HI Market View Commentary 11-18-2024

Don’t forget that the first week of January we go over the new target pricing for our stocks

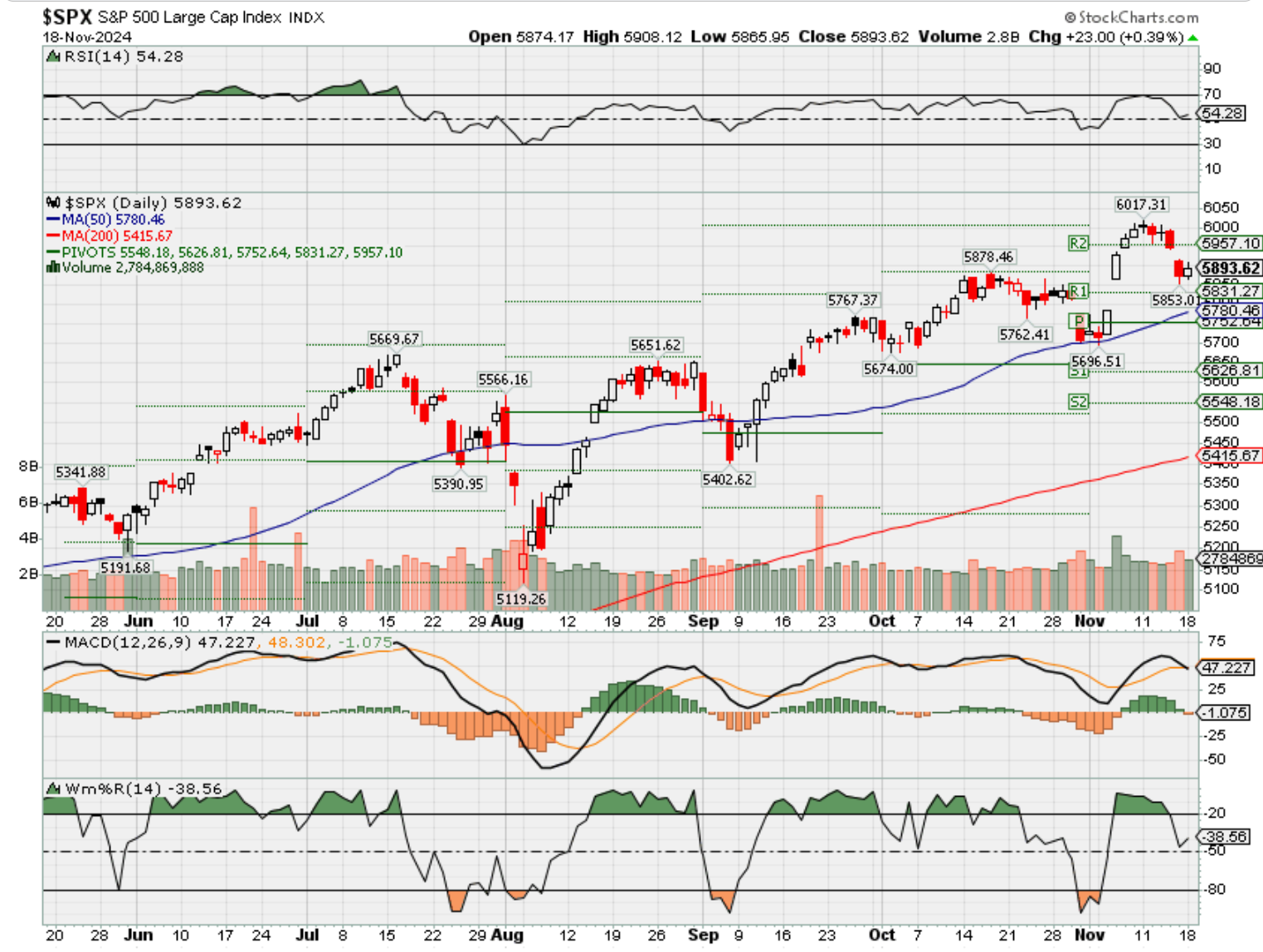

How the heck does the S&P 500 get to 8000? When the S&P 500 closed today @ 5,893.62

8000 – 5892 = 2108/5892 = 35.77% growth

What is the time frame?= 2030 = 6 years 35.77/6 years = 5.96% average growth per year

Deregulation adds +5% growth per year, Tax cuts IF 21% goes to 15% it also decreases fixed costs by 25% in the tax category

In the next 6 years S&P 500 growth hits $400 * Average PE 20 = 8000

Second question = What about our stocks – We are sticking with our holding

AAPL, BAC, BIDU, COST, DIS, F, GM, GOOGL, JPM, KEY, META, MU, NVDA, UAA, VZ,

Will be interested in BA, NFLX, O, JEPI, SQ, ZION

Looking to stay away from Energy, Bio Pharma and Healthcare

What was her big 2.3ish% loss attributed to last week?= Powell admitting he doesn’t see a need to lower rate quickly

Earnings dates:

BABA 11/21 BMO

BIDU 11/21 BMO

DG 12/05 est

MU 12/28 est

NVDA 11/20 AMC

TGT 11/20 BMO

https://www.briefing.com/the-big-picture

The Big Picture

Last Updated: 15-Nov-24 15:01 ET

Pulling back from the overdone pull forward

Some of the election dust has settled, but not all of it. There was a lot of dust kicked up by the stock market, which quickly ran to new all-time highs after the election results showed Donald Trump had scored a decisive victory in the presidential election and that he was likely to have a GOP majority in the House and Senate with which to work.

The GOP majority in the House was confirmed this week, which ended up being a pullback week for a stock market that had pulled forward a lot of good news.

Questions Being Asked

As discussed last week, the stock market’s enthusiasm for the election results revolved around its thinking that president-elect Trump will pursue plans to cut taxes and regulations in what has been labeled a pro-growth agenda.

Growth is good. The path to future growth is paved with good intentions, but as we also noted last week, it is always easier to campaign than it is to govern.

President-elect Trump will have Congress on his side — certainly for the first two years of his administration. The numbers just line up that way, yet the GOP majority in the House will be a slim majority that leaves little room for defection when it comes to passing tax plans.

The current period is a kumbaya period where GOP members all seem to be on board with the president-elect’s plans, only the train hasn’t left the station.

Eliminating taxes on tips; eliminating taxes on overtime pay; and eliminating taxes on Social Security benefits are promising-sounding campaign proposals that just might get derailed by deficit hawks inside the GOP, who will also be dealing with proposals to lower the corporate tax rate, raise the SALT cap, and extend the reduced personal tax rates from the 2017 Tax Cuts and Jobs Act that expire at the end of 2025.

That possibility wasn’t taken into account in the post-election rally. In that rally, everything was possible, if not likely. It was a buy-first-ask-questions-later kind of move. The pullback this week was about questions being asked.

- Did the market get too far ahead of itself in its post-election rally?

- Is inflation going to heat up again — or at least not make it to the Fed’s 2% target?

- How many times will the Fed cut rates, and will the neutral rate be higher than previously thought?

- Why are market rates going up?

- Can president-elect Trump keep the deficit under control and inflation in check with his policy proposals?

- Can NVIDIA (NVDA) live up to investors’ sky-high expectations when it reports its earnings results in the coming week?

The Velveteen Estimate

Today, we plan only to tackle the first question: Did the market get too far ahead of itself in its post-election rally?

The answer is yes. It is an easy answer because nothing has happened — and things won’t start happening on the policy front for another few months when the new Congress is sworn in, and president-elect Trump rightfully becomes President Trump again on January 20.

Nonetheless, there is no stopping a forward-looking market when it has its mind made up that good things are in the offing. In this case, it envisioned stronger profit growth with a lower corporate tax rate and less regulation.

How much stronger? Goldman Sachs estimates that the lower corporate tax rate could add 4-5% to S&P 500 earnings growth, but that wouldn’t be until 2026. According to FactSet, the current consensus estimate for 2026 S&P 500 earnings is $308.84. A 5% increase would elevate that number to $324.28, which is 19% higher than the current 2025 consensus estimate of $273.46.

| S&P 500 Price | Period | Consensus Estimate | P/E |

| 5,862.00 | Forward 12-Month | 268.95 | 21.8 |

| 5,862.00 | CY25 | 273.46 | 21.4 |

| 5,862.00 | CY26 | 308.84 | 19.0 |

| 5,862.00 | CY26 +5% | 324.28 | 18.1 |

Source: FactSet

What looks better? A P/E multiple of 21.8 or a P/E multiple of 18.1? Here again, it is an easy answer.

A P/E multiple of 18.1 is a lot less demanding than a P/E multiple of 21.8 when stacked against a 10-year average of 18.1. Participants clearly saw a pathway in the inflated 2026 estimate to the market not being “overvalued” like it was on November 4, and they ran with that.

In effect, they pulled forward an earnings estimate that isn’t real yet, but because they loved it, they made it real in their mind, justifying the rush to new all-time highs.

Take It Back

Who knows? The Velveteen 2026 earnings estimate could end up being real, but there is a long negotiating row to hoe to get there, and it won’t be easier if interest rates remain elevated — or also move higher into 2026 because of other issues like deficit concerns or inflation heating up.

The October CPI and PPI reports didn’t connote some warm and fuzzy inflation feelings with core-CPI up 3.3% year-over-year and core-PPI up 3.1% year-over-year. What they did do is temper the market’s rate cut expectations. Those got pulled forward as well.

A month ago, the market expected the target range for the fed funds rate to be 3.25-3.50% following the September 2025 FOMC meeting. Now, it is expected to be 3.75-4.00%, according to the CME FedWatch Tool, so 50-basis points higher than previously envisioned.

Given that, the stock market has taken back some of the rate cut premium in stock prices that had been pulled forward.

What It All Means

The parabolic move following the election wasn’t going to be sustained. The market had gotten ahead of itself, all charged up with a powerful mix of liquidity, a fear of missing out on further gains, short-covering activity, and the most upbeat earnings view into 2026 (forget about 2025).

It pulled forward that view, and pulled down the earnings multiple along with it, to rewrite an overvalued narrative that flowed from a market cap-weighted S&P 500 trading at 22.4x forward 12-month earnings at its post-election peak on November 11 — a 24% premium to the 10-year average.

While there is a difference between campaigning and governing, there is also a difference between proposals and policy.

There isn’t a policy agreed to yet that will lower the corporate tax rate or any tax rate. There will be a push for that, but the market pulled forward too much, too soon, when it comes to pricing in tax cuts and rate cuts. Hence, it needed to pullback to let the dust from an overdone, post-election rally settle.

—Patrick J. O’Hare, Briefing.com

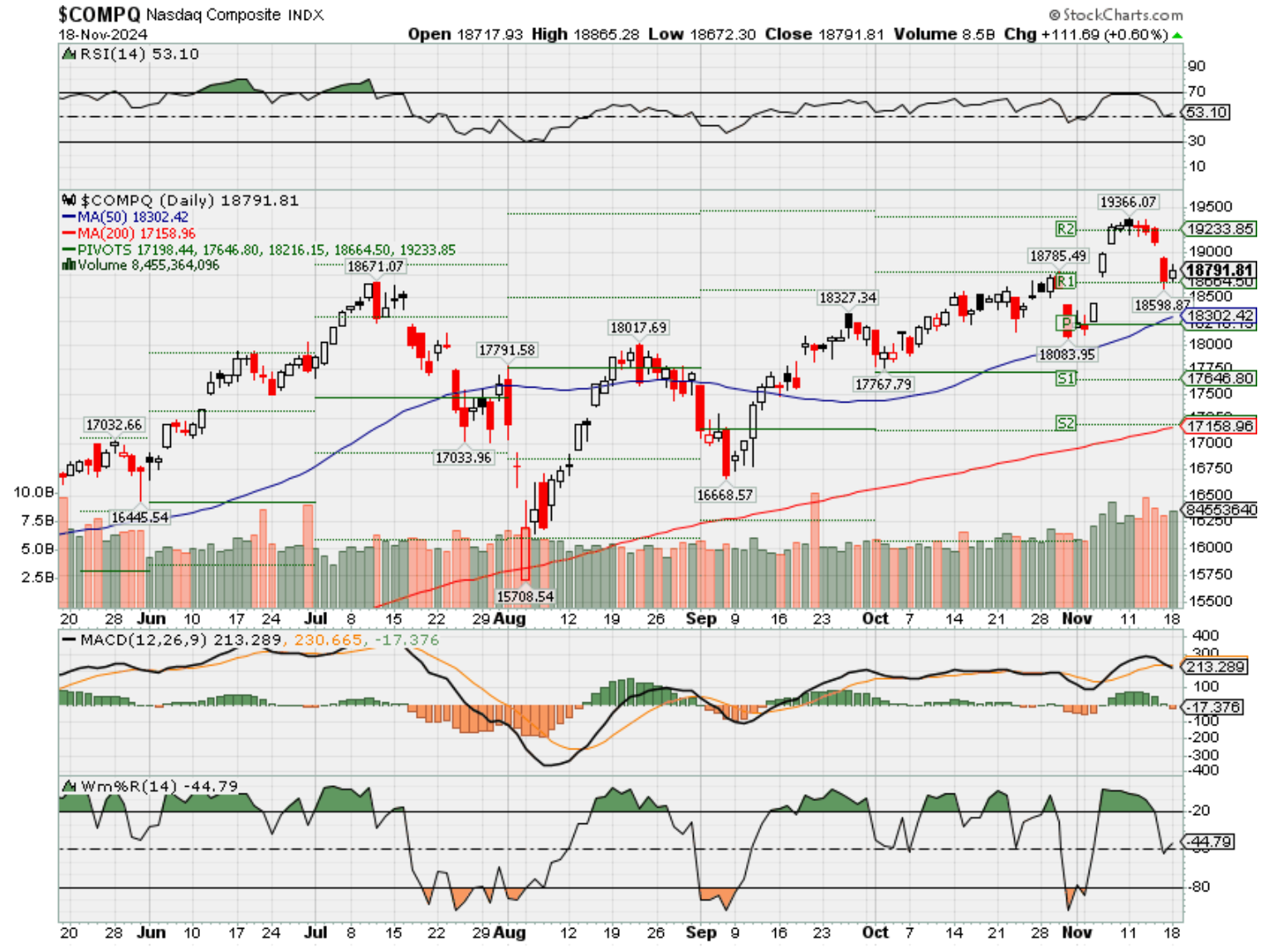

Where will our markets end this week?

Higher

DJIA – Bullish

SPX – Bullish

COMP – Bullish

Where Will the SPX end November 2024?

11-18-2024 +2.00

11-11-2024 +2.00

11-04-2024 ????

10-28-2024 ????

Earnings:

Mon:

Tues: LOW, WMT

Wed: TGT, TJX, JACK, PANW, SNOW, NVDA

Thur: BJ, GAP, INTU, BUDI

Fri: BKE

Econ Reports:

Mon: NAHB Housing, Net Long Term

Tue Building Permits, Housing Starts,

Wed: MBA,

Thur: Initial Claims, Continuing Claims, Existing Home Sales, Leading Indicators, Phil Fed

Fri: Michigan Sentiment

How am I looking to trade?

RIGHT NOW is the time to get ready to back the truck up and load up stocks if the market has a “interest rate or inflation fear” !!!

www.myhurleyinvestment.com = Blogsite

info@hurleyinvestments.com = Email

Questions???

Yes MU for HI is a huge buy right now, Buy Before the NVDA earnings

What investors need to consider when choosing a dividend-paying fund

Published Tue, Nov 12 20248:54 AM EST

Key Points

- Investors who want income may turn to dividend-paying strategies.

- When choosing between funds, it’s important to consider whether the strategy fits your goals and what you will pay, experts say.

For investors who want income, dividends may provide an answer.

Dividends are corporate profits that companies pay to shareholders in the form of either cash or stock.

In comparison to other income-paying investments — such as certificates of deposit, bonds or Treasurys — dividends may provide the opportunity for more appreciation, said Leanna Devinney, vice president and branch leader at Fidelity Investments in Hingham, Massachusetts.

“Dividends can be very attractive because they offer the opportunity for growth and income,” Devinney said.

Dividend investment options may come in the form of single company stocks or dividend-paying funds, like exchange-traded funds or mutual funds.

With individual stocks, it’s easy to see the dividend a company may offer in exchange for owning its share, Devinney said. Notably, not all companies pay dividends.

However, dividend-paying funds like ETFs or mutual funds may provide a broader exposure to dividend securities, often at lower costs, she said.

For investors who are considering putting a portion of their portfolios in dividend-paying strategies to fulfill their income-seeking goals, there are some things to consider.

What kind of dividend-paying fund fits my goals?

Generally, there are two types of dividend funds from which to choose, according to Daniel Sotiroff, senior analyst for passive strategies research at Morningstar.

The first group focuses on high dividend yield strategies. Dividend yield is how much a company pays in dividends each year compared to its stock price. With high-yield strategies, the investor is trying to get higher income than the market generally provides, Sotiroff said.

High-yield dividend companies tend to have been around for decades, like Coca-Cola Co., for example.

Alternatively, investors may opt for dividend growth strategies that focus on stocks expected to consistently grow their dividends over time. Those companies tend to be somewhat younger, such as Apple or Microsoft, Sotiroff said.

‘There’s a lot of good’ for markets in post-election surge, says Hightower’s Stephanie Link

To be clear, both of these strategies have trade-offs.

“The risks and rewards are a little bit different between the two,” Sotiroff said. “They can both be done well; they can both be done poorly.”

If you’re a younger investor and you’re trying to grow your money, a dividend appreciation fund will likely be better suited to you, he said. On the other hand, if you’re near retirement and you’re looking to create income from your investments, a high-yield dividend ETF or mutual fund is probably going to be a better choice.

To be sure, some fund strategies combine both goals of current income and future growth.

How expensive is the dividend strategy?

Another important consideration when deciding among dividend-paying strategies is cost.

One dividend fund that is highly rated by Morningstar, the Vanguard High Dividend Yield ETF, is well diversified, which means investors won’t have a lot of exposure to one company, he said. What’s more, it’s also “really cheap,” with a low expense ratio of six basis points, or 0.06%. The expense ratio is a measure of how much investors pay annually to own a fund.

That Vanguard fund has historically provided a yield of about 1% to 1.5% more than what the broader U.S. market offers, which is “pretty reasonable,” according to Sotiroff.

Get this delivered to your inbox, and more info about about our products and services.

By signing up for newsletters, you are agreeing to our Terms of Use and Privacy Policy.

While investors may not want to add that Vanguard fund to their portfolio, they can use it as a benchmark, he said.

“If you’re taking on higher yield than that Vanguard ETF, that’s a warning sign that you probably have exposure to incrementally more volatility and more risk, Sotiroff said.

Another fund highly rated by Morningstar is the Schwab U.S. Dividend Equity ETF, which has an expense ratio of 0.06% and has also provided 1% to 1.5% more than the market, according to Sotiroff.

Both the Vanguard and Schwab funds track an index, and therefore are passively managed.

Investors may alternatively opt for active funds, where managers are identifying companies’ likelihood to increase or cut their dividends.

“Those funds typically will come with a higher expense ratio,” Devinney said, “but you’re getting professional oversight to those risks.”

The S&P 500 could hit 8,000 by end of the decade: Ed Yardeni

October 15, 2024

The bull market is officially two years old, and as investors head into the third year, Yardeni Research President Ed Yardeni explains what could lie ahead.

Yardeni expects earnings to continue to push the market higher, especially as valuations are “already stretched.” He adds that if valuations increase, it may spark a melt-up, which he tells Yahoo Finance, “You can make a lot of money still from here. But then you got to figure out when to get out. And then you have to get out pretty significantly.”

Overall, he expects earnings to drive market growth and support a bull market: “I’m thinking that the market goes up on earnings and that earnings, which were probably about $250 a share this year, go up to $275 a share next year, and $300 a share the year after that. By the way, by the end of the decade, I think we could be at $400 per share, which times a 20 multiple or so gets us to 8,000 on the S&P 500 (^GSPC). So I think it’s still a bull market.”

With this market backdrop, Yardeni explains that he is Overweight on technology (XLK), industrials (XLI), and financials (XLF). On the other hand, he is “not too keen on” utilities (XLU) and other interest-rate-sensitive areas: “We don’t think interest rates are going to come down as much as the market has been discounting.”

Watch the video above to hear what Yardeni thinks about the bond market (^TYX, ^TNX, ^FVX).

To watch more expert insights and analysis on the latest market action, check out more Market Domination Overtime here.

This post was written by Melanie Riehl

DIS Earnings: Disney Skyrockets after Q4 Earnings Beat Expectations

Annika MasraniNov 14, 2024, 05:45 AM

Disney soars in pre-market trading on stellar Q4 results.

Walt Disney’s DIS -1.34% ▼ stock skyrocketed 10.25% in pre-market trading following an impressive fourth-quarter report for Fiscal 2024. The company reported adjusted earnings per share (EPS) of $1.14, which comfortably surpassed analysts’ consensus of $1.11. The quarterly revenue of $22.6 billion exceeded the forecasted $22.49 billion, marking a 6% year-over-year increase. This robust performance signals that Disney is emerging strong from recent challenges, positioning itself well for future growth.

Don’t Miss our Black Friday Offers:

- Discover the latest stocks recommended by top Wall Street analysts, all in one place with Analyst Top Stocks

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

Disney’s EPS Surpasses Consensus

Disney’s performance in Q4 was particularly strong in terms of earnings. The company posted a notable 79% year-over-year increase in EPS for the quarter, reaching $0.25, compared to $0.14 in Q4 2023. Full-year EPS also more than doubled, jumping to $2.72 from $1.29 in the previous year. The company’s ability to deliver solid profits despite market turbulence reflects the strength of its diversified business model and strategic investments in content and innovation.

Disney’s Entertainment and Streaming Drive Growth

Revenue growth was largely driven by gains in Disney’s entertainment and streaming segments. For Q4, the company reported a 23% growth in total segment operating income, with a significant contribution from Disney’s Direct-to-Consumer (DTC) services, including Disney+ and Hulu. Disney+ saw a 14% rise in ad revenue, adding to the streaming division’s operating income of $321 million for the quarter. Additionally, box office hits like Inside Out 2 and Deadpool 3 helped boost content sales, adding $316 million to operating income.

The company ended Q4 with a total of 174 million Disney+ Core and Hulu subscriptions, which includes more than 120 million paid Disney+ Core subscribers—a 4.4 million increase from the previous quarter. These results suggest strong momentum in Disney’s streaming business, which has been a crucial growth driver in recent years.

Disney Expects Positive Growth for 2025

Looking ahead, Disney remains optimistic about its long-term growth. The company expects high-single-digit adjusted EPS growth for Fiscal 2025 compared to Fiscal 2024, forecasting adjusted EPS between $3.02 to $3.15, up from $2.72 in 2024. The company also expects approximately $15 billion in cash from operations, with capital expenditures of around $8 billion.

For Fiscal 2026, Disney projects double-digit growth in adjusted EPS and cash flows, with segment operating income in Entertainment expected to grow by a double-digit percentage. The company also targets a 6% to 8% increase in operating income for its Experiences segment, with the second half of the year expected to be stronger.

Is Disney a Buy, Sell or Hold?

Analysts remain bullish about DIS stock, with a Strong Buy consensus rating based on 12 Buys and four Holds. Year-to-date, DIS stock has increased by more than 10%, and the average DIS price target of $114 implies an upside potential of 11% from current levels.

Goldman says buy these stocks that are set to benefit most from Trump tax cuts

Published Thu, Nov 7 20242:17 PM ESTUpdated Thu, Nov 7 20245:51 PM EST

As Wall Street gears up for President-elect Donald Trump’s return to the White House, one subset of stocks stands to potentially benefit the most from his plan to cut corporate tax rates, according to Goldman Sachs.

Trump’s victory reduces the political uncertainty hanging over stocks and serves as a near-term catalyst to help drive equities broadly higher, analysts led by Goldman chief U.S. equity strategist David Kostin wrote in a research report on Wednesday. Some of that move came the day after Tuesday’s election, when the Dow Jones Industrial Average soared 3.6%, the S&P 500 surged 2.5% and the Nasdaq Composite jumped nearly 3%, all of them the largest post-Election Day moves in history.

“Along with the resolution of election uncertainty, resilient recent economic growth data and continued Fed rate cuts support the healthy near-term outlook for U.S. stocks,” Kostin wrote. Overall, Kostin forecasts the S&P 500 could end the year at 6,015 if the broad market index follows the historical pattern of returning 4% between Election Day in November and year-end.

The fate of the U.S. House of Representatives remains to be seen, however, and is key to whether Trump enters the White House with unified government fully in Republican hands, or faces a divided Congress. While several races for House seats remain too close to call, the chamber is leaning toward the GOP, which already wrested control of the Senate on Tuesday.

A unified Republican government that swiftly passes Trump’s proposed corporate tax cuts could boost Goldman’s earnings per share growth forecast for S&P 500 companies by four percentage points, Kostin said. Trump favors slashing the corporate tax rate to 15% from 21%. Goldman forecasts earnings per share growth of 11% in 2025 and 7% in 2026. Previously enacted Trump tax cuts are set to expire at the end of 2025 unless Congress extends them or approves new legislation.

To find a group of beneficiaries from lower corporate tax rates, Goldman screened for stocks that have seen the highest median corporate tax rate over the past 10 years. Companies on the list pay median corporate tax rates higher than the S&P 500 median of 21%.

Here is a look at some of the stocks that turned up on Goldman’s screen.

Stocks that may benefit most from a lower corporate tax

| ticker | name | 10-year median tax rate |

| DIS | Walt Disney | 29% |

| LOW | Lowe’s | 30% |

| HLT | Hilton Worldwide | 29% |

| WMT | Walmart | 30% |

| CVX | Chevron | 28% |

| AXP | American Express | 26% |

| CAH | Cardinal Health | 37% |

| DAL | Delta Airlines | 31% |

| SMCI | Super Micro Computer | 21% |

| WDC | Western Digital | 34% |

Source: Goldman Sachs Portfolio Strategy Research

Powell says the Fed doesn’t need to be ‘in a hurry’ to reduce interest rates

Published Thu, Nov 14 20243:00 PM ESTUpdated Thu, Nov 14 20244:30 PM EST

Jeff Cox@jeff.cox.7528@JeffCoxCNBCcom

Key Points

- Federal Reserve Chair Jerome Powell said Thursday that strong U.S. economic growth will allow policymakers to take their time in deciding how far and how fast to lower interest rates.

- “The economy is not sending any signals that we need to be in a hurry to lower rates,” Powell said in Dallas.

Jerome Powell: Fed doesn’t need to be ‘in a hurry’ to reduce interest rates

Federal Reserve Chair Jerome Powell said Thursday that strong U.S. economic growth will allow policymakers to take their time in deciding how far and how fast to lower interest rates.

“The economy is not sending any signals that we need to be in a hurry to lower rates,” Powell said in remarks for a speech to business leaders in Dallas. “The strength we are currently seeing in the economy gives us the ability to approach our decisions carefully.”

In an upbeat assessment of current conditions, the central bank leader called domestic growth “by far the best of any major economy in the world.”

Specifically, he said the labor market is holding up well despite disappointing job growth in October that he largely attributed to storm damage in the Southeast and labor strikes. Nonfarm payrolls increased by just 12,000 for the period.

Powell noted that the unemployment rate has been rising but has flattened out in recent months and remains low by historical standards.

On the question of inflation, he cited progress that has been “broad based,” noting that Fed officials expect it to continue to drift back toward the central bank’s 2% goal. Inflation data this week, however, showed a slight uptick in both consumer and producer prices, with 12-month rates pulling further away from the Fed mandate.

Still, Powell said the two indexes are indicating inflation by the Fed’s preferred measure at 2.3% in October, or 2.8% excluding food and energy.

“Inflation is running much closer to our 2 percent longer-run goal, but it is not there yet. We are committed to finishing the job,” said Powell, who noted that getting there could be “on a sometimes-bumpy path.”

Powell’s cautious view on rate cuts sent stocks lower and Treasury yields higher. Traders also lowered their expectations for a December rate cut.

The remarks come a week after the Federal Open Market Committee lowered the central bank’s benchmark borrowing rate by a quarter percentage point, pushing it down into a range between 4.5% and 4.75%. That followed a half-point cut in September.

Powell has called the moves a recalibration of monetary policy that no longer needs to be focused primarily on stomping out inflation and now has a balanced aim at sustaining the labor market as well. Markets still largely expect the Fed to continue with another quarter-point cut in December and then a few more in 2025.

However, Powell was noncommittal when it came to providing his own forecast. The Fed is seeking to guide its key rate down to a neutral setting that neither boosts nor inhibits growth, but is not sure what the end point will be.

“We are confident that with an appropriate recalibration of our policy stance, strength in the economy and the labor market can be maintained, with inflation moving sustainably down to 2 percent,” he said. “We are moving policy over time to a more neutral setting. But the path for getting there is not preset.”

Powell added that the calculus of getting the move to neutral rate will be tricky.

“We’re navigating between … the risk that we move too quickly and the risk that we move too slowly. We want to go down the middle and get it just right so that we’re providing support for the labor market but also helping enable inflation to come down,” he said. “So going a little slower, if the data let us go a little slower, that seems like a smart thing to do.”

The Fed also has been allowing proceeds from its bond holdings to roll off its mammoth balance sheet each month. There have been no indications of when that process might end.

There’s trouble brewing in the chip sector outside of Nvidia, according to the charts

Published Mon, Nov 18 20241:09 PM ESTUpdated 6 Hours Ago

Outside of Nvidia, semiconductor stocks have faltered during the second half of the year. Since peaking on July 11th, the PHLX Semiconductor Equal Weighted Index has returned approximately a negative 25%, which compares to a nearly 6% gain for the S&P 500 over that same period.

A source of downside leadership within the industry has been in semiconductor equipment stocks. ASML Holdings N.V. (ASML), which is a bellwether in this space, saw an earnings-driven breakdown in October that reversed its cyclical bull trend that been in place since 2022.

Now, U.S. semiconductor equipment stocks like Applied Materials (AMAT) and Lam Research (LRCX) are testing key support levels on their charts, putting their cyclical uptrends in jeopardy. Starting with their monthly charts, AMAT and LRCX have each seen their monthly MACDs shift lower for the first time since early 2022, indicating that long-term momentum has weakened notably in a headwind for the next several months.

Applied Materials monthly chart

Fairlead Strategies, CQG

The monthly stochastics for each are not yet oversold, increasing risk that their corrective phases continue into the first half of 2025.

Lam Research monthly chart

Fairlead Strategies, CQG

For AMAT, it gapped lower last Friday, taking it below support at its weekly cloud model, near $177. Should that breakdown be confirmed with this week’s close, it would be a long-term bearish reversal on the chart. The 2021 high, which is former resistance turned support near $167, is roughly in-line and has the potential to generate short-term stabilization, but a confirmed cloud breakdown would indicate that this level is also vulnerable to breaking. Secondary support is a 61.8% Fibonacci retracement level near $142. Our weekly indicators point lower and show no signs of downside exhaustion, increasing downside risk.

Applied Materials, weekly chart

Fairlead Strategies, CQG

LRCX has already confirmed a breakdown below its weekly cloud model in a long-term bearish development and now has a breakdown pending this Friday’s close below the 2021 peak, which is support near $73. Like AMAT, the weekly MACD is negative for LRCX, and there are no signs of downside exhaustion, increasing risk its corrective phase deepens into year-end. Secondary support is a 61.8% Fibonacci retracement level, near $62.

Lam Research, weekly chart

Fairlead Strategies, CQG

NVDA earnings on Wednesday have the potential to generate short-term volatility for semiconductor stocks as a group. However, the bearish setup on the monthly charts of AMAT and LRCX increases the odds that their breakdowns are ultimately confirmed, even if a short-term rebound keeps support levels intact temporarily.

—Katie Stockton with Will Tamplin

Access research from Fairlead Strategies for free here.

DISCLOSURES: (None)

All opinions expressed by the CNBC Pro contributors are solely their opinions and do not reflect the opinions of CNBC, NBC UNIVERSAL, their parent company or affiliates, and may have been previously disseminated by them on television, radio, internet or another medium.

THE ABOVE CONTENT IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY. THIS CONTENT IS PROVIDED FOR INFORMATIONAL PURPOSES ONLY AND DOES NOT CONSITUTE FINANCIAL, INVESTMENT, TAX OR LEGAL ADVICE OR A RECOMMENDATION TO BUY ANY SECURITY OR OTHER FINANCIAL ASSET. THE CONTENT IS GENERAL IN NATURE AND DOES NOT REFLECT ANY INDIVIDUAL’S UNIQUE PERSONAL CIRCUMSTANCES. THE ABOVE CONTENT MIGHT NOT BE SUITABLE FOR YOUR PARTICULAR CIRCUMSTANCES. BEFORE MAKING ANY FINANCIAL DECISIONS, YOU SHOULD STRONGLY CONSIDER SEEKING ADVICE FROM YOUR OWN FINANCIAL OR INVESTMENT ADVISOR.

Click here for the full disclaimer.

Fairlead Strategies Disclaimer:

This communication has been prepared by Fairlead Strategies LLC (“Fairlead Strategies”) for informational purposes only. This material is for illustration and discussion purposes and not intended to be, nor construed as, financial, legal, tax or investment advice. You should consult appropriate advisors concerning such matters. This material presents information through the date indicated, reflecting the author’s current expectations, and is subject to revision by the author, though the author is under no obligation to do so. This material may contain commentary on broad-based indices, market conditions, different types of securities, and cryptocurrencies, using the discipline of technical analysis, which evaluates the demand and supply based on market pricing. The views expressed herein are solely those of the author. This material should not be construed as a recommendation, or advice or an offer or solicitation with respect to the purchase or sale of any investment. The information is not intended to provide a basis on which you could make an investment decision on any particular security or its issuer. This document is intended for CNBC Pro subscribers only and is not for distribution to the general public. Certain information has been provided by and/or is based on third party sources and, although such information is believed to be reliable, no representation is made with respect to the accuracy, completeness, or timeliness of such information. This information may be subject to change without notice. Fairlead Strategies undertakes no obligation to maintain or update this material based on subsequent information and events or to provide you with any additional or supplemental information or any update to or correction of the information contained herein. Fairlead Strategies, its officers, employees, affiliates and partners shall not be liable to any person in any way whatsoever for any losses, costs, or claims for your reliance on this material. Nothing herein is, or shall be relied on as, a promise or representation as to future performance. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS. Opinions expressed in this material may differ or be contrary to opinions expressed, or actions taken, by Fairlead Strategies or its affiliates, or their respective officers, directors, or employees. In addition, any opinions and assumptions expressed herein are made as of the date of this communication and are subject to change and/or withdrawal without notice. Fairlead Strategies or its affiliates may have positions in financial instruments mentioned, may have acquired such positions at prices no longer available, and may have interests different from or adverse to your interests or inconsistent with the advice herein. Any investments made are made under the same terms as nonaffiliated investors and do not constitute a controlling interest. No liability is accepted by Fairlead Strategies, its officers, employees, affiliates, or partners for any losses that may arise from any use of the information contained herein. Any financial instruments mentioned herein are speculative in nature and may involve risk to principal and interest. Any prices or levels shown are either historical or purely indicative. This material does not take into account the particular investment objectives or financial circumstances, objectives or needs of any specific investor, and are not intended as recommendations of particular securities, investment products, or other financial products or strategies to particular clients. Securities, investment products, other financial products or strategies discussed herein may not be suitable for all investors. The recipient of this information must make its own independent decisions regarding any securities, investment products or other financial products mentioned herein. The material should not be provided to any person in a jurisdiction where its provision or use would be contrary to local laws, rules, or regulations. This material is not to be reproduced or redistributed absent the written consent of Fairlead Strategies.

Russia warns U.S. is adding fuel to fire with long-range missile decision

Published Mon, Nov 18 20249:21 AM ESTUpdated Mon, Nov 18 202412:51 PM EST

Key Points

- The U.S. decision, reported by NBC News, marks a major reversal in Washington policy a mere two months before the mandate expiry of President Joe Biden, who has steered U.S. engagement in the Ukraine conflict since Russia’s wholescale invasion in February 2022.

- “It is obvious that the outgoing administration in Washington intends to take steps to continue adding fuel to the fire and continue to provoke tension around this conflict,” Kremlin spokesperson Dmitry Peskov said earlier on Monday, according to Reuters.

- Analysts at the Institute for the Study of War warn that Washington’s limited authorization could prove insufficient to materially alter the course on the battlefield.

The Kremlin has lashed back against a White House decision to now allow Ukraine to use U.S.-made long-range weapons for limited strikes inside Russian territory.

The decision, reported by NBC News, marks a major reversal in Washington policy a mere two months before the mandate expiry of President Joe Biden, who has steered U.S. engagement in the Ukraine conflict since Russia’s wholescale invasion in February 2022.

Previously, the Biden administration had limited the deployment of American-made long-range arsenal to the Ukrainian battlefield, but had green lit Kyiv’s use of U.S.-made High Mobility Artillery Rocket Systems, HIMARS, in cross-border attacks to defend Ukraine.

The latest authorization follows the deployment of North Korean troops to support Moscow in the stagnating conflict, along with what Ukrainian President Volodymyr Zelenskyy qualified as “one of the largest Russian strikes” against his country over the weekend.

“It is obvious that the outgoing administration in Washington intends to take steps to continue adding fuel to the fire and continue to provoke tension around this conflict,” Kremlin spokesperson Dmitry Peskov said earlier Monday, according to Reuters.

“If such a decision was really formulated and communicated to the Kyiv regime, then, of course, this is a qualitatively new round of tension and a qualitatively new situation from the point of view of the US involvement in this conflict,” he added, in Google-translated comments reported by Russian state news agency Ria Novosti.

Ukraine depends on Western allies for military and humanitarian aid, including the provision of weapons — which NATO members have largely supplied for defensive purposes on Ukrainian grounds, amid fears of further war escalation and Russian retaliation. Speaking to journalists on Sept. 12, Kremlin leader Vladimir Putin had warned that a then-potential decision on behalf of any NATO country to allow Ukraine the use of long-range weapons against targets on Russian soil would amount to direct participation in the war.

“The issue is not about allowing the Ukrainian regime to strike Russia with these weapons or not. The issue is about making a decision: NATO countries directly participate in the military conflict or not. If this decision is made, it will mean nothing other than the direct participation of NATO countries — the United States, European countries — in the war in Ukraine,” Putin said at the time, according to Russian state news agency Tass.

Yet analysts at the Institute for the Study of War warn that Washington’s limited authorization could prove insufficient to materially alter the course on the battlefield.

“The partial lifting of restrictions on Ukraine’s use of Western-provided long-range weapons against military objects within Kursk Oblast will not completely deprive Russian forces of their sanctuary in Russian territory, as hundreds of military objects remain within ATACMS range in other Russian border regions,” they said in a note, with reference to the U.S. long-range Army Tactical Missile System.

They added that “Russian forces will benefit from any partial sanctuary if Western states continue to impose restrictions on Ukraine’s ability to defend itself and that the US should allow Ukraine to strike all legitimate military targets within Russia’s operational and deep-rear within range of US-provided weapons – not just those in Kursk Oblast.”

“The only way to truly stop this terror is to eliminate Russia’s ability to launch attacks. And this is absolutely realistic,” Zelenskyy said Monday on social media, without directly referencing the reports of the U.S. permission. “It is not just defense; it is justice— the right way to protect our people. Any nation under the attack would act this way to defend its citizens. We must do the same, together with our partners. Russia must be left with no capacity for terror.”

It remains to be seen whether European countries will follow Washington’s suit over Kyiv’s use of their weapons. CNBC has reached out to the foreign ministries of major Western NATO allies Germany, France and the U.K. for comment.

EU foreign affairs ministers are meanwhile gathering in Brussels on Monday to hold talks that will also touch on the Ukraine conflict.

“I’ve been saying once and again that Ukraine should be able to use the arms we provided to them, in order to not only to stop the arrow, but also to be able to hit the archers. I continue to believe this is what has to be done. And I’m sure will be discussed once again. I hope members will agree on that,” EU foreign policy chief Josep Borrell said before the meeting.

Such a decision raises questions over the extent of Ukraine’s current long-range missile arsenal to support direct attacks, at a time when NATO braces for the White House return of U.S. President-elect Donald Trump – who has previously pledged to end the war in Ukraine within a day of assuming power, without supplying details.

Nevertheless, the U.S. authorization “could mark a paradigm shift in the war,” Tytti Tuppurainen, member of the Finnish Parliament, told CNBC’s Silvia Amaro on Monday.

“If it is true … I think we welcome that, we welcome that full heartedly. If it is one thing we regret, it is that it comes so late,” she added. “Europe has to stand up now. This is a critical moment. This is certainly a wake-up call for Europe. From the U.S. side, the election of Donald Trump tells us that we have to take the responsibility of our own destiny, and if Russia wins in Ukraine, it means that Russia will only continue.”