HI Market View Commentary 06-12-2023

What’s happening this week in the stock market?

FOMC Rate Hike meeting = +0.25

Key word to continue our new bull run ?= Pause

What do you think the pros are saying ? Waffling They don’t know, can’t predict the future and no algorithm is helping them

Kohler – Need to have protection = AAPL ATM $180, $170

Meta = $250, $265

F – 13.50

BIDU = 125

GOOGL ITM 125 Short Calls

We are mostly NON – DIRECTIONAL = We make money either way

Leaning Bullish

Our market gains are mostly from 7 stocks and we have a ton of others waiting to head higher

The Start of a Bull Market Is Good News. Expect This Next.

At long last, the S&P 500 pulled out of the lengthiest bear market since 1948.

That’s a relief, but what’s more likely to happen next–could it be a new record high for the index, which would mean another 10% leg higher to a level last seen on Jan. 3, 2022? Or another 20% retreat into a new bear market?

Here’s the bear case: The S&P’s gains have been carried by just seven technology companies. That’s coming to be known as a skinny bull market, and it wouldn’t take much to drag those few names down to undermine the advance.

The Federal Reserve, once thought to be delivering interest-rate cuts by the end of the year, now looks like it will just take a break next week and then keep hiking. Inflation is still too hot, and the labor market is still too tight for the Fed to consider easing. The sluggish rise of stocks since October is set to remain tepid at best.

Here’s the bull case: Because the S&P’s gains have been driven by so few stocks that leaves plenty of room for the rest of the index to catch up, as if they’re attached by a rubber band, and that will fatten up the bull market the rest of the year.

Sure, the Fed may still be hiking, but most of that information is already priced into stocks. Unemployment remains historically low, and price gains are slowing–more data are due on Tuesday. Overall, the economy has managed to fend off a recession for much longer than many had imagined, despite the worst inflation and most aggressive rate hikes in 40 years.

So decide for yourself. The beauty of the skinny bull is in the eye of the beholder.

*** Join Penta senior writer Abby Schultz today at noon when she talks to Sara Naison-Tarjano, global head of Goldman Sachs Apex and private wealth management capital markets, about how the world’s wealthiest families invest based on results from a recent survey of family offices worldwide

https://www.briefing.com/the-big-picture

The Big Picture

Last Updated: 09-Jun-23 10:45 ET | Archive

Fed and economy are engaged in a tough squash match

The Conference Board’s Leading Economic Index declined 0.6% in April, marking the 13th consecutive decline in that series, and signaling, according to the Conference Board, a worsening economic outlook. The Conference Board’s Consumer Confidence Index for May featured an Expectations Index that slipped to 71.5, continuing a string of sub-80.0 readings in every month since February 2022, except for December 2022. A reading below 80.0, the Conference Board says, is associated with a recession in the next year.

The PCE Price Index increased to 4.4% year-over-year in April from 4.2% in March. The core-PCE Price Index, which excludes food and energy, increased to 4.7% year-over-year from 4.6%. That is the Fed’s preferred inflation gauge, and it is moving in the wrong direction.

The Consumer Price Index, for added measure, showed total CPI up 4.9% year-over-year, versus 5.0% in March, and core CPI up 5.5% year-over-year, versus 5.6% in March. Clearly, CPI moved in the right direction, yet that did not excuse the fact that consumer inflation is still too high — certainly relative to the Fed’s 2.0% inflation target.

Hard Landing or Soft Landing?

It will surprise no one to hear that recession concerns are part of the market narrative, but to be fair, there has been some burgeoning optimism that a hard landing for the U.S. economy can be avoided. That optimism has been rooted in the ongoing strength of the labor market.

No one, however, is really looking for a boom in economic activity. The choice is between a hard landing and a soft landing. The latter is winning out these days in the stock market, which is trading at its best levels since last August but still adhering to a 13-month trading range.

A word that has been creeping into the market narrative, however, is stagflation. That term is used to describe a period when high unemployment and stagnant demand is accompanied by high inflation.

We have high inflation now and we are hearing increasingly that demand is moderating due to macro pressures, but we do not have a high unemployment rate. Granted the May unemployment rate moved to 3.7% from 3.4% in April, but 3.7% isn’t high. In the recessions seen since 1980, the average unemployment rate has ranged from 4.8% to 9.0%.

The Fed, of course, seems wedded to the idea that a further softening in the labor market is needed to help bring inflation back down to its target rate on a sustainable basis. That would suggest the Fed is not done raising rates given the resilience of the labor market or, at the least, won’t be cutting rates anytime soon as it waits on the lag effect of prior rate hikes to squash demand and the labor market.

Home on the Range

Like the stock market, the Treasury market has also been locked in a trading range for the past nine months, tossing and turning on inflation data, rate hike expectations, a mini banking crisis, debt ceiling uncertainty, and fickle economic views.

Treasury yields today are a far cry from where they were only 15 months ago when the Fed started raising its target range for the fed funds rate from 0.00-0.25%. Today, the target range is 5.00-5.25%. The fed funds futures market is not expecting a rate hike at the June FOMC meeting, yet that view could be subject to quick change pending the June 13 release of the May Consumer Price Index. In any case, there is currently a 67.0% probability of a 25-basis points rate hike at the July FOMC meeting.

What It All Means

The question of course is, will prior rate hikes end up squashing demand that, in turn, squashes the labor market and inflation? Or will prior rate hikes squash demand while structural forces lead to continued strength in the labor market and the persistence of high inflation?

The answer will reverberate across capital markets, but if the Fed finds reason to stay higher for longer with its policy rate, then Treasury yields will be poised to stay higher for longer, respecting their current trading ranges or something worse that will remain a competitive headwind for stocks.

—Patrick J. O’Hare, Briefing.com

Where will our markets end this week?

Higher

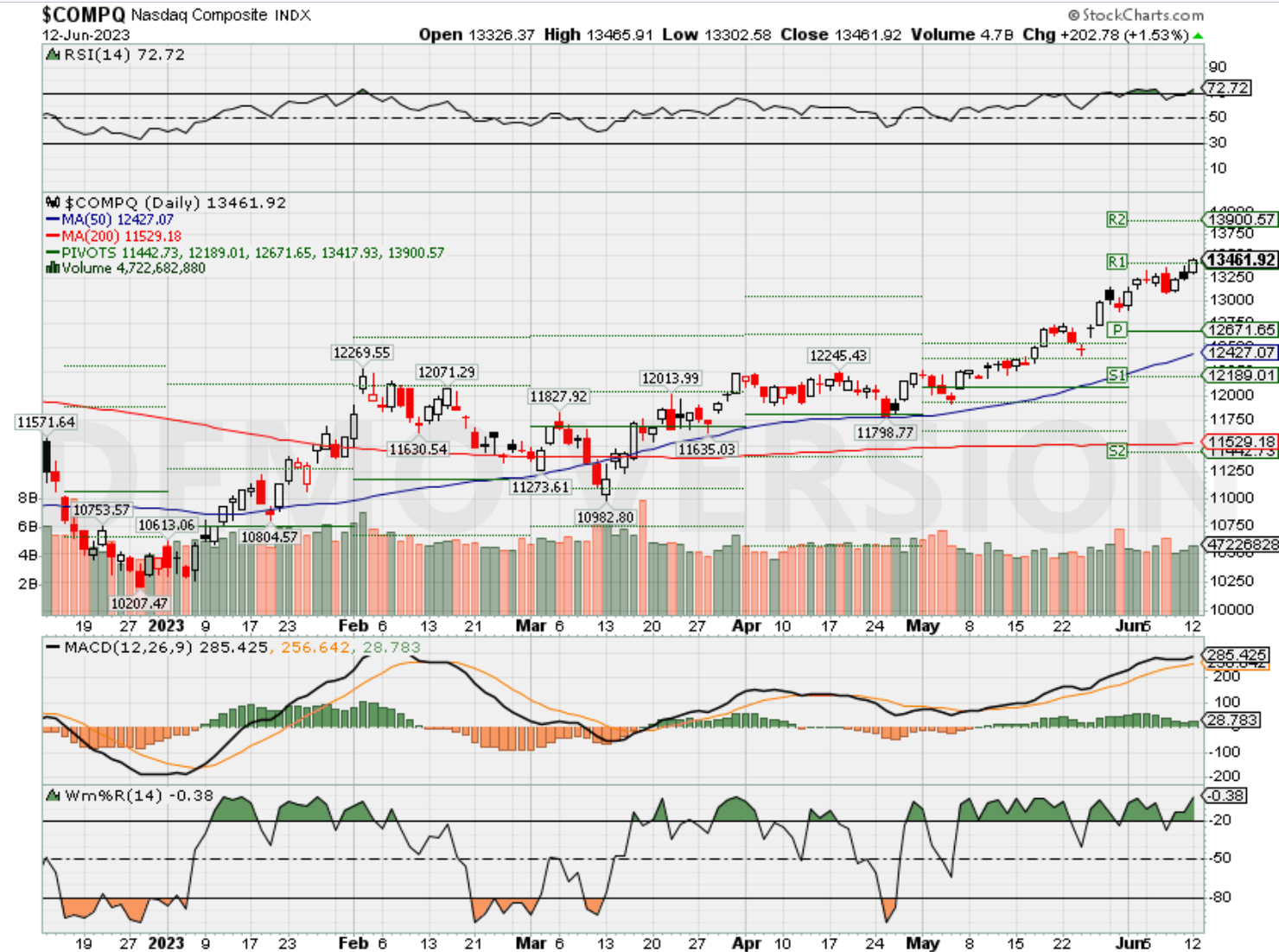

DJIA – Bullish

SPX –Bullish

COMP – Bullish

Where Will the SPX end June 2023?

06-12-2023 +2.0%

06-04-2023 +2.0%

Earnings:

Mon: ORCL

Tues:

Wed: LEN

Thur: JBL, KR, ADBE

Fri:

Econ Reports:

Mon: Treasury Budget

Tue CPI, Core CPI

Wed: MBA, PPI, Core PPI, FOMC Rate Decision

Thur: Initial Claims, Continuing Claims, Empire Manufacturing, Phil Fed, Retail Sales, Retail ex-auto, Capacity Utilization, Business Inventory, Industrial Production, Net TIC Flows

Fri: Michigan Sentiment

How am I looking to trade?

Protection is on but for some stocks protection is at a lower price than where the stocks are currently trading at

www.myhurleyinvestment.com = Blogsite

info@hurleyinvestments.com = Email

Questions???

Cathie Wood’s Ark Invest misses out on Nvidia’s powerful rally — dumped stock too early, citing high valuation

PUBLISHED TUE, MAY 30 202311:06 AM EDTUPDATED TUE, MAY 30 20231:55 PM EDT

In this article

Cathie Wood, CEO of Ark Invest, speaks during an interview on CNBC on the floor of the New York Stock Exchange (NYSE) in New York City, February 27, 2023.

Brendan McDermid | Reuters

Ark Invest’s Cathie Wood, known for her investments in next-generation technologies, missed out on the jaw-dropping rally in Nvidia — the biggest winner in artificial intelligence this year.

Her flagship Ark Innovation ETF (ARKK) exited Nvidia entirely in early January, before the chipmaker went on to enjoy a powerful rally that propelled it to a $1 trillion market capitalization.

She even trimmed Nvidia holdings in her smaller funds on Thursday when the stock spiked 26% on a huge forecast beat driven by AI chip demand. The ARK Autonomous Tech. & Robotics ETF (ARKQ) now has 4.4% in Nvidia, while its biggest holding is Tesla with a 14% weighting. ARKK and ARKQ are up 8.9% and 5.8% this month, respectively, compared to Nvidia’s 40% gain.

Wood revealed that her reason for dumping Nvidia was its high valuation. Typically though, growth investors like Wood aren’t fazed by how expensive a stock is.

“At 25x expected revenue for this year, however, $NVDA is priced ahead of the curve,” she said in a Twitter post on Monday.

Meanwhile, ARKK doesn’t own any of the semiconductor names and other AI-related stocks that had a big move up recently alongside Nvidia, including AMD, Taiwan Semiconductor or C3.ai.

“Active management seeks to find potential winners but can often miss out with security-selection decisions,” said Todd Rosenbluth, head of research at VettaFi. “This is why some investors are turning to broad-based thematic index ETF strategies.”

Rosenbluth said Global X Artificial Intelligence & Technology ETF (AIQ), iShares Robotics and Artificial Intel Multisector ETF (IRBO), and ROBO Global Artificial Intelligence ETF (THNQ) are three AI-focused exchange-traded funds that have benefited from owning Nvidia.

AI winners elsewhere?

Wood said she believes better opportunities to ride the AI boom are elsewhere. She called Tesla “the most obvious beneficiary of the recent breakthroughs in AI.”

The innovation investor said the Elon Musk-led electric vehicle company is trading at six times revenue. She said she’s betting on its autonomous-driving ambitions as Tesla aims for a total addressable market of $8 trillion to $10 trillion in revenue in self-driving mobility by 2030.

Wood previously said biotech firm Exact Sciences, ARKK’s seventh-biggest holding, is also a leader in AI in terms of its data on cancer and its molecular diagnostic-testing franchise.

In its base case, Ark believes Exact Sciences could compound at an average annual rate of 25%, reaching $140 by 2027. The stock traded around $83 a share on Tuesday.

https://www.cnbc.com/2023/06/04/spider-man-across-the-spider-verse-domestic-box-office-opening-.html

Spider-Man: Across the Spider-Verse’ opens to $120.5 million, second-highest debut of 2023

PUBLISHED SUN, JUN 4 202311:46 AM EDT

KEY POINTS

- Sony’s “Spider-Man: Across the Spider-Verse” opened to $120.5 million at the domestic box office this weekend.

- It was the second-biggest opening of 2023, just behind Universal’s “Super Mario Bros. Movie.”

- The film also marks the third-best opening weekend for any Spider-Man film, animated or live-action.

Still from Sony’s “Spider-Man: Across the Spider-Verse.”

Sony

Spider-Man returned to the big screen this weekend, webbing up an estimated $120.5 million at the domestic box office.

Sony’s “Spider-Man: Across the Spider-Verse,” the much anticipated sequel to the Academy Award-winning “Spider-Man: Into the Spider-Verse,” had the second-biggest opening of 2023, just behind Universal’s “Super Mario Bros. Movie.”

The film also marks the third-best opening weekend for any Spider-Man film, animated or live-action.

“As a PG animated film, ‘Across The Spider-Verse’ is able to capture a younger audience beyond the core fans of the live action PG-13 films and thus ensures the long-term cross-generational appeal of the character and the movies,” said Paul Dergarabedian, senior media analyst at Comscore. “This is money in the bank for the studio and movie theaters.”

“Across the Spider-Verse” is estimated to have pulled in more than 9 million moviegoers over the weekend, according to data from EntTelligence. Tickets for the film represent around 56% of all foot traffic to theaters from Thursday through Sunday, the data firm reported.

Additionally, 29% of patrons saw the film in a premium format, paying an average of $4.52 more per ticket.

“This debut is further proof that audiences are eager for fresh, edgy takes on both superhero and animated movies,” said Shawn Robbins, chief analyst at BoxOffice.com.

Sony’s animated Spider-Man sequel arrives on the heels of several strong box office openings, including Disney and Marvel’s “Guardians of the Galaxy: Vol. 3” and Disney’s “The Little Mermaid.”

With another $10.2 million in ticket sales during its fifth weekend in theaters, “Guardians of the Galaxy: Vol 3” has generated around $322.7 million domestically. The film has tallied $780.1 million globally.

“The Little Mermaid” saw a 58% drop in ticket sales from its first weekend to its second, on par with industry averages, adding $40.6 million to its cumulative global take. The film has secured $186.2 million in domestic ticket sales and stands at $326.7 million globally.

Additionally, Disney’s “The Boogey Man” opened to $12 million in domestic ticket sales and Universal’s “Fast X” added $9.24 million in ticket sales over the weekend, bringing its domestic haul to $128.4 million.

At present, the year-to-date domestic box office tally stands at around $3.6 billion, just 21.9% behind prepandemic levels, according to data from Comscore. The 2023 box office so far this year is 27.9% above the same period in 2022.

“Between Spidey’s big start, ‘Little Mermaid’s’ strong hold, ‘Boogeyman’s’ horror offering, the holdover prowess of ‘Guardians’ and ‘Fast X,’ and plenty more to come, theater owners, studios, and audiences are now heading full throttle into the most exciting summer market in four years,” Robbins said.

Disclosure: Comcast is the parent company of NBCUniversal and CNBC. NBCUniversal distributed “The Super Mario Bros. Movie” and “Fast X.”

https://www.cnbc.com/2023/06/08/stock-market-today-live-updates.html

S&P 500 notches fourth straight positive week, touches highest level since August: Live updates

The S&P 500 rose slightly Friday, touching the 4,300 level for the first time since August 2022 as investors looked ahead to upcoming inflation data and the Federal Reserve’s latest policy announcement.

The broad-market index gained 0.11%, closing at 4,298.86. The Nasdaq Composite rose 0.16% to end at 13,259.14. The Dow Jones Industrial Average traded up 43.17 points, or 0.13%, closing at 33,876.78. It was the 30-stock Dow’s fourth consecutive positive day.

CNBC

For the week, the S&P 500 was up 0.39%. This was the broad-market index’s fourth straight winning week — a feat it last accomplished in August. The Nasdaq was up about 0.14%, posting its seventh straight winning week — its first streak of that length since November 2019. The Dow advanced 0.34%.

Investors were encouraged by signs that a broader swath of stocks, including small-cap equities, was participating in the recent rally. The Russell 2000 was down slightly on the day, but notched a weekly gain of 1.9%.

“It’s the first time in a while where investors seem to be feeling a greater sense of certainty. And we think that’s been a turning point from what had been more of a bearish cautious sentiment,” said Greg Bassuk, CEO at AXS Investments.

“We think that as we walk through these next few weeks, that will be increasingly clear that the economy is more resilient than folks have given it credit for the last six months,” said Scott Ladner, chief investment officer at Horizon Investments. “That will sort of dawn on people that small-caps and cyclicals probably have a reasonable shot to play catch up.”

The market is also looking toward next week’s consumer price index numbers and the Federal Open Market Committee meeting. Markets are currently anticipating a more than 71% probability the central bank will pause on rate hikes at the June meeting, according to the CME FedWatch Tool.

7 Companies Are Dominating the Stock Market. Meet the ‘Skinny Bull.’ | Barron’s (barrons.com)

7 Companies Are Dominating the Stock Market. Meet the ‘Skinny Bull.’

By Allan Sloan

Updated June 7, 2023 4:59 pm ET / Original June 7, 2023 1:57 pm ET

The Barron’s Daily

A morning briefing on what you need to know in the day ahead, including exclusive commentary from Barron’s and MarketWatch writers.

I would also like to receive updates and special offers from Dow Jones and affiliates. I can unsubscribe at any time.

I agree to the Privacy Policy and Cookie Policy.

Seven companies account for 98% of the return of the FT Wilshire 5000 Index.

Michael M. Santiago/Getty Images

About the author: Allan Sloan is an independent business journalist and seven-time winner of the Loeb Award, business journalism’s highest honor.

We seem to be in a bull market or about to enter one. But boy, this is one of the skinniest bulls ever, with a mere seven companies (and a total of eight stocks) accounting for more than the entire 9.65% total return (including price gains and reinvested dividends) that the S&P 500 had for the first five months of the year. That’s an annualized return of more than 23%, which is very nice.

But without the Select Seven, the S&P is down slightly for the first five months.

And wait, there’s more. As you can see from the table below, those seven companies represent an astounding 98% of this year’s return for the entire 3,480-company U.S. stock market, as measured by the FT Wilshire 5000 Index .

The Skinny Bull

Just seven companies produced 98% of the FT Wilshire 5000’s return.

| Stock | Wilshire Market Weight | Return Contribution |

| Apple | 6.88% | 2.04% |

| Microsoft | 5.88% | 1.76% |

| Nvidia | 2.19% | 1.48% |

| Alphabet* | 3.37% | 1.04% |

| Amazon | 2.67% | 0.88% |

| Meta | 1.45% | 0.87% |

| Tesla | 1.35% | 0.57% |

| Total | 23.79% | 8.64% |

| Wilshire Total | 100% | 8.84% |

Note: Alphabet includes A and C stock combined. Returns through May 31, 2023.

Source: Wilshire Indexes

I’m using the Wilshire because it’s a much bigger, much broader indicator than the S&P. And it gets a lot less attention because unlike the S&P, the Wilshire doesn’t have trillions of dollars indexed to it.

That 98% piece of the return is more than four times the companies’ combined month-end index weight of a bit under 24%.

And get this: in May, Nvidia (ticker: NVDA), whose month-end weight was a mere 2.19% of the index, accounted for more than the index’s entire gain. According to statistics that I got from Wilshire Indexes, Nvidia’s 36% May return boosted the Wilshire by 0.59%, which exceeded the index’s 0.43% return for the month.

What on earth is going on here? And how can we cope with it?

In search of wisdom and a bit of context, I talked and emailed with Philip Lawlor, Wilshire’s managing director for market research. I asked Lawlor, who has more than 30 years of experience as an investment strategist and a money manager, what investors can do about the fact that the market’s substantial gains are so narrowly focused.

The problem, of course, is that with so few stocks accounting for so much of a substantial gain, it’s easy to miss out even if you put your money into this year’s hot areas: digital information and services, and technology. These areas had returns of 31.9% and 39.6%, respectively, for the first five months of the year, about four times the Wilshire’s 8.84% return.

“You could have backed the wrong horses even if you picked the right sector,” Lawlor told me.

That makes things especially difficult for active money managers, whose goal is to pick individual stocks that allow them to beat the market. Miss out on Nvidia—this year’s scorching hot stock, which returned 159% through May and kept rising in June when last I looked—and your portfolio is almost sure to have a below-market return.

But for those of us who are retail investors, there are other approaches than hoping that we don’t miss picking the market’s hotties du jour.

If broad-based index funds (my biggest personal equity investments) bore you but this year’s hot market sectors intrigue you, Lawlor says that you can buy into technology or semiconductor exchange traded funds.

Please note that Lawlor isn’t advising you to do that—he’s just offering you options.

With a sector ETF, you can get a piece of stocks like Apple (AAPL), Microsoft (MSFT), and Nvidia, the three hottest big stocks for the year through May, along with other stocks like Amazon (AMZN), Meta (META)(formerly Facebook), and Alphabet (GOOGL) (formerly Google) that could become this week’s hotties. If you pick the right ETF, you might find one that also has Tesla (TSLA), another of our Select Seven companies.

By going the ETF route, Lawlor says, “you don’t have to cherry pick individual stocks.”

Sure, buying sector ETFs isn’t as much fun as hitting a grand slam with Nvidia. But it reduces the chances of getting your head handed to you if the market suddenly sours on Nvidia. Its earnings have been soaring thanks to its huge share of the market for chips that power artificial intelligence applications.

If the rapid rise of a handful of enormous stocks reminds you of the 1999-2000 Internet bubble, you’re not alone.

At the peak of the bubble in March of 2000, Lawlor says, the 10 biggest stocks accounted for 20.3% of the Wilshire. As of May 31, the Top Ten accounted for 25.9% of the index. That’s a serious concentration.

I don’t know if the Skinny Bull Market will flesh out, or whether it will get even skinnier. It’s going to be a lot of fun to watch. But it won’t be a lot of fun if you decide to go all in and don’t have the emotional or financial staying power you’ll need if the Skinny Bull morphs into a Big Bad Bear.

So enjoy the bull run. But remember that in the financial markets, nothing lasts forever.

Guest commentaries like this one are written by authors outside the Barron’s and MarketWatch newsroom. They reflect the perspective and opinions of the authors. Submit commentary proposals and other feedback to ideas@barrons.com.