HI Market View Commentary 02-21-2023

What about BIDU?= Google of China, with 6 other profit legs

1st We are in BIDU because of long standing track record of making money.

2nd It diversifies our portfolios to the second largest economy in the world

Earnings are tomorrow morning before the market opens.

There huge pent up demand of money to be spent in China

We seem to be cash heavy – Because we are making profit on puts (stock ownership insurance)

WE ARE NOT adding more shares until we feel like we have a bottom

Earnings dates:

BIDU – 2/22 BMO

MU – 3/29

SQ – 2/23 AMC

https://www.briefing.com/the-big-picture

The Big Picture

Last Updated: 17-Feb-23 15:36 ET | Archive

Second half earnings estimates at risk (along with the economy)

The fourth quarter earnings reporting period is not over yet, but it is mostly over. More than 80% of S&P 500 companies have reported their results. In aggregate, they have been about as weak as expected, which, in reality, means they have been worse than expected.

When we provided an earnings preview on January 12, we noted that S&P 500 earnings for the fourth quarter, as of January 6, were expected to decline 4.1% year-over-year, according to FactSet. At the time, we also added that the blended earnings growth rate, which accounts for companies that have reported actual results and estimates for companies that have yet to report, stood at -4.8%.

Today, the blended earnings growth rate stands at… -4.8%.

The recognition that the blended growth rate hasn’t deteriorated further might be seen by some as cause for celebration, but knowing that a typical reporting period often sees the final earnings growth rate come in two to four percentage points higher than the estimate at the start of the reporting period, we can call this reporting period a disappointment so far.

That isn’t a genuine surprise to us. What is a genuine surprise to us are the forecasts for earnings growth in the second half of the year that are accented with a hockey-stick like ramp for the fourth quarter.

Surprise! Surprise! Surprise!

Frankly, we have been surprised by a lot to begin the year.

- The stock market has done far better than we expected.

- The economy, so far, is holding up better than we thought.

- China ended its zero-COVID policy.

- Natural gas prices have collapsed.

- The lowest-quality stocks, generally speaking, have shown the biggest gains.

- Growth stocks have vastly outperformed value stocks.

- The stock market has been convincing itself that the Fed will cut rates before the end of the year.

We come back to earnings estimates, however, because they are the basis for why we are surprised the stock market has done so well. The gist of the matter is that stock prices have rallied while earnings estimates have been cut.

As of this writing, the S&P 500 is up 6.2% for the year. It had been up as much as 9.3% at its high on February 2 (i.e., the day before the much stronger than expected January employment report). Since the start of the year, the forward twelve-month earnings estimate has dropped from $229.38 to $225.62, according to FactSet.

We would be remiss not to add that the forward twelve-month earnings estimate has increased from $225.37 on February 3 (i.e. the day of the much stronger than expected January employment report) to $225.62. That welcome turn has coincided with some generally pleasing earnings reports and economic data that have bolstered expectations for a soft landing — or what some proclaim as “no landing” — for the economy.

On a related note, the Atlanta Fed’s GDPNow initial Q1 real GDP forecast provided on January 27 was 0.7%. It went to 2.1% after the employment report, and following this week’s data it now stands at 2.5%. That is a long way from a recession.

It’s a Second Half Thing

If there is going to be a recession, a growing number of economists now think it will unfold in the second half of 2023. The following assumptions are contributing to that view:

- The long and variable lags of the Fed’s rate hikes (and rate hikes by other central banks) will start to be felt more acutely in the second half of the year.

- Consumer spending will weaken with rising unemployment and the resumption of student loan payments.

- Repayment burdens for variable rate debt will command a larger share of disposable income due to continued rate hikes by the Fed.

- Personal savings, as a percentage of disposable personal income, are at depressed levels, which will detract from spending potential as concerns about job security/job losses increase.

These are reasonable assumptions in the face of a Federal Reserve that sounds adamant about continuing to raise rates and keeping rates at higher levels for longer to ensure inflation comes back down to its 2.0% target and stays there.

At the moment, though, the consensus EPS growth estimates for the second half of the year are not in sync with views that the economy will be in recession in the second half of the year.

According to FactSet, analysts expected S&P 500 earnings to be up 3.3% in third quarter and up 9.7% in the fourth quarter. The expected ramp in the fourth quarter is typical — not from a seasonal standpoint but from a forecasting standpoint. The outlook is always brighter 6-12 months down the road.

Granted this fourth quarter reporting period is providing an easier comparison, but frankly, the U.S. economy has yet to show any real fractures because the labor market has remained as strong as it has. The Fed, of course, sees a weaker labor market as a solution to its inflation problem, meaning it is apt to keep tightening the policy screws until it is confident the labor market has loosened adequately enough to keep inflation under control.

With a 3.4% unemployment rate, there is a lot of loosening ground that still needs to be traveled.

What It All Means

Maybe, then, the earnings forecasts for the first half of 2023 are too pessimistic.

Analysts currently expect first quarter earnings to decline 5.4% and second quarter earnings to decline 3.4%. It is still a big leap, though, to get to earnings growth in either period, knowing that earnings were up 9.5% in the first quarter of 2022 and up 6.2% in the second quarter.

It is a bigger leap in our estimation, however, to deliver on the type of earnings growth projected for the second half of 2023 when the weight of the Fed’s rate hikes should be pressing more on economic activity.

To be fair, analysts aren’t accounting for much earnings growth overall in 2023. The current estimate, according to FactSet, projects just 2.3% growth over 2022, which is down from 5.0% at the start of the year.

That forecast incorporates a hockey-stick like ramp in the fourth quarter growth estimate, which is ambitious indeed for an economy that should be weakening, not strengthening, in the months ahead. The degree to which it weakens is the great unknown, but under the Fed’s watch, weaken it will.

Although the forward twelve-month estimate has come up a bit in recent weeks, we remain unconvinced that the earnings estimate trend has bottomed because it is abundantly clear that the Fed’s rate hikes haven’t topped and won’t roll over soon when they do, barring some shock to the economy that would be even worse for earnings prospects.

—Patrick J. O’Hare, Briefing.com

https://go.ycharts.com/weekly-pulse

| Market Recap |

| WEEK OF FEB. 13 THROUGH FEB. 17, 2023 |

| The S&P 500 index fell 0.3% last week amid worries that further monetary tightening might be needed to keep inflation in check after January producer prices came in higher than expected.

The market benchmark ended Friday’s session at 4,079.09, down from last week’s closing level of 4,090.46. The index is almost flat for the month with a February-to-date gain of almost 0.1%. It’s up 6.2% for the year to date. The slim movement for the week came as data showed the producer price index rose 0.7% last month, surpassing the consensus estimate according to Econoday for a 0.4% increase. On an annual basis, the PPI advanced 6%, which was higher than analysts’ consensus estimate for 5.5% growth, but down from December’s 6.5% pace. The higher-than-expected producer prices were unwelcome news for investors who’ve been hoping for inflation to ease enough for the Federal Reserve’s policy-setting committee to slow down its rate increases. Adding to the concerns, Cleveland Fed President Loretta Mester said last week that the risks of inflation accelerating are still tilted to the upside and will require further monetary policy tightening. The impact of the rate increases was evident in January housing data released last week as housing starts fell more than expected in January amid elevated mortgage rates. The energy sector — which had been the only gainer last week — led last week’s decliners with a 6.9% drop. Other decliners included real estate, down 1.4%, and materials, down 1.1%. The health care, technology and financial sectors also fell slightly. The gainers were led by consumer discretionary, which rose 1.6%, followed by gains of 0.9% each in utilities and consumer staples. Other gainers included industrials and communication services. The energy sector’s drop came as crude oil futures and natural gas futures also fell. The decliners included shares of Devon Energy (DVN), which issued an outlook that RBC described as softer than expected. Devon also declared a quarterly dividend that RBC said was below its expectation. Shares fell 16% on the week. In real estate, shares of Host Hotels & Resorts (HST) fell 6.8% as the lodging real estate investment trust reported Q4 results above analysts’ mean estimates but forecast 2023 adjusted funds from operations below analysts’ consensus view at the time. The REIT also forecast 2023 earnings per share below analysts’ mean estimate at the time. The consumer discretionary sector’s gainers included Aptiv (APTV), which received higher price targets from analysts at a number of firms, including RBC Capital Markets, which cited a stronger margin outlook. Shares of Aptiv rose 6.1%. In utilities, shares of Exelon (EXC) rose 5.7% as the company reported Q4 adjusted earnings per share and revenue above year-earlier results. The adjusted EPS matched the Street consensus estimate while revenue surpassed the Street view. Exelon also issued a guidance range for 2023 adjusted operating EPS that bracketed the Street view. In addition, the company boosted its quarterly dividend rate. Next week’s earnings calendar will feature retailers including Walmart (WMT), Home Depot (HD) and TJX (TJX) as well as other companies such as Medtronic (MDT), NVIDIA (NVDA) and Intuit (INTU). The market will be closed on Monday for the Presidents Day holiday in the US. Economic reports expected in the rest of the week include January existing and new home sales, Q4 gross domestic product, January consumer spending and January personal consumption expenditures. Provided by MT Newswires |

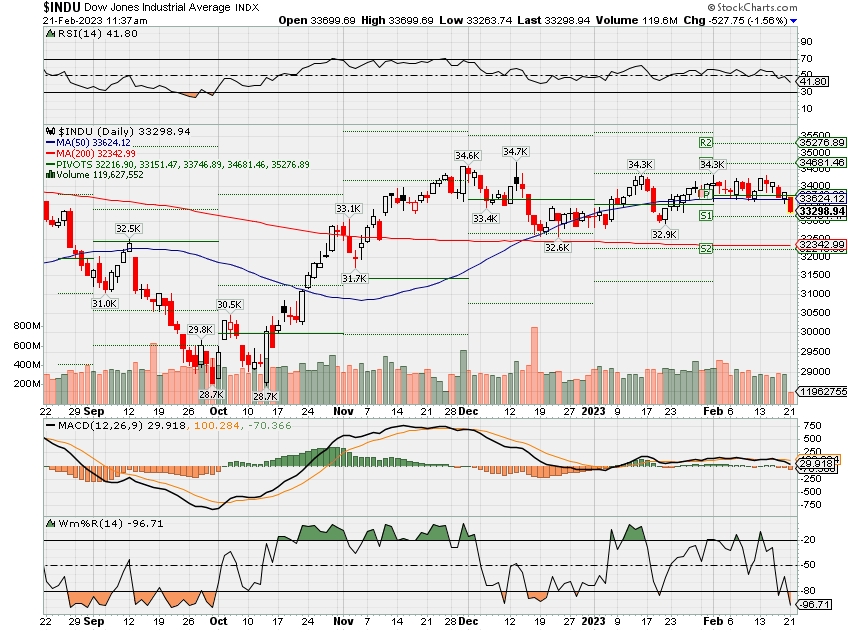

Where will our markets end this week?

Lower

DJIA – Bearish

SPX –Bearish

COMP – Bullish

Where Will the SPX end February 2023?

02-20-2023 +0.0

02-13-2023 +2.0

02-06-2023 +2.0

Earnings:

Mon:

Tues: FLR, HD, TAP, WMT, CHK, COIN, FLS, PANW, TOL, RIG

Wed: GRMN, TSA, EBAY, IMAX, MOS, VMI, BIDU, NVDA

Thur: LNG, DDS, KDP, NTES, NEM, PZZA, BYND, INTU, LZ, SQ, BABA

Fri: CNK

Econ Reports:

Mon: PRESIDENTS DAY HOLIDAY

Tue Existing Home Sales

Wed: MBA, FOMC Minutes

Thur: Initial Claims, Continuing Claims, GDP, GDP Deflator

Fri: PCE Prices, Personal Income, Personal Spending, New Home Sales, Michigan Sentiment

How am I looking to trade?

Currently running mostly stocks with protection

BIDU & SQ Earnings next week

Monday Holiday

www.myhurleyinvestment.com = Blogsite

info@hurleyinvestments.com = Email

Questions???

Another ‘Volmageddon’? JPMorgan becomes the latest to warn about an increasingly popular short-term options strategy.

Last Updated: Feb. 16, 2023 at 9:33 a.m. ETFirst Published: Feb. 16, 2023 at 7:01 a.m. ET

By

Barbara Kollmeyer

Critical information for the U.S. trading day

Wake up investors?

ANGELA WEISS/AGENCE FRANCE-PRESSE/GETTY IMAGESmail icon

Another big data day is testing animal spirits that seem to be keeping stock markets from running off a cliff, despite rising bond yields and signs of a strong economy that may lock in tighter Fed policy for longer.

Producer prices came in hotter than expected and stock futures are falling.

Onto our call of the day, which warns of “Volmageddon” from an increasingly popular short-term options strategy that could cause market chaos. It comes from a team led by JPMorgan’s top strategist, Marko Kolanovic, who also warned of a U.S. stocks peak earlier this week.

Kolanovic and his team noted “very large volumes” on zero days to options expirations (0DTEs) — puts and calls on stocks and indexes that expire within 24 hours. Refresher: a call option gives an investor to buy an asset at a specific price by a specific date, while a put option allows an investor to sell that asset at a certain price by a certain date.

Kolanovic’s chart shows what he sees as pretty high daily notional volumes — around $1 trillion.

His main concern is a repeat of what was seen in February 2018, when a spike in volatility crushed short volatility strategies, dubbed “Volmaggedon.” By some estimates it wiped out $2 billion in investor assets.

“While history doesn’t repeat, it often rhymes, and current selling of 0DTE (zero day to expiry), daily and weekly options is having a similar impact on markets,” said Kolanovic.

“If there is a big move when these options get in the money, and sellers cannot support these positions, forced covering would result in very large directional flows. These flows could particularly impact markets given the current low liquidity environment,” he added.

As he explained, these are typically “low delta options that rarely get in the money and their impact is mostly through volatility suppression and an intraday buy-the-dip pattern that results from hedging,” Kolanovic says. Delta is a metric that measures how much the price of a derivative would change, given a $1 shift in its underlying security.

MarketWatch’s Joe Adinolfi noted last October that 0DTE strategies were getting increasingly common, notably among institutional traders, who wanted

to profit by anticipating the hedging activity of large options dealers.

‘Insure against the worst’: Goldman picks stocks for a soft — and hard — economic landing

PUBLISHED MON, FEB 20 20238:00 PM ESTUPDATED 5 HOURS AGO

Investors are on edge after U.S. stocks fell for three consecutive weeks, signaling the possibility of higher interest rates for longer than expected.

The yield on the 6-month and 1-year Treasury bonds closed at 5% on Friday, thanks to several economic data releases last week that pointed toward a strong U.S. economy.

A rise in bond yields leads to increased borrowing costs for companies, which adds downward pressure on stocks.

Despite this challenging environment, Goldman Sachs remains optimistic and expects a “soft-landing” for the U.S. economy. In this scenario, inflation is controlled with a mild recession at most.

Nevertheless, the investment bank recommended that its clients: “Expect the best (soft-landing) but insure against the worst (hard-landing),” in a note published on Feb. 17.

“Growth, inflation, earnings, margins, and rates drive our [stock] recommendations,” the bank said in the note, entitled “Where to Invest Now.”

‘Soft-landing’ stock picks

To capture the upside in a soft-landing scenario, the Wall Street bank said that investors should own stocks that can benefit from a decelerating inflation environment.

What follows are the first four stocks named by Goldman Sachs in its “soft-landing portfolio.” The bank describes the list as “cyclical laggards with low valuations and strong balance sheets” on the Russell 3000.

GOLDMAN’S ‘SOFT-LANDING’ STOCK PICKS

| COMPANY | Ticker | Closing price ($) | Consensus price target ($) | Consensus upside (%) |

| TESLA | TSLA-USA | 208.31 | 200.00 | -3.99 |

| GARMIN | GRMN-USA | 97.01 | 102.50 | 5.66 |

| MOHAWK INDUSTRIES | MHK-USA | 113.93 | 123.00 | 7.96 |

| TOPBUILD | BLD-USA | 198.91 | 212.00 | 6.58 |

Source: FactSet / Goldman Sachs, Feb. 17

Goldman’s picks include Tesla; Garmin, the GPS technology company; Mohawk Industries, a global flooring manufacturer; and TopBuild, a supplier of insulation and building material.

Goldman Sachs analysts expect an earnings-per-share growth of 5% for Tesla and 7% for Garmin over the next 12 months, compared to a 1% growth for the S&P 500.

‘Hard-landing’ stock picks

Although not the bank’s base case, Goldman also provided investors with a “hard-landing portfolio” of Russell 1000 companies with “low valuations, strong balance sheets, [and] dividend yield.”

The top names on this list were video game giants video Activision Blizzard and Electronic Arts, along with retailers Home Depot and Lowe’s Companies.

GOLDMAN’S ‘HARD-LANDING’ PICKS

| COMPANY | Ticker | Closing price ($) | Price target ($) | Upside (%) |

| ACTIVISION BLIZZARD | ATVI-USA | 77.57 | 95.00 | 22.47 |

| ELECTRONIC ARTS | EA-USA | 112.00 | 131.75 | 17.63 |

| HOME DEPOT | HD-USA | 317.95 | 343.00 | 7.88 |

| LOWE’S COMPANIES | LOW-USA | 212.75 | 235.00 | 10.46 |

Source: FactSet / Goldman Sachs, Feb. 17

The Wall Street bank also told clients to own companies with resilient margins, as these are expected to hold up better in an economic downturn. Investors should avoid stocks with vulnerable margins, it added, especially if there is a chance that the recent decline in cost-cutting and expenses could reverse.

Goldman Sachs has previously predicted that the S&P 500 will finish the year at the same level it started —4,000 — representing a return of 0% for 2023. It ended Friday at 4,079.09.

—CNBC’s Michael Bloom contributed to this report.

High-profile hedge funds dive back into beaten-down tech stocks to capitalize on the big comeback

PUBLISHED MON, FEB 20 20238:05 AM EST

Many high-profile hedge funds jumped back into technology stocks — the group that hurt their alpha the most last year — just in time to benefit from the furious comeback in the new year.

Stephen Mandel’s Lone Pine Capital significantly upped its holdings in Microsoft and Amazon, making them top bets at the end of the fourth quarter. Meanwhile, Philippe Laffont’s Coatue Management significantly hiked its stakes in Alibaba, Microsoft and Advanced Micro Devices during the fourth quarter. Coatue also more than doubled its shares in Meta Platforms and Adobe.

Baupost’s Seth Klarman more than doubled his holdings in Google-parent Alphabet, making it his seventh biggest stake at the end of 2022. Klarman also drastically increased his Meta and Amazon bets last quarter.

Money managers with assets under management over $100 million are required to disclose their long positions quarterly with the Securities and Exchange Commission. The latest filings showed their bets at the end of 2022.

These big investors loaded up on stocks that were among last year’s biggest losers amid the Federal Reserve’s aggressive rate hikes. The tech-heavy Nasdaq Composite tumbled 33.1% in 2022, suffering its worst year since 2008. Hedge funds overall saw significant negative long alpha (-12.1%) last year, with the single biggest contributor being exposure to info tech, according to Goldman Sachs.

The rebound in technology stocks came fast and furious in the new year. The Nasdaq is up more than 12% year to date after notching its best monthly performance since July in January. Meta has added 43% in 2023, while Amazon has gained 15%. AMD is up 21% this year.

The strength in the sector came despite announcements of thousands of job cuts as the companies prepare for an economic slowdown and even a recession. Many investors, however, took the wave of bad news as a positive catalyst for the stocks as layoffs could help improve company margins.

Hedge funds overall were able to beat the market significantly. Goldman estimated that the group on average registered a loss of just 1%. The outperformance was driven by the significant positive short alpha (+6.9%), which marked the best year on Goldman’s record.

Greenlight Capital’s David Einhorn posted one of his best years ever with an outstanding return north of 30%, thanks in part to his short position in a slew of innovative technology stocks like those touted by growth investor Cathie Wood.

President Joe Biden makes surprise visit to Kyiv just days before one-year anniversary of Ukraine war

PUBLISHED MON, FEB 20 20235:09 AM ESTUPDATED MON, FEB 20 20239:58 AM EST

KEY POINTS

- After leaving Ukraine, Biden will continue on to Poland where he will meet his counterpart Andrzej Duda.

- Biden said in a White House statement that he was meeting with Zelenskyy to “reaffirm our unwavering and unflagging commitment to Ukraine’s democracy, sovereignty, and territorial integrity.”

- Zelenskyy described Biden’s visit — the first by a U.S. president in almost 15 years — as “the most important visit in the history of Ukrainian-American relations.”

U.S. President Joe Biden made a surprise visit to Kyiv, Ukraine, Monday in a show of solidarity, nearly a year after Russia began its full-scale invasion of the country.

Biden said in a White House statement that he was meeting with Ukraine President Volodymyr Zelenskyy to “reaffirm our unwavering and unflagging commitment to Ukraine’s democracy, sovereignty, and territorial integrity.”

“I will announce another delivery of critical equipment, including artillery ammunition, anti-armor systems, and air surveillance radars to help protect the Ukrainian people from aerial bombardments,” he added. “And I will share that later this week, we will announce additional sanctions against elites and companies that are trying to evade or backfill Russia’s war machine.”

The Kremlin was notified of the U.S. president’s trip a few hours before his departure for “deconfliction purposes,” White House national security advisor Jake Sullivan said Monday without going into specifics.

Zelenskyy described Biden’s visit — the first by a U.S. president in almost 15 years — as “the most important visit in the history of Ukrainian-American relations.”

“At this time, when our country is fighting for its freedom and freedom for all Europeans, for all people of the free world, it emphasizes how much we have already achieved and what historical results we can achieve together with the whole world, with Ukraine, with the United States, with the whole of Europe,” he said on Telegram, according to a NBC translation.

The U.S. head of state left the Ukrainian capital after a more than five-hour visit, according to the Associated Press. Biden said that he will continue on to Poland where he will meet his counterpart Andrzej Duda. The Polish president could press Biden on post-war “security guarantees” for Ukraine, which he on Sunday told the Financial Times would be “important” for Kyiv.

Biden’s visit to Ukraine comes after a concerted show of international support from global leaders and politicians during the Munich Security Conference over recent days. Allied forces have pledged financial support and weapons for Ukraine, but have fallen short of Zelenskyy’s pleas for the supply of jet fighters.

On Feb. 18, Biden’s second-in-command, Vice President Kamala Harris, announced that Washington had determined that Russia had committed crimes against humanity in Ukraine, upgrading the U.S. administration’s March pronouncement that Moscow had committed war crimes.

The latest round of U.S. sanctions will follow the EU’s tenth round of penalties against Russia for its war in Ukraine. European Commission President Ursula von der Leyen said last week that the sanctions will target exports worth 11 billion euros ($11.78 billion), dual use and advanced tech goods, as well as Russian propagandists. The latest EU package is subject to the approval of EU member countries.

NATO Secretary-General Jens Stoltenberg on Saturday expressed doubts to CNBC’s Hadley Gamble that financial repercussions will deter Putin, however.

“What we have seen is that Russia is actually willing to pay a hard price for this war,” he said.

“There are no signs that President Putin is preparing or planning for peace. He is preparing for more war, or new offensive, mobilizing more troops, setting the Russian economy on a war footing and also actually reaching out to other authoritarian regimes like North Korea and Iran to get more weapons.”

Retailers could face cost cuts and slower sales this year

PUBLISHED SUN, FEB 19 20238:00 AM ESTUPDATED SUN, FEB 19 202310:03 AM EST

KEY POINTS

- Walmart and Home Depot will kick off retail earnings season this week.

- Industry-watchers expect companies to strike a more cautious tone as inflation lingers.

- Healthier profit margins could be a silver lining, as some costs come down.

After benefitting from a pandemic-era shopping spree, retailers are preparing for a reality check.

Walmart and Home Depot will kick off retail earnings season Tuesday by sharing holiday-quarter results. Other big-name retailers will follow, including big-box players like Target and Best Buy, and mall staples like Macy’s and Gap.

The companies’ reports will come as recession fears cloud the year ahead. Americans are more worried about inflation now than they are about Covid. People are choosing to spend more on dining out, traveling and other services while cutting back on goods. Higher interest rates threaten the housing market.

A slowdown in sales growth also seems likely after the sharp increases of the past three years.

For investors, the end of retail’s sugar high brings a mixed picture. Companies may share modest sales outlooks. Yet healthier profit margins could be a silver lining, as freight costs fall and retailers have less excess merchandise to mark down. Plus, companies may have more cautious spending plans, such as smaller inventory orders and a slowdown in hiring. That could boost profit margins, even if consumers don’t spend as freely.

“The world is focused on top-line momentum,” said David Silverman, a retail analyst at Fitch Ratings. “So many market participants are focused on what revenue is what revenue is what revenue is.”

But, he added, “it’s the operating profit that could bounce back nicely from a difficult 2022.”

Silverman said retailers’ strategies have flipped from a year ago. Then, they bet on sky-high sales becoming the new normal and made riskier bets, from placing bigger orders to paying extra to expedite shipments. That hurt companies’ margins, as unsold merchandise wound up on the clearance rack and costs crept up, along with sales.

A dose of reality over the holidays

Already, retailers have gotten a dose of reality. Walmart, Target and Macy’s are among the companies that have spoken about a more careful consumer.

Several retailers already previewed holiday results. Macy’s warned that holiday-quarter sales would come in on the lighter side of its expectations. Nordstrom said weaker sales and more markdowns hurt its November and December results. Lululemon said its profit margins would be lower than anticipated, as the athletic apparel retailer juggles excess inventory.

Industry-wide holiday results fell below expectations, too, according to the National Retail Federation. Sales in November and December grew 5.3% year over year to $936.3 billion, below the major trade group’s prediction for growth of between 6% and 8% over the year prior. In early November, NRF had projected spending of between $942.6 billion and $960.4 billion.

Retail leaders have looked closely for clues, as they gear up for the coming fiscal year. (Most retailers’ fiscal years end in January.)

Macy’s CEO Jeff Gennette told CNBC last month that the department store operator noticed fewer holiday shoppers buying items for themselves while shopping for gifts. He said those lower purchases “more than offset the good news that we were getting on gifting and occasion.”

The company’s credit card data flashed warning signs, too, he added: Customers’ balances on Macy’s, Bloomingdale’s and co-branded American Express credit cards are rising and more of those balances are getting carried to the next month rather than paid off.

“When we look at our credit portfolio, you’ve got a customer that’s coming under more pressure,” he said.

Tough calls, cautious outlooks

Some retailers have already made some difficult moves to prepare for what could be a tough year. Luxury retailer Neiman Marcus and Saks.com, the e-commerce retailer spun off from Saks Fifth Avenue stores, have both had recent layoffs. Stitch Fix laid off 20% of its corporate workforce. Wayfair laid off 10% of its global workforce. Amazon began cutting over 18,000 employees, including many in its retail division.

Bed Bath & Beyond, which has warned of a potential bankruptcy filing, recently cut its workforce deeper as it also shutters about 150 of its namesake stores.

Target in November said it would cut up to $3 billion in total costs over the next three years, as it warned of a slower holiday season. It did not provide specifics on that plan. The company will report its fourth-quarter results on Feb. 28.

Many retail leaders said they anticipate cost-cutting measures for their workforces in the next 12 months, too, such as hiring temporary workers rather than full-time employees, according to a survey of 300 retail executives in December by consulting firm AlixPartners. Thirty-seven percent said they expect slowing raises or promotions and 28% said they expect cutting benefits at their companies in the coming year.

Of those surveyed, 19% said layoffs had happened at their companies in the last 12 months and 19% said they expect layoffs to happen in the next 12 months.

Marie Driscoll, an analyst covering beauty, luxury and fashion for retail advisory firm Coresight Research, said she expects companies to give other line items a closer look, such as free shipping and returns, as well as digital marketing expenses.

As interest rates rise, she said retailers may “find operating religion.”

“Retailers are looking at their businesses and saying not every sale is worth having,” she said. “The fact that there is a real cost of money is changing the way that companies are looking at their business.”

Yet some factors still work in retailers’ favor, she said. The tight labor market could give consumers the confidence to spend, even as inflation remains hot. People are dressing up and buying fragrances as they go out again, a factor that may have lifted January retail sales along with more spending at bars and restaurants.

She said the earnings season will bring surprises and show which companies can navigate choppier waters. Nike, for instance, raised its outlook after topping Wall Street’s expectations in December.

“A lot of it is dependent on their consumer and the strength of their brand,” Driscoll said. “There’s strength out there.”