HI Market View Commentary 12-19-2022

DON’T FORGET Market is closed Monday after the holidays !!!

So Why aren’t you doing your webinars? SO my game plan is to give you guys information on a weekly basis to educate you on the stock market, Its prepares you for the week we have coming up, to allow you ask questions and to better understand what we are doing in your portfolios.

What we heard from Powell – 2026 we might hit 2% on Inflations, Still attaching inflation with rate hikes, no real good news for the next two years

Stock picking and protection are going to be extremely important.

Millionaires holding individual stocks = they aren’t in funds = because they know how to work the numbers to find undervalued stocks

They work the numbers with a decreasing earnings outlook and an increasing inflationary environment!!!!

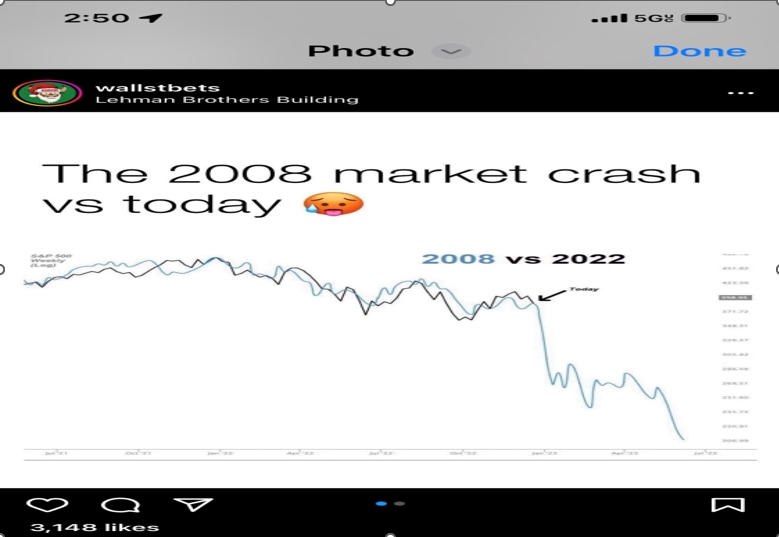

What does this all mean for next year?= For the first half of the year we could, VERY EASILY, touch 3200 to 3000 level

Simple reasons why = higher unemployment, higher interest rates, starting in Jan GDP will be negative and we will enter another recession like 2022, there are still labor shortages because people won’t work, we’ve gone through a 40 year bond bliss market and a 13 year historical bull market but now we need to pay more attention to the history related to the mid 70’s thru 80’s

Always there are higher than expected S&P 500 Estimates given at the beginning of the year. The last 13 years have skewed the averages but any 17-19 times earnings has been cheap and historically average in a short period of time.

$195 X 15 earnings = 2925

$200 X 15 earnings = 3000

$205 x 16.5 earnings = 3382

$190 x 16.5 earnings = 3135

3817 – 3135 = drop of 682 points or 682/3817= 17.86% for a low next year

Wed S&P -0.61 we were 0.34

Thur S&P -2.49 we were down -1.31

Fri S&P -1.11 we were up +0.09

Today market was down -0.90 and we were down -0.54

That’s the goal for next year is to over-protect

What does it mean when you are over protected in up days?= Less Profit, not make as much, not be as high as the market

What could we add to make up the downward trend?= consumer staples, oil,

Earnings dates:

MU 12/21 AMC

https://www.briefing.com/the-big-picture

The Big Picture

Last Updated: 16-Dec-22 13:19 ET | Archive

A Dogs of the Dow 2023 Preview

2022 has not been a good year for the stock market. In fact, it has been annus horribilis. As of this writing, the Nasdaq Composite is down 31.9%, the Russell 2000 is down 22.1%, the S&P is down 19.5%, the S&P Midcap 400 is down 15.4%, and the Dow Jones Industrial Average is down 10.0%.

A 10% decline for the Dow Jones Industrial Average isn’t cause for celebration in an absolute sense, but it is in a relative sense. What has also been cause for celebration is the average total return of the 2022 Dogs of the Dow.

Stronger Together

The Dogs of the Dow are the ten Dow Jones Industrial Average components with the highest dividend yield. Sometimes those high dividend yields are the result of falling stock prices while other times they are simply a case of a stock having a high dividend yield.

It is a pretty simple process for investing in a Dogs of the Dow portfolio. After the market closes on the last day of the year, identify the ten highest-yielding Dow stocks, and then buy them at the start of the year investing an equal dollar amount in each of the stocks. Hold the stocks for a year and repeat the process at the end of the next year.

A variation of the strategy is to buy the five lowest-priced of the ten highest-yielding Dow stocks. These are called the “Small Dogs of the Dow.” Again, one would purchase them at the start of the year, investing an equal dollar amount, and hold them for a year.

The table below provides a snapshot of the 2022 Dogs of the Dow. Individually, there have been some real dogs in the bunch, but collectively, they have vastly outperformed the market with an average total return of 0.3% versus -17.0% for the S&P 500. The Small Dogs of the Dow are in blue.

| Stock | Symbol | Price | 2022 Total Return (%) |

| Dow, Inc. | DOW | 49.07 | -9.2 |

| IBM | IBM | 139.11 | 9.3 |

| Verizon | VZ | 36.84 | -25.2 |

| Chevron | CVX | 167.90 | 48.3 |

| Walgreens Boots Alliance | WBA | 38.70 | -22.3 |

| Merck | MRK | 108.96 | 46.7 |

| Amgen | AMGN | 266.83 | 22.4 |

| 3M | MMM | 120.52 | -29.3 |

| Coca-Cola | KO | 62.48 | 8.6 |

| Intel | INTC | 26.53 | -46.5 |

Source: FactSet

Less than Average

The website dogsofthedow.com offers an insightful look at the historical performance of the Dow Dogs and the process for carrying out this investment strategy.

Past performance is no guarantee of future results, yet the strategy has a decent track record.

Since 2000, the Dogs of the Dow has had an average annual total return of 8.7% and the Small Dogs of the Dow has had an average annual total return of 9.3%, according to dogsofthedow.com. The 2022 Dogs of the Dow portfolio, then, has been less than average, yet it has clearly fared much better than the broader market. The Small Dogs of the Dow portfolio has not with an average total return of -18.9%.

There are still nine trading days left in 2022, but an early glimpse of a Dogs of the Dow portfolio for 2023 is included in the table below. The Small Dogs of the Dow are in blue. They are the same, with the exception of Cisco, which has replaced Coca-Cola in that projected grouping.

| Stock | Symbol | Price | Dividend Yield (%) |

| Verizon | VZ | 36.86 | 6.9 |

| Dow, Inc. | DOW | 49.07 | 5.7 |

| Intel | INTC | 26.54 | 5.5 |

| Walgreens Boots Alliance | WBA | 38.72 | 5.0 |

| 3M | MMM | 120.41 | 4.9 |

| IBM | IBM | 139.34 | 4.7 |

| Chevron | CVX | 167.92 | 3.4 |

| Amgen | AMGN | 267.00 | 3.2 |

| Cisco | CSCO | 47.61 | 3.2 |

| JPMorgan Chase | JPM | 128.73 | 3.1 |

Source: FactSet

We will post a final Dogs of the Dow for 2023 portfolio at the end of trading on Friday, December 30, to our In Play page.

We will reserve this space that day for our annual “Year in Review.”

Happy holidays!

—Patrick J. O’Hare, Briefing.com

(Editor’s Note: the next installment of The Big Picture will be the Year in Review on December 30)

https://go.ycharts.com/weekly-pulse

| Market Recap |

| WEEK OF DEC. 12 THROUGH DEC. 16, 2022 |

| The S&P 500 index fell 2.1% last week amid worries about how high interest rates may climb and whether a recession is in the works.

The market benchmark ended Friday’s session at 3,852.36, down from last week’s closing level of 3,934.38. This is the index’s second week in a row in the red. The S&P 500 is now down 5.6% for December to date and down 19% for the year to date, with just two weeks remaining in the month and year. Last week’s decline came as the Federal Open Market Committee increased its benchmark lending rate by 50 basis points, as expected, but also raised its median rate outlook, which spooked investors. While the federal funds rate was moved to a range of 4.25% to 4.5%, the FOMC now expects an increase in the 2023 median funds rate to 5.1%, up from an estimate of 4.6% in September. Its estimated median rates for 2024 and 2025 were increased to 4.1% and 3.1%, respectively, from September estimates of 3.9% and 2.9%. Weaker-than-expected readings on US retail sales and industrial production only added to investors’ worries. November US retail sales fell 0.6% in November, worse than the Econoday consensus estimate for a 0.2% decline and marking the largest monthly drop last year. US industrial production unexpectedly fell for the second month in a row amid decreases in mining and manufacturing output. The fall in manufacturing output marked the first monthly drop since June. All but one of the S&P 500’s sectors declined last week. Consumer discretionary led the slide with a drop of 3.6%, followed by a 2.7% decline in technology, and drops of 2.5% each in financials and communication services. Energy was the lone gainer with a 1.7% increase. The consumer discretionary sector’s decliners included shares of Tesla (TSLA), which lost 16% as regulatory filings showed Chief Executive Elon Musk sold 22 million shares of the electric vehicle company last week. In the technology sector, shares of Trimble (TRMB) fell 13% as the industrial technology company said it agreed to acquire Transporeon, a cloud-based transportation management software platform, in an all-cash transaction valued at EUR1.88 billion. Among the decliners in the financial sector, shares of M&T Bank (MTB) slipped 7.5%. The bank named a new chief financial officer, Daryl Bible, effective in Q2 2023. Bible will join the company from Truist Financial, where he served as CFO. The company said its current finance chief, Darren King, “will assume an expanded set of responsibilities to include oversight of a portfolio of businesses, including retail and business banking, mortgage, and consumer lending.” In communication services, shares of Charter Communications (CHTR) fell 20% as the broadband connectivity company laid out capital expenditure plans of $10.50 billion to $10.80 billion for 2023. Also in communication services, shares of Warner Bros. Discovery (WBD) shed 11% as the media and entertainment company raised the amount of restructuring charges it expects to book after its merger with AT&T’s (T) media and entertainment unit. The energy sector’s advance, meanwhile, came amid a climb in crude oil and natural gas futures. Gainers included shares of EQT (EQT), which received an investment rating upgrade to outperform from peer perform. Shares rose 4.4%. Next week’s economic calendar will be heavy on housing and inflation data. Early in the week, investors will receive the National Association of Home Builders index for December as well as building permits, housing starts and existing home sales for November. Later in the week, new home sales for November will be reported on Friday, though the personal consumption expenditures — or PCE — price index, a key inflation reading, is likely to receive the most attention on Friday. Provided by MT Newswires |

Where will our markets end this week?

Lower

DJIA – Bearish

SPX –bearish

COMP –bearish again

Where Will the SPX end December 2022?

12-19-2022 -4.0%

12-12-2022 -4.0%

12-05-2022 -4.0%

Earnings:

Mon:

Tues: GIS, BB, NKE,

Wed: CTAS, RAD, MU

Thur: KMX, PAYX

Fri:

Econ Reports:

Mon: NAHB Housing Index

Tue Housing Starts, Building Permits

Wed: MBA, Current Account Balances, Existing Home Sales,

Thur: Initial Claims, Continuing Claims, GDP, GDP Deflator,

Fri: Durable Goods, Durable ex-trans, Personal Income, Personal Spending, PCE Prices, New Home Sales, Michigan Sentiment

How am I looking to trade?

Currently have protection on for downward market movements, SPY puts in accounts for possible earnings disappointment

www.myhurleyinvestment.com = Blogsite

info@hurleyinvestments.com = Email

Questions???

BA has already been down and recently had a 43 billion dollar order with a 9.56 year backlog

DIS down because Avatar only made 240ish million dollars worldwide and 134 domestically

F pre recessionary fears, because truck orders are strong, pre orders for the electric “NOT” a real truck are strong, but they’ve raised the electric truck price by 40%

AAPL price is collapsing? I don’t see pricing collapsing but worries in China and covid

Am I worried about China ? not so much because I’ve seen BABA and BIDU strengthening recently

Are you going to change your core holding? Probably not, but I may add to them for a sector that can buck the market

Goldman and Citi love these two beaten-down tech giants and expect them to rebound in 2023

PUBLISHED WED, DEC 14 20223:17 AM EST

The technology sector has been slammed in 2022, but that has left opportunities for investors to snap up discounted stocks heading into next year.

“While we recognize the multiple challenges facing the broader Internet sector, we continue to believe the long-term secular advantages outweigh those in the short term,” wrote Citi analyst Ygal Arounian in a Dec. 12 note. “Internet has seen meaningful underperformance in 2022 as multiples moved from all-time highs to all-time lows, coupled with material downward estimate revisions for many companies across our coverage.”

At the same time, however, the core drivers of the internet sector have not changed, and there is opportunity in the group over time, Arounian said. He reiterated that Amazon remains Citi’s top pick in the space, and Meta Platforms the second.

Goldman Sachs also sees potential in pockets of technology.

“We see the most compelling risk/reward in the group among a collection of large cap companies that have many of the same narratives in common,” wrote Eric Sheridan in a Dec. 13 note. Those narratives include well-established and scaled end-market positioning, the ability to manage for improved margin trajectory in 2023 and beyond, as well as a “wall of worry” that has become more pronounced in the past six months.

Goldman’s top picks include Amazon and Meta.

Top pick – Amazon

Amazon has enjoyed bullish ratings from Wall Street even as it’s plunged roughly 45% year to date.

While Citi recognizes that there are demand challenges facing Amazon, especially in its retail business. Still, it believes that the company can continue to gain wallet share even amid economic uncertainty.

In addition, “adoption of AWS can accelerate through improved operating efficiencies and hiring freezes can deliver improving operating income,” Arounian wrote. Citi has a buy rating and $145 price target on the stock. Shares ended Tuesday’s session at $92.49, up about 2% for the day.

Goldman Sachs also sees a buying opportunity for Amazon as one of its own top picks, with a buy rating. The stock has seen multiple years of underperformance as margins have absorbed the Covid pandemic and ensuing macroeconomic headwinds, according to Sheridan.

In addition, the company is benefiting from the “rising utility nature of the shopping habits of the Prime user base, cross platform narratives building across advertising and media consumption,” he said.

Amazon has the potential for margin self-repair in 2023 and beyond, plus a well-established multi-year secular growth opportunity for AWS, Sheridan added.

Top pick – Meta

Meta Platforms is Citi’s second pick in technology – the company has a buy rating and $168 price target on the stock. The social media giant has suffered this year, sliding nearly 65% in 2022. Shares ended Tuesday higher, rising 4.7% to close at $120.15

“While IDFA challenges persist amid elevated operational and capital expenses, given improving engagement trends across Feed, Stories, Reels, and Messenger, we believe Meta is delivering greater meaningful social interaction (MSI) across its user base, making it more relevant,” said Arounian, referring to a major privacy change Apple made to its iOS operating system last year.

“This as its advertising platform is rebuilt for a post-IDFA environment and demand for newer ad products like Reels, Click-To-Message, and Advantage+ attract incremental advertising dollars,” the analyst said.

Goldman is also bullish on Meta. While there is a “downside scenario for core business and fears over investment cycle increasingly priced into shares; large elements of engagement and consumer utility remain mostly unmonetized,” said Sheridan.

Those include messaging and short-form video, the core product is exiting 12 to 18 months of headwinds from Apple privacy changes and advertiser slump in long-tailed eCommerce and other growth categories, he said. Goldman also has a buy rating on Meta.

-CNBC’s Michael Bloom contributed to this story.

2022 didn’t go as expected for bank investors. How to avoid pitfalls in the sector in 2023

PUBLISHED MON, DEC 19 202211:09 AM EST

Banks finally got a long-awaited boost to interest rates this year after a decade of toiling in a low-rate environment. It didn’t go as planned.

A year ago, big lenders including Bank of America and Wells Fargo were the top picks of the analyst community because they were expected to benefit from higher rates. Loan growth coupled with vast deposit bases would drive gains in interest income as the Federal Reserve hiked rates, the thinking went.

While that trend played out, the bull case was spoiled by inflation at four-decade highs, which forced the Fed to boost rates more than expected, triggering concerns of a recession. In a downturn, banks are exposed to surging loan defaults, reduced loan demand and write-downs on assets.

That’s why the KBW Bank Index slumped 23% through mid-December, worse than the 17% decline of the S&P 500 and on track for its worst year since 2008.

Higher rates didn’t boost bank stocks as expected

“The interest rate-trade is getting long in the tooth, and meanwhile there are uncertainties on deposits, both on costs and outflows,” David Konrad, a KBW analyst, told CNBC in a phone interview. He cut his recommendation on the sector to market weight from overweight last week.

Net interest income growth will probably peak in this year’s fourth quarter at 30% and slump to just 5% by the end of 2023, Konrad said in a Dec. 13 note.

Among banks, he favors Goldman Sachs and Morgan Stanley because “they have already been operating in a recession” and their capital markets businesses will rebound before retail banking does, he said in the interview.

Multiple headwinds

Headwinds faced by banks next year include expectations for shrinking loan margins in the second half, higher reserves for bad loans, rising funding costs for deposits, higher expenses due to wage inflation and continued pressure on mortgage, wealth management and investment banking revenue, according to Raymond James analysts led by Daniel Tamayo.

BANK STOCKS TO WATCH IN 2023

| TICKER | NAME | YTD PERFORMANCE | CONSENSUS PRICE TARGET | TARGET PRICE IMPLIED RETURN | MEDIAN RATING |

| GS | Goldman Sachs | -9.46% | $393.43 | 13.59% | Overweight |

| MS | Morgan Stanley | -11.51% | $93.57 | 7.73% | Overweight |

| CDNS | Cadence Bank | -12.42% | $191.67 | 17.44% | Overweight |

| HBAN | Huntington Bancshares | -11.48% | $16.22 | 18.83% | Hold |

| FRC | First Republic | -41.38% | $137.27 | 13.40% | Overweight |

| WTFC | Wintrust Financial | -11.67% | $109.17 | 36.09% | Buy |

| BAC | Bank of America | -28.75% | $41.33 | 30.38% | Overweight |

| USB | U.S. Bancorp | -24.96% | $52.90 | 25.50% | Overweight |

| PNC | PNC Financial | -25% | $180.02 | 19.70% | Overweight |

Source: FactSet; Note: Implied return based on Dec. 16 closing price

“With many of our positive catalysts from 2021-22 played out, we believe 2023 will be volatile for bank stocks, with the best performers those who can withstand headwinds for the industry,” Tamayo said in a Dec. 15 note.

Tamayo favors smaller banks over megacaps for their lower valuations, less strict regulatory oversight and the possibility of mergers. He has a strong buy rating on Cadence Bank, Huntington Bancshares, First Republic and Wintrust Financial.

Hold off until 2024?

In that vein, Morgan Stanley analyst Betsy Graseck advised that it was too early to go long large cap banks. Investors should pile into the sector only after loan delinquencies peak or the Fed ends its balance sheet-shrinking campaign known as quantitative tightening, she said in a Dec. 6 note.

“It’s not enough for the Fed to just slow or stop hiking rates, it has to end QT to get more positive on the banks,” Graseck said.

That’s because “we expect that credit is likely to surprise more negatively than positively over the next 12 months as the economy deals with still-high inflation, higher borrowing costs” and rising joblessness, she added.

The wait could be long: Morgan Stanley economists see QT ending in the first half of 2024.

The bull case

On the other hand, the group could rally next year if the economy manages a soft landing or mild recession, Bank of America analyst Ebrahim H. Poonawala said in a Dec. 11 note. Much of the downside for the industry is already embedded in current valuations, according to Baird analyst David George.

That could set up the inverse of 2022 – a year in which pessimism leads to better-than-expected stock returns.

Veteran analyst Mike Mayo of Wells Fargo said that bank stocks could pop 50% in 2023 by proving their resilience in a recession. That’s because they’ve been de-risked over more than a decade of increasingly stringent financial regulations.

“We think banks should perform better in an upcoming recession than for any other in modern history,” Mayo said in a Dec. 14 note. “What seems most underappreciated is the degree that bank structural changes over the past decade prepare the industry for the cyclical challenges ahead.”

His top picks are Bank of America, U.S. Bancorp and PNC Financial Services. The three lenders are prepared to navigate a downturn with strong credit quality, lower expenses and higher efficiency, he said.

—CNBC’s Michael Bloom contributed to this report.

The U.S. and China are one step closer to preventing stocks like Alibaba from delisting. What to watch next

PUBLISHED SUN, SEP 4 20229:01 PM EDTUPDATED SUN, SEP 4 202210:56 PM EDT

KEY POINTS

- The U.S. Public Company Accounting Oversight Board said its inspectors are set to arrive in Hong Kong in mid-September, shortly after which “all audit work papers requested by the PCAOB must be made available to them.”

- What needs to happen next is a smooth on-ground inspection in China by the U.S., and adequate support from the Chinese authorities, analysts said.

- However, there’s uncertainty around implementation, analysts said.

BEIJING — The U.S. and China recently took a significant first step toward keeping U.S.-listed Chinese stocks like Alibaba from being forced off U.S. stock exchanges.

What needs to happen next is a smooth on-ground inspection in China by the U.S. with adequate support from Chinese authorities, analysts said.

“Many implementation details probably can only be figured out by the auditing firms and the [Ministry of Finance] — together with [the China Securities Regulatory Commission] — through real-case auditing trials under this unprecedented agreement,” said Winston Ma, adjunct professor of law at New York University.

The U.S. Public Company Accounting Oversight Board said its inspectors are set to arrive in Hong Kong in mid-September, shortly after which “all audit work papers requested by the PCAOB must be made available to them.”

Audit work papers differ from the actual information on companies gathered by accounting firms.

The work papers record the audit procedure, tests, gathered information and conclusions about the review, according to the PCAOB website. It is not clear what level of highly sensitive information, if any, would be included in the work papers.

The ability of the U.S. to inspect those work papers for Chinese companies listed in the U.S. has been a years-long dispute. U.S. political and legal developments in the last two years have sped up the threat that the Chinese companies might need to delist from U.S. stock exchanges.

A turning point came in late August when the PCAOB and China Securities Regulatory Commission signed a cooperation agreement that laid the regulatory basis for allowing U.S. inspections of audit firms within China’s borders.

That’s according to statements from both government entities, which also said China’s Ministry of Finance signed the deal.

“I see this as a big ‘progress,’ meaning that both sides were willing to take steps to move this forward,” said Stephanie Tang, head of private equity for Greater China and partner at Hogan Lovells.

“The subject or the audience of this PCAOB investigation would be the audit firms,” she said, emphasizing she is not an accountant.

Need for more implementation clarity

China’s registered accounting firms are overseen by the the Ministry of Finance, making it the leader on the Chinese side of next steps, said Ming Liao, founding partner of Beijing-based Prospect Avenue Capital.

However, there’s uncertainty around implementation of the agreement as it only established a framework, analysts said.

“Our accounting firms still don’t know how to proceed,” said Peter Tsui, president of the Hong Kong-based Association of Chinese Internal Auditors. That’s according to a CNBC translation of his Mandarin-language remarks Thursday.

He said questions remain over what information the firms should share in order to remain compliant with Chinese regulation.

“Give [us] some guidelines,” Tsui said.

Tsui said the inspections should go smoothly if it’s just a matter of accountants on both sides, and there is no political interference on the U.S. side. He said the big four accounting firms — KPMG, PwC, Deloitte and EY — are members of the association.

China’s Ministry of Finance has yet to release a public statement on the audit cooperation agreement. The ministry did not immediately respond to a CNBC request for comment.

One development Prospect Avenue Capital’s Liao is watching is whether U.S. President Joe Biden and Chinese President Xi Jinping meet in-person this fall for the first time under the Biden administration. That could speed up a final agreement on the audit dispute, he said.

“In the end, resolving the audit work paper problem relies on political interaction between China and the U.S.,” Liao said in Chinese, according to a CNBC translation. “With trust, this problem can very easily be resolved.”

A decision by the year’s end

The PCAOB said it will make a determination in December on whether China was still obstructing access to audit information.

U.S. regulators will likely “start to know in October or November” what determination the PCAOB will make on whether U.S.-listed Chinese companies might be headed for delisting, Gary Gensler, chair of the U.S. Securities and Exchange Commission, told CNBC’s David Faber in late August.

Alibaba and many other U.S.-listed Chinese companies have started in the last few years to issue shares in Hong Kong — partly seen as a way to hedge against a potential delisting from U.S. stock exchanges. Since Chinese ride-hailing company Didi’s U.S. IPO in the summer of 2021, Beijing has also increased its scrutiny of Chinese companies wanting to list overseas.

The combined political uncertainty has slowed the flow of Chinese IPOs in the U.S., especially of larger companies.

Since July 1, 2021, 16 Chinese companies have listed in the U.S., excluding special-purpose acquisition companies, according to Renaissance Capital. Back in 2020, 30 China-based companies had listed in the U.S., the firm said then.

By value, the five largest U.S. institutional holdings of U.S.-listed Chinese stocks are: Alibaba, JD.com, Pinduoduo, NetEase and Baidu. That’s according to Morgan Stanley research dated Aug. 26.

Gun Shops And Customers Claim Credit Card Firms “Restrict” Firearm Purchases

BY TYLER DURDEN

FRIDAY, DEC 09, 2022 – 09:20 PM

Gun rights advocates warned that a new change to the credit card industry to add a firearm and ammunition-specific Merchant Category Code (MCC) for gun stores wasn’t about tracking guns necessarily, but could lead to the denial of lawful firearms purchases by law-abiding citizens.

In September, Visa, Mastercard, and American Express all said they would adopt the MCC code to categorize sales at gun shops; months later, several social media posts of alleged gun stores and customers claim they experienced card issues.

Twitter account “Battlecock Tactical” tweeted, “Federal Firearms License [gun shop] in a Facebook group shared this. Looks like the doomers accurately called how that new firearms merchant code would go down.”

Battlecock Tactical’s images show what appears to be a retail POS system at an FFL that reads $913.70 transaction was “declined.” The error code on the merchant’s computer read:

“Transaction declined: Charge declined RESTRICTED CARD Customer bank does not allow this card to be used at this type of merchant.”

Another picture from the customer’s view had the same error message.

Battlecock Tactical’s tweet had what appears to be another FFL by the handle “3dprintfreedom.com” who replied:

Someone with the handle “AnarchyCoiner” tweeted:

“I had this happen with my PayPal credit card. I tried to use it to buy ammo at my local FFL and it was denied.”

Another person said:

“Tried to buy a psa dagger slide a bit ago and had the same issue ordering from their website with my debit card – credit card let me order tho.”

And perhaps the gun advocates were right from the get-go…

As credit card companies were rolling out the new code in mid-September, National Shooting Sports Foundation lawyer Lawrence Keane explained:

“It was never about gathering data to aide law enforcement. It is, and always has been, a concerted effort to pressure credit card companies to deny lawful purchases of firearms and put every single gun purchaser on a watchlist.”

Could these be some of the first examples of backdoor anti-gun policies enforced through big corporations?

Meanwhile, an alleged former FFL holder had this to say:

https://www.cnbc.com/2022/12/19/analyst-say-these-stocks-have-the-most-to-lose-in-2023.html

Beware these stocks: Analysts see a rough year ahead for these companies

PUBLISHED MON, DEC 19 202212:26 PM EST

Next year is expected to be a volatile one for the stock market, yet certain companies may be hurt more than others.

Persistent inflation, a possible recession, earnings cuts and the Federal Reserve’s reduction of its bond holdings could send the S&P 500 tumbling to 3,000 in the first half of 2023, Bank of America’s Savita Subramanian recently wrote in a note. That’s about a 22% drop from Friday’s close.

Meanwhile, Morgan Stanley strategist Mike Wilson is predicting earnings will shrink 15% to 20% next year.

CNBC Pro looked at stocks that are poised to lose the most in 2023 based on the average analyst price target, according to FactSet. We also included the percentage of sell ratings among the analysts that cover the stocks and their performances so far this year.

STOCKS SET TO FALL THE MOST IN 2023

| SYMBOL | NAME | SECTOR/INDUSTRY | UPSIDE TO AVG PT (%) | (%) SELL RATING | YTD % CHANGE |

| BEN | Franklin Resources, Inc. | Finance | -12.1 | 33.3 | -23.1 |

| ED | Consolidated Edison, Inc. | Utilities | -11.3 | 37.5 | 11.5 |

| TROW | T. Rowe Price Group | Finance | -11.0 | 37.5 | -43.8 |

| CPB | Campbell Soup Company | Consumer Non-Cyclicals | -9.5 | 22.2 | 31.3 |

| PFG | Principal Financial Group, Inc. | Finance | -7.9 | 56.3 | 17.4 |

| GIS | General Mills, Inc. | Consumer Non-Cyclicals | -7.6 | 10.0 | 29.0 |

| PNW | Pinnacle West Capital Corporation | Utilities | -7.5 | 20.0 | 10.4 |

| IVZ | Invesco Ltd. | Finance | -7.2 | 5.9 | -20.1 |

| KMB | Kimberly-Clark Corporation | Consumer Non-Cyclicals | -6.8 | 10.0 | -5.3 |

| CLX | Clorox Company | Consumer Non-Cyclicals | -6.8 | 33.3 | -17.1 |

| GPC | Genuine Parts Company | Consumer Cyclicals | -5.9 | 7.1 | 26.1 |

| EXPD | Expeditors International of Washington, Inc. | Industrials | -5.4 | 33.3 | -19.2 |

| MKTX | MarketAxess Holdings Inc. | Finance | -5.3 | 7.7 | -32.3 |

| UHS | Universal Health Services, Inc. Class B | Healthcare | -5.3 | 22.2 | 4.7 |

| MTD | Mettler-Toledo International Inc. | Healthcare | -4.9 | 7.1 | -15.9 |

| SJM | J.M. Smucker Company | Consumer Non-Cyclicals | -4.7 | 31.3 | 14.4 |

| DGX | Quest Diagnostics Incorporated | Healthcare | -4.7 | 5.6 | -13.7 |

| XYL | Xylem Inc. | Industrials | -4.3 | 0.0 | -8.3 |

| MKC | McCormick & Company, Incorporated | Consumer Non-Cyclicals | -4.0 | 14.3 | -13.7 |

| ETSY | Etsy, Inc. | Consumer Non-Cyclicals | -3.7 | 3.4 | -42.3 |

Source: FactSet

Asset manager Franklin Resources has the most downside next year, set to lose 12%, according to the average analyst price target on FactSet. Some 33% of analysts covering the stock rate it a sell. The firm has $1.4 trillion of assets under management as of Nov. 30, up from $1.318 trillion at Oct, 31. Franklin Resources is down 23% so far this year.

Following Franklin Resources is Consolidated Edison, which analysts believe could drop 11%, per FactSet, essentially erasing its gains this year. Of the analysts that cover the utility stock, 37% have a sell rating. When Consolidated Edison reported third-quarter earnings-per-share of $1.63 in November, it beat expectations. CEO Timothy Cawley also highlighted the company’s recent announcement it was selling its clean energy business for $6.8 billion, noting the sale will allow Consolidated Edison to focus on its core utility business.

Also making the list is food giant General Mills, which has nearly 8% downside to the average analyst price target. Some 10% of analysts covering the stock rate it a sell.

General Mills, which has gained 29% year to date, is set to release fiscal second-quarter earnings on Tuesday. Wall Street is expecting earnings per share of $1.06, according to StreetAccount. That’s an increase of about 7% from the same time last year.

Another consumer name on the list is Clorox. The stock has nearly 7% downside to the average analyst price target, per FactSet. About 33% of analysts covering the stock have a sell rating. When the company reported earnings in November, it said it expected net sales between a 4% decrease to a 2% increase for fiscal 2023, compared to the prior year. It also expects a gross margin increase of about 200 basis points. Clorox is down about 17% year to date.

Lastly, Etsy has nearly 4% downside to the average analyst price target. The online marketplace has tumbled 42% so far this year, but is up 44% since reporting an earnings beat on Nov. 2. Only 3.4% of analysts covering the stock rate it a sell. Citi recently initiated coverage of Etsy with a buy rating, saying it sees an attractive risk/reward outlook for the stock. Earlier in December, Jefferies reiterated its buy rating, saying it believes Etsy will be among the winners this holiday shopping season.

https://www.cnbc.com/2022/12/19/millionaire-investors-havent-been-this-bearish-since-2008.html

Millionaire investors haven’t been this bearish since 2008

PUBLISHED MON, DEC 19 20227:59 AM ESTUPDATED 47 MIN AGO

KEY POINTS

- Rich investors are betting on double-digit declines in stocks next year, according to the CNBC Millionaire Survey.

- Fifty-six percent of millionaire investors surveyed expect the S&P 500 to decline by 10% in 2023.

- There is a large optimism gap between younger and older millionaires. Eighty-one percent of millennial millionaires expect their assets to be higher at the end of next year.

Millionaire investors are betting on double-digit declines in stocks next year, reflecting their most bearish outlook since 2008, according to the CNBC Millionaire Survey.

Fifty-six percent of millionaire investors surveyed expect the S&P 500 to decline by 10% in 2023. Nearly a third expect declines of more than 15%. The survey was conducted among investors with $1 million or more in investible assets.

They also expect falling equities to reduce their wealth. When asked about the biggest risk to their personal wealth over the next year, the largest number (28%) said the stock market.

The last time millionaire investors were this gloomy was during the financial crisis and Great Recession more than a decade ago.

“This is the most pessimistic we’ve seen this group since the financial crisis in 2008 and 2009,” said George Walper, president of Spectrem Group, which conducts the survey with CNBC.

Inflation, rising rates and the potential for recession are all weighing on the minds of wealthy investors, Walper said. And while markets have already fallen this year, with the S&P 500 down about 18%, wealthy investors are forecasting even more pain ahead next year.

The bleak outlook could also put additional pressure on markets, since millionaire investors own more than 85% of individually held stocks. More than a third of millionaires expect their overall investment returns (which include bonds and other asset classes, along with stocks) to be negative next year. Most are expecting returns of less than 4%, which is low given that short-term Treasurys are now yielding over 4%.

Many millionaires are holding cash and planning to stay on the sidelines, at least for the foreseeable future. Nearly half (46%) of millionaire investors have more cash in their portfolio than last year, with 17% holding “a lot more.”

Millionaires are also bearish about the economy, with 60% expecting the economy to be “weaker” or “much weaker” at the end of 2023.

There is a large optimism gap, however, between younger and older millionaires. Eighty-one percent of millennial millionaires expect their assets to be higher at the end of next year, with nearly half (46%) expecting their assets to be up 10% or more. By contrast, most (61%) baby boomer millionaires expect their assets to be lower or “much lower” next year. More than half of millennial millionaires say the S&P 500 will be up 10% or more next year.

Walper said millennials have grown up in a financial world of low interest rates and rising asset prices, where market sell-offs have usually been followed by quick rebounds. Older generations, he said, may remember the high-inflation, rising-rate world of the 1970s and early 1980s, when the S&P drifted lower for more than a decade.

“The millennial millionaires have never lived through a true inflationary environment,” Walper said. “For their entire business life, they’ve seen interest rates that were managed by the Fed. They’ve never seen rate hikes this aggressive.”

Millionaire pessimism is also affecting their views of their financial advisors. A majority say they have consulted “very little” or “not at all” with their financial advisors about how to position for inflation. Walper said approval levels for financial advisors “have never dropped this much this quickly, at all wealth levels.”

“They feel that their advisors are not communicating or preparing them for how to deal with it,” Walper said. “They’re not talking to them about what all this means for their financial future.”

The CNBC Millionaire Survey was conducted online in November. A total of 761 respondents, representing financial decision-makers in their households, qualified for the survey. The survey is conducted twice a year, in the spring and in the fall.