HI Market View Commentary 08-12-2019

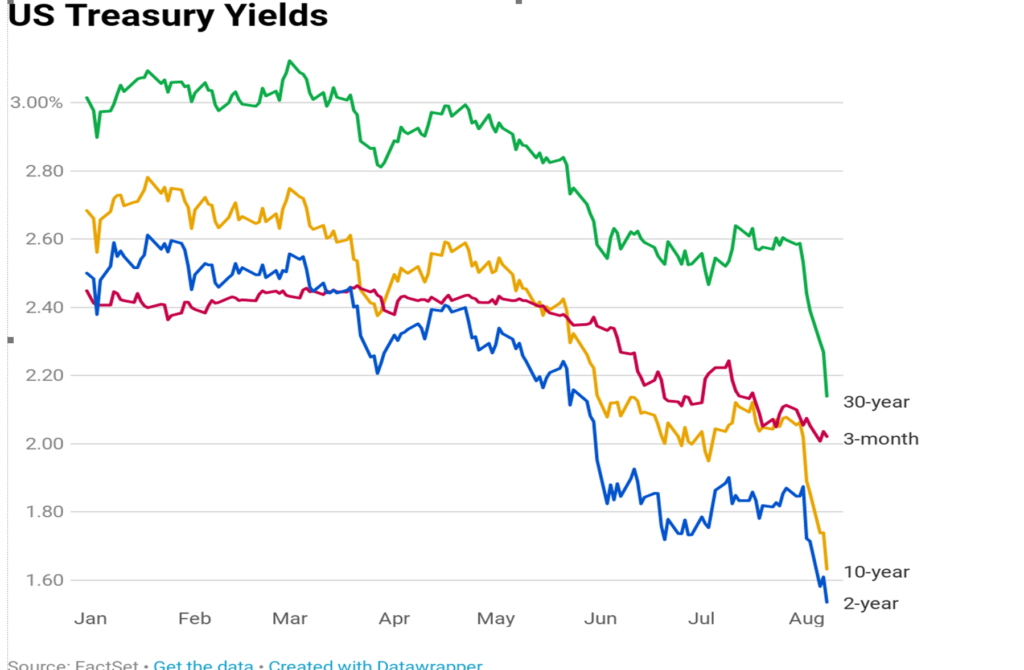

Right now we have the equity market and bond market moving in unison

Right now 60% of dividend paying stocks and the S&P 500 1.98% Dividend Yield is higher then ahte ten year treasury at 1.649%

SO why is this a problem? – VALUATIONS

Valuation is the relative pricing of stocks and equity, indexes, compared to past performance

The market has no clue on where to value itself!!!!!

Nobody knows if it is cheap, expensive or fair valued

Going forward Sept, Oct scare me and I would expect a big drop in one of those months

So what changes the narrative?

China progress in September, a weaker dollar that can’t happen because we are the reserve currency, lowering interest rates will only cause more of the same thing that is happening right now

As a money manager what is your biggest concern? Are we (U.S.) going to go through the 2008 reset on our market like we should have done 11 years ago

How high could gold and silver go?

Where will our markets end this week?

Higher

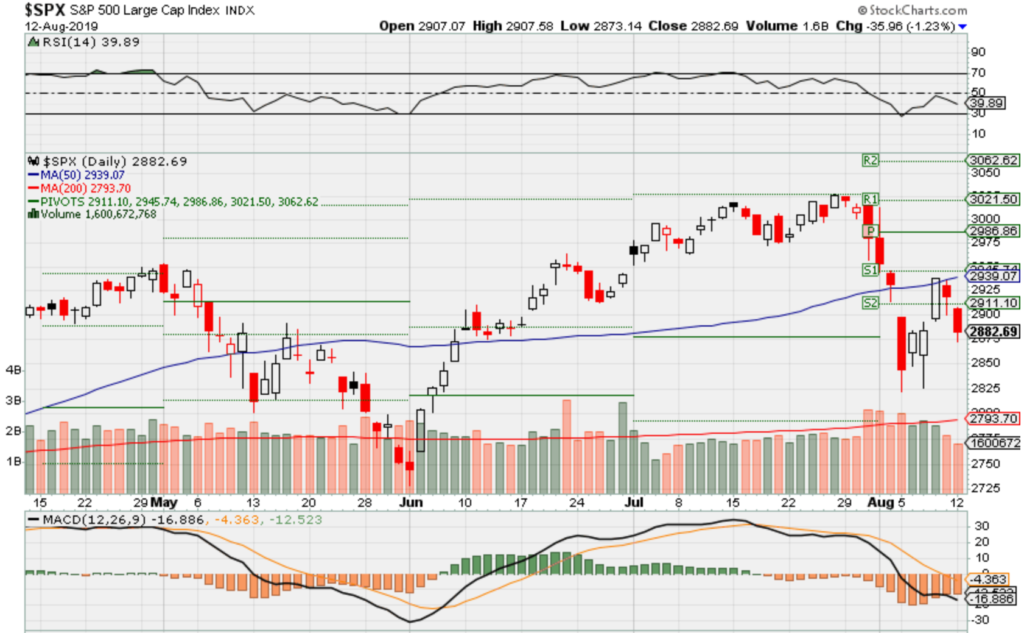

DJIA – Bearish

SPX – Bearish

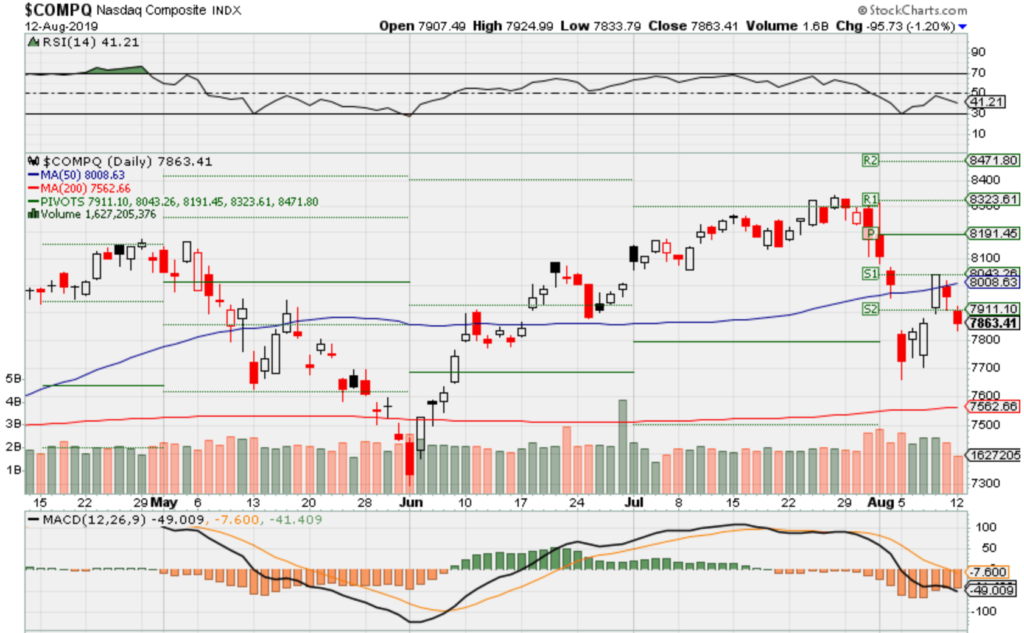

COMP – Bearish

Where Will the SPX end Aug 2019?

08-12-2019 -1.0%

08-05-2019 0.0%

07-29-2019 +0.5%

Earnings:

Mon: SYY

Tues: JD

Wed: M, A, NTAP, CSCO

Thur: BABA, WMT, JCP, TPR, DDS, NVDA

Fri: DE

Econ Reports:

Mon: Treasury Budget

Tues: CPI, Core CPI

Wed: MBA, Import, Export

Thur: Initial, Continuing, Retail Sales, Retail ex-Auto, Phil Fed, Productivity, Unit Labor Costs, Industrial Production, Capacity Utilization, Business Inventories,

Fri: Housing Starts, Building Permits, Michigan Sentiment, MONTHLY OPTIONS EXPIRATION

Int’l:

Mon –

Tues –

Wed – CN: Retail Sales, Industrial Production

Thursday –

Friday- CN: Foreign Direct Investments (YOY) (YTD)

Sunday –

How am I looking to trade?

I’m preparing for earnings = Adding long puts

BIDU – 8/19 est

MU – 9/19 est

MRVL 9/05 est

www.myhurleyinvestment.com = Blogsite

customerservice@hurleyinvestments.com = Email

Questions???

So why haven’t you protected everything yet?

https://seekingalpha.com/article/4284844-fundamental-analysis-disney

A Fundamental Analysis Of Disney

Aug. 12, 2019 11:32 AM ET

Summary

Disney posted underwhelming earnings results for their most recent fiscal quarter.

Disney is still a fundamentally well-positioned company.

Despite volatility in the macroeconomy, Disney is a long-term investment worth considering.

If you’re interested in the lore of equity investing, you’ve probably heard of William O’Neil, one of the most successful stockbrokers and investors in American history. It probably doesn’t surprise you, then, to hear that O’Neil is featured in “Market Wizards” – my current reading. In the book, O’Neil describes his judgment structure for gauging a winning stock pick. It’s called the CANSLIM system. Here’s a brief summary:

- The “C” stands for current earnings per share. “The best performing stocks showed a 70 percent average increase in earnings for the current quarter over the same quarter in the prior year before they made their major advance.”

- The “A” stands for annual earnings per share. O’Neil’s research showed that outstanding growth companies had a five-year average annual compounded earnings growth rate of 24% or higher.

- The “N” stands for something new. New can mean a new service or product, new management, a new high in stock price, or some new change in the industry.

- The “S” stands for shares outstanding. Stocks with the strongest performance had fewer than 25 million shares of outstanding when they hit their stride.

- The “L” stands for leader or laggard. Leading stocks with high relative strength values are the most effective way of earning a profit. O’Neil restricts his equity buys to companies with relative strength ranks above 80.

- The “I” stands for institutional sponsorship. Leading stocks have institutional backing, however excessive sponsorship is not desired because it would be a large source of selling should anything go wrong with the company or general industry.

- The “M” stands for market. “Three-quarters of stocks will move in the same direction as a significant move in the market averages. That is why you need to learn how to interpret price and volume on a daily basis.”

Source: Schwager, Jack. “Market Wizards”

Clearly this is a very restrictive list of criteria. While I don’t entirely subscribe to O’Neil’s process, I can appreciate his fundamental points: Strong companies earn. Strong companies are fundamentally sound. Strong companies are innovative. Strong companies are leaders. Strong companies compete. A lasting company has ways to dynamically change with the business and social environments in which they operate. Disney can do – and does – all of these things. The overreaction to Tuesday’s (8/6) earnings report will subside. In the long term, Disney is a green-light investment for all types of investors.

Recent Price Action

{kind=link}

I always like to provide context on where we are before jumping to analysis. Here’s a one-year candle chart & single moving average line showing the recent price action on DIS. On April 11th Disney announced the November launch date for Disney+, which explains the 20% upward price explosion. There is a strong price support level around the $130 mark, and even with the recent selloff Disney is comfortably above that level. Lately there’s been some unsteady movement with the stock, but with the volatility in the macroeconomy we can expect Disney to see some shakiness. Price volatility in the short term is anticipated, but long-term growth should see an uptrend as Disney continues to innovate and grow.

Business Model Summary

Operationally, Disney separates their business into two categories: ‘Media Networks’ and ‘Parks, Experience & Products’.

Media Networks

Disney’s most prominent operations in this category include Disney, ESPN, FX, National Geographic, ABC, and Freeform television networks. Disney also owns or has high equity stakes in multiple other TV networks that require efforts in producing and distributing content (ex: a 50% stake in A+E Television Networks, which operates networks such as HISTORY and Lifetime). Revenues are generated through affiliate fees, advertising, and TV/SVOD distribution. Expenses in this category are primarily production and programming costs, SG&A costs, and depreciation and amortization. Disney+ is a new and significant component to this media product mix.

Parks, Experience & Products

This category involves operating some of the most recognizable theme parks in the world, such as Walt Disney World Resort, Disneyland Resort, Disneyland Paris, Hong Kong Disneyland Resort, and Shanghai Disney Resort. Disney also licenses IP to a third-party operator in Tokyo for the Tokyo Disney Resort. This part of the business model also includes something called ‘consumer products operations,’ which essentially means the selling and licensing of Disney-branded merchandise and IP to manufacturers, retailers, game developers, etc., who want to use Disney-owned content for their businesses. Disney generates revenue in this category primarily through theme park admissions, food & beverage, and licensing fees. One thing worth noting – parks will see much higher capital expenditure need as new/updated equipment is needed for safety, park expansion, technological improvements, etc.

Quarter Financial Performance

On the top line, things didn’t look too bad. As compared to the previous year quarter, Disney saw ‘Media Network’ revenue rise 21%, ‘Parks, Experience & Products’ revenue rise 7% (despite attendance drops of 3%), ‘Direct-to-Consumer & International’ revenue rise 367%, and ‘Studio Entertainment’ revenue rise 33%. Offsetting these revenue jumps was a total expense growth of 61%. The addition of Fox and Hulu operations were the source of the expense surge as large amounts of capital were required to integrate operations & assets into the business. EPS fell to $1.35 per share from $1.87per share in the prior year quarter, and EPS for the 9 months ended June 29, 2019 fell to $5.98 from $6.81 in the prior year period. That being said, Disney has a decent scapegoat. Disney specifically cited Fox films “X-Men: Dark Phoenix” and “Alita: Battle Angel” as the reasons for the low earnings mark. Combined, the production of the films cost about $520 million, but generated a domestic total of only $150 million. Regardless, the 24-hour period following the earnings report saw some unhappy headlines.

The Fundamentals

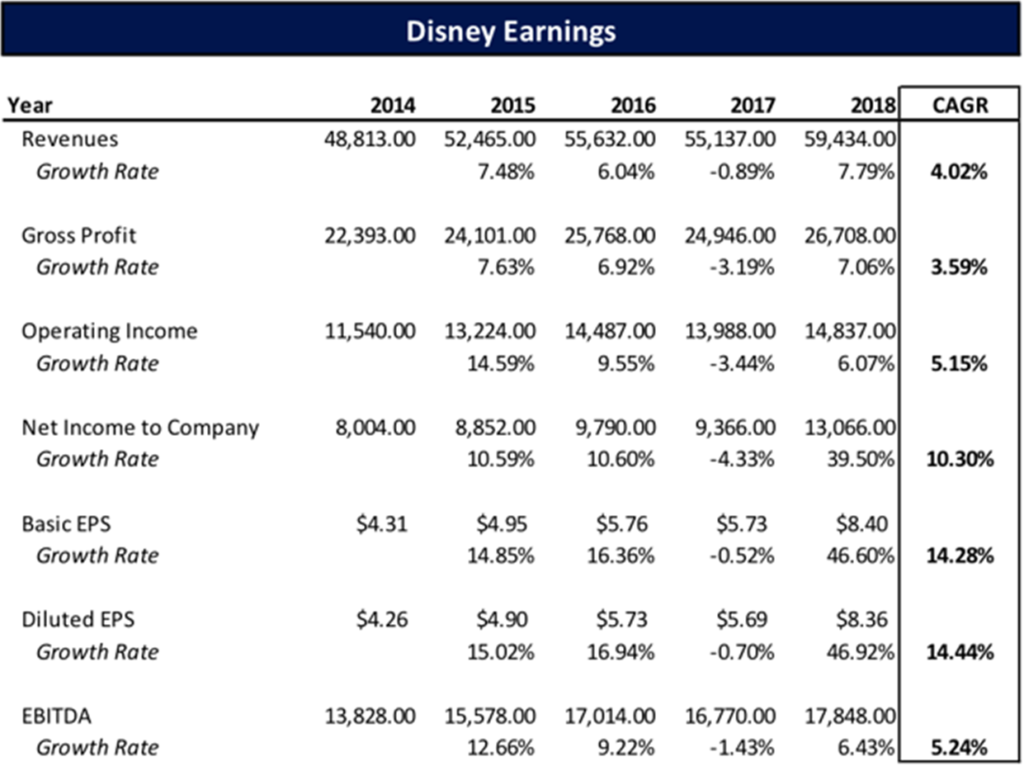

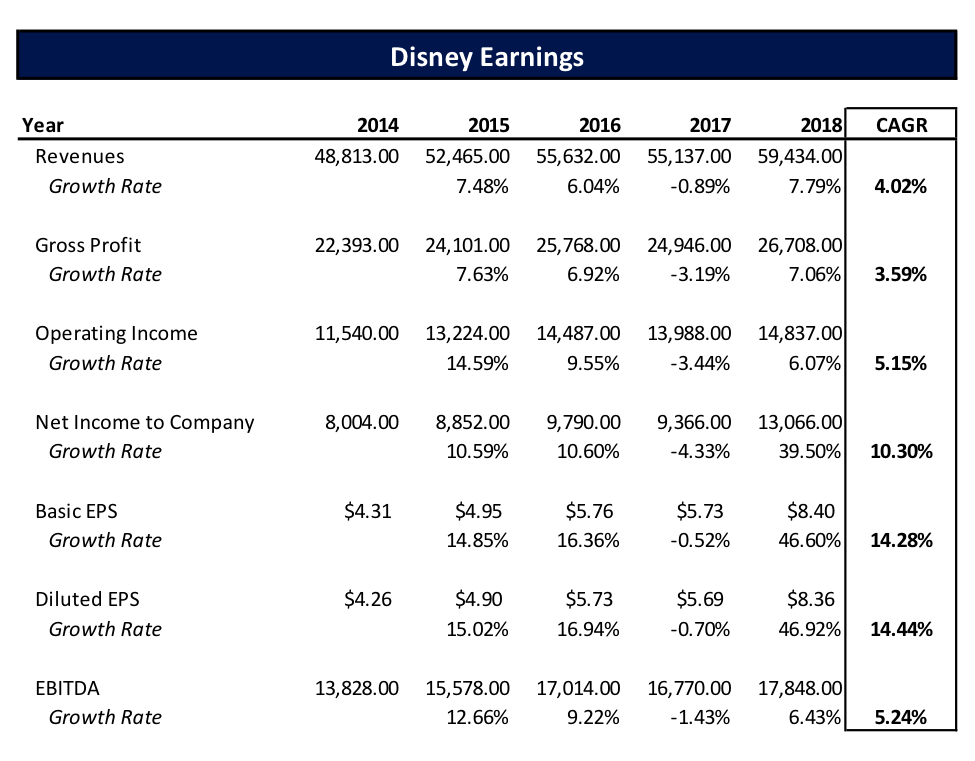

Disney Earns.

We’re looking at Disney as a long-term play. Let’s distance ourselves from the most recent quarterly results and check on YOY growth in some key line items:

{kind=link}

A 5-year glance shows a consistent CAGR in revenues, gross profit, operating income, net income, EPS, and EBITDA over the past five years. FY 2017 saw disappointing results, but Disney bounced back hard in FY 2018. These EPS numbers might not match the CANSLIM criteria, but 5-year growth of nearly 15% is a great number for a company of this size.

One note – the development of Disney+ is going to weigh on earnings. Pouring cash into a new streaming service isn’t going to look great on the books in the near term. Disney knows this, and finance chief Christine McCarthy has already publicly stated that the company expects an approximate $900 million loss in the Direct-to-Consumer division for the quarter ending in September. In fact, Disney isn’t projected to turn a profit on its streaming business until 2024. The context here is that Disney is a giant that can still generate enough cash through other ventures to allow for dumping billions into Disney+. Cash is always required for growth, and Disney has an excellent investment track record.

Disney is Fundamentally Sound.

Brands matter – and Disney has one of the best in the world. In 2016, Brand Finance ranked Disney the number 1 brand in the world. Brand Finance specifically noted Disney’s “many acquisitions and the powerful brands it has brought under its control.” Disney is also the creator/owner of some of the best film series ever, including “Avengers,” “Star Wars,” and classics like “The Lion King.” Future installments of these movies will command extremely high viewership and profits. In total, the company is home to over 740 movies (not including Fox movies). Disney has leveraged their success in the film industry to drive success in their world-renowned theme parks as well, which draw some of the biggest attendance numbers for venues across the world. On top of all this, Disney is a prominent player in the TV market. They own big names (ESPN, ABC, National Geographic) which expand reach into audiences that may not have originally interacted with the Disney franchise. When you syndicate all these components under one roof, you end up with a far-reaching profit producing powerhouse that has a number of competitive advantages and high growth potential.

Disney is Innovative.

Ranked as 2019’s ‘Most Innovative Company’ by Fast Company, Disney continues to make innovative moves in the business world. Bob Iger (Disney CEO) began acquiring companies like Pixar and Lucasfilm years ago with the goal of making Disney the foremost player in the movie industry. He was validated, as Disney in 2016 became the first movie studio to ever make over $7 billion at the box office. When Disney saw declining ESPN viewership through traditional cable networks, they pivoted, and began brainstorming ways of getting ESPN and the Disney brand involved with the rise in demand for easy access streaming. This led to the creation of Disney+, one of the most highly anticipated streaming service releases in the past decade. Whether it’s creating new animations for theme parks, reaching new audiences through acquisitions and repositioning services, or bundling platforms to create a never-before-seen streaming service, Disney is doing it.

Disney is a Leader.

In 2018 the Themed Entertainment Association ranked the world’s most popular theme parks. Eight of the top ten were owned by or affiliated with Disney. The most popular of the bunch, Walt Disney Attractions, saw over 157 million visitors last year. The number 2 ranked park didn’t see half that. With the newfound ability to integrate Star Wars characters into their theme parks, Disney’s 2019 EOY theme park visitation is expected to skyrocket. With regard to television, ESPN is by far and away the most watched cable prime networkin terms of total viewers. Additionally, ABC was the overall 3rd most-watched network in 2018. Disney also holds the rights to 4 of the top 5 highest grossing movies in history (Endgame, Avatar, The Force Awakens, Infinity War). Soon, Disney is going to be a major player in streaming platforms with the introduction of Disney+, which will arrive in November. In one way or another, Disney is at the front of the pack in nearly every business segment with which they involve themselves.

Disney Competes.

Streaming giant Netflix is Disney’s main obstacle to becoming number 1 in the streaming industry – and Disney is taking them head-on. Disney+ will be available on its own for $6.99, and available as a bundle with ESPN+ and Hulu for a price of $12.99(!). Streaming aside, that combo looks like a decent replacement for a full traditional cable package. $12.99 is the same price as Netflix’s most popular price plan, and as the market for streaming services becomes more saturated, there’s going to be a real battle for subscribers. I’m not saying the streaming industry is a zero-sum game, but the introduction of Disney+ is going to make it very difficult for Netflix to raise prices. Either way, Disney is showing no reluctance in attacking an industry colossus.

Disney and the CANSLIM

“To say that a stock is undervalued because it is selling at a low P/E ratio is nonsense… A common mistake a lot of investors make is to buy a stock solely because the P/E ratio looks cheap. There is usually a good reason why a P/E ratio is low… Another common mistake is selling stocks with high P/E ratios… There is no correlation between dividends and a stock’s performance… I rarely pay any attention to overbought/oversold indicators (William O’Neil).” It’s fascinating how O’Neil became so successful while ignoring some of the must-have indicators for other investors. You can’t read an analyst report these days without seeing “P/E ratio” plastered to the page in 15 different places. That’s what makes the market a beautiful place; there’s no one-size-fits-all strategy that’s needed for success. I looked at the numbers for Disney after writing this article, but nothing I saw changed my opinion. It’s clear that this is a company poised for long-term growth and strong performance. Maybe it wouldn’t pass the CANSLIM test, but I think O’Neil would see the value.

Conclusion

If you’re a Disney shareholder it hurts to see a down quarter, but don’t let one slow quarter dissuade you from seeing the bigger picture. Disney has too many things going for them for shareholders to be concerned about performance. There’s *always* an overreaction to subpar earnings reports. The fundamentals are there for Disney, and it’s a long-term keeper.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

The yield curve everyone’s worried about is inches away from flashing a recession signal

PUBLISHED THU, AUG 8 2019 2:00 PM EDTUPDATED THU, AUG 8 2019 6:49 PM EDT

KEY POINTS

- The Treasury yield curve — the obscure plot of U.S. interest rates based on maturity dates — is sloping even more downward, threatening to send 10-year rates below 2-year rates.

- An inversion of the 2- and 10-year yields has preceded every recession over the past 40 years.

- While any inversion doesn’t guarantee a recession, “it’s a harbinger of elevated recession risks,” Bank of America’s Mark Cabana tells CNBC.

The dramatic scramble for U.S. debt as a safe haven has pushed a bond market recession indicator inches away from the warning zone.

The Treasury yield curve — the obscure plot of U.S. interest rates based on maturity dates — is sloping even more downward and threatening to send 10-year rates below 2-year rates.

The yield on the 10-year Treasury note — an important rate banks use when setting mortgage rates and other lending — is in free fall, plunging more than 40 basis points over the last month.

But the 2-year rate, more sensitive to changes in Federal Reserve policy, hasn’t fallen as much and has been kept in check after the central bank suggested it may not cut rates as fast as some had hoped.

That has narrowed the relative return long-term investors enjoy for lending to the U.S. government over the long term. In fact, loaning to Uncle Sam for 10 years only earns a long-term bond investor 1.76%, just 13 basis points — or 0.13 percentage point — above the expected return on the much-shorter 2-year Treasury note, currently trading at 1.63%.

To be sure, portions of the yield curve have been inverted for months, with the rate on the 3-month Treasury bill first rising above that of the 10-year note in March. Any such inversion tends to signal lower growth and inflation, as well as bad credit in the near-term.

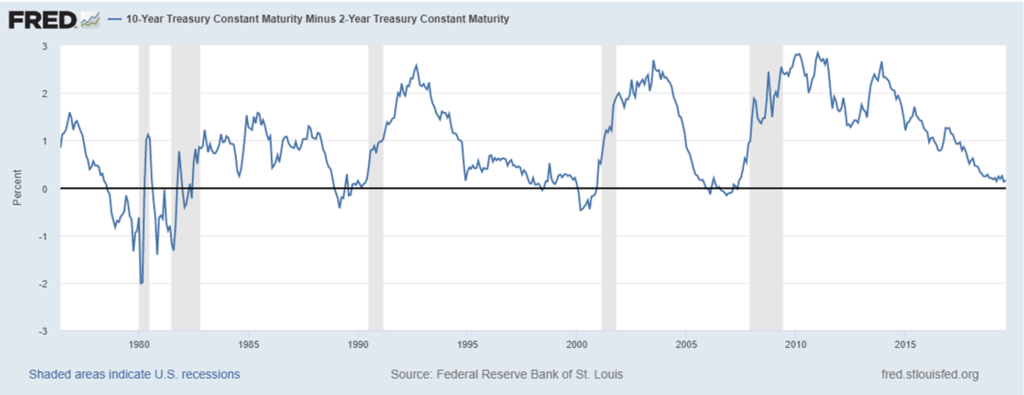

But despite the early signal, many fixed income investors opted to wait for an inversion of the 2-year and 10-year note yields, seen by many as the more meaningful indicator. Investors often give the spread between the 10-year and the 2-year special attention because inversions of that part of the curve have preceded every recession over the past 40 years.

Historical inversions of the 10-2 spread, recessions in gray

Source: Federal Reserve Bank of St. Louis

While abstract and largely ignored during times of economic health, the yield curve is normally represented by an upward-sloping line, illustrating the increasing amount the U.S. government doles out to bondholders in tandem with how long they’re willing to loan Washington cash. However, its usual upward shape can flatten or invert when investors think economic growth is likely to fall.

And while an economic downturn wasn’t as obvious in late 2018, investors now appear more certain that U.S. growth could be set for a slump following two critical policy errors, according to Mark Cabana, head of U.S. short rate strategy at Bank of America Merrill Lynch.

The combination of an intensifying U.S.-China trade war and a less-sympathetic Fed are convincing investors that a downturn is more likely, boosting demand for long-term bonds.

“On trade, obviously the escalation isn’t good for global growth, and the longer it persists, the worse it is for the global economic backdrop,” Cabana told CNBC. “The Fed isn’t getting ahead of this enough. They characterized their rate cut as a ‘midcycle adjustment’ … that clearly isn’t what the market feels is necessary.”

To be sure, while every recession in the modern era has been foretold by an inversion, there have been a few “false alarms” along the way.

“It doesn’t mean you will have a recession. It does not bring about recession,” Cabana said. “But it clearly shows there’s more demand on the long end. It’s a harbinger of elevated recession risks.”

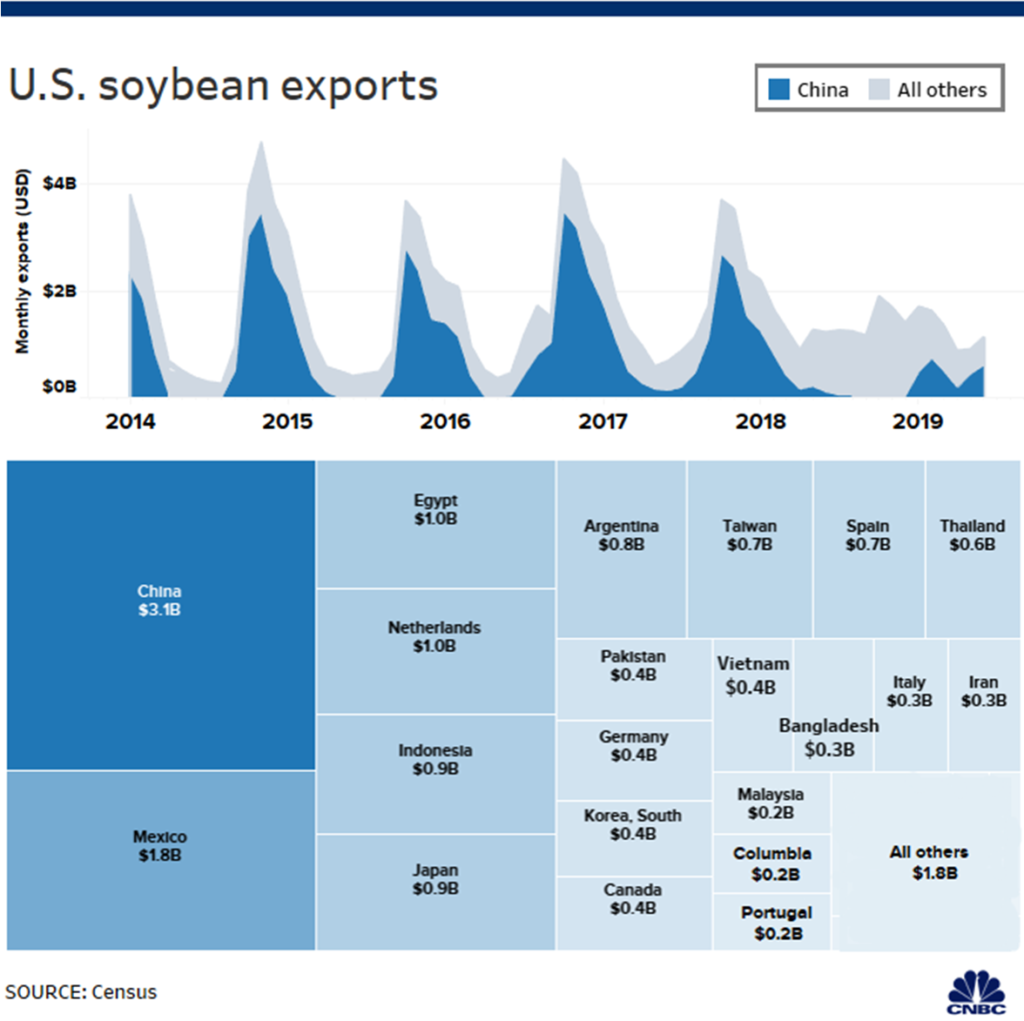

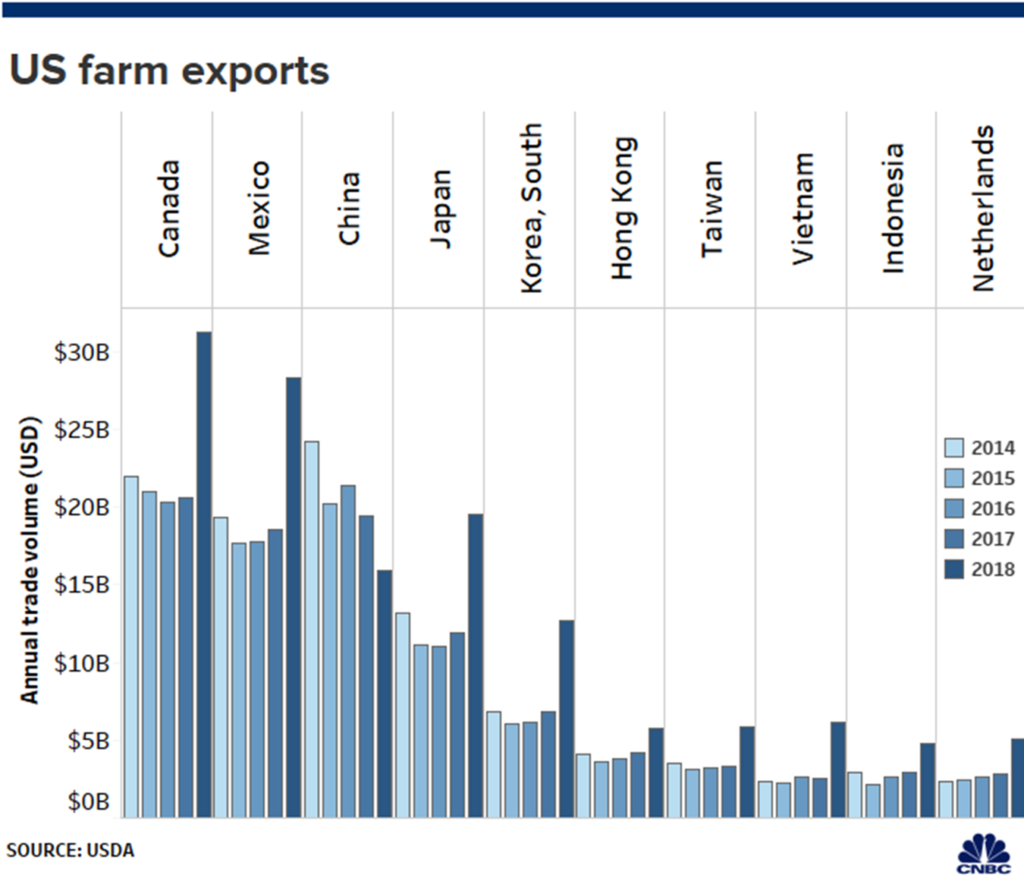

‘Trump is ruining our markets’: Struggling farmers are losing a huge customer to the trade war — China

PUBLISHED SAT, AUG 10 2019 9:15 AM EDTUPDATED 2 HOURS AGO

KEY POINTS

- U.S. farmers lost their fourth largest export market after China officially cancelled all purchases of U.S. agricultural products, a retaliatory move following President Donald Trump’s pledge to slap 10% tariffs on $300 billion of Chinese imports.

- China’s exit piles on to a devastating year for farmers, who’ve struggled through record flooding and droughts that destroyed crop yields, and trade war escalations that have lowered prices and profits this year.

- “It’s really, really getting bad out here,” Bob Kuylen, a farmer of 35 years in North Dakota, told CNBC. “There’s no incentive to keep farming, except that I’ve invested everything I have in farming, and it’s hard to walk away.”

U.S. farmers lost one of their biggest customers after China officially cancelled all purchases of U.S. agricultural products, a retaliatory move following President Donald Trump’s pledge to slap 10% tariffs on $300 billion of Chinese imports.

China’s exit piles on to a devastating year for farmers, who have struggled through record flooding and an extreme heat wave that destroyed crop yields, and trade war escalations that have lowered prices and profits this year.

“It’s really, really getting bad out here,” said Bob Kuylen, who’s farmed for 35 years in North Dakota.

“Trump is ruining our markets. No one is buying our product no more, and we have no markets no more.”

Agriculture exports to China dropped by more than half last year. In 2017, China imported $19.5 billion in agricultural goods, making it the second-largest buyer overall for American farmers. In 2018, that dropped to $9.2 billion as the trade war escalated, according to the United States Department of Agriculture.

This year, China’s agricultural imports from the U.S are down roughly 20%, and U.S. grain, dairy and livestock farmers have seen their revenue evaporate as a result. Over the last 6 years, farm income has dropped 45% from $123.4 billion in 2013 to $63 billion last year, according to the USDA.

Kuylen, who farms roughly 1,500 acres of wheat and sunflowers, lost $70 per acre this year, despite growing good crops. Current government subsidies only cover about $15 per acre, he said.

“There’s no incentive to keep farming, except that I’ve invested everything I have in farming, and it’s hard to walk away,” he said.

“When four to five generations ahead of you have succeeded, and you come along and fail, you don’t see it as not your fault. You snap.”

Zippy Duvall, president of the American Farm Bureau Federation, said China’s exit is a “body blow to thousands of farmers and ranchers who are already struggling to get by.”

China’s exit will most impact U.S. grain farmers. China is the world’s top buyer of American soybeans, buying about 60% of U.S. soybean exports last year. Analysts estimate that soybean prices have dropped 9% since the beginning of the trade war. Soybean exports to China have dropped by 75% from September 2018 to May 2019, compared to the same nine-month period in 2017 and 2018, according to data from the USDA.

“It’s killing us,” said Mark Watne, a wheat and soybean farmer who is president of the North Dakota Farmers Union. Watne said he lost $3 per bushel of soybeans he planted this year.

The U.S. currently leverages 25% tariffs on $250 billion in Chinese goods, while China tariffs on U.S. imports are currently at $110 billion. China will also consider imposing tariffs on U.S. agricultural imports it has already purchased.

Trade war bailout

In May, the Trump administration rolled out a $16 billion federal aid package for farmers. On Tuesday, a day after China announced its exit from U.S. agriculture, Trump promised farmers that China’s mounting attacks on the U.S. farm sector won’t hurt them, and promised more aid in 2020 if necessary.

More than 2,300 counties that voted for Trump in 2016 have received money from the bailout program, and counties that flipped from voting for Barack Obama in 2012 to Trump in 2016 were more likely to get money than counties that were red during both elections, according to Environmental Working Group data obtained by the Washington Post.

Some farmers say the billions in bailouts and rounds of subsidies they’ve received thus far have failed to cover enough of their profit losses. Many say they’d rather make a profit in the marketplace than through a government program.

“I’m happy for the $16 billion, but I’d much rather get it from the marketplace,” Watne said. “The reality is I can’t. It’s going to be too little, too late for some farmers.”

“They should start thinking about another major bailout,” he added. “Either you let a bunch of farmers go broke or you do another payout.”

Allen Williams, who’s farmed for nearly 50 years in Illinois, said the trade war benefits no one, and that the government subsidies are an unjust expense for taxpayers. Subsidies have covered 8% of his gross receipts this year.

“I’m very grateful to get subsidies, but they won’t result in making a loss into a profit for most grain farms,” he said.

“And I don’t think it’s right for the American taxpayer to subsidize this segment of the economy just because of what I see as a mistake of a trade war,” he added.

Loyalty to Trump

Farmers are an important voting base for Trump, who is running for reelection next year. While he’s given no indication of backing off in the trade war, struggling farmers appear to remain loyal.

Trump’s overall approval rating is 79% among farmers, according to a Farm Pulse survey taken last month. And arecord-high number of farmers, some 78%, said the trade war will ultimately benefit U.S. agriculture, according to a July survey from Purdue Center for Commercial Agriculture. More than 75% of rural farmers voted for Trump in the 2016 election.

Mike Knipper, a grain farmer from Iowa who likes some of Trump’s policies and dislikes others, said that most farmers in his community are Trump supporters who will continue to support him through the trade war.

“It doesn’t matter who is president. People like Trump and will support him, and few will change their ideas,” he said.

“Everyone’s willing to see this through, and those government subsidy checks might help them get by for another year.”

Kulyn, the North Dakota farmer who does not support Trump, said he was frustrated that many in his community were still supporting the president despite trade issues.

“A lot of farmers are in love with Trump. People say the problems have nothing to do with Trump,” he said. “Don’t complain to me how badly you’re doing, and support the person that put you there. It’s terribly frustrating.”

— Graphics by CNBC’s John Schoen

https://seekingalpha.com/article/4283710-armour-positioned-comeback

Under Armour: Positioned For A Comeback

Aug. 9, 2019 4:30 AM ET

Summary

Following a difficult few years and subsequent restructuring plan, Under Armour is more focused and determined to succeed.

Athletic apparel industry has favorable economics and Under Armour is positioned to benefit.

As its cost structure is optimized and margins return to historic levels, earnings power should reaccelerate.

In the Saga Partners Investor Letter sent out this week, we provided an update to our investment in Under Armour (UA, UAA). Below is the excerpt from the recent letter.

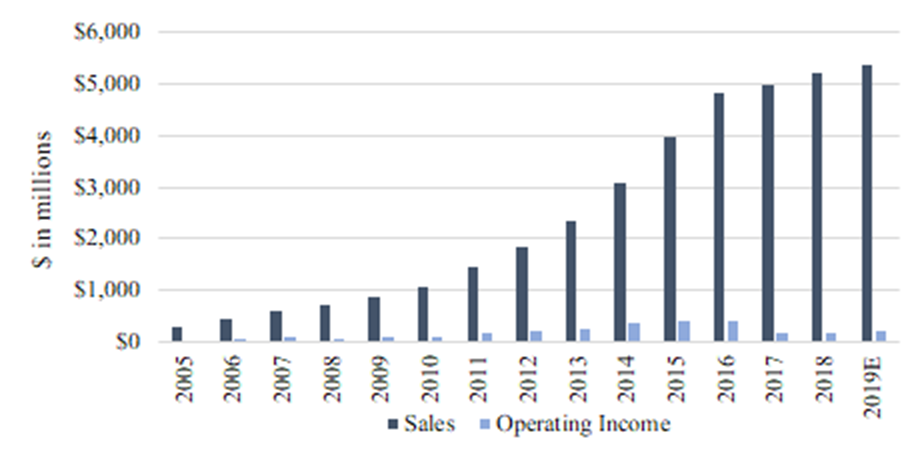

Source: FactSet Research Systems, Inc.

Sales and operating income grew a respective 4% and 14% in 2018 and are expected to grow a respective 3% and 30% in 2019. Operating income peaked in 2016 at $417 million and is still recovering from the 2017 headwinds and subsequent restructuring plan.

Under Armour’s key advantage is its brand. It can be difficult to distinguish between an enduring brand or a trendy fad. Brands are a promise built over many years and interactions between a company’s product/service and its customers. With brands, there is customer captivity within the search costs of not knowing if a non-branded product will be of similar quality to something you are familiar with. What is the value to a consumer in drinking Coca-Cola or using Crest toothpaste versus a private label alternative?

A brand in and of itself is not necessarily a competitive advantage. For example, Mercedes Benz is one of the most admired and respected auto brands in the world. Its brand has been a status symbol for quality and success; however, the brand has not translated into significant profitability for the company throughout the years. It is the barriers to entry that determines whether an advantage truly exists and therefore provides a company with above-average economic returns.

U.S. luxury auto manufacturers did not always earn lackluster returns. Before foreign luxury cars entered the U.S. in the 1970s and 1980s, Cadillac and Lincoln had attractive returns on invested capital. These high returns attracted Mercedes (OTCPK:DDAIF) and BMW (OTCPK:BMWYY) to enter the market, later followed by Lexus, Acura, and others. While the prices on these luxury cars remained at a premium price point, total U.S. auto demand remained stable while the market became more fragmented among the many luxury auto manufacturers. Unit sales declined for Cadillac and Lincoln and were then shared among several other competitors. The companies still had to spend heavily on product development, advertising, and its service networks but the fixed costs were spread across fewer sold cars, therefore increasing fixed cost and lowering net profits per car sold.

Alternatively, the larger sports apparel companies such as Nike (NYSE:NKE), Adidas (OTCQX:ADDYY), Anta (Fila) (OTC:ANPDF), Columbia Sportswear (NASDAQ:COLM), and Under Armour until recently, have all consistently earned very attractive returns on capital. Each of these companies sells its products around the world and to a similar target market.

If the returns are so attractive, why don’t new competitors enter the market, undercut on price, steal share, and inevitably push returns down to just average? The answer is barriers to entry, a large and growing end-market, and the primary competitors each trying to sell high quality, premium priced products.

It takes many years and interactions with athletes to build trust that a product is high quality and will perform as expected. Under Armour and Fila are the only major sports apparel companies to emerge as players on a global scale in recent decades. Under Armour was started in 1996 and had 2018 sales of $5.2 billion. Fila is headquartered in South Korea, started in 1991 and had 2018 sales of $3.6 billion. Lululemon (NASDAQ:LULU) is in a similar category but is more focused on serving the high-end female athleisure market. It was started in 1998 and had 2018 sales of $2.6 billion. Outside of these companies, few have been able to go head-to-head with Nike and Adidas. It has proven very difficult to start and build a widely accepted/trusted sports brand.

While economies of scale will make it difficult for many new sporting apparel companies to pop up, it is true Nike and Adidas, being a respective 7x and 5x Under Armour’s sales, have a relative advantage. Nike and Adidas’ size gives them wider brand recognition, relationships and negotiating power with suppliers and distribution channels, and marketing and sponsorship deals with top athletes. Despite Nike and Adidas’ favorable unit economics, Under Armour was able to prosper and become the fastest athletic apparel brand to reach $500 million and then $1 billion in sales, initially growing in its niche Football market and expanding from there.

Beyond the barriers for new entrants, the major existing players have another advantage, they are all focused on providing premium, high-quality products. This helps all three earn attractive economics. Let’s say there was a Nike, an Adidas, and an Under Armour jacket on sale for $100 each. A competitive market would expect one company to discount its jacket to $80 to take market share, sell more jackets, and make more profits. Subsequently, the other companies would lower their prices as well until the price reaches a point that profits become unattractive.

While this is what is to be expected in a competitive environment, if each of the three companies were determined to sell high-quality products at premium price points and the market demand was large enough to support all three companies, each could earn attractive returns.

The above example and investment thesis for the premium sports apparel industry assumes all three major companies want to sell premium products and won’t discount products to the point it makes them economically unattractive. This thesis was tested in 2016 when Sports Authority filed bankruptcy which impacted the entire U.S. sporting goods industry, particularly Under Armour which had 90% of sales in the U.S. at the time. Retailers were stuck with excess inventory and forced to discount and move apparel to off-price channels. Nike poured fuel on the fire when it reduced its minimum advertised price in late 2016 for the first time in its history, allowing retailers to advertise discounts by as much as 25% on its shoes and apparel during 2017.

Companies that go through some type of adversity and survive, often come out stronger on the other end. Since 2016, excess industry inventories have declined, Nike’s minimum advertised price returned to normal, and Under Armour has refocused on operational efficiencies through better-segmented product, inventory management, and SKU rationalization.

While we expect each of the major sports apparel companies to fare well financially over the long term, we think Under Armour shares look attractively priced to outperform going forward. Under Armour has the ability to compete with the big players and grow from a much smaller base as they continue to achieve greater economies of scale. Once its cost structure is optimized and margins return to historic levels, we expect earnings power to reaccelerate.

Disclosure: I am/we are long UA. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Self-made millionaire: This is the greatest paradox of wealth—and most people fail to recognize it

Published Thu, Aug 8 2019 12:08 PM EDTUpdated Thu, Aug 8 2019 12:18 PM EDT

Ramit Sethi, Contributor@RAMIT

Change is a constant and continuous process in life. As we grow older, we change how we dress, what we eat, where we live and who we become friends with.

Yet when it comes to how we use our time and money ― especially for high earners and wealthy individuals ― we tend to be more resistant to change.

Here’s a little scenario to illustrate my point: I have a friend who earns more than $750,000 a year. He loves his job, but if you asked him how he’s doing, his biggest complaint would be: “I’m so busy.”

So imagine my surprise when I visited him one day and pointed to the bags sitting on his kitchen counter.

“Oh, I just got back from the grocery store,” he said.

After a quick pause, I asked, “Have you ever considered having someone else do your grocery shopping?”

He looked at me like I was crazy. Pay to have someone do his grocery shopping? What kind of elitist would do that?

Here was an adult earning $750,000 a year, but behaving as if he still earns $50,000.

The hidden paradox of money vs. time

The concept of buying back your time is one of the most powerful productivity concepts I’ve learned as a business owner.

Buying back your time is all about convenience: By spending on things like Lyft rides, pre-cooked meals or a housekeeper, you’re actually saving money because you get back the hours that you’d normally spend doing things that don’t make you happy.

Most high earners fail to recognize the effectiveness of buying back time. Maybe it’s because growing up, their parents didn’t have more money than time, which changes the calculus of how they make decisions. As a result, those high earners never end up changing their approach to work and their personal lives.

This is a huge paradox of earning more money: Many people claim they value time over money, but if you look at their calendars, you’ll find that the opposite is true.

Buying back your time isn’t an act of arrogance

I used to scoff at people who flew first-class and think,Why would anyone spend an insane amount of money something so pointless? We’re all getting to the same destination.

But more often than not, those people were not stupid. They were high earners who understood value in a different way than I used to.

If you earn $40,000 a year, for example, spending $5,000 on a first-class flight is crazy. But if you’re a CEO who earns $450,000 a year, it makes perfect sense.

In business, misaligned beliefs on time and money can cost you dearly ― while getting aligned can become a force multiplier.

Sometimes, people who buy back their time are seen as showing off. But guess what? Many of us already do it:

- Eating at a restaurant instead of cooking at home

- Getting the car oil changed instead of doing it yourself

- Taking an Uber instead of walking or taking public transportation

- Paying retail price instead of looking for a good deal

I’d bet that some of you do these things every week and don’t consider it as “buying back your time.” But you actually are because you’re spending on convenience so you can focus on getting results and move on to more important things.

I’m really into fitness, for example, and Theoretically, I could read a ton of material on bodybuilding, structure my diet and fitness routine ― and stick to it.

But I know I’ll never be as efficient as my trainer, who lives and breathes fitness. By paying him, I can trade money for time and get the best results. (Again, I could be doing it all on my own, but I don’t have to; I’d rather spend that time on my business and with my family.)

Give it a shot―it might change your life

I still find it difficult to know when it’s “right” to spend money or time on something ― and I’m not alone.

Think about all the wealthy and successful people, like my friend who earns $750,000 per year, who are uncomfortable with the idea of delegating tasks to others. But if you’re working hard, you should be able to buy back your time.

The key is to ask yourself: What do I get out of it?

What do you get if you got three hours of your time back every week? Do you get to fly your parents out and put them up in an amazing suite? (If you’re Indian like me, the answer is no: They’ll be staying with you.) Do you get to do things you really enjoy, like cooking your own meal or composing music?

If you’re making more money than ever, aim to save at least one hour per week. Think about all the responsibilities that you hate (e.g., doing the laundry, grocery shopping, managing your finances) where there are great solutions available to outsource or systematize the work.

Then, as you get more advanced, you can tackle trickier topics like scheduling, email management and entire project management.