And this too shall pass.

Let’s go over positions by looking at charts and going over what we have in place.

This could be the start of a correction and/or be a buying opportunity

Earnings

DG 03/12 est

MU 03/18 est

https://www.briefing.com/the-big-picture

The Big Picture

Last Updated: 27-Feb-26 12:35 ET | Archive

AI uncertainty to cap multiple expansion

Briefing.com Summary:

*Markets are struggling to price AI’s long-term impact, creating volatility and delaying broad-based confidence in future earnings durability.

*Earnings growth remains strong, but surprise levels haven’t been as strong.

*Companies across industries must prove AI enhances profitability rather than disrupts business models and compresses profit margins.

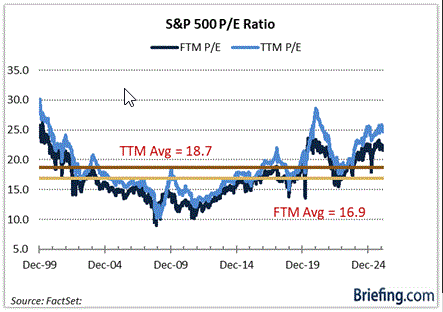

We are going to share a story about valuation. It is going to begin with a picture and end with a twist.

Multiple Compression

We have seen some multiple compression to begin the year thanks largely to a rollback in many of the mega-cap stocks. Specifically, the S&P 500 entered 2026 trading at 22.1x forward twelve-month earnings and 25.4x trailing twelve-month earnings. Today, those P/E multiples sit restlessly at 21.8x and 25.1x, respectively.

In other words, they haven’t come down that much and are still stretched appreciably relative to averages covering the period from 2000 to present. Another interesting consideration is that the multiple compression stems from earnings growth rising faster than prices.

The S&P 500 is up 0.2% year-to-date versus a 3.0% increase for the forward twelve-month estimate and a 3.2% increase for the trailing twelve-month estimate. On the plus side, these things are all moving in the right direction, but on the downside, the existing stretched valuations are standing in the way of multiple expansion.

Said another way, the good earnings news has been mostly priced in. That is partly why a stock like NVIDIA (NVDA) would trade down 5.5% after the AI leader reported quarterly revenue up 73% year-over-year, a non-GAAP gross margin of 75.2%, and adjusted diluted EPS up 82% year-over-year.

Positive Feedback Loop

There were other factors involved with NVIDIA’s post-report decline, as was the case with Amazon’s (AMZN) post-report decline, Microsoft’s (MSFT) post-report decline, and declines in many stocks, either immediately after their reports or in subsequent weeks, like in the cases of Meta Platforms (META), Tesla (TSLA), and Alphabet (GOOG/GOOGL).

The hangup for NVIDIA is that its results were too good. Investors appeared skeptical that NVIDIA could continue to deliver the same monstrous growth as it contends with the law of large numbers, budding competition, and a potential scaling back of capex budgets by the hyperscalers.

Ironically, hyperscalers faced investor backlash for investing too much in their AI buildout plans without a quantifiable pathway to meaningful returns on their investment. At this point, it is a bill of sale that the returns will be there eventually. Other companies, meanwhile, got pummeled on the notion that their business models, cash flows, and earnings prospects will be weakened by the rise of AI models, tools, and agents borne out of the heavy investment in AI.

This positive feedback loop has thrown the market for a loop to begin the year, never mind that each of the major indices is higher year-to-date.

The fact that the consumer staples sector has outperformed the information technology sector by nearly 2100 basis points year-to-date and the financial sector by nearly 2300 basis points, that the 10-yr note yield has declined 20 basis points, and that the CBOE Volatility Index is up 34% underscores how loopy the stock market has been even though the earnings growth, in aggregate, has been better than expected… or has it?

The S&P 500 is on pace for its fifth consecutive quarter of double-digit earnings growth. According to FactSet, companies, in aggregate, have reported earnings 7.2% above expectations, but here is the relative rub: that is below the one-year average of 7.4% and the five-year average of 7.7%.

In short, the fourth-quarter earnings reporting has been good, as expected. It just hasn’t been as good as past periods from a surprise perspective, so it hasn’t led to multiple expansion.

Briefing.com Analyst Insight

When you have a rich valuation, it gets harder to provide a true positive surprise. The reason being is that the rich valuation is a byproduct of investors frontrunning the expected good earnings news, so much so that by the time the good earnings news arrives, it is already in the stock price (and then some).

It gets even harder, though, when doubts emerge about being able to follow through quarter after quarter with impressive earnings results. That is the predicament the mega-cap stocks find themselves in, and the predicament many other industries are facing with respect to being disrupted by AI advancements.

That is why the market cap-weighted S&P 500, anyway, has been range-bound since October even though the forward twelve-month earnings estimate has continued to be revised higher.

The hyperscalers are going to have to prove that they are getting meaningful returns on their massive AI investments. Hardware companies that need memory are going to have to prove that the spike in memory costs is not adversely impacting their profit margins. Software companies are going to have to prove that they aren’t being disintermediated by AI tools. The same goes for logistics companies and financial services firms, and right on down the line.

AI is a change agent, but it is unclear to what degree for just about every business out there. It will be better for some than others, but every publicly traded company is a show-me story now.

How long it takes to convince investors that AI is a change agent for the better is the great unknown. That uncertainty will be a headwind for multiple expansion, certainly at the index level, which is dictated by the behavior of the mega-cap stocks, but it will infiltrate (and already has) other industry groups.

It will take some patience to watch things get sorted out. We expect many twists and turns along the way. We just don’t expect any significant multiple expansion at this juncture when the AI plot twist has thickened.

—Patrick J. O’Hare, Briefing.com

Where will our markets end this week?

Lower

DJIA – Bullish

SPX – Bearish

COMP – Bearish

Where Will the SPX end March 2026?

03-02-2026 -2.0%

Volatility Index

Volatility of Volatility Index

Econ Reports:

Mon: Construction Spending, ISM Manufacturing

Tue

Wed: MBA, ADP Employment, Services

Thur: Initial Claims, Continuing Claims, Productivity, Unit Labor Costs, Business Inventories, Factory Orders,

Fri: Average Workweek, Non-Farm Payroll, Private Payroll, Hourly Earnings, Unemployment Rate, Consumer Credit

How am I looking to trade?

Protection and still holding onto cash we raised end of last year/beginning of this year

www.myhurleyinvestment.com = Blogsite

info@hurleyinvestments.com = Email

Questions???

https://finance.yahoo.com/news/goldman-traders-see-painful-path-214030246.html

Goldman Traders See ‘Painful’ Path for US Stocks Before Rebound

(Bloomberg) — US equities may need to pull back further before they can mount a durable advance, Goldman Sachs Group Inc.’s trading desk warned, citing fragile sentiment and choppy flows that left the S&P 500 vulnerable after its latest attempt to clear the 7,000 level fizzled.

“The only way up is down from here,” Goldman’s trading desk team including Gail Hafif and Brian Garrett wrote in a note to clients. A broadly supportive macro backdrop has done little to help stocks absorb geopolitical tensions and sharp swings in commodity prices, creating what the bank’s traders called a “painful” near-term path.

The S&P 500 closed little changed on Monday, bouncing back from a steep early loss, as traders debated the potential market impact from an escalating conflict in the Middle East that triggered a spike in oil prices. Crude surged as a near halt to traffic through the Strait of Hormuz and disruption at a big refinery in Saudi Arabia upended energy markets. Brent futures settled about 6.7% higher, near $78 a barrel, the biggest gain since June.

While the spike in oil prices has rattled investors, historical data shows that the damage may be limited. In 22 instances since 2000 when West Texas Intermediate crude jumped 10% or more in a single session, S&P 500 returns beyond the immediate selloff were often positive, the Goldman traders noted. The index fell an average 0.24% the next day, but one-month returns averaged 1.23%, with a median gain of 3.57%, according to Goldman’s data. Spikes in Brent crude showed similar patterns.

Meanwhile, Goldman’s Dom Wilson sees higher oil weighing on equities and credit in the near term, but argues that only a severe, sustained supply disruption would meaningfully damage global growth.

March Headwinds

Yet seasonality also looks mixed in March, according to the Goldman traders. This month ranks as the fourth-worst month for the S&P 500 going back to 1928, with the first half historically choppy. The stretch from March 1 to March 14 averages just a 30 basis-point gain but performance tends to improve, with the two weeks from March 15 averaging an 80 basis-point advance.

Some other highlights from the Goldman trading desk note:

- Retail investors, who have been consistently buying the dip in US stocks, are showing less exuberance this year compared with 2025 amid persistent volatility in the first two months of 2026.

- Corporate buybacks might have provided some support to US stocks, with last week’s repurchase activity running at roughly 1.7 times the 2025 year-to-date daily average and 1.5 times 2024 levels. But that support is about to fade. The next blackout window, during which corporations pause share repurchases, is expected to begin around March 16 and run through the end of April.

- Companies have announced $317 billion in buybacks year-to-date, the second-most active start on record, just behind 2023, but Goldman cautioned that buybacks alone are unlikely to spark a rally, and their removal could amplify weakness.

- Among positive factors, tax refunds could support consumer spending and sentiment into spring. Roughly a quarter of annual refunds are distributed in March, with about three-quarters delivered by end of April.

- Systematic funds have largely stepped back from US equities, but commodity trading advisers are incrementally turning into buyers, the bank’s models show. Yet this dynamic that could shift sharply depending on how market trends evolve.

Apple to move some Mac Mini production to U.S. this year as part of effort to boost domestic manufacturing

Published Tue, Feb 24 20262:44 PM EST

Jennifer Elias@in/jennifer-elias-845b1130/

Key Points

- Apple said it’s moving some of the manufacturing for its Mac Mini to the U.S. as a part of a previously announced $600 billion commitment to domestic manufacturing.

- The company said it’s expanding plans for a Houston production facility.

- Apple has been hit by President Trump’s reciprocal tariffs, and has been cozying up to the administration.

Apple said it’s moving production of some of its Mac Mini computers to the U.S. later this year as the company seeks to bolster domestic manufacturing.

The iPhone maker last year unveiled plans to invest $600 billion in the U.S., with CEO Tim Cook appearing at the White House with President Donald Trump in August for the announcement of a $100 billion outlay. The company also has said it will purchase parts and expand its relationship with U.S. suppliers.

“As part of our $600B commitment, Mac mini will be produced in the US for the first time later this year!” Cook wrote in a post on X on Tuesday. “We’re accelerating our progress even further — producing more AI servers and opening an all-new Apple Advanced Manufacturing Center for hands-on training.”

The Mac Mini is Apple’s compact, more affordable desktop computer, which start at about $600, according to the company’s website. Later this year, production will begin at a new factory in Houston, where Apple started producing AI servers last year, the company said in a statement.

“We began shipping advanced AI servers from Houston ahead of schedule, and we’re excited to accelerate that work even further,” Cook said in the release.

Apple has been hit hard by tariffs imposed by the Trump administration, paying about $3.3 billion since the president initiated the levies last year. Apple is sourcing half of its iPhones for the U.S. from India and most of its other U.S.-bound products like Macs, AirPods and watches from Vietnam.

The Supreme Court on Friday struck down a large chunk of President Trump’s far-reaching tariff agenda, but uncertainty remains after Trump rebuked the decision.

Apple said its 20,000-square-foot advanced manufacturing center in Houston will open its doors later this year. The company said it will provide training in advanced manufacturing techniques to students, supplier employees, and American businesses, teaching them “the same innovative processes that are used to make Apple products.”

JPMorgan turns bullish on Netflix, says streamer is better insulated from AI disruption risk

Published Mon, Mar 2 20267:59 AM EST

Artificial intelligence presents a tailwind rather than a threat for Netflix, according to JPMorgan.

JPMorgan resumed coverage of the streaming giant following a period of restriction. The bank now views Netflix as a buy, up from neutral. Analyst Doug Anmuth’s new price target on Netflix is $120 signals a gain of 25%, though it’s down from a previous forecast of $124.

The upgrade follows Netflix’s decision to walk away from its deal to buy Warner Bros. Discovery after an offer from Paramount Skydance was deemed superior.

Anmuth applauded Netflix’s strong underlying fundamentals. He wrote that the company remains committed to margin expansion.

“We believe NFLX remains a healthy organic growth story, driven by a combination of strong content, global subscriber growth, continued pricing power, & an early-stage/under-monetized Ad tier,” he said. “We expect continued strong FCF generation, & we look for elevated share repurchases in 2026 driven by the $2.8B termination fee & a currently opportunistic share price”

Anmuth also views artificial intelligence as a tailwind, rather than a headwind.

“AI should drive improved content discovery & personalization, better advertising solutions & measurement, & ultimately reduce content production costs. While AI video models such as Bytedance’s Seedance 2.0 and others reduce barriers to content creation, we believe storytelling and talent will remain critical moats, ultimately better insulating NFLX from AI disruption risk compared to transactional business models,” he wrote.

As another upcoming tailwind, Anmuth predicts that Netflix’s viewing hours will continue to grow from here. Viewing hours for Netflix originals already accelerated to 9% in the second half of 2025, and the analyst nodded to the company’s strong content slate for 2026.

Anmuth also sees a U.S. price increase as possible in the middle or latter half of the year. The analyst added that Netflix’s ad revenue is expected to double to around $3 billion in 2026 after growing more than 150% last year.

“We believe NFLX’s scale & streaming leadership position, 3-year growth of double digits for revenue & 20%+ for operating income/GAAP EPS/FCF, & a well-insulated subscription-based model all support a premium valuation,” the analyst wrote.

Netflix Inc

Shares of Netflix have added 3% this year and are down 2% over the past 12 months.