Let’s talk about the difference between implied volatility and realized volatility. (see article below).

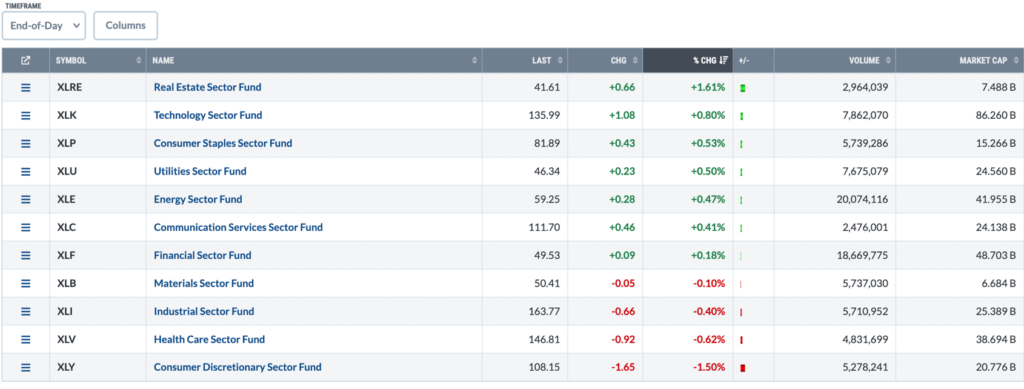

I also want to look at the sectors we are in (heavy in Tech) vs others. We want to be in those stocks that are carrying the overall indexes. That’s Tech.

Earnings –

AA 4/16 AMC

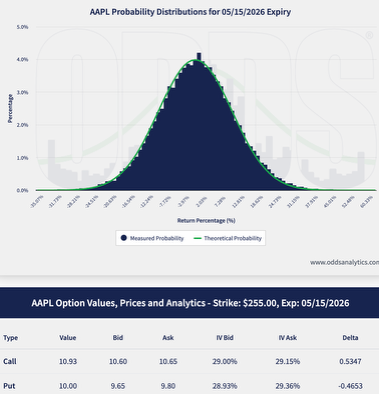

AAPL 4/29 est

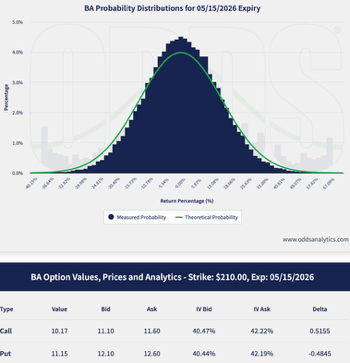

BA 4/22

BABA 5/13 est

BIDU 5/19 est

CB 4/21

CVS 5/06

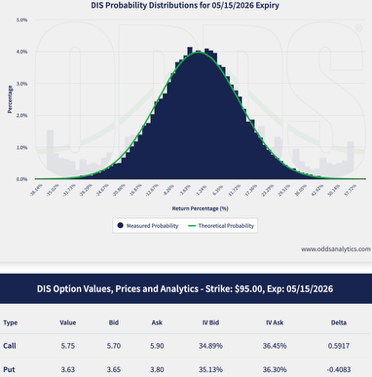

DIS 5/05 est

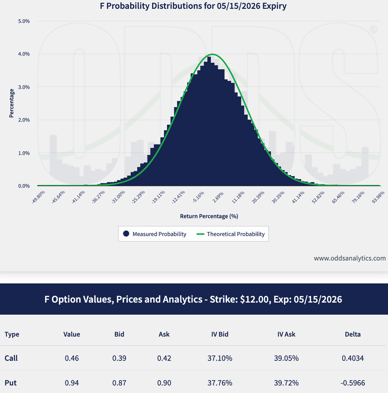

F 4/29

GE 4/21

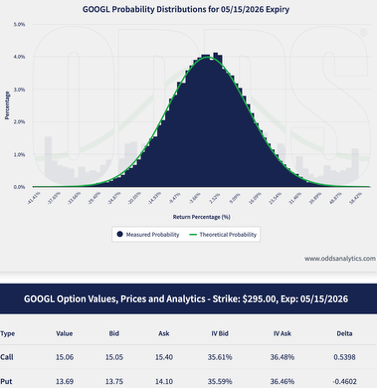

GOOGL 4/22 est

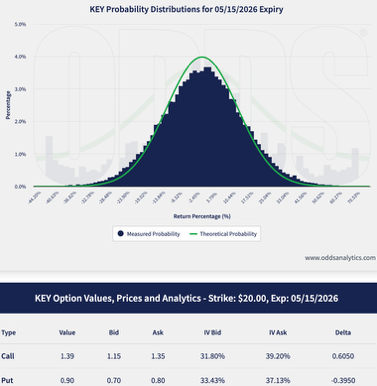

KEY 4/16 est

LMT 4/23

META 4/28 est

MSFT 4/29 est

MSTR 4/29 est

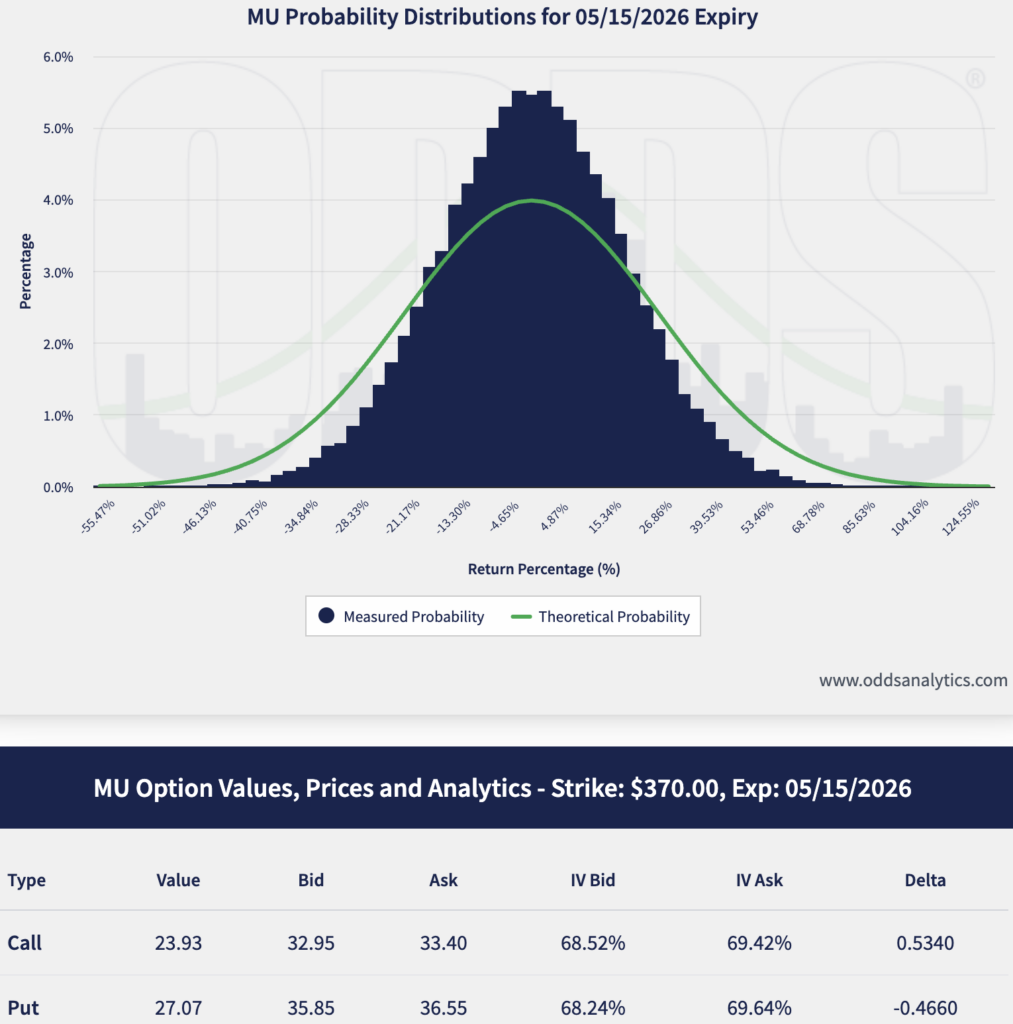

MU 6/23 est

NEM 4/23

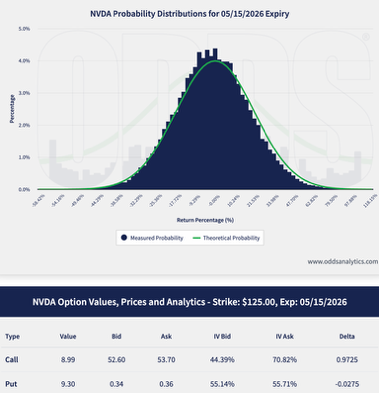

NVDA 5/20

O 5/04 est

OWL 5/03 est

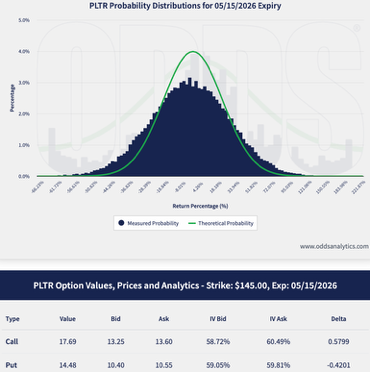

PLTR 5/04 est

UAA 5/11 est

V 4/27 est

VZ 4/27

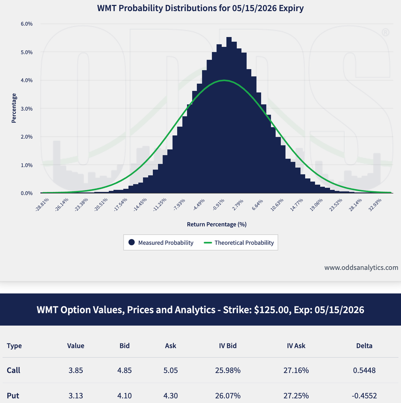

WMT 5/21

https://www.briefing.com/the-big-picture

Fog of war clouds the prior rose-colored outlook

Briefing.com Summary:

*Market sentiment has soured since the start of the war with Iran.

*Earnings estimates have continued to increase, but doubts are surfacing about the achievability of those estimates.

*The market is nearing some red lines that create an opportunity to leg into beaten-down stocks and sectors.

Through February 28, the stock market was looking pretty good. Granted, most of the mega-cap cohort was languishing, but the broader market seemed to be benefiting at their expense, fueled by confidence in the economic, earnings growth, and interest rate outlooks.

One day and one month, though, has made things look and feel differently. On February 28, the U.S. and Israel jointly launched a military campaign against Iran under the pretense of preventing Iran from getting a nuclear weapon, destroying its ballistic missile-making capabilities, and triggering regime change.

The ensuing market response has not been good. The major indices have rolled over; oil prices have skyrocketed 47%; the 2-yr note yield has spiked 53 basis points; the 10-yr note yield has jumped 46 basis points; and expectations for another rate cut this year have been swept away.

Simply put, the fog of war has clouded the stock market’s rose-colored outlook.

Takes Two to Tango

With oil prices rising due to shipping disruptions through the Strait of Hormuz, inflation concerns have increased. That is the genesis of why Treasury yields have risen and why market participants no longer expect a rate cut this year. In fact, the fed funds futures market has assigned a 37% probability to a 25-basis-point hike at the December FOMC meeting, according to the CME FedWatch Tool.

A rate hike in 2026 wasn’t on anyone’s bingo card when the year began, so it goes to show how quickly this geopolitical conflagration has changed the dynamic.

The latter point notwithstanding, the stock market is still harboring hope that the Iran war can end soon and that oil, fertilizer, and other goods can start flowing freely again through the Strait of Hormuz. The main hangup at the moment is that there is no clear sense that Iran harbors the same hope.

It bears repeating that it takes only one party to start a war, but both parties to end it. On that note, just because the U.S. declares the war is over doesn’t mean Iran will consider the war over. That is why the context and the participation around any such declaration are key for the market’s direction of travel.

For now, things are going south in terms of stock prices and bond prices, but not all things are going south. Remarkably, earnings estimates have continued to rise.

On February 27, the forward twelve-month earnings estimate for the S&P 500 was $317.82. Today it is $329.02. With the S&P 500 down 7% in the interim, the result has been multiple compression. The forward 12-month P/E multiple has slipped from 21.7 to 19.7, a slight premium to its 10-year average. For the equal-weighted S&P 500, the forward twelve-month P/E multiple has gone from 17.6 to 15.9, which is a 5% discount to its 10-yr average.

Things have gotten less expensive, but of course, things have also gotten a lot more uncertain and have created misgivings about the achievability of earnings estimates.

Picking Spots

Although the U.S. and Israel started the war with Iran, the reverberations of what is going on are not isolated. They are having far-reaching effects around the globe, with markets in Europe and Asia feeling the pinch of shipping disruptions more acutely than the U.S., since they are highly dependent on energy imports.

The energy price shock for them, then, has a higher voltage than it does for the U.S. Nonetheless, the interconnected global economy is at risk of seeing a slowdown in spending driven by supply chain disruptions that are leading to higher prices for consumers and businesses alike.

Central banks are all grappling with whether to raise rates to combat the inflation pressure. That understanding has driven up sovereign bond yields and has led to flatter yield curves and less conviction in the outlook. Hence, the willingness to buy complacently on any dip has been supplanted by more discernment related to the achievability of earnings estimates.

Market participants are no longer chasing stocks higher. Rather, they are picking spots to average down in an environment where phrases like “stagflation,” “recession,” “rate hikes,” and “tighter financial conditions” are a credible part of the market narrative that is also featuring talk of private credit concerns and AI disruption.

They have a lot of spots from which to choose. Every S&P 500 sector is down since the war began, with losses ranging from 3.2% to 11.5%. The lone exception is the well-situated energy sector (+12.5%). The major indices have fallen between 8% and 12% from their 52-week highs. Only 22% of S&P 500 stocks are above their 50-day moving average, while only 44% are above their 200-day moving average.

The S&P 500 itself is trading below its 200-day moving average (6,635).

Briefing.com Analyst Insight

The stock market has gone from looking supremely confident to looking inordinately shaky. That could change in a hurry if, and when, the U.S., Israel, and Iran are all on the same ceasefire page, and the hope is that concession comes sooner rather than later.

In The Big Picture column we posted on March 5, we identified some red lines that we think President Trump wouldn’t want to see markets cross with velocity. They were $100.00/bbl oil, a 4-handle on the national average for gasoline prices (we’re at $3.98 now, according to AAA), a 4.50% 10-yr note yield, and an S&P 500 that trades below 6,300. The latter would mark a 10% correction from the 52-week high.

We are close in each respect, so it is our expectation that the Trump put will be exercised in some fashion when those lines are crossed. Again, though, for the sentiment tide to turn, there has to be conviction in the belief that Iran is done being at war with the U.S. and Israel as much as the U.S. and Israel are done being at war with Iran and its proxies.

That understanding and when it is no longer in doubt are equally important. The longer the war drags on, the longer the energy price shock and supply chain disruptions will persist and upend global economic activity and lofty earnings estimates.

With the S&P 500 nearing a 10% correction and some other important red lines coming into focus, there is an opportunity to start legging into the market with cash sitting on the sidelines. However, with other issues lurking out there, like the private credit worries, rising mortgage default rates, tariffs, and AI disruption, it is not an “all-in” environment because it is tough to be all-in like before on the achievability of earnings estimates.

—Patrick J. O’Hare, Briefing.com

(Editor’s Note: the next installment of The Big Picture will be posted the week of April 6.)

Where will our markets end this week?

HIGHER

DJIA – Bearish

SPX – Bearish

COMP – Bearish

Where Will the SPX end April 2026?

04-06-2026 +2.5%

Earnings:

Mon:

Tues: LEVI

Wed: DAL,

Thur: BB, WDFC

Fri:

Econ Reports:

Mon: ISM Services,

Tue Durable Goods, Durable ex-trans, Consumer Credit,

Wed: MBA, FOMC Minutes

Thur: Initial Claims, Continuing Claims, Personal Income, Personal Spending, PCE, PCE Core, GDP GDO Deflator, Wholesale Inventories,

Fri: CPI, Core CPI, Factory Orders, Michigan Sentiment, Treasury Budget

How am I looking to trade?

www.myhurleyinvestment.com = Blogsite

info@hurleyinvestments.com = Email

Questions???

https://www.investing.com/analysis/is-the-vix-lying-200677501

Is The VIX Lying?

Expected and historical (realized) volatility are sending investors a puzzling signal. Because of the Iran conflict, intense oil price swings, and rising interest rates, the VIX, or implied volatility (what options markets are pricing in as future fear), is elevated.

However, actual realized volatility has been much more subdued. That gap between the VIX and realized volatility is wider than historical norms, thus worth examining. The graph below shows the difference between the VIX and realized volatility, measured in standard deviations (Sigma). Currently, the gap is over two sigma’s, a somewhat rare event.

The bearish interpretation is that the VIX is telling the truth and realized volatility is the lie. Options markets are pricing in risks that the equity market has not yet acknowledged. Simply, investors are paying a steep premium for protection against a shock that the market has not priced in. The bearish scenario is the gap closing with realized volatility catching up to implied volatility.

The bullish interpretation is that realized volatility is low because the underlying economy, despite higher oil prices, remains reasonably healthy and corporate earnings are unlikely to be significantly affected. Accordingly, the market is treating the Iranian conflict and surge in oil prices as a temporary disruption rather than a structural shock.

Thus, the bullish scenario is that the gap closes not through a realized volatility spike but through a gradual decline in implied volatility as the geopolitical situation stabilizes.

Both interpretations are defensible. When VIX, the market’s fear gauge, and actual volatility are telling different stories, paying close attention is warranted.

Powell sees inflation outlook in check, no need to hike rates because of oil shock

Published Mon, Mar 30 202611:40 AM EDTUpdated Mon, Mar 30 20263:34 PM EDT

Jeff Cox@jeff.cox.7528@JeffCoxCNBCcom

Key Points

- Federal Reserve Chair Jerome Powell said that he sees inflation expectations as being grounded, even as energy prices rise.

- In the near term, the right move is to look beyond the short-term gyrations of the energy market and concentrate on the Fed’s goals of stable prices and low unemployment, Powell said.

- The central bank leader said that the current shake-up in the private credit space doesn’t seem to have the makings of a broader systemic event.

Fed Chair Powell: Inflation expectations appear to be well anchored beyond the short term

Federal Reserve Chair Jerome Powell, in a wide-ranging talk at Harvard University, said Monday that he sees inflation expectations as grounded despite rising energy prices so the central bank doesn’t need to respond with higher interest rates.

As his term leading the central bank nears an end, Powell avoided questions about the longer-term direction of interest rates or inclinations his designated successor has espoused.

In the near term, he said the proper move is to look beyond the short-term gyrations of the energy market and focus on the Fed’s goals of stable prices and low unemployment.

“Inflation expectations do appear to be well anchored beyond the short term, but nonetheless, it’s something we will eventually maybe face the question of what to do here,” he said during a question-and-answer question with a moderator and students. “We’re not really facing it yet, because we don’t know what the economic effects will be, but we’ll certainly be mindful of that broader context when we make that decision.”

As he has in the past, Powell said he believes the current rate target, in a range between 3.5%-3.75%, is “a good place” for the Fed to sit as it observes events currently playing out, including the Iran war and the impact tariffs are having on prices.

The comments appeared to register in financial markets, with traders no longer pricing in a significant chance of a rate hike this year. As recently as Friday morning, markets were looking at a better than 50% probability of a quarter percentage point increase amid expectations the Fed would react to the surge in energy costs. However, odds of a hike by December fell to 2.2% after Powell’s appearance.

Powell said raising rates now could have negative effects on the economy later. He noted that Fed rate moves have a lagged impact on the economy, so tightening here wouldn’t help the inflationary impact of the Iran war.

“By the time the effects of a tightening in monetary policy take effect, the oil price shock is probably long gone, and you’re weighing on the economy at a time when it’s not appropriate. So the tendency is to look through any kind of a supply shock,” he added.

Market-based measures such as breakeven rates in Treasury yields indicate few fears of an inflation spike. Breakevens measure the difference between Treasurys and inflation-indexed securities. The five-year breakeven rate most recently was around 2.56% and trending lower over the past 10 days.

Powell’s term ends in mid-May, and President Donald Trump has nominated former Governor Kevin Warsh as the next chair. However, Warsh’s nomination is being held up in the Senate Banking Committee as U.S. Attorney Jeanine Pirro continues her investigation into renovations at Fed headquarters.

Though a judge threw out a subpoena Pirro’s office issued to Powell, she has appealed the decision. While the case is being adjudicated, Sen. Thom Tillis, R-N.C., has vowed to prevent the nomination from going through.

For his part, Warsh has stated a preference for lower interest rates than the current level. Asked to comment on his successor’s plans, Powell said, “I’m not going to swing at that pitch.”

Regarding private credit, Powell noted rising defaults, investor withdrawals and concerns about wider issues in the $3 trillion sector.

“I’m reluctant to say anything that suggests that we’re dismissive of the risk, but we’re looking for connections to the banking system and things that might result in contagion. We don’t see those right now,” he said. “What we see is a correction going on, and certainly there’ll be people losing money and things like that. But it doesn’t seem to have the makings of a broader systemic event.”