HI Market View Commentary 02-19-2019

What I want to talk about today?

Have things gone my way in this year’s stock market?

For the most part yes – AAPL, DIS, V, F, BAC, RHT, ZION, AOBC, IBB,

Maybes – UAA, FB, FCX,

NO – MO, BIDU, MRVL, INTC, MRO,

Why do I collar trade? Weather the storms, to make more as things come back

Risks – Whipsawed on technicals, tweets, short term headline risk, quitting, stagnation

You options are the big box firms: So if you like NOT talking to your advisor , Just waiting it out with diversification helping you, Averages

AVERAGES ARE NOT your Friend:

Story of the $1 over 2008-2009

2008 – 38% drop = $0.62

2009 – 23% gain = $0.76

So you lost 15% over the last two year meaning your dollar is down 15% and you THINK it is worth $0.85

On average you were down 7% yearly and you think you have $0.93

Where will our markets end this week?

????

DJIA – Bullish

SPX – Bullish

COMP – Bullish

Where Will the SPX end February 2019?

02-19-2019 +2.0%

02-11-2019 -2.0%

02-04-2019 -2.0%

Earnings:

Mon:

Tues: NBL, WMT, DVN

Wed: GRMN, OC, FLS, NTES, NE

Thur: DPZ, NEM, VG, WEN, FLR, IQ, ROKU, BIDU

Fri:

Econ Reports:

Mon:

Tues: NAHB Housing Market Index

Wed: MBA, FOMC Minutes

Thur: Initial, Continuing, Phil Fed, Existing Home Sales, Leading Indicators, Durable, Durable ex-trans,

Fri: CHINA deal update – Tariffs of 25% or maybe another 90 grace period

Int’l:

Mon –

Tues –

Wed –

Thursday –

Friday-

Sunday –

How am I looking to trade?

Earnings are coming up and protecting through earnings with protective puts and NO short Calls

AOBC – 2/28

BIDU – 2/21 AMC

MRVL – 3/17

RHT – 3/26

www.myhurleyinvestment.com = Blogsite

customerservice@hurleyinvestments.com = Email

Questions???

https://seekingalpha.com/article/4242051-disney-forced-transform-business

Disney: Forced To Transform Its Business

Feb. 19, 2019 9:54 AM ET

Summary

The shift in content consumption has impacted the business model for Disney and changed the business fundamentals.

Higher debt levels reduce the financial flexibility of the company, and there is no turning back from this point.

Why is Disney in a transformation phase, and how will it impact the future of the company?

Will Disney’s investments eventually generate higher returns for shareholders?

Investment Thesis

Disney (DIS) is a diversified worldwide entertainment company with operations in four main business segments: Media Networks, Parks and Resorts, Studio Entertainment, and Consumer Products & Interactive Media.

Disney is currently in a transformation phase and is investing in order to respond to the changing market dynamics and stay relevant in today’s market environment. The shift in content consumption, driven by companies like Netflix (NASDAQ:NFLX), has put pressure on Disney’s business model.

In the fiscal year 2018, Disney bought Twenty-First Century Fox, Inc. (21CF) (NASDAQ:FOX), and the closing of the deal is expected to occur H1 2019. The company is also developing a new direct-to-consumer (DTC) service, Disney+, which is scheduled to be launched by the end of 2019. Disney+ will be able to offer Disney, Pixar, Marvel, and Lucasfilm movies released theatrically after 2018. It will also feature exclusive original series and movies from the company’s film and television libraries.

Disney has placed its bets by acquiring 21CF and by the planned rollout of the DTC platform. This will lower the financial and operational flexibility of the company but, if successful, secure the business fundamentals for the company long term.

In this article, we will seek to understand why the transformation occurred at this point in time, assess the historical financial results, and understand the impact of the transformation. Will higher risk be accompanied by high returns?

Source: Annual Report, Fiscal Year 2018

Why Transformation?

The stock price for Disney has been more or less stable for the past 3 years. The lack of strong growth catalysts and relatively low dividend yield (1-2%) have made investors cautious. For the past years, Disney has not been a particularly attractive investment from a growth perspective, nor from an income perspective. The transformation this year is set to change that and has defined the roadmap for the company.

Building a robust direct-to-consumer business is our top priority, and we continue to invest in exceptional content and innovative technology to drive our success in this space.”

Source: Disney’s Q1 FY19 Earnings Results

Data by YCharts

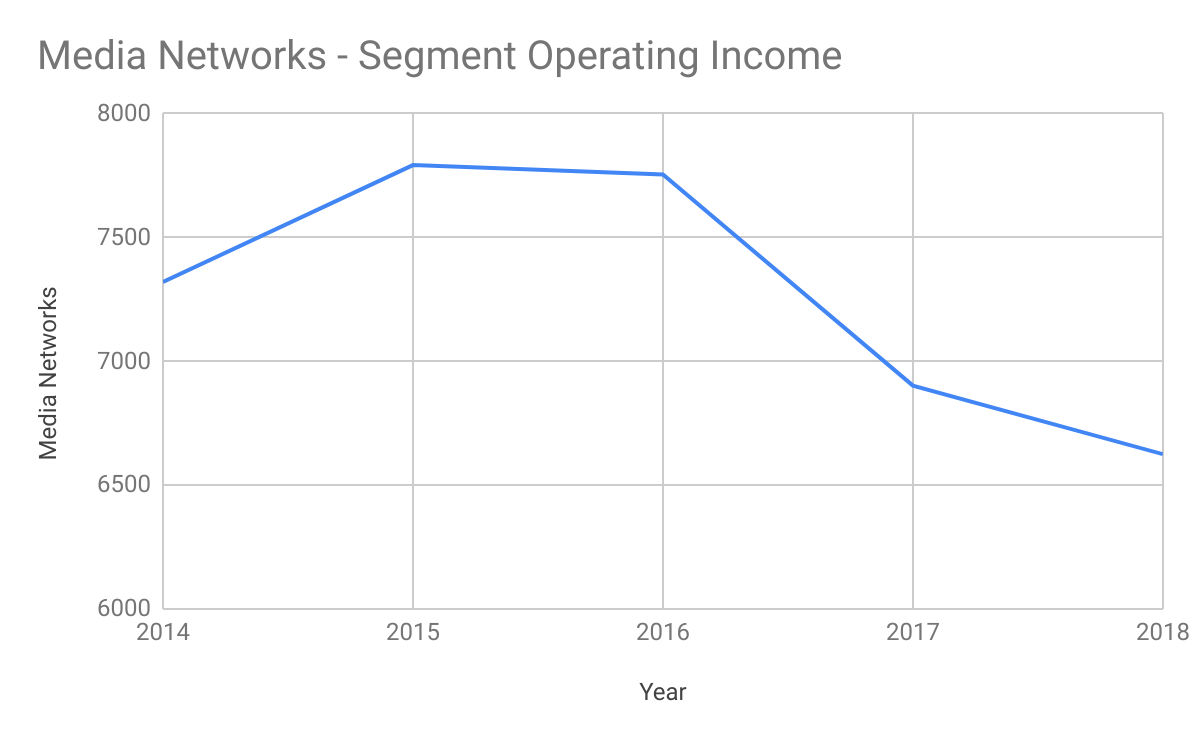

A majority of Disney’s revenues comes from media networks, and the shift in content consumption has impacted the business model for Disney. Industry-wide decline in ratings for broadcast television, demand for homeentertainment sales of theatrical content, and the development of alternative distribution channels impact the operating income for this business segment.

Disney’s portfolio of brands poses a strong durable advantage, but Disney needs to succeed in its ability to reach out with its content in order to maintain its current profit margins long term.

{kind=link}

The transformation into DTC is a reaction to the new market environment, and the transformation has simply become a necessity for Disney. The acquisition of 21CF will expand Disney’s already-rich content library, which can be used in the DTC initiative. The short-term profitability will likely come from a higher market share in traditional media and allow the company to invest for the long term in its DTC platform, where the profit pool is likely going to be in the future.

There is no turning back from this point in the transformation, the investments need to generate a good balance between short and long-term profitability.

Source: Annual Report, Fiscal Year 2018

Annual Results 2018 and Growth Outlook

Income Statement

(USD in millions except per share data)

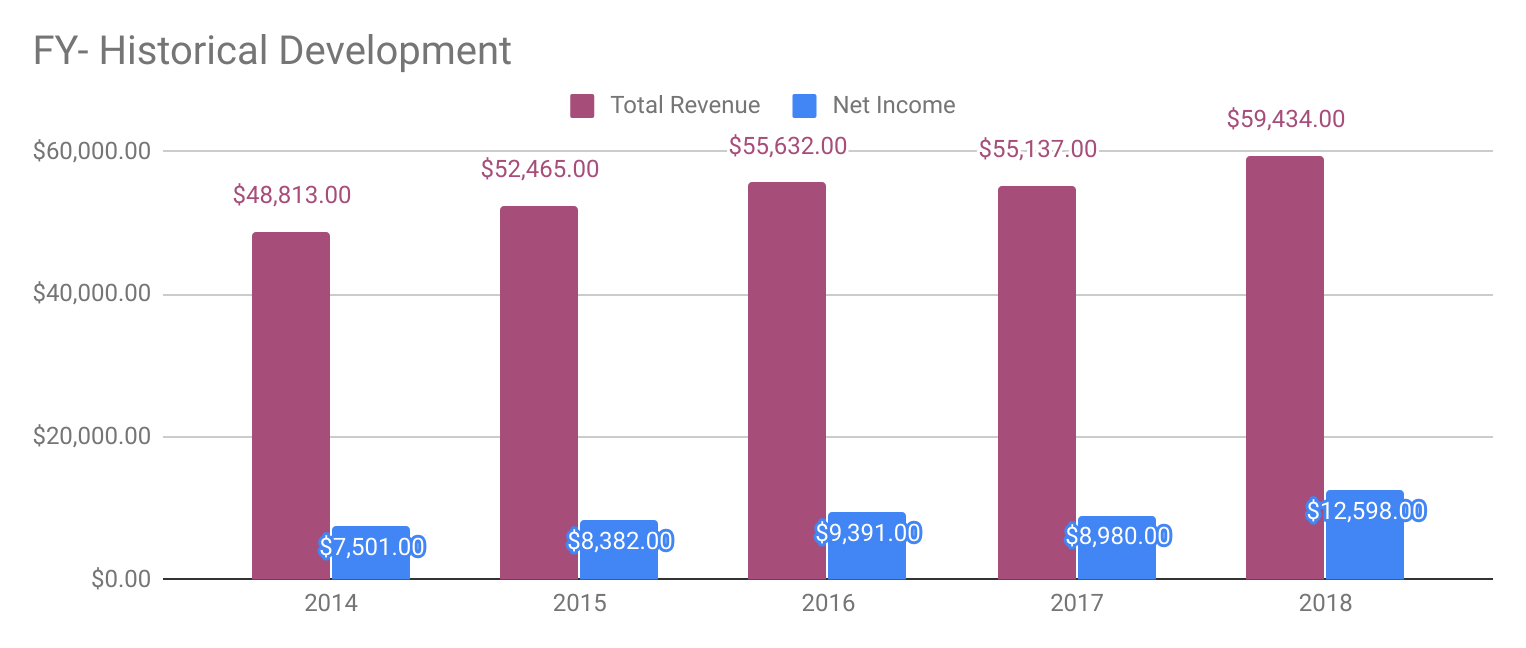

Total revenues for the company have grown 5.0% YoY on average for the past 5 years. For the fiscal year 2018, total revenues amounted to $59,432, up +7.8%. The higher revenues were driven by double-digit growth in the Park and Resorts and Studio Entertainment business segments. Operating income has grown +6.5% on average YoY, and for the fiscal year 2018, it amounted to $14,837, up +6.9%. The net income has grown at a similar historical growth rate as operating income but was impacted by special items in the fiscal year 2018. Net income amounted to $12,598, up +40.3% for the fiscal year 2018. This was mainly driven by a lower effective income tax rate vs. previous year.

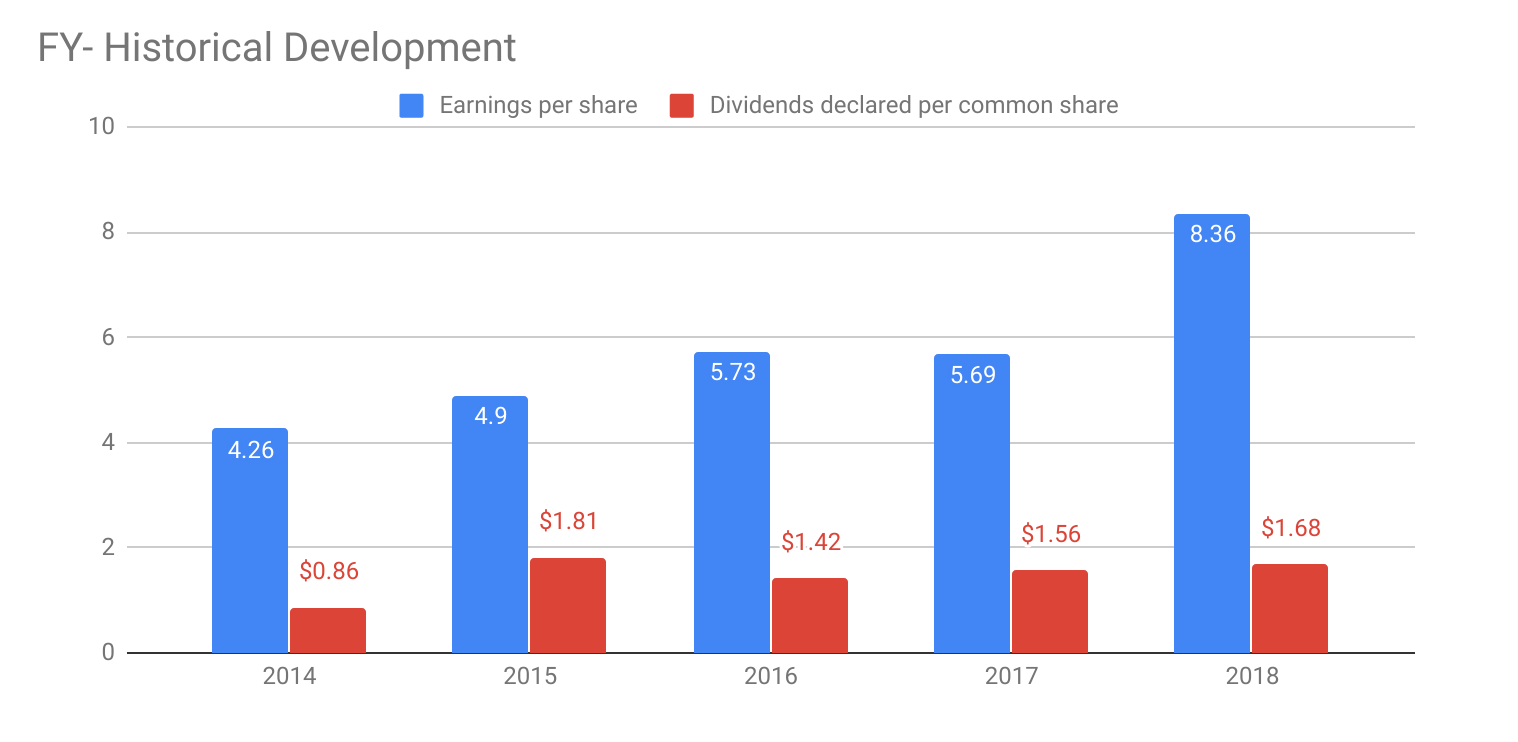

On a diluted EPS basis, the historical growth has been +18.4%, driven by higher net income but also by a slight reduction in outstanding shares.

{kind=link}

{kind=link}

Balance Sheet

(USD in millions)

Disney’s cash position has been more or less stable at $4,000 for the past 4 years. The short-term debt and long-term debt have, however, grown considerably over the years and amounted to $20,874 for the fiscal year 2018. Upon the completion of the acquisition of 21CF, the total outstanding debt is projected to amount to $40 billion (short + long-term debt). This will translate to a total interest expense of approximately $2 billion per year.

The increased indebtedness of Disney reduces the flexibility to respond to changing business and economic conditions.

The increased levels of indebtedness following completion of the acquisition could also reduce funds available for capital expenditures, share repurchases and dividends, and other activities and may create competitive disadvantages for us relative to other companies with lower debt levels.”

Source: Annual Report, Fiscal Year 2018

The Positives

Disney has an unparalleled portfolio of content and brands that create strong durable competitive advantages in the segments in which they operate. The acquisition of 21CF further strengthened this competitive advantage, and the new company will truly be a powerhouse in traditional media.

Even though traditional media is in a secular decline, it will remain a profitable business segment for Disney. Park and Resorts will most likely also continue to generate healthy profits for the company in the future.

With the Disney+ initiative, the company is establishing itself in the fast-growing DTC business segment and can offer consumers a wide library of content from the start of the launch.

Conclusions

Disney’s ongoing transformation is essential for the continued success of the company. Slowing organic growth from Disney’s current business segments, in combination with heavy investments to deliver the transformation objectives, adds significant risks for the company and shareholders. The current low dividend yield also means that investors are not rewarded while waiting for the transformation to be completed and potentially bear fruit.

Strong brands and a rich content library are very positive factors for the launch of Disney+, but the success in the DTC business is far from certain. Even if we assume that Disney will be successful in its launch, generating profits will likely take time as Disney will face fierce competition in this business segment.

The business fundamentals have changed for so much for Disney that we recommend current investors to sell their position in the company at the current price of $112.6. We need to see proof that transformation is successful in its initial stage and that the overall profitability improves in the DTC segment for it to be an interesting investment. For now, we believe that there are more profitable opportunities to invest in.

We have covered some of them in our previous articles here at Seeking Alpha.

https://seekingalpha.com/article/4241952-challenges-sight-baidu

Challenges In Sight For Baidu

Feb. 18, 2019 6:39 PM ET

Summary

Recent developments in China concerning the public perception of Baidu as a search engine has soured dramatically.

Increasing competition, not from Google, but WeChat, makes the PR headache an inopportune nightmare for Baidu.

It remains to be seen if this is a temporary problem (such as the 2016 fiasco) or a permanent and existential crisis.

Its iQIYI and Apollo program are still a mixed bag with positive news but worrying ones as well (competition and costs).

Having previously written bullishly about Baidu (NASDAQ:BIDU) back when its stock price was about $219, I initiated a position at $211 and bought more at $181. Baidu has since fallen about 22% since my initial bullish report and thus I’m interested in understanding if my investment thesis on Baidu has since changed or is it a good time to load up on more Baidu before its Q4 earnings report on Feb. 21.

Updates on Baidu’s position as China’s leading search engine

Part 1 of my initial thesis on Baidu was the presence of strong and diversified revenue drivers, particularly its dominant position as China’s leading search engine which sees it enjoying around 25% growth in Baidu Core revenue. Has this changed? The short answer is yes and no.

Since publishing my article in early October 2018, there have been several more bullish articles on Baidu, however not a single article covered the recent surge in negative sentiment on Baidu in China. Quartz recently published a great article on this, summarizing the points made by Fang Kecheng, a veteran Chinese political journalist whose well-articulated analysis titled “Search engine Baidu is dead” became viral across the Chinese internet. The article accuses Baidu of prioritizing its own websites and apps when returning search results.

Baidu is no longer a place for you to search for content on China’s Internet, but rather an internal search for Baidu content,” wrote Fang in the piece, which published late Tuesday (Jan. 22) on a WeChat public account he runs. “It won’t lead you to good quality food for the spirit from China’s Internet, but content hoarded at home, gone bad.

For example, Fang conducted nine different searches on a variety of topics (Brexit, China’s 2019 GDP, how to buy train tickets, etc) and found that the first page of search results were all from Baidu’s own apps and websites including Baijiahao (Chinese Medium) and Baike (Chinese Wikipedia).

Thomas Graziani of WalkTheChat conducted his own search on Obama with similar results. Thomas Graziani also correctly and astutely points out that this would not have been a major problem if Baijiahao and Baike were reputable sources of information however, Baijiahao in particular have faced increasing backlash on spreading fake news. Fang wrote that Baijiahao helped spread satirical news from The Onion as real news, claiming that the C.I.A issued a posthumous apology to Osama Bin Laden after clearing him of involvement in 9/11 attacks.

{kind=link}

Immediately after Fang’s article became viral on Weibo, Microsoft’s (NASDAQ:MSFT) Bing (unblocked in China) saw a surge in traffic. Whether this is a temporary problem or a permanent one remains to be seen. However, more worrying than Bing or a possible Google (NASDAQ:GOOG) (NASDAQ:GOOGL) re-entry is the bad timing that such bad PR would happen just when WeChat launches its search function.

WeChat’s recently launched Search function is slightly different from Google and Baidu’s traditional search engine function in that it’s a bit more of a social feature. According to Quartz, “searching for “Apple” yields recent news at the very top, followed by mentions of Apple made by one’s friends. An assortment of random articles follows at the bottom. Tapping on any of these links — even the articles — always keeps one within WeChat’s built-in browser, and many of the linked articles are ones published directly to WeChat. This is particularly problematic for Baidu considering the significant amount of time Chinese spend on WeChat,users no longer have to leave the convenience of the app. Furthermore, WeChat is able to leveragethe large amount of data that it has collected on its more than 900 million users to create personalized results.

This is not the first time Baidu has faced an existential crisis to this degree, with many investors still remembering the 2016 fiasco regarding health and medical advertisements. Baidu, as a company and its stock, has since recovered from that incident so I wouldn’t put it past Baidu to be able to overcome this problem as well. The situation is helped by the near complete lack of competition in the search engine field. However, it’s interesting to note that Fang believes this time the problem is far worse.

It wasn’t the same situation one year ago, or even five, 10 years ago. Back then, Baidu had all kinds of different problems, but at least it was a real search engine, an entrance for you to explore China’s Internet. You could get some satisfactory answers from it,” Fang wrote, noting the worrying quality of some of the Baijiahao results, “…It’s pathetic that given the size of China’s internet, we’ve fallen into a situation where we don’t even have a search engine.”

Personally, I’m worried about the precarious situation Baidu seems to have found itself in. This couldn’t have come at a worse time for Baidu and I will be keeping a close eye on how it responds to the situation as well as how WeChat search is received by Chinese netizens. This makes the quarterly results for Q4 and the upcoming quarters all the more important, to see if MAU and Baidu Core revenue (especially online advertising) have been hurt by these recent developments.

Updates on its diversification efforts

Part 2 of my bullish thesis on Baidu was its diversification efforts, particularly through iQIYI (NASDAQ:IQ), the so-called Netflix of China. In its most recent Q3 results, iQIYI reported increasing subscriber counts and strong revenue growth. However, costs including costs of revenue and sales and marketing costs continue to balloon, leading to operating losses of 2.6 billion RMB, a -37% operating margin vs. a -23% operating margin in the same quarter a year ago. This resulted in an EPS loss of -$0.63, significantly higher than analysts’ expectation of -$0.38.

Its other moonshot bet is in autonomous driving where it’s one of China’s leading companies in autonomous driving. A recent report by The South China Morning Post shed some light on this increasing competitive field and how Chinese companies are faring vis-a-vis its US rivals. According to data disclosed in an annual report by the California Department of Motor Vehicles, Pony.ai, the front-runner among Chinese autonomous driving companies, reported human intervention once every 1,022 miles, far better than Baidu’s 205 miles. This continues to lag far behind its US rivals where Waymo required intervention only once every 11,000 miles while Cruise required intervention once every 5,200 miles.

Worryingly, Pony.ai, which was only founded in 2016 by the former Chief Architect of Baidu’s Autonomous Driving program appears to have overtaken or at least are level with Baidu’s autonomous driving program. Its rapid progress can be seen in that only 18 months ago, it required human intervention once every 100 miles, a far cry from its current numbers.

{kind=link}

Conclusion

Baidu’s incredibly cheap valuation means that I will not be selling my stake in Baidu anytime soon. However, I’m growing incredibly worried about recent developments at Baidu, in particular the perception of it as a search engine. I will definitely be keeping an eye out on future metrics to determine if this is a temporary problem or a permanent one. I also will be looking out for any developments made by management to address accusations (besides denial) that its search results favor its own apps and websites.

Data by YCharts

I’m less worried about iQIYI and its Apollo division as both are in industries that are enjoying secular growth and it’s still hard to determine the clear winners and losers.

Disclosure: I am/we are long BIDU, TCEHY. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

https://www.investopedia.com/ask/answers/05/bondrisks.asp

INVESTING BONDS / FIXED INCOME

What are the risks of investing in a bond?

Updated Jan 9, 2018

The most well-known risk in the bond market is interest rate risk – the risk that bond prices will fall as interest rates rise. By buying a bond, the bondholder has committed to receiving a fixed rate of return for a set period. Should the market interest rate rise from the date of the bond’s purchase, the bond’s price will fall accordingly. The bond will then be trading at a discount to reflect the lower return that an investor will make on the bond.

Interest Rate Risk Factors For Bonds

Market interest rates are a function of several factors, including the demand for and supply of money in the economy, the inflation rate, the stage that the business cycle is in, and the government’s monetary and fiscal policies.

From a mathematical standpoint, interest-rate risk refers to the inverse relationship between the price of a bond and market interest rates. To explain, if an investor purchased a 5% coupon, 10-year corporate bond that is selling at par value, the present value of the $1,000 par value bond would be $614. This amount represents the amount of money that is needed today to be invested at an annual rate of 5% per year over a 10-year period, in order to have $1,000 when the bond reaches maturity.

Now, if interest rates increase to 6%, the present value of the bond would be $558, because it would only take $558 invested today at an annual rate of 6% for 10 years to accumulate $1,000. In contrast, if interest rates decreased to 4%, the present value of the bond would be $676. As you can see from the difference in the present value of these bond prices, there truly is an inverse relationship between the price of a bond and market interest rates, at least from a mathematical standpoint.

From the standpoint of supply and demand, the concept of interest-rate risk is also straightforward to understand. For example, if an investor purchased a 5% coupon and 10-year corporate bond that is selling at par value, the investor would expect to receive $50 per year, plus the repayment of the $1,000 principal investment when the bond reaches maturity.

Now, let’s determine what would happen if market interest rates increased by one percentage point. Under this scenario, a newly issued bond with similar characteristics as the originally issued bond would pay a coupon amount of 6%, assuming that it is offered at par value.

For this reason, under a rising interest rate environment, the issuer of the original bond would find it difficult to find a buyer willing to pay par value for their bond, because a buyer could purchase a newly issued bond in the market that is paying a higher coupon amount. As a result, the issuer would have to sell her bond at a discount from par value in order to attract a buyer. As you can probably imagine, the discount on the price of the bond would be the amount that would make a buyer indifferent in terms of purchasing the original bond with a 5% coupon amount, or the newly issued bond with a more favorable coupon rate.

The inverse relationship between market interest rates and bond prices holds true under a falling interest-rate environment as well. However, the originally issued bond would now be selling at a premium above par value, because the coupon payments associated with this bond would be greater than the coupon payments offered on newly issued bonds. As you may now be able to infer, the relationship between the price of a bond and market interest rates is simply explained by the supply and demand for a bond in a changing interest-rate environment.

Six biggest bond risks

BY GLENN CURTIS

Updated Dec 19, 2017

Bonds can be a great tool to generate income and are widely considered to be a safe investment, especially compared with stocks. However, investors need to be aware of some potential pitfalls and risks to holding corporate and/or government bonds. Below, we’ll expose the risks that could effect your hard-earned profits.

1. Interest Rate Risk and Bond Prices

Interest rates and bond prices have an inverse relationship; as interest rates fall, the price of bonds trading in the marketplace generally rises. Conversely, when interest rates rise, the price of bonds tends to fall.

This happens because when interest rates are on the decline, investors try to capture or lock in the highest rates they can for as long as they can. To do this, they will scoop up existing bonds that pay a higher interest rate than the prevailing market rate. This increase in demand translates into an increase in bond price.

On the flip side, if the prevailing interest rate were on the rise, investors would naturally jettison bonds that pay lower interest rates. This would force bond prices down.

Let’s look at an example:

Example – Interest Rates and Bond Price

An investor owns a bond that trades at par value and carries a 4% yield. Suppose the prevailing market interest rate surges to 5%. What will happen? Investors will want to sell the 4% bonds in favor of bonds that return 5%, which in turn forces the 4% bonds’ price below par.

2. Reinvestment Risk and Callable Bonds

Another danger that bond investors face is reinvestment risk, which is the risk of having to reinvest proceeds at a lower rate than the funds were previously earning. One of the main ways this risk presents itself is when interest rates fall over time and callable bonds are exercised by the issuers.

The callable feature allows the issuer to redeem the bond prior to maturity. As a result, the bondholder receives the principal payment, which is often at a slight premium to the par value.

However, the downside to a bond call is that the investor is then left with a pile of cash that he or she may not be able to reinvest at a comparable rate. This reinvestment risk can have a major adverse impact on an individual’s investment returns over time.

To compensate for this risk, investors receive a higher yield on the bond than they would on a similar bond that isn’t callable. Active bond investors can attempt to mitigate reinvestment risk in their portfolios by staggering the potential call dates of their differing bonds. This limits the chance that many bonds will be called at once.

3. Inflation Risk and Bond Duration

When an investor buys a bond, he or she essentially commits to receiving a rate of return, either fixed or variable, for the duration of the bond or at least as long as it is held.

But what happens if the cost of living and inflation increase dramatically, and at a faster rate than income investment? When that happens, investors will see their purchasing power erode and may actually achieve a negative rate of return (again factoring in inflation).

Put another way, suppose that an investor earns a rate of return of 3% on a bond. If inflation grows to 4% after the bond purchase, the investor’s true rate of return (because of the decrease in purchasing power) is -1%.

4. Credit/Default Risk of Bonds

When an investor purchases a bond, he or she is actually purchasing a certificate of debt. Simply put, this is borrowed money that must be repaid by the company over time with interest. Many investors don’t realize that corporate bonds aren’t guaranteed by the full faith and credit of the U.S. government, but instead depend on the corporation’s ability to repay that debt.

Investors must consider the possibility of default and factor this risk into their investment decision. As one means of analyzing the possibility of default, some analysts and investors will determine a company’s coverage ratio before initiating an investment. They will analyze the corporation’s income and cash flow statements, determine its operating income and cash flow, and then weigh that against its debt service expense. The theory is the greater the coverage (or operating income and cash flow) in proportion to the debt service expenses, the safer the investment.

5. Rating Downgrades of Bonds

A company’s ability to operate and repay its debt (and individual debt) issues is frequently evaluated by major ratings institutions such as Standard & Poor’s or Moody’s. Ratings range from ‘AAA’ for high credit quality investments to ‘D’ for bonds in default. The decisions made and judgments passed by these agencies carry a lot of weight with investors.

If a company’s credit rating is low or its ability to operate and repay is questioned, banks and lending institutions will take notice and may charge the company a higher interest rate for future loans. This can have an adverse impact on the company’s ability to satisfy its debts with current bondholders and will hurt existing bondholders who might have been looking to unload their positions.

6. Liquidity Risk of Bonds

While there is almost always a ready market for government bonds, corporate bonds are sometimes entirely different animals. There is a risk that an investor might not be able to sell his or her corporate bonds quickly due to a thin market with few buyers and sellers for the bond.

Low buying interest in a particular bond issue can lead to substantial price volatility and possibly have an adverse impact on a bondholder’s total return (upon sale). Much like stocks that trade in a thin market, you may be forced to take a much lower price than expected to sell your position in the bond.

German car industry warns US over auto tariffs

US trade officials are believed to have told President Donald Trump that European car imports harm US national security. German carmakers are concerned that Trump could use the report to justify tariffs.

Any decision by the US to label European car and auto-part imports a danger to US national security would be incomprehensible, the German Association of the Automotive Industry (VDA) has said.

The trade body was responding to reports that US Commerce Secretary Wilbur Ross’ report on the impact of imports had reached the White House, in advance of a Sunday deadline.

German car companies were responsible for more than 113,000 jobs at some 300 factories in the United States and were the biggest exporters of cars in the country, VDA said.

“All this strengthens the United States and cannot be seen as a security problem,” it added.

Read more: EU ramps up attack on Trump auto tariff plans

EU car imports dangerous?

In May, President Donald Trump ordered the US Commerce Department to probe whether car imports threatened US national security.

If the department finds that all or some imports do harm national security, the president has 90 days to decide whether to introduce tariffs of up to 25 percent to wean the US off those imports.

Handelsblatt newspaper reported on Sunday that German officials were certain the department had told the White House that European car imports do harm national security.

Read more: Why higher US tariffs on car imports would backfire

The president has not however decided on whether to introduce tariffs, Reuters reported, citing officials. The news agency said Trump has 90 days to decide whether to act upon the recommendations, and there is stiff resistance among some officials in the US government to the move.

Currently the US levies a 2.5 percent tariff on European auto imports, while the European Union imposes a 10 percent duty.

Those in favor of tariffs reportedly want to use them as leverage in trade talks with the European Union and other trading partners such as Japan. On Friday, Trump said: “I love tariffs, but I also love them to negotiate.”

Read more: Are German cars American enough?

Significant hit expected

Experts say a 25 percent tariff would be against the interests of US consumers and could devastate the US auto industry, which depends on foreign car parts.

The US-based Center for Automotive Research said on Friday that its worst-case prediction showed such a tariff would lead to nearly 370,000 job losses in the car industry and 1.3 million fewer car sales a year.

Major carmakers said last year that the US automotive industry might experience price increases totaling $83 billion (€73 billion) a year.

The Munich-based Ifo Institute, meanwhile, warned that German auto exports would fall as much as 50 percent as a result of the move, and would affect imports of vehicle parts into the EU.

Merkel: US probe ‘frightening’

The European Union and Japan are both expected to retaliate with counter-tariffs on US goods if Trump decides to take action against their car companies.

Speaking at the Munich Security Conference on Saturday, German Chancellor Angela Merkel said it was “frightening” that the US was even considering whether cars made in the United States by German manufacturers were a national security threat.

Trump has repeatedly vowed to reduce the US trade deficit with other countries and bring back manufacturing jobs. So far, he has slapped tariffs on imported steel, aluminum, solar panels and hundreds of Chinese goods.

These stocks could surge the most if the US lowers tariffs on China and makes a trade deal

- The market popped Thursday on a Wall Street Journal report that the U.S. could ease tariffs on China during negotiations, helping to increase the chances of a long-term trade deal.

- U.S. stocks with revenue exposure to China of more than 20 percent, including Skyworks Solutions, Broadcom, Micron Technology and Marvell Technology Group can be big winners if a trade deal comes through, says HSBC’s Ben Laidler.

Published 3:02 PM ET Thu, 17 Jan 2019 Updated 9:57 AM ET Fri, 18 Jan 2019

The stock market popped on Thursday after a report from the Wall Street Journal suggested U.S. officials may lower tariffs on China during trade negotiations as an incentive to hatch a longer-term deal.

If a deal appears to be getting close, there is a possible game plan for traders.

“Any deal would likely see a relief rally as we believe markets have meaningfully priced in risks of trade tensions escalating,” said Ben Laidler, HSBC’s global equity strategist, in a note Tuesday. He also pointed out that tariff-sensitive stocks have underperformed significantly and their valuations are getting cheap.

To find the best names to buy on a trade deal pop, HSBC ran a screen looking for stocks with three main attributes:

- Listed U.S. stocks with revenue exposure to China of more than 20 percent.

- Underperformance during this three-month market pullback on trade deal concerns.

- Cheap valuation on a forward price-earnings basis.

The names that came up were focused in tech including Skyworks Solutions, Broadcom, Micron Technology and Marvell Technology Group.

A resolution on trade between the world’s two biggest economies could be a big catalyst for a relief rally in the stock market. BlackRock Chairman and CEO Larry Fink said Wednesday on CNBC’s “Squawk Box” that there would be “a surge in investment sentiment” if both sides call off tariffs on each other’s goods.

Washington and Beijing reached a 90-day truce last month to halt any new levies as they seek to work up a long-term deal through negotiations. There has been mixed feedback on the trade talks — Sen. Chuck Grassley, R-Iowa, said recently that U.S. Trade Representative Robert Lighthizer saw no progress on key issues, while President Donald Trump tweeted about “big progress” with China. In the latest development, China’s vice premier, Liu He, has accepted an invitation to Washington this month for trade talks.

Fears of a full-on trade war with China have been on top of investors’ minds for months. The volatile stock market suffered its worst year since the financial crisis in 2018, with the S&P 500 tanking a whopping 14 percent in the fourth quarter. U.S. companies have also sounded alarms on the trade war’s impact on their business.

To be sure, this is lining up to be a risky binary trade. These names (and the whole market) could be hit hard if there is not a trade deal.

If the negotiations go nowhere and a 25 percent tariff is imposed on all Chinese goods, HSBC estimated 4.5 percentage points would be subtracted from 2019 earnings growth, more than halving the growth rate from current levels, Laidler said in the note.