trusted to hit a 2 percent target, why is a 3 percent target any more believable? After the next crisis—and given how bad the Fed is at its job, there will certainly be one—will the Fed acquiesce to a 3.5 percent or 4 percent target? What about the crisis after that? There’s no end to this ratchet. The Fed’s hard-won reputation as a guarantor of nominal stability would be lost, perhaps forever.

There is no good reason to accept a higher inflation target. All the arguments for it rely on dark-age macroeconomics, which should have stayed buried with the stagflation of the 1970’s. If the Fed can really make such an elementary error and get away with it, a major prudential reason for keeping it around would no longer hold. A Fed that willingly accedes to the dollar-depreciation racket is too dangerous to keep around.

Apple, Google, Nvidia and other tech giants are considering buying Arm shares

PUBLISHED TUE, SEP 5 20233:06 PM EDTUPDATED 4 HOURS AGO

KEY POINTS

- Nvidia CEO Jensen Huang had positive things to say about Arm in the chip-design company’s digital roadshow.

- The comments come after Nvidia dropped a plan to buy Arm as regulators said the deal could hurt competition.

Chip design firm Arm said in a Tuesday filing that Apple, Google parent Alphabet, Nvidia and other technology companies are interested in buying up to $735 million in its shares as it seeks to go public on Nasdaq.

The investments might not happen, but the fact that these companies are considering them underlines the importance of Arm, whose designs are used for processors in data center servers, consumer devices and industrial products.

Chip foundry operators Intel, Samsung and TSMC are interested in investing alongside the three trillion-dollar technology companies, along with AMD and MediaTek, which make chip designs based on Arm architectures. Cadence Design Systems and Synopsys, which make electronic design automation software for processor development, have also expressed interest, according to a revised prospectus for Arm’s shares sale. As part of the deal, Arm could wind up with a $52 billion market capitalization and almost $5 billion in new cash.

Initial public offerings in technology have been rare in the past two years, with higher interest rates making investors less willing to place bets on risky high-growth companies. Arm, established in 1990, is different. It was listed in London and New York before SoftBank bought it for $32 billion in 2016. It produced a $105 million profit on $675 million in revenue in the second quarter.

In 2020, Nvidia announced plans to acquire Arm from SoftBank for $40 billion, but regulators in the U.S. and the U.K. pushed back. The two companies dropped the transaction in 2022, paving the way for Arm’s current U.S. IPO. Nvidia has introduced its own Arm-based chip that can work alongside its own graphics processing units.

The fact that Nvidia wasn’t able to buy Arm didn’t stop Nvidia’s co-founder and CEO Jensen Huang from talking up Arm during the chip-design company’s IPO roadshow.

“Arm is an extraordinary company, and everybody in the world knows how fond I am of this company and of this platform and this franchise and world-class management team,” Huang said in his signature leather jacket during the prerecorded roadshow video.

Nvidia is collaborating with Arm on a new cloud data center ecosystem, Huang said. Historically, Intel chips have dominated in data center servers.

Huang isn’t Arm’s only external promoter. Rick Tsai, vice chairman and CEO of MediaTek, appeared during Arm’s virtual roadshow, saying more products drawing on the two companies’ products will appear over time.