HI Market View Commentary 07-22-2024

What’s happening in today’s market???=

Lot’s of volatility = Political uncertainty = VP Vance for Trump, Harris is the candidate for the democrats but not elected/chosen democratically

First assignation attempt since Ronald Regan

13% of S&P 500 had earnings 80% beating but 30% come this week and 30% ish more nextweek

Rotation out of tech into small caps, energy, health and Finance

Small CAPS = IWM Russell 2000 index small companies with huge potential growth = borrow money to fund ALL aspects of the business = much more sensitive to interest rate hikes and cuts

Earnings = big movmements next two weeks

Rebound = coming off over bought

Markets will seem bullish on Trump Tax breaks / Tariffs can hurt the markets

My concern is a recession = Earnings will tell a lot

GDP / GDP Deflator = Thursday

VZ met EPS $1.15 vs est $1.15 Revunue 32,800 B vs est 33,048

Misses revenues by 250 Million dollars

Our Mag 7 stocks we took profits and rolled long puts lower= NVDA, GOOGL

Highlights

- With the third estimate, Q1 GDP was revised up to 1.4% (Briefing.com consensus 1.3%) from 1.3%, although personal spending growth was revised down to 1.5% from 2.0%.

- The GDP Price Deflator was revised up to 3.1% (Briefing.com consensus 3.1) from 3.0%.

Key Factors

- Personal consumption expenditure growth was revised to 1.5% from 2.0% in the second estimate and 3.3% in the fourth quarter. PCE contributed 0.98 percentage points to growth.

- Gross private domestic investment was up 4.4% versus 3.2% in the second estimate and 0.7% in the fourth quarter. Gross private domestic investment contributed 0.77 percentage points to growth.

- Exports increased 1.6% versus 1.2% in the second estimate and 5.1% in the fourth quarter. Imports rose 6.1% versus 7.7% in the second estimate and 2.2% in the fourth quarter. Net exports subtracted 0.65 percentage points from growth.

- Government spending increased 1.8% versus 1.3% in the second estimate and 4.6% in the fourth quarter. Government spending contributed 0.31 percentage points to growth.

- Real final sales of domestic product, which excludes the change in private inventories, increased 1.8% versus 1.7% in the second estimate and 3.9% in the fourth quarter.

- The personal savings rate as a percentage of disposable personal income was 3.8%, unchanged from the second estimate and versus 3.7% in the fourth quarter.

- The PCE price index increased 3.4% versus 3.3% in the second estimate and 1.8% in the fourth quarter. The core PCE price index, which excludes food and energy, increased 3.7% versus 3.6% in the second estimate and 2.0% in the fourth quarter.

Big Picture

- The key takeaway from the report is that it is dated (we’re just days away from the end of Q2) so its impact should be limited; however, the slowdown in personal spending is noteworthy in light of more anecdotal evidence in the interim that suggests consumers, in aggregate, are reining in their discretionary spending.

| Category | Q1 | Q4 | Q3 | Q2 | Q1 |

| GDP | 1.4% | 3.4% | 4.9% | 2.1% | 2.2% |

| Inventories (change) | $28.6B | $54.9B | $77.8B | $14.9B | $27.2B |

| Final Sales | 1.8% | 3.9% | 3.6% | 2.1% | 4.6% |

| PCE | 1.5% | 3.3% | 3.1% | 0.8% | 3.8% |

| Nonresidential Inv. | 4.4% | 3.7% | 1.4% | 7.4% | 5.7% |

| Structures | 3.4% | 10.9% | 11.2% | 16.1% | 30.3% |

| Equipment | 1.6% | -1.1% | -4.4% | 7.7% | -4.1% |

| Intellectual Property | 7.7% | 4.3% | 1.8% | 2.7% | 3.8% |

| Residential Inv. | 16.0% | 2.8% | 6.7% | -2.2% | -5.3% |

| Net Exports | -$960.3B | -$918.5B | -$930.7B | -$928.2B | -$935.1B |

| Export | 1.6% | 5.1% | 5.4% | -9.3% | 6.8% |

| Imports | 6.1% | 2.2% | 4.2% | -7.6% | 1.3% |

| Government | 1.8% | 4.6% | 5.8% | 3.3% | 4.8% |

| GDP Price Index | 3.1% | 1.6% | 3.6% | 1.7% | 3.9% |

Flights were returning to normal, cruise ships have higher booking numbers, national parks have an increase in foot traffic

Where is the problem that is causing people to spend less?= Higher debt=running up credit cards, running out of savings, job lasses, inflation on goods- food/gas.

https://www.briefing.com/the-big-picture

The Big Picture

Last Updated: 19-Jul-24 15:32 ET | Archive

The Buffett Indicator is playing with fire

Is the stock market due for a correction? Some think so. Goldman Sachs recently published a research note suggesting the stock market is at risk of a “setback in the summer” and shifted to a neutral stance for equities on a three-month horizon. It was pointed out in that same note, however, that the firm is still overweight equities for a 12-month horizon.

This notion of a summer setback, then, would be considered a tactical call.

The message between the lines is that one might want to think about trimming one’s exposure to the equity market if one wants to avoid a setback this summer. That’s a defensible view in light of how far the stock market — and its mega-cap leaders — has risen in a short amount of time.

There is another indicator out there, however, that also points to a higher risk of a correction, if not something more. That would be the Buffett Indicator.

Playing with Fire

What is the Buffett Indicator? It is the ratio of the Wilshire 5000 market capitalization to nominal GDP.

It is known as the Buffet Indicator because Warren Buffett (you might have heard of him) called attention to it as possibly the best single measure of valuation. He did this in an interview with Forbes Magazine in late 2001.

Mr. Buffett provided some added perspective on how to think of this ratio:

“If the percentage relationship falls to the 70% or 80% area, buying stocks is likely to work very well for you. If the ratio approaches 200%–as it did in 1999 and a part of 2000–you are playing with fire.”

Let’s take a look now where the Buffet Indicator stands.

For the record, the Buffett Indicator is just shy of 200%. That is interesting because that is where it was in December 2021, or just before the swoon of 2022 that was precipitated by the Fed’s aggressive tightening campaign.

It is double where it was just before the financial crisis and it is nearly 40% greater than where the ratio stood at the peak of the dot-com bubble.

We can imagine what Warren Buffett might be thinking these days about the market’s valuation. If there was a thought bubble above his head, it might look something like this:

Note the trajectory of Berkshire Hathaway’s cash position. It looks closely aligned with the Buffet Indicator, which is to say Berkshire Hathaway looks ready to strike opportunistically in the event of a valuation reset (much like it appeared to do in 2022).

A Nice Dividend

If nothing else, Berkshire Hathaway’s massive cash position implies Mr. Buffett isn’t looking to play with fire.

Given how far the stock market has run, some might contend that Berkshire Hathaway and Warren Buffett have gotten burned sitting on all that cash (and cash-like instruments). These people shouldn’t forget that Apple (AAPL) is one of Berkshire Hathaway’s largest public holdings or that T-bills and money market funds have offered a decent and mostly risk-free return.

The latest 13F filing in May showed Berkshire Hathaway trimmed its position in Apple to 789.37 million shares from 905.56 million shares. Apple pays a quarterly dividend of $0.25 per share, which equates to $1.00 per year. In other words, Berkshire Hathaway is in line to receive nearly $800 million in dividends alone from its Apple position.

To be sure, Warren Buffett has not gotten burned while the stock market has continued to snub its nose at the Buffett Indicator.

What It All Means

Markets can stay overbought longer than one might think. The reverse holds true in that they can remain oversold longer than one might think, too. The Buffett Indicator at this point, however, doesn’t connote a market in an oversold position. It does suggest it is overbought and, more directly, overvalued.

It is just one indicator, however, so it shouldn’t be taken in isolation as the be all-end all indicator for investment decisions. What the Buffett Indicator connotes is that valuation risk at the index level is greater now and that one needs to be more discerning in allocating money to the market, as well as to individual stocks.

The need for discernment is evident in Berkshire Hathaway’s cash position running figuratively a step ahead of the stock market’s run to record highs.

—Patrick J. O’Hare, Briefing.com

Earnings dates:

AAPL 08/01 AMC

BA 07/31 BMO

BABA 08/08 BMO

BIDU 08/22 BMO

DG 08/29 est

DIS 08/07 BMO

F 07/24 AMC

GM 07/23 BMO

GOOGL 07/23 AMC

JCI 08/01 est

KO 07/23 BMO

LMT 07/23 BMO

META 07/31 AMC

MU 09/25 est

MRO 05/01 AMC

O 08/05 AMC

SQ 08/01 AMC

TGT 08/21 BMO

UAA 08/09 est

V 07/23 AMC

VZ 07/22 BMO

ZION 07/22 AMC

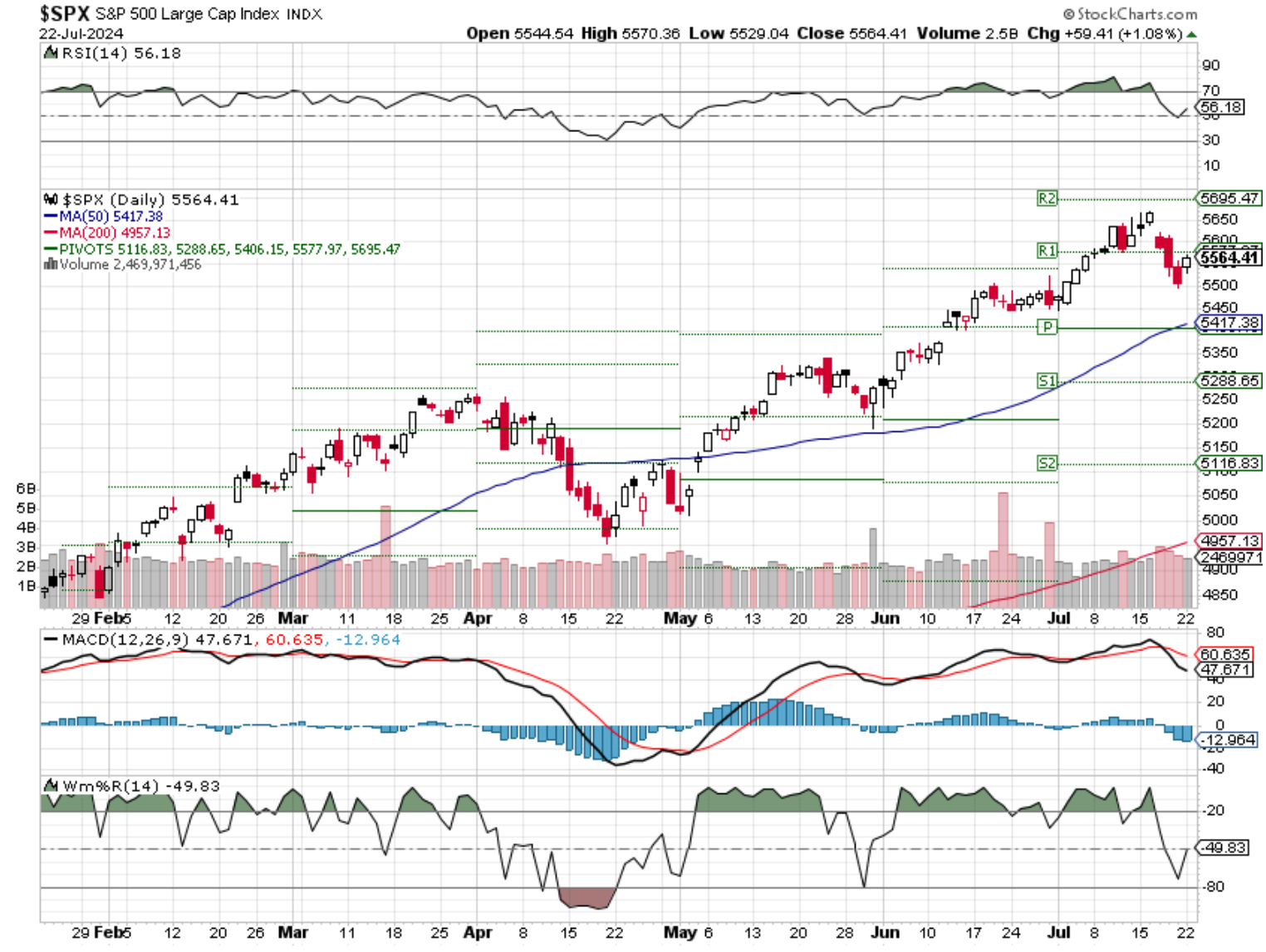

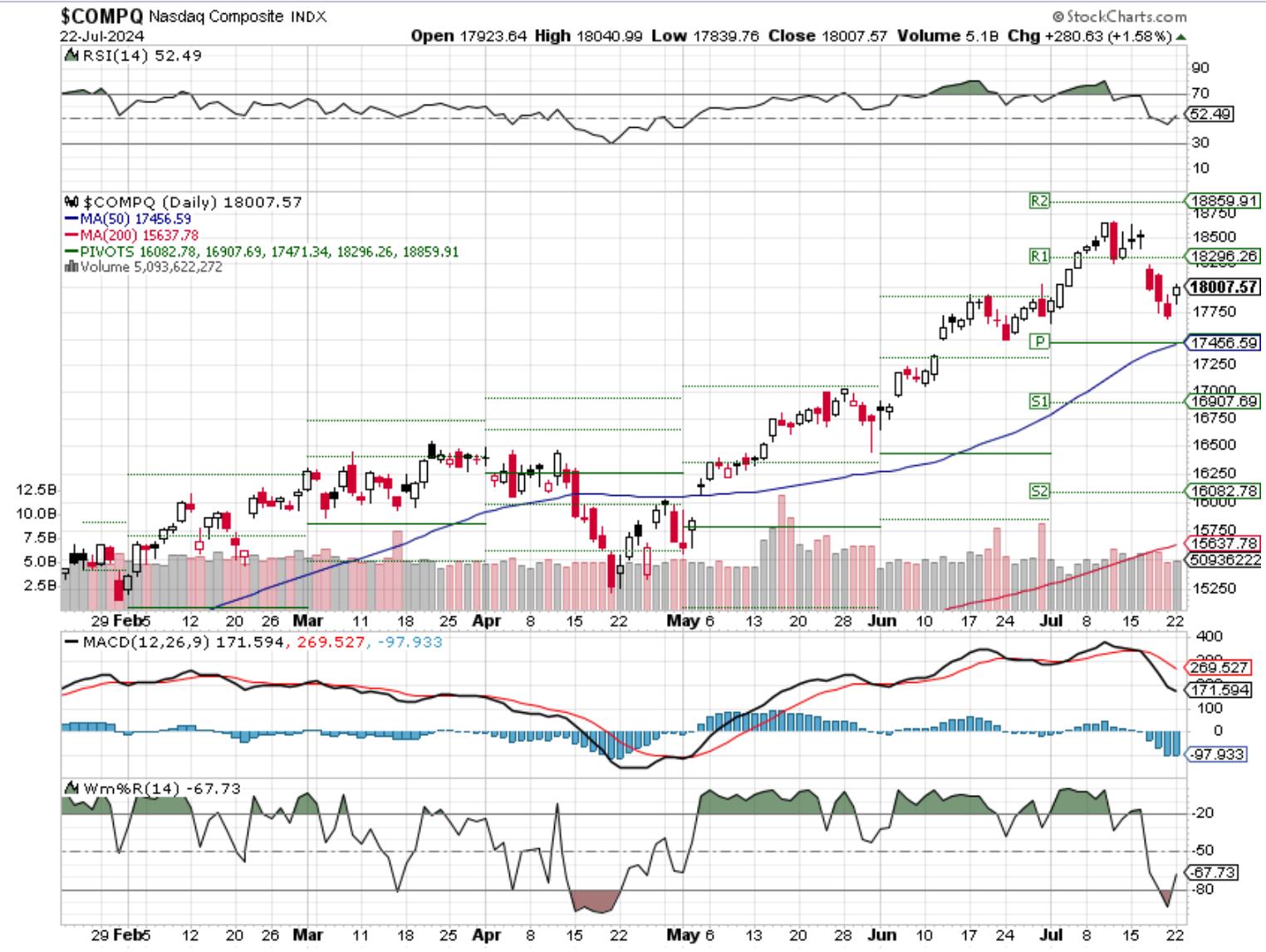

Where will our markets end this week?

Higher

DJIA – Bullish

SPX – Bullish

COMP – Bullish

Where Will the SPX end July 2024?

07-22-2024 +2.00%

07-15-2024 -2.00%

07-08-2024 -2.00%

07-01-2024 -2.00%

Earnings:

Mon: CLF, NUE, VZ, ZION,

Tues: FCX, PM, PHM, UPS, COF, V, KO, GM, GOOGL, TSLA,

Wed: T, CME, IP, CMG, IBM, VMI, WM, WHR

Thur: AAL, HON, KDP, RCL, LUV, UNP, VLO, JNPR, SKYW

Fri: MMM, BMY

Econ Reports:

Mon:

Tue Existing Home Sales,

Wed: MBA, New Home Sales,

Thur: Initial Claims, Continuing Claims, GDP, GDP Deflator, Durable Goods, Durable ex-trans,

Fri: PCE, PCE CORE, Michigan Sentiment, Personal Income, Personal Spending,

How am I looking to trade?

Protection On Everything

www.myhurleyinvestment.com = Blogsite

info@hurleyinvestments.com = Email

Questions???

A ‘triple-whammy’ threat is building for U.S. stock investors, strategist warns

Last Updated: July 9, 2024 at 8:35 a.m. ETFirst Published: July 9, 2024 at 6:58 a.m. ET

By

Barbara Kollmeyer

Critical information for the U.S. trading day

Investors are climbing those S&P peaks as they face a trio of threats, warns Shard Capital’s Bill Blain.

Lit green for July thus far, the S&P 500 faces a big economic and earnings week, kicking off with Fed Chair Jerome Powell this morning.

Our call of the day from Shard Capital’s market strategist Bill Blain warns U.S. stock investors face a “standard triple-whammy threat: overvaluation on over-euphoria, misunderstanding the economic reality, and the political aspect.”

Blain says in a blog post that while markets “seem unstoppable,” history is full of mean reversions as he sees U.S. politics feeding a “volatile” four months ahead.

The strategist compares past treks up a Scottish mountain famed for its false summits to markets now: “Climbing Schiehallion is almost as pointless and foolish as believing stock markets will rally forever. On the basis ‘Markets have no memory’ they are doomed to repeat the same mistakes repeatedly, at some point there will inevitably be a reckoning.”

“Issue no 1 for the U.S. market is the behavioral psychosis driving the market: irrational hopes and expectations trumps rationality at times like these,” with greed continuing to drive money into American stocks and private markets. U.S. are valued much higher than Europe, emerging markets or China partly because it’s awash in so much capital.

He also warns over the impact of what he calls the new normality, of interest rates around 5%. “Central banks and regulators want normalized interest rates, not the monetary and market distortions created by artificially low interest rates,” he says.

And his final concern is over the U.S. election, as he says the election period could become highly unstable, such as calls from some Democrats for President Joe Biden to drop out to the possibility he could stage a comeback against former President Donald Trump, perceived by some as a market friendlier candidate. That’s not to mention, he adds, if demand recounts in some states and other post-election events occur.

The buzz

Fed Chairman Powell will testify in front of the Senate Banking Committee at 10 a.m., with Treasury Sec. Janet Yellen giving separate testimony in front of the House Financial Services Committee. Fed Gov. Michelle Bowman is due to speak at 1:30 p.m.

The NFIB small business optimism reached the highest reading of the year in June.

https://seekingalpha.com/article/4702918?gt=d1e41e8f9b6224a8

Disney: Still Missing The Magic

Jul. 08, 2024 9:00 AM ET

This article is a gift from a Seeking Alpha Premium subscriber

Welcome to Seeking Alpha. Register for free today and continue enjoying the benefits that come with being a part of our global community

Summary

- Disney’s shift towards a direct-to-consumer model is risky during an economic downturn, with revenue growth lagging behind competitors like Netflix.

- Concerns over Disney’s overvalued share price, plateauing business growth, and reliance on cost-cutting measures indicate a potential downward trend.

- Despite new content releases and entertainment experiences, competition remains strong and economic conditions may impact Disney’s future success.

RinoCdZ

Investment Thesis

In my last article on the house of mouse, I rated Disney (NYSE:DIS) as a hold given what I believe to be as foundational issues with Disney+ streaming strategy. However, their recent performance has led me to change my stance. One of my primary concerns is the company’s increasing reliance on their direct-to-consumer (DTC) segments, such Disney+ which I mentioned before, and has not met expectations, but also other DTC business lines like their parks division. Despite the initial promise of a vast library of content for their Disney+ division, Disney has shifted towards producing new content, a strategy more aligned with Netflix but also one that eliminates what content edge they had.

Being less dependent on enterprise cable sales and more on their DTC segment is highly risky in my opinion. This avenue for revenue is highly sensitive to economic downturns especially given the premium price point they charge for certain products like their parks and entertainment packages. Business for Disney has seemed to plateau, likely caused by the slowing consumer spending and tightening of budgets. For instance, Disney+ lost 1.6 million international subscribers in the second quarter of 2024. The company’s shares, based on their price to earnings ratio (P/E), seem to be overvalued.

Looking at their competitors, the performance of Disney+ significantly lags behind Netflix both in content and now facing new threats in their physical entertainment division. Disney+’s revenue growth does not look promising, with only a 2.84% year-over-year increase projected for fiscal year 2024, compared to Netflix’s projections of 13% to 15%. Downward revisions in revenue estimates further exacerbate this problem, with 19 downward revisions, compared to 4 upward, in the last three months alone. It is clear that Disney seems to be under financial strain, considering the company hopes to implement $7.5 billion in cost cuts to offset declining revenues.

Given these factors, I am personally downgrading Disney’s stock to a strong sell. The increased dependency on the DTC segment during an economic downturn, combined with an overvalued share price and plateauing business growth, leaves me concerned over the company’s future.

Why I Am Doing Followup Coverage

Since my last article on Disney in March, share price has dropped by 16.19%, while the S&P 500 has outperformed the company, jumping by 6.19%.

As I mentioned above, Disney+’s original intent was to serve as a platform that consisted of years of content in one library. However, the company has recently been turning their focus towards investing heavily in new content, running contrary to the original value proposition. Because of this, their business model is fairly similar to Netflix, who has also been focusing on producing a large quantity of new content.

The purpose of this follow-up coverage is not to just harp on poor Disney+ performance (even though I warned of this in March). Rather, this is to show that all of the other divisions that were supposed to drive operating profits while the company pivoted away from cable are now slowing as well.

With a weakening consumer base, and concerns over the companies, I think it is important to do follow-up coverage.

Performance Is Still Lacking

Disney’s performance, particularly in its streaming services, continues to lag behind their competitors, especially Netflix. As I mentioned above, Disney actually lost about 1.6 million subscribers worldwide in their last quarter. On the other hand, Netflix (NFLX) gained over 9 million in their last quarter.

During the earnings call, there were some quotes that really stood out to me regarding their future performance. For example, Hugh Johnston, CFO, mentioned

we are forecasting a loss for Entertainment DTC in the third quarter, the vast majority of which is due to Disney+ Hotstar’s ICC cricket rights. We also do not expect to see core subscriber growth at Disney+ in the third quarter – Q2 2024 earnings call.

Compared to Netflix’s 9.9 million subscriber gain in Q1 this is rough.

Looking at revenue, below is a chart of Disney+’s revenue.

Disney+ Revenue (Business of Apps)

While their revenue has been largely increasing (somewhat driven due to price hikes), their recent quarterly revenue was about $2.643 billion. However, looking at Netflix, it is clear Disney is lagging behind.

Netflix Revenue (Stock Analysis)

Although he later went on to say that numbers will likely turn around in the fourth quarter, this still leaves me weary regarding their future. Johnston also mentioned during the call that:

the third quarter’s results will be impacted by three additional factors, higher wage expenses, pre-opening expenses related to the Disney treasure and adventure cruise ships, as well as Disney Cruise Line’s New Island, Lookout Cay, and some normalization of post-COVID demand – Q2 2024 earnings call.

He further expands on this “normalization” stating:

[we’re] seeing some evidence of a global moderation from peak post-COVID travel – Q2 2024 earnings call.

The quotes above mainly discuss Q3’s expected performance, but Johnston also went on to state that:

pressures from wages, reopening costs and demand impacts are expected to persist in Q4 – Q2 2024 earnings call.

Although he believes operating income growth will rebound in the same quarter, I am still concerned over their future performance.

With rising inflation and economic uncertainty, many families are cutting back on discretionary spending, making it harder for Disney to attract visitors to their parks and cruises. The company acknowledged some of the struggles faced by their parks, as CFO, Hugh Johnston, stated in their Q2 call:

At Disneyland, despite growing attendance and per-capita spend, results declined year-over-year due to cost inflation, including from higher labor expenses – Q2 2024 earnings call.

With this, as I mentioned above, Disney’s theme parks division is very sensitive to economic conditions. For example, an economic assessment completed by Harold L Vogel, a CFA, revealed that a 1% rise in unemployment rate correlates to a 3% drop in U.S. Disney park attendance.

Overall, I believe Disney’s performance is very sensitive to any economic downturn. Until Disney can demonstrate significant improvement across their business segments, and make them more robust to consumer spending, the company’s performance will likely continue to lag behind their competitors. I think the company’s P/E multiple does not yet reflect this.

Valuation

Disney’s current valuation appears increasingly unsustainable given the company’s anemic revenue growth and elevated price-to-earnings (P/E) ratio. The company has experienced a notable slowdown in revenue, with projections indicating 2.84% year-over-year growth for fiscal year 2024. I believe this modest growth rate is insufficient to justify Disney’s high P/E ratio, which remains elevated compared to the industry average. Disney’s forward non-GAAP P/E ratio is 20.60, which is 62.97% higher than the sector median of 12.64. Such a discrepancy suggests that the market may be overly optimistic about Disney’s future earnings potential.

Adding to the concerns, Disney has faced numerous downward revisions in their revenue estimates. Over the past three months, there have been 19 downward revisions, and only 4 upward revisions. This ratio of downward to upward revisions highlights the increasing skepticism among analysts about the company’s ability to meet their financial targets.

In an attempt to maintain performance, Disney has resorted to significant cost-cutting measures, announcing their plan to cut $7.5 billion. While these cuts are necessary to manage short-term financial pressures, they come at a critical time when the company needs to invest heavily in order to compete with their competitors, who as I mentioned above, are already outperforming them greatly. These cost cuts are only a one-off measure too, meaning that this is a temporary bump in EPS growth, but the company has to be more creative in the long run to get their EPS to compound.

Given these factors, I believe Disney’s valuation should be adjusted downward to reflect the sector median. Based on the company’s P/E ratio, if it was adjusted to the sector median, this would represent 38.6% downside.

Bull Thesis

Despite the numerous challenges and the recent underperformance, I think there could still be some reasons to be optimistic about Disney’s future. The company has an impressive content slate lined up, which could potentially turn the tide. For example, Disney is currently working on new content such as Deadpool & Wolverine, Mufasa: The Lion King, and Moana 2. One of their most recent releases, Inside Out 2, has already proven to be a huge success. This movie, only being in theaters for a few weeks, has passed $1 billion at the global box office.

This content slate doesn’t just stop here. Below is an image from the company’s earnings deck.

Disney Content Slate (Disney Investor Relations)

This image presents the vast amount of content Disney will be releasing in the next year. If these movies are as successful as “Inside Out 2”, the company’s revenue could be promising.

However, while this new content may seem promising for Disney, competition is stronger than before. In addition to this, this new movie slate may struggle to live up to the older slates such as the Marvel Series.

The company also continues to build on their current line of entertainment experiences. As shown during the earnings call presentation, Disney plans to open multiple new entertainment experiences. For example, Fantasy Springs, Lookout Cay, Tiana’s Bayou Adventure (which all opened in June), and the Disney Treasure cruise. However, as I previously mentioned, these revenue routes are highly sensitive to any downturn in economic conditions. If consumers do not have the money, these business sectors will not be successful for Disney even if they are new and novel.

Takeaway

Unfortunately, despite Disney’s iconic brand and rich history, I now think they are a strong sell. The company’s shift towards a direct-to-consumer model during a potential impending economic downturn, combined with their overvalued share price and plateauing business growth, greatly concerns me. I think, as I mentioned above, Disney’s attempts to cut costs may provide a short-term boost but could lead to long-term consequences. If they reduce investment in improving customer experience, it is likely they will fall even further behind competitors such as Netflix. The house of mouse appears overvalued at this point.

This article was written by

This account is managed by Noah’s Arc Capital Management. Our goal is provide Wall Street level insights to main street investors. Our research focus is mainly on 20th century stocks (old economy) undergoing a 21st century transformation, but occasionally we’ll write on companies that help transform 20th century firms as well. We look for innovations in a business model that will cause a stock to change dramatically. Associated with SA contributors Thomas Potter and Elijah Buell.

Show more

Show More

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Noah Cox (account author) is the managing partner of Noah’s Arc Capital Management. His views in this article are not necessarily reflective of the firms. Nothing contained in this note is intended as investment advice. It is solely for informational purposes. Invest at your own risk.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Amazon sellers lose coveted buy box ahead of Prime Day after Target discount snafu

PUBLISHED SAT, JUL 13 20248:30 AM EDT

KEY POINTS

- Amazon sellers interviewed by CNBC said they were penalized after the company’s pricing algorithms found their items were being sold for less on Target’s online marketplace.

- Target ran a competing discount event, which ends Saturday, in the lead-up to Amazon’s Prime Day next week.

- Amazon’s pricing algorithms have been the focus of an FTC lawsuit.

When Brandon Fishman ran a discount on his vitamin-infused coffee for Target’s weeklong deals event, he wasn’t worried about how it would affect his business on Amazon. He certainly didn’t expect his sales there to “fall off a cliff.”

Fishman was in for a rude surprise. During Target’s sales event this week, Amazon’s automated systems detected his bag of VitaCup coffee was available there for $13.43, about $1.50 cheaper than his listing on Amazon.com.

One of Amazon’s key tenets is that it offers “the lowest prices across Earth’s largest selection.” It’s up to Amazon merchants to fulfill that promise, and those who sell their items for a lower price on a competing website risk losing perhaps the most valuable virtual real estate in e-commerce: the buy box. That’s the listing that pops up first when a visitor clicks on a particular product, and the one that gets purchased when a shopper taps “Add to Cart.”

Even though Fishman is the owner of the VitaCup brand, he said he lost the buy box to a reseller of his coffee products.

“I’ve had to purposely lose the buy box all week because of this Target issue, and my sales went way down on Amazon,” said Fishman, who has been selling VitaCup coffee on Amazon since 2017, pulling in roughly $20 million in annual sales on the site.

Target to stop accepting personal checks: Here’s why

Amazon has long relied on algorithms that continuously scan the internet to match or beat the price of products listed elsewhere. Other marketplaces, including Walmart, use similar systems in a bid to offer the cheapest prices.

Amazon’s algorithms have attracted scrutiny from lawmakers and regulators who claim the system is anti-competitive. The practice is at the center of a lawsuit filed in September by the Federal Trade Commission that accuses Amazon of using an “anti-discounting strategy” and a “massive web-crawling apparatus that constantly tracks online prices” to stifle competition.

The company has rejected the FTC’s claims, and said the pricing tool is part of running a good business.

“Just like any store owner who wouldn’t want to promote a bad deal to their customers, we don’t highlight or promote offers that are not competitively priced,” David Zapolsky, Amazon’s general counsel, wrote in a blog post after the lawsuit was filed. Amazon has also said third-party sellers set their own prices.

An Amazon spokesperson declined to comment on the concerns raised by sellers.

The importance of the buy box

Amazon launched Prime Day in 2015 as a way to attract new members to its currently $139-a-year subscription program, while also showcasing its own products, notably its electronic devices, and other services. The promotional event has turned into a big revenue driver for other retailers, which often hold competing sales timed around Prime Day.

Analysts at JPMorgan forecast total revenue for Prime Day, which is set to kick off on Tuesday, will reach $7.9 billion this year, up 11% from 2023, according to a note to clients on Friday.

Target began running discounts across its site on July 7, as part of its Circle Week promotional event. Circle Week is typically held in the lead-up to Amazon’s bargain bonanza.

The problem for Fishman and other sellers resulted from a change in how Target promoted deals for Circle Week. In the past, the company would would show the percentage discount off the regular price to avoid tipping off Amazon’s pricing algorithms, Fishman said.

But this year, instead of listing his item as 25% off, Target showed the item’s actual sale price. That meant it was indexed by Amazon’s pricing algorithms, Fishman said, causing him to lose the buy box.

Winning the buy box is paramount to a seller’s success on Amazon. Without it, shoppers can still find a seller’s product, but they have to take the extra step of clicking into a separate window, where all the offers available are listed. Nearly 98% of sales made on Amazon go through the buy box button, the FTC alleged in its suit.

Mason Arnold’s experience last week was similar to Fishman’s.

Arnold said that after Target launched Circle Week, sales of his Sunwink herbal tonics and powders started plummeting on Amazon because he lost the buy box to resellers.

“The only way to get back the Amazon buy box is to lower our price on Amazon,” Arnold said.

Sunwink did just that, cutting the price of one of its products to $19 from $23. Sales have since started to pick up, but Arnold is doubtful he’ll be able to make a profit at that level. Amazon retail is already a low-margin business due to pricing competition and all the fees for fulfillment, advertising and other services.

“We lowered our prices so we’re currently losing money until it gets fixed,” Arnold said. “We don’t know what the total is going to be, but for us at a minimum it’s hundreds of thousands of dollars” in losses, he said.

Arnold said some resellers buy his products from offline discount retailers and sell them at a markup on Amazon, forcing him to compete selling his own brand.

Fishman said that he and other sellers in his network took their concerns to Target. The company then adjusted the Circle Week discounts on some listings to say, “See price in cart,” meaning shoppers would have to add the product to their cart in order to see the price, Fishman said. The change skirted Amazon’s pricing algorithms, he added.

Target disputed the claim and declined to comment further.

Third-party sellers like Arnold and Fishman are the heartbeat of Amazon’s dominant e-commerce business. Since about 2017, they’ve accounted for at least half of all goods sold on the site. In the first quarter of this year, that number swelled to 61%.

Still, Fishman says the company is quick to penalize sellers, who are just trying to make a living. In so doing, the company is stifling competition, he says.

“Their whole point is we always want to have the lowest price,” Fishman said. “Well, me as a brand, if I want to have a sale on Target for a week, I should be allowed to. I shouldn’t have to be on sale everywhere.”

Berkshire has eliminated 10% of outstanding shares as Buffett values the enduring power of buybacks

PUBLISHED SUN, JUL 21 20247:37 AM EDT

Berkshire Hathaway has reduced a sizable chuck of share count through buybacks in recent years as Warren Buffett views the repurchase program as an effective way to reward long-term shareholders.

Over the past five and a half years (22 quarters), the conglomerate has repurchased nearly $75 billion worth of its common stock, eliminating more than 10% of the company’s total shares outstanding, according to Greggory Warren, Berkshire analyst at Morningstar.

The “Oracle of Omaha” initiated a buyback program in 2011 and relied on repurchases in recent years during a competitive dealmaking environment and an expensive stock market. Buffett believes buybacks are beneficial to shareholders for one simple reason: You don’t need to spend a dime to increase your percentage of shares held.

“Through that simple act, we increase your share of the many controlled and non-controlled businesses Berkshire owns,” Buffett said in his 2021 annual letter. “When the price/value equation is right, this path is the easiest and most certain way for us to increase your wealth.”

The Omaha-based Berkshire will only buy back shares when two conditions are met: 1) Buffett thinks the stock is selling for less than it’s worth; 2) Berkshire will still have ample cash after the proposed buybacks.

The 93-year-old legendary investor believes that it would be “value-destroying” if he overpaid for Berkshire shares.

“If you’re repurchasing shares above a rationally calculated intrinsic value, you are harming your shareholders, just as if you issue shares beneath that figure, you are harming your shareholders,” Buffett once said in 1996.

Hoping for an occasional big opportunity

Berkshire spent $2.6 billion in the first quarter of 2024 to buy back its own common stock on the open market, up from $2.2 billion in the fourth quarter of 2023.

Earlier this year, Buffett said he feels good about his conglomerate’s pace of buybacks right now, but if prices are attractive, he would spend even more.

“Under certain market conditions, we could deploy quite a bit of money in repurchases,” he said at the shareholder meeting. “We will try to reduce shares when it makes sense to do so. We will hope for an occasional big opportunity. And we’re quite satisfied with the position we’re in.”

Shares of the conglomerate are up more than 20% this year after hitting a record closing high this week. The stock has outperformed the S&P 500 in 2024 so far.

UBS estimated that Berkshire’s shares are trading at around a 6% discount to intrinsic value, compared to the 19% average discount since the conglomerate resumed repurchases in 2018. The Wall Street firm projected that Berkshire repurchased almost $2.5 billion worth of stock in the second quarter.

JD Vance is Trump’s VP pick after Rubio and Burgum were passed over for running mate

PUBLISHED MON, JUL 15 202410:51 AM EDTUPDATED TUE, JUL 16 20249:26 AM EDT

Kevin Breuninger@KEVINWILLIAMB

KEY POINTS

- Donald Trump has selected Sen. JD Vance of Ohio as his presidential running mate.

- Vance was later formally selected as Trump’s running mate, during the first day of the Republican National Convention in Milwaukee, Wisconsin.

- Doug Burgum and Marco Rubio have both been told that Trump will not pick them at the RNC, sources told NBC.

Donald Trump has selected Sen. JD Vance of Ohio as his presidential running mate, ending months of speculation about the Republican nominee’s choice to help him challenge President Joe Biden and Vice President Kamala Harris.

“After lengthy deliberation and thought, and considering the tremendous talents of many others, I have decided that the person best suited to assume the position of Vice President of the United States is Senator J.D. Vance of the Great State of Ohio,” Trump said Monday in a Truth Social post.

Vance was formally selected as Trump’s running mate later Monday afternoon, during the first day of the Republican National Convention in Milwaukee, Wisconsin.

Trump was officially picked as the GOP’s presidential nominee earlier in the day.

Trump’s selection provides a sudden, massive jolt in stature for the 39-year-old Vance, who joined the Senate as a political newcomer less than two years ago.

It’s also the culmination of a long-term shift toward Trumpism for Vance, who was once a vocal critic of Trump.

Vance gained fame in 2016 through his bestselling memoir “Hillbilly Elegy,” which traced his rural upbringing in Ohio and mused on the culture and politics of Appalachia.

While not without its critics, the book quickly earned Vance a reputation as a trenchant political analyst who, despite an Ivy League education, possessed a unique sense of how the White working class viewed the rest of the country.

In the private sector, Vance worked for Mithril Capital, the venture-capital firm run by Peter Thiel, and started his own VC firm, Narya, in 2019.

Vance ran in 2022 for the U.S. Senate seat being vacated by retiring Sen. Rob Portman, a Republican. Vance beat former Rep. Tim Ryan, D-Ohio, by a 53%-47% margin, and took office in January 2023.

In an interview with Fox News’ Sean Hannity that aired Monday night, Vance described receiving the call from Trump earlier in the day asking him to be his running mate.

“He just said ‘Look, I think that we got to go save this country. I think you’re the guy who can help me in the best way. You can help me govern. You can help me win. You can help me in some of these midwestern states like Pennsylvania, Michigan, and so forth,’” Vance said Trump told him.

Two other top Republican vice presidential contenders, Sen. Marco Rubio of Florida and North Dakota Gov. Doug Burgum, were told earlier that they would not be picked for the role, NBC News reported.

The Biden campaign promptly panned the selection, accusing Trump of picking Vance because he will “bend over backwards to enable Trump and his extreme MAGA agenda, even if it means breaking the law and no matter the harm to the American people.”

“Billionaires and corporations are literally rooting for J.D. Vance: they know he and Trump will cut their taxes and send prices skyrocketing for everyone else,” read the statement from Biden-Harris campaign chair Jen O’Malley Dillon.

Harris has previously accepted an invitation from CBS News to participate in a vice presidential debate on either July 23 or Aug. 13.

After Trump revealed his selection, Harris left Vance a message congratulating him and welcoming him to the race, a source familiar with the call told NBC.

Shortly after Vance was announced as Trump’s running mate, the senator’s wife, Usha Vance, resigned from Munger, Tolles & Olson, the law firm where she worked as an attorney.

“Usha has informed us she has decided to leave the firm,” according to a statement from the firm shared with CNBC. “Usha has been an excellent lawyer and colleague, and we thank her for her years of work and wish her the best in her future career.”

Before entering politics, Vance had slammed Trump as a “total fraud” and even compared him and his MAGA political movement to a harmful drug.

“Trump’s promises are the needle in America’s collective vein,” Vance wrote in The Atlantic before Trump won the 2016 election.

But as a politician, Vance has morphed into one of the most loyal and extreme backers of both Trump and his brand of nationalist, populist politics.

In his interview with Hannity, Vance said he was not trying to “hide from” his prior criticism of Trump.

“I was certainly skeptical of Donald Trump in 2016,” Vance told Hannity. “But President Trump was a great president, and he changed my mind. I think he changed the minds of a lot of Americans, because again, he delivered that peace and prosperity.”

In recent months, Vance has been quick to display his new pro-Trump stance.

He was among the parade of Republicans who appeared outside of Trump’s criminal hush money trial in New York City to decry the prosecution of the GOP leader.

He later claimed the trial was “election interference,” and that its “main goal” was “psychological torture” against Trump. The jury in that trial convicted Trump on 34 counts of falsifying business records; Trump is currently set to be sentenced on Sept. 18.

After Trump survived a shocking assassination attempt at a campaign rally in Pennsylvania over the weekend, Vance baselessly blamed the Biden campaign for the attack.

“The central premise of the Biden campaign is that President Donald Trump is an authoritarian fascist who must be stopped at all costs,” Vance wrote within hours of the shooting. “That rhetoric led directly to President Trump’s attempted assassination.”

The attack, which left one rally attendee dead and Trump with a minor injury, sent shockwaves across the country and spurred condemnations of violence across the political aisle.

Biden, in an Oval Office address after the Trump rally shooting, urged Americans to lower the temperature of political rhetoric and reaffirm the democratic norms of civil disagreement and decency.

As a senator, Vance has opposed sending U.S. aid to Ukraine as it fights against invading Russian forces, and he has repeatedly voted against legislation that would preserve or expand federal abortion rights.

The Vance announcement added to an already eventful day of Trump-related news.

Earlier Monday morning, federal Judge Aileen Cannon dismissed the criminal case charging the former president with illegally retaining classified documents and obstructing the government’s efforts to retrieve them.

— CNBC’s Josephine Rozzelle contributed reporting.

JPMorgan’s Jamie Dimon warns inflation and interest rates may stay higher

PUBLISHED FRI, JUL 12 20247:49 AM EDTUPDATED FRI, JUL 12 202410:47 AM EDT

JPMorgan Chase CEO Jamie Dimon on Friday issued another warning about inflation despite recent signs of easing in price pressures.

“There has been some progress bringing inflation down, but there are still multiple inflationary forces in front of us: large fiscal deficits, infrastructure needs, restructuring of trade and remilitarization of the world,” Dimon said in a statement along with the bank’s second-quarter results. “Therefore, inflation and interest rates may stay higher than the market expects.”

His comments came after this week’s data showed the monthly inflation rate dipped in June for the first time in more than four years, which fueled bets that the Federal Reserve could cut rates soon.

The consumer price index, a broad measure of the costs for goods and services across the U.S. economy, declined 0.1% in June from May, putting the 12-month rate at 3%, around its lowest level in more than three years.

Fed Chairman Jerome Powell earlier this week expressed concern that holding interest rates too high for too long could jeopardize economic growth, teasing that rate reductions could be on the horizon as long as inflation continues to show progress.

Dimon joined many economists in sounding the alarm on burgeoning U.S. debt and deficits. The federal government has so far spent $855 billion more than it has collected in the 2024 fiscal year. For fiscal 2023, the government’s deficit spending came in at $1.7 trillion.

Powell indicates Fed won’t wait until inflation is down to 2% before cutting rates

PUBLISHED MON, JUL 15 20241:03 PM EDTUPDATED MON, JUL 15 20242:32 PM EDT

Jesse Pound@/IN/JESSE-POUND@JESSERPOUND

KEY POINTS

- Powell referenced the idea that central bank policy works with “long and variable lags” to explain why the Fed wouldn’t wait for its target to be hit.

- The central bank is looking for “greater confidence” that inflation will return to the 2% level, Powell said.

- The Fed’s next policy meeting is at the end of July.

Fed Chair Powell: The central bank will not wait until inflation hits 2% to cut interest rates

Federal Reserve Chair Jerome Powell said Monday that the central bank will not wait until inflation hits 2% to cut interest rates.

Speaking at the Economic Club of Washington D.C., Powell referenced the idea that central bank policy works with “long and variable lags” to explain why the Fed wouldn’t wait for its target to be hit.

“The implication of that is that if you wait until inflation gets all the way down to 2%, you’ve probably waited too long, because the tightening that you’re doing, or the level of tightness that you have, is still having effects which will probably drive inflation below 2%,” Powell said.

Instead, the Fed is looking for “greater confidence” that inflation will return to the 2% level, Powell said.

“What increases that confidence in that is more good inflation data, and lately here we have been getting some of that,” he said.

Powell also said he thinks a “hard landing” for the U.S. economy was not “a likely scenario.”

Monday was Powell’s first public speaking appearance since the consumer price index report for June showed cooling inflation, with prices actually falling month over month.

Powell said at the beginning of his appearance that he was not intending to make any signals about when the Fed might start to cut interest rates. The central bank’s next policy meeting is at the end of July.

Powell made the remarks as part of a discussion with David Rubenstein, chairman of the Economic Club of Washington, D.C., and co-founder of The Carlyle Group, where the Fed chair previously worked.

The target range for the federal funds rate is currently 5.25% to 5.50%. That is up from a range of 0% to 0.25% during the Covid-19 pandemic, and a range of 1.50%-1.75% before that health crisis.

The federal funds rate influences, directly or indirectly, the cost of money throughout the economy, such as mortgage rates.

“People I don’t know will always say, ‘hey, cut rates.’ Somebody said that in the elevator this morning,” Powell said jokingly.

‘Ludicrous’: Donors leave call with Kamala Harris frustrated and annoyed

PUBLISHED SUN, JUL 21 20243:56 AM EDT

A call Friday featuring Vice President Kamala Harris and about 300 major Democratic donors left many who dialed in frustrated, with one donor declaring it “ludicrous” shortly before it ended, according to two sources familiar with the call.

One person on the call referred to it as “mismanaged” and “rushed.” They added expectations had not been managed well and some participants left feeling admonished.

That person and two other sources said many donors joined hoping to get an insider’s view of how to move forward in the wake of President Joe Biden’s dismal debate performance and the growing number of Democrats calling for him to drop out of the race. Instead, they said donors left the call feeling disappointed and like they had not gained any new insights or helpful information.

“It was a total failure,” said one source who was on the call and who spoke on the condition of anonymity to provide a candid assessment. “It was damaging. It was poor planning.”

The call had been organized by Jen O’Malley Dillon, the chair of Biden’s campaign, and not by the campaign’s finance team, according to a source familiar with the planning. One of the sources who was on the call said that the donors who participated represented a wide range of views — some diehard Biden fans, some unconvinced about his path forward and many views in between.

At the end of the call, hundreds of participants were unmuted, and one person declared that the call was “ludicrous,” according to two of the sources.

One source stressed that they took the comment to mean that the call was poorly run and not as a criticism of Harris.

During the call, Harris, who was asked to join the call by Biden’s senior advisors, praised Biden, according to campaign officials.

“We know which candidate in this election puts the American people first: Our President, Joe Biden,” she said according to the campaign officials. “With every decision he makes in the Oval Office, he thinks about how it will impact working Americans. And I witness it every day.”

Harris also spoke positively about Democrats’ chances of beating former President Donald Trump. “Something I believe in my heart of hearts,” Harris said according to campaign officials. “It is something I feel strongly you should all hear and should take with you when you leave. And tell your friends too. We are going to win this election. We are going to win.”

NBC News reached out to the Biden campaign for comment.

Biden’s family begins discussing his potential exit from the 2024 race

The fallout from the call comes as donations to the Biden-Harris campaign and Democratic groups have plummeted and as Harris has been deployed several times to speak with donors as questions swirl over Biden’s future on the ticket.

The call with donors started with presentations from field organizers who expressed anger at the ongoing debate within the Democratic party about backing President Biden, given what they’ve seen and heard from voters on the ground, according to one source with direct knowledge of the discussion.

One source said before Harris joined there seemed to be an effort to stall, which they said is normal for events with high ranking officials. But what angered many donors, this source said, was that during the wait — which was about 20 minutes — donors were “admonished.” Participants of the call were told they needed to “lock in and get behind” Biden and to not pursue efforts to push out the president.

“Please help us turn down the volume on this conversation publicly,” Melissa Morales, founder and president of Somos Votantes, said on the call, according to a transcript obtained by NBC News. “It’s time to stop the leaks and the rampant rumors. Your message has been heard and received. But every day that we continue this publicly chaotic conversation, we come closer to a loss — no matter who the nominee is.”

That didn’t sit well with some on the call.

“These are donors who are not used to getting admonished and told what to do,” the source said.

Another source who was on the call and is supportive of Harris being the Democratic nominee pushed back on the donor’s feelings of frustrations.

The person said while many donors thought they were going to get insightful and confidential information, they immediately went to the media and proved why they shouldn’t get it.

Meanwhile, on Saturday, Harris spoke at a campaign fundraiser in Provincetown, Mass. and praised Biden as one the most consequential presidents in history.

Harris garnered applause at various parts of her speech talking about her and Biden’s record including advocating for the rights of the LGBTQ community.

But, the loudest applause from the crowd came when someone in the crowd of 1,000 people shouted “Go get him Kamala,” as Harris criticized Trump.

The applause lasted for several seconds as Harris smiled and looked out onto the cheering crowd of some one thousand people.

Biden campaign says there’s no alternative plan for new nominee

After Harris left the stage, Lennie Alickman, 63, said she wanted to see Biden step aside.

“She is on a tightrope. She has to be very careful not to alienate Biden,” Alickman said when asked about Harris praising Biden throughout the speech. “I actually would like to see Kamala at the top of the ticket. She could carry out and continue the policies of the Biden administration. I love Biden but I’m not sure he is up to the job. And, I’m worried he is going to lose against Trump.”

John Newton, 75, who attended the fundraiser, also said he believes Biden needs to drop out of the race and wants to see Harris become the party’s nominee.

“I love Joe,” Newton said. “In a business context, it’s like your 81 year old salesman that’s goofed up at the convention and not making his numbers. And, you gotta go in and tell him, ‘Judy is replacing you.’ It’s no fun. But sadly that has to happen.”

Harris closed her speech at the event which was said to have raised $2 million by talking about her campaign manager when she ran for district attorney in San Francisco.

She said he told her, “You must recognize what you’re up against — and know that those who oppose progress will always try to suggest that a movement for freedom is somehow subversive and that it undermines who we are as a nation or our traditions. But what we know is that it strengthens who we are as a nation when we fight to expand rights.”

HI Financial Services Mid-Week 06-24-2014