HI Market View Commentary 07-13-2021

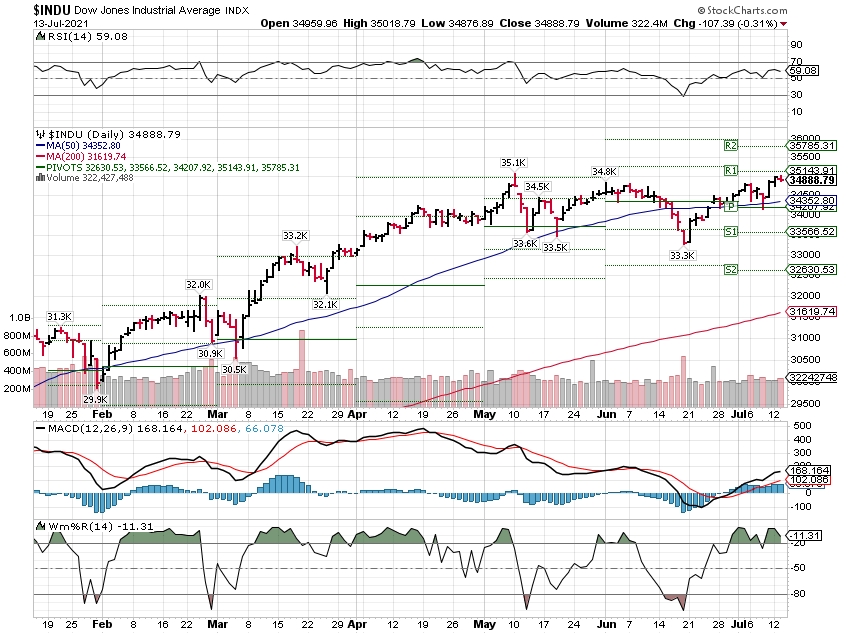

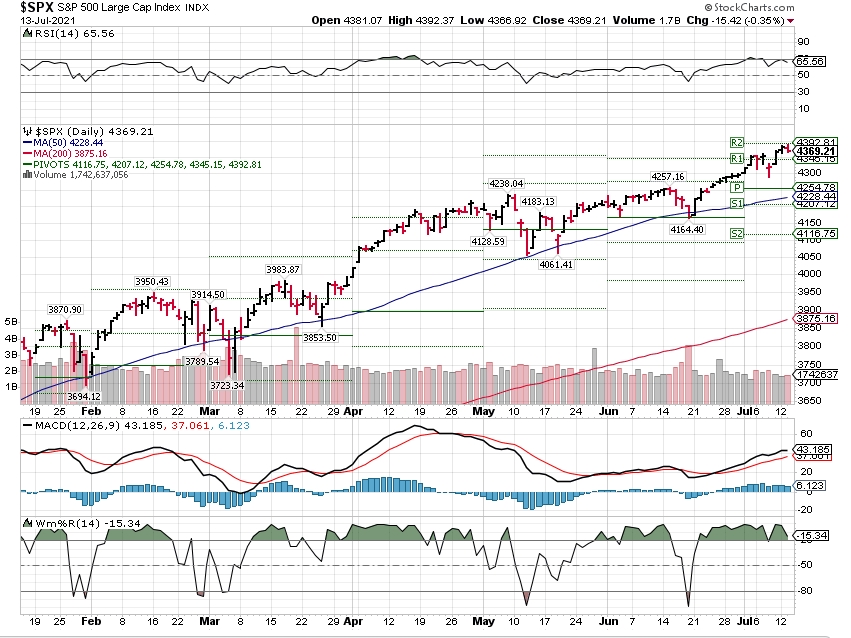

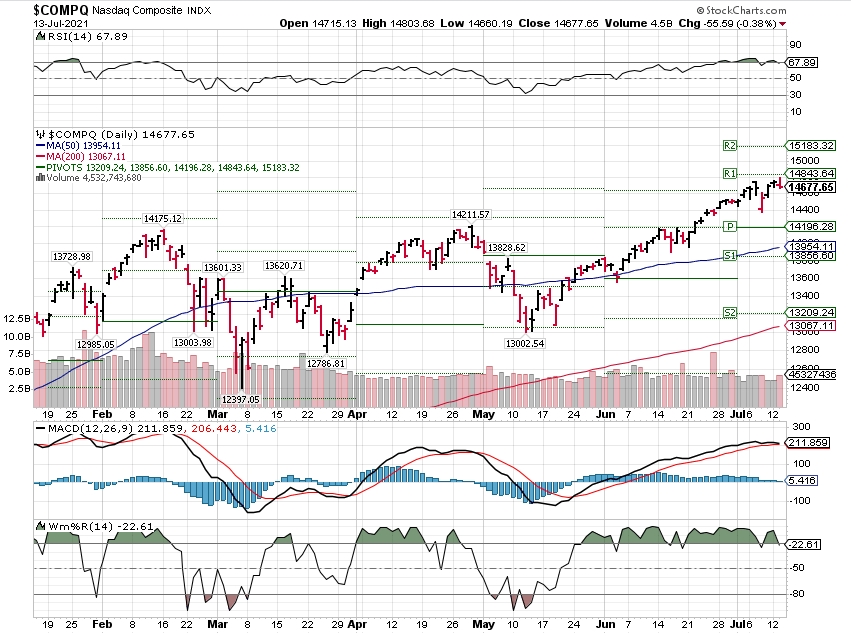

https://www.investopedia.com/terms/p/pivotpoint.asp

What Is a Pivot Point?

A pivot point is a technical analysis indicator, or calculations, used to determine the overall trend of the market over different time frames. The pivot point itself is simply the average of the intraday high and low, and the closing price from the previous trading day. On the subsequent day, trading above the pivot point is thought to indicate ongoing bullish sentiment, while trading below the pivot point indicates bearish sentiment.

The pivot point is the basis for the indicator, but it also includes other support and resistance levels that are projected based on the pivot point calculation. All these levels help traders see where the price could experience support or resistance. Similarly, if the price moves through these levels it lets the trader know the price is trending in that direction.

- A pivot point is an intraday technical indicator used to identify trends and reversals mainly in equities, commodities, and forex markets.

- Pivot points are calculated to determine levels in which the sentiment of the market could change from bullish to bearish, and vice-versa.

- Day traders calculate pivot points to determine levels of entry, stops, and profit-taking.

Pivot Points vs. Fibonacci Retracements

Pivot points and Fibonacci retracements or extensions both draw horizontal lines to mark potential support and resistance areas. The Fibonacci indicator is useful because it can be drawn between any two significant price points, such as a high and a low. It will then create the levels between those two points.

Fibonacci retracement and extension levels can thus be created by connecting any price points on a chart. Once the levels are chosen, lines are drawn at percentages of the price range selected.

Pivot points, in contrast, do not use percentages and are based on set fixed numbers: the high, low, and close of the prior day.

Limitations of Pivot Points

Pivot points are based on a simple calculation, and while they work for some traders, others may not find them useful. There is no assurance the price will stop at, reverse at, or even reach the levels created on the chart.

Other times the price will move back and forth through a level. As with all indicators, it should only be used as part of a complete trading plan.

https://www.investopedia.com/terms/w/williamsr.asp

What is Williams %R?

Williams %R, also known as the Williams Percent Range, is a type of momentum indicator that moves between 0 and -100 and measures overbought and oversold levels. The Williams %R may be used to find entry and exit points in the market. The indicator is very similar to the Stochastic oscillator and is used in the same way. It was developed by Larry Williams and it compares a stock’s closing price to the high-low range over a specific period, typically 14 days or periods.1

KEY TAKEAWAYS

- Williams %R moves between zero and -100.

- A reading above -20 is overbought.

- A reading below -80 is oversold.

- An overbought or oversold reading doesn’t mean the price will reverse. Overbought simply means the price is near the highs of its recent range, and oversold means the price is in the lower end of its recent range.

- Can be used to generate trade signals when the price and the indicator move out of overbought or oversold territory.

What Does Williams %R Tell You?

The indicator is telling a trader where the current price is relative to the highest high over the last 14 periods (or whatever number of lookback periods is chosen).

When the indicator is between -20 and zero the price is overbought, or near the high of its recent price range. When the indicator is between -80 and -100 the price is oversold, or far from the high of its recent range.

During an uptrend, traders can watch for the indicator to move below -80. When the price starts moving up, and the indicator moves back above -80, it could signal that the uptrend in price is starting again.

The same concept could be used to find short trades in a downtrend. When the indicator is above -20, watch for the price to start falling along with the Williams %R moving back below -20 to signal a potential continuation of the downtrend.

Traders can also watch for momentum failures. During a strong uptrend, the price will often reach -20 or above. If the indicator falls, and then can’t get back above -20 before falling again, that signals that the upward price momentum is in trouble and a bigger price decline could follow.

The same concept applies to a downtrend. Readings of -80 or lower are often reached. When the indicator can no longer reach those low levels before moving higher it could indicate the price is going to head higher.

The Difference Between Williams %R and the Fast Stochastic Oscillator

The Williams %R represents a market’s closing level versus the highest high for the lookback period. Conversely, the Fast Stochastic Oscillator, which moves between 0 and 100, illustrates a market’s close in relation to the lowest low. The Williams %R corrects for this by multiplying by -100. The Williams %R and the Fast Stochastic Oscillator end up being almost the exact same indicator. The only difference between the two is how the indicators are scaled.

Limitations of Using the Williams %R

Overbought and oversold readings on the indicator don’t mean a reversal will occur. Overbought readings actually help confirm an uptrend, since a strong uptrend should regularly see prices that are pushing to or past prior highs (what the indicator is calculating).

The indicator can also be too responsive, meaning it gives many false signals. For example, the indicator may be in oversold territory and starts to move higher, but the price fails to do so. This is because the indicator is only looking at the last 14 periods. As periods go by, the current price relative to the highs and lows in the lookback period changes, even if the price hasn’t really moved.

Highlights

- Consumer credit increased by $35.3 bln in May (Briefing.com consensus $19.0B) after increasing an upwardly revised $20.0 bln (from $18.6 bln) in April.

Key Factors

- Nonrevolving credit, which includes auto loans, increased by $26.1 billion in May to $3.305 trillion. Revolving credit increased by $9.2 billion to $974.6 billion.

- Consumer credit increased at a seasonally adjusted annual rate of 10.0% in May.

- Revolving credit increased at an annual rate of 11.4% while nonrevolving credit increased at an annual rate of 9.5%.

Big Picture

- The key takeaway from the report is that the expansion in consumer credit in May was the largest since December 2010.

| Category | MAY | APR | MAR | FEB | JAN |

| Total Credit | $35.3B | $20.0B | $19.3B | $20.3B | -$1.7B |

| Revolving | $9.2B | -$1.0B | $1.4B | $3.5B | -$13.1B |

| Nonrevolving | $26.1B | $21.0B | $17.9B | $16.8B | $11.4B |

https://go.ycharts.com/weekly-pulse

| Market Recap WEEK OF JUL. 5 THROUGH JUL. 9, 2021 The S&P 500 index managed to climb 0.4% last week to a fresh closing high at the conclusion of a short but turbulent week for US stocks. The market benchmark ended Friday’s session at 4,369.55, up from last Friday’s closing level of 4,352.34, which had also been a record closing high at the time. It reached a new intraday high Friday at 4,371.60. The week began quietly, with the US stock market closed Monday following the Independence Day holiday, but was marked by sharp moves later in the week. It reached a then-new closing high on Wednesday at 4,358.13 but tumbled Thursday after the Labor Department’s report of weekly jobless claims showed a surprise increase that sparked concerns about the strength of the US economic recovery. However, investors came in Friday to “buy the dip” and ultimately sent the index up to more fresh records. The activity came at a time of market suspense ahead of Q2 earnings reports, which will begin kicking off next week with reports from heavyweights including JPMorgan Chase (JPM), Goldman Sachs (GS) and Alcoa (AA). The real estate sector had the largest percentage gain of the week, up 2.6%, followed by a 1.4% rise in consumer discretionary. Other gainers included utilities, technology, health care and consumer staples. On the downside, the energy sector had the sharpest percentage drop of the week, down 3.4%, followed by a 0.6% slip in financials and a 0.4% decline in communication services. The real estate sector’s gainers included residential real estate investment trusts Mid-America Apartment Communities (MAA), Essex Property Trust (ESS) and AvalonBay Communities (AVB), up 5.7%, 4.7% and 4.5%, respectively, as the stocks were among six residential REITs that received price target boosts from RBC Capital Markets. In raising its price targets on the stocks, RBC cited lower capitalization rates and higher estimates for core funds from operations. The energy sector’s tumble came as crude oil futures fell on the week amid worries that COVID-19 Delta variant could crimp demand while investors were also concerned that a collapse of OPEC+ negotiations could spur another fight for market share. The energy sector’s decliners included Diamondback Energy (FANG), whose shares fell 8.8% on the week even as Wells Fargo raised its price target on the stock to $101 from $90. In the financial sector, shares of Lincoln Financial Group (LNC) shed 3.5% on the week as Piper Sandler and Autonomous Research cut their price targets on the shares of the provider of retirement, insurance and wealth protection services. The company began exchange offers and consent solicitations for outstanding capital securities. Next week’s Q2 earnings calendar will feature reports from JPMorgan Chase and Goldman Sachs on Tuesday, Bank of America (BAC) and Delta Air Lines (DAL) on Wednesday, and Morgan Stanley (MS) and Alcoa (AA) on Thursday, among others. On the economic calendar, the market will be looking at inflation data with the June consumer price index due Tuesday and the June producer price index due Wednesday. Weekly jobless claims on Thursday will also be in focus, especially after last week’s negative surprise, while June retail sales and July consumer sentiment will come Friday. Provided by MT Newswires |

Earnings Dates

AAPL – 07/27 AMC

BA – 07/28 est

BABA – 08/19 est

BAC – 07/14 BMO

BIDU – 08/12 est

COST – 09/23 AMC

DIS – 08/12 AMC

F – 07/28 AMC

FB – 07/28 AMC

FSLR – 07/29 est

GE – 07/27 BMO

GM – 08/04 AMC

JPM – 07/13 BMO

MU – 06/30 AMC

TGT – 08/19 BMO

UAA – 08/03 BMO

V- 07/27 est

Where will our markets end this week?

Higher

DJIA – Bullish

SPX – Bullish

COMP – Bullish

Where Will the SPX end July 2021?

07-13-2021 3.0%

07-06-2021 3.0%

06-28-2021 3.0%

Earnings:

Mon:

Tues: FAST, GS, PEP, JPM

Wed: C, BLK, DAL, WFC, BAC

Thur: SCHW, MS, USB, UNH, AA

Fri: ALV, FHN

Econ Reports:

Mon:

Tues: CPI, Core CPI, Treasury Budget

Wed: MBA, PPI, Core PPI, Fed Beige Book,

Thur: Initial Claims, Continuing Claims, Empire Manufacturing, Import, Export, Phil Fed, Capacity Utilization, Industrial Production,

Fri: Retail Sales, Retail ex-auto, Business Inventories, Michigan Sentiment

Int’l:

Mon –

Tues –

Wed –

Thursday –

Friday-

Sunday –

How am I looking to trade?

Added protection for earnings

www.myhurleyinvestment.com = Blogsite

customerservice@hurleyinvestments.com = Email

Questions???

Disney attracts bullish view from Morgan Stanley on long-term streaming, parks potential

Jul. 13, 2021 7:41 AM ETThe Walt Disney Company (DIS)By: Clark Schultz, SA News Editor8 Comments

- Morgan Stanley reiterates an Overweight rating on Disney (NYSE:DIS) after seeing shares lag the market.

- Analyst Benjamin Swinburne: “While near-term (FH21) consensus Disney Plus net adds appear optimistic, we remain confident in the ’24 streaming guidance and raise FY22 EPS estimates on rapidly reopening Parks.”

- The firm’s bullish thesis on Disney is based on the company building content assets that enable it to take advantage of the significant direct-to-consumer streaming opportunity ahead. Disney’s underlying IP is called best-in-class to support long-term content monetization opportunities. Historical cycles are also said to suggest a potential return to U.S. Parks revenue in FY23 above the prior peaks.

- Shares of Disney are up 0.13% premarket.

- Yesterday, Disney turned some heads with a plan to hike prices on ESPN Plus by about 17%.

- Now read: Disney raising price of ESPN Plus to $6.99/month

Bank stocks drop even as JPMorgan, Goldman earnings beat estimates

Jul. 13, 2021 10:19 AM ETC, GS…By: Liz Kiesche, SA News Editor24 Comments

- Even though JPMorgan Chase (JPM -1.7%) and Goldman Sachs (GS -1.8%) post earnings that exceed consensus estimates, bank stocks drop as the 10-year Treasury yield heads south.

- 10Y UST yield dips almost 2 basis points to 1.35%.

- SPDR S&P Bank ETF (NYSEARCA:KBE) falls 1.8% and SPDR S&P Regional Bank ETF (NYSEARCA:KRE) drops 1.8%.

- Citigroup (C -1.3%), which reports Q2 on Wednesday, and Morgan Stanley (MS -0.6%), which reports on Thursday, are among the universal banks with the smallest declines.

- Bank of America (BAC -2.0%), Wells Fargo (WFC -1.8%) and Goldman fall the most of the universal banks.

- For the two banks that reported this morning, strong investment banking results, especially in dealmaking, helped offset the decline in trading revenue.

- Wolfe Research analyst Steven Chubak saw a few negatives in the JPMorgan report. He sees the increase in FY2021 expense guidance (to $71B from $70B) and the lower excess capital under its supplementary leverage ratio likely weighing on JPM’s shares today.

- Positives in the JPM report include average loans rising 1% Q/Q, average deposits up 4% Q/Q, Corporate & Investment Bank fees up 25% Y/Y and core EPS/ROTCE ex-reserve release “still very strong,” Chubak notes.

- Jefferies analyst Ken Usdin points out that JPM’s guidance for card net charge-offs of less than 2.5% vs. previous guidance of ~2.5% is “well below LT expectations in the 3%+ area.”

- Goldman’s results included better investment banking results, continued efficiency gains, strong deposit growth, and “strong TBVPS growth,” Chubak notes. He expects stock reaction to be muted due to its already strong YTD performance.

- Goldman’s beat was powered by excess equity investment gains and investment banking revenue beating across all three segments, and closes the quarter “with another record backlog,” said Jefferies analyst Daniel Fannon.

- Expenses in Q2 of $8.6B were higher than the $7.5B consensus, reflecting higher revenue, he added.

- Earlier, JPMorgan Q2 earnings reflect weaker fixed income results and Goldman Q2 earnings beat powered by investment banking strength.

Tencent-Sogou deal cleared by top Chinese regulator

Jul. 13, 2021 6:59 AM ETBIDU, SOGO…By: Carl Surran, SA News Editor10 Comments

- Tencent’s (OTCPK:TCEHY) plan to privatize the Sogou (NYSE:SOGO) search engine developer is approved by China’s anti-monopoly regulator, sending shares up as much as 4.3% in Hong Kong.

- Tencent, which owns 39% of the Baidu (NASDAQ:BIDU) rival and controls more than half of its voting rights, proposed buying out other investors for ~$2.1B last July.

- Shares of Chinese firms listed in the U.S. are higher on the news, including BABA +2.5%, PDD +2.2%, JD +1.8%, DIDI +1.6%.

- The WSJ reported the news earlier and Reuters reported that the Sogou deal was likely to be approved earlier this month.

- Just days ago, the regulator ordered Tencent to halt the merger of game-streaming platforms Huya and Douyu, saying the combination would hurt competition.

Disney gains 1% as J.P. Morgan calls it top media pick, seeing recovery in theaters, parks

Jul. 12, 2021 10:46 AM ETThe Walt Disney Company (DIS)By: Jason Aycock, SA News Editor1 Comment

- Walt Disney’s (DIS +1.3%) fiscal third quarter has closed, and J.P. Morgan has reiterated its Overweight rating with updated thoughts heading into next month’s earnings report.

- The studio is still emphasizing theatrical exhibition even with the online premium success of Black Widow, analyst Alexia Quadrani notes – and so she’s expecting a “more substantial” improvement in theatrical revenues in the fourth quarter and into 2022, with the return of exclusive theatrical windows.

- Meanwhile, Disney Plus subscriber growth should slow down on a sequential basis, the firm says, estimating 110M subscribers in the quarter – with incremental growth skewed to Hotstar, with Malaysia and Thailand launched during the quarter. The next quarter should bring better subscriber growth as Star Plus launches in Latin America Aug. 31, it says.

- Over in the Parks business, a recovery is “more firmly” taking hold, and the firm expects domestic capacity is likely to hit normalized levels in the fiscal fourth quarter (the current quarter).

- “Customers’ intent to visit has returned to 2019 levels at Walt Disney World; Disneyland Paris reopened on June 17, and all of Disney’s parks were open by the end of FQ3 for the first time following their closure from COVID-19,” Quadrani and team write.

- “With its continued digital transformation and recovery at the legacy business, Disney remains our top pick in media in 2021, and we view current levels as a particularly favorable entry point for the long-term investor,” they say.

- J.P. Morgan is reiterating its $220 December 2021 price target, implying 23% further upside.

Disney’s Successful Superhero Streaming Experiment Raises Surprising New Possibilities

Jul. 12, 2021 7:00 AM ETThe Walt Disney Company (DIS)T11 Comments6 Likes

Summary

- After a long delay, Disney released Marvel’s Black Widow and earned $80 million domestically, but in a shocking twist, it was revealed the movie made another $60 million via streaming.

- Disney initially resisted utilizing a hybrid release for the film, but after COVID spiked internationally, the company changed its plans to add a layer of financial protection.

- Some have argued that releasing movies day-and-date via streaming and theatrically in effect leaves “money on the table,” but that argument doesn’t hold water as we saw (again) this weekend.

- What has become clearer is that while we initially saw the streaming and traditional options as rival methods that couldn’t co-exist, they actually can, which sets up multiple new possibilities.

- Studios can use streaming to add an extra layer of profitability by catering to those who prefer at-home viewing and to protect other movies they may be worried could flop.

Back in the ’90s when soap operas were more of a “thing,” fans looked for “red-letter days.” These were the dates when key storyline events were going to happen on the daytime staples – in other words “can’t miss moments.”

For investors in Disney (NYSE:DIS) and any type of film studio/streamer, July 9th was the equivalent of a red-letter day.

And not just any red-letter day – arguably the biggest one at the box office so far since we came out of lockdown.

After a long delay, Disney finally released Black Widow, effectively kicking off “Phase 4” of the Marvel Cinematic Universe. Starring fan favorite Scarlett Johansson, this superhero origin story has long been one of the most anticipated projects in Hollywood.

However, COVID-centric delays have ratcheted up that anticipation tenfold for investors because the movie has taken on new levels of importance and may be a defining moment in the future of film distribution.

Am I being over-dramatic?

Maybe a little, but the stakes here were definitely higher than with past recent new releases and Disney ended the weekend by throwing out a curveball nobody in the industry saw coming.

First as always though, some background.

As I mentioned in the past, with the onset of COVID, many studios pivoted their release strategies. Some shelved their films until further notice, some proceeded as planned just over paid streaming/on demand and others switched to a free hybrid model.

Disney chose a fourth method.

Hybrid premium.

While ATT/Warner Bros. (NYSE:T) did day-and-date releases with HBO Max as part of the price of the subscription, Disney opted to add a $30 surcharge for the ability to watch new releases from home. Dubbed Disney+ Premier, it was a special tag only that until now was only doled out three times (Mulan, Raya and the Last Dragon, Cruella).

In all other cases, Disney opted to just move some of their movies to Disney+ as streaming exclusives that were available at no extra cost.

The difference was the movies that headed to Disney+ for free were movies Disney could make a return based on other factors (i.e. subscription drivers, awards, word of mouth, etc.) or they were moved out of fear they may underperform and this provided them cover.

And then there were the exceptions.

With Mulan, the movie cost them a ton of money to produce and executives needed to hedge their bets, while Raya sported a more unknown voice cast and storyline that on its own wasn’t likely going to be a traditional driver. In both cases though delaying further wasn’t an option.

I’ll get to Cruella in a minute.

The point is that with restrictions lifting and vaccines working, it looked like Disney+ Premier was going to go head into the legendary Disney vault, but while COVID was becoming more manageable Stateside, internationally it was (and is) still a huge problem.

To play it safe, Disney opted to re-arrange its plans – it pushed Black Widow to July and moved Cruella up to May, while adding Disney+ Premier options to both. Shortly after it also did the same thing with Jungle Cruise, for largely the same reasons.

In each case these movies are more than one-offs features, they are part of larger franchises and initiatives where their success or failures cause a domino effect – and Disney doesn’t play around with dominos. It wants to make they fall in the direction they want at the precise time they want – nothing is left to chance.

However, all of this led to more questions.

For example, if nothing is left to chance, then was nothing also left on the table as well by using this approach? In other words, did creating a streaming option (paid or free) siphon off box office revenue to the point it would impact Disney’s financial bottom line and be noticeable to investors?

It’s a loaded question because the common practice had been NOT to reveal the revenue or any solid metrics that came from a streaming film – at least that WAS the case, but I’m skipping ahead.

All of that said though nothing stopped the industry from speculating and that’s what made theaters especially nervous.

For example, Cruella earned around $27 million domestically, which despite what many think, in COVID-world was solid (but not spectacular). However, factoring in what we know from third-party data, the movie then looks to have earned another $20 million from the streaming upcharge option – combined that puts the movie closer to what you would have expected pre-COVID for an opening weekend.

The difference is that $20 million was all Disney’s to keep – there was no split with theaters.

The decision to take some of the exclusivity away from theaters has always been controversial and resentment begin to grow among a select group of traditionalists. That group is where those “money left on the table arguments” come from.

Well, them and people who (understandably) were upset they are being cut out of the profits. This narrative was started in order to rail against it and it has worked to the effect that it comes up every time one of these hybrid movies open.

That said, others look at it from the perspective of this is Disney and it can do what it wants. That includes opting to go fully streaming and cutting theaters out completely. Yet many investors likely remember the House of Mouse pre-pandemic had been a supporter of the traditional model so the studio wanted to give theaters the ability to exhibit the movie.

And audiences took advantage – on Friday the film’s total was at around $40 million, (counting an impressive $13 million from Thursday night “preview” screenings), with a weekend total of around $80 million.

Not counting Avengers movies which are a league of their own, that total is in shooting distance of pre-pandemic numbers. The last Spider-Man film did $92 million and prior to that Ant-Man’s sequel hit $75 million during their first frames. (As an aside, you can’t really count Black Panther as traditional because like Avengers, that was a special case driven by a number of outside factors.)

Simply put, a $80+ million opening for the first entry in a Marvel series is not that far out of line with tradition and a big sign the box office’s demise was greatly exaggerated. In fact, it was also reported that compared to the same window in 2019, the overall box office was about the same.

But then Disney+ Premier comes into play.

And a new question comes up.

How much did the stream-at-home option take away from the box office?

Personally, I think that’s the wrong question, at least for investors in a company like Disney. The better question is does it matter?

(Credit: Disney)

Some have quipped the Premier option is why Widow fell short of a $100 million opening in theaters and again since traditionally studios never revealed any meaningful data it was an argument that would get a lot of oxygen.

Except this time Disney decided to weigh in and in a bombshell move revealed Black Widow earned an additional $60 million through Disney+ Premier and combined globally the total stands around $219 million.

So yes, while Disney can’t claim its movie earned $100 million in theaters, do you think they really care so long given in actuality it made $140 million combined in the States alone? Plus remember that extra revenue is NOT being split with theaters so it’s going straight back into the company and its bottom line.

As I’ve said before that “left on the table” argument really doesn’t hold water.

Yes, this is the first time we can clearly see a drop in revenue from one day to the next corresponding to a streaming option. At one point Widow was expected to clear $90 million, with a shot at $100 million, but ultimately settled around $80 million – but the amount of money spent didn’t change just the way it was spent.

And that has opened the door for a new version of the same “money on the table” arguments to come up – this time pegged to how it is impacting theaters and how Disney just opened Pandora’s Box.

I’m sympathetic to theaters, I love the shared experience of watching a movie in a crowded setting on opening weekend and I know I’m not alone. Although I also know Hollywood is and has always been a business and Disney just showed how those who operate in this business can stand to make a lot more money for themselves and their investors.

Remember, theaters making it cost so much for tickets and concessions is what drove the traditional model to the brink in the first place, but lost in the conversation is the theaters didn’t exactly get iced out here either.

Earlier I mentioned red-letter days and while July 9th was the biggest date, it is not the only one. June 25th was one and August 6th is the other. The 25th marked the debut of Universal’s (NASDAQ:CMCSA) Fast & Furious 9 while the 6th is when Warner Bros. unleashes its new-look Suicide Squad with Guardians of the Galaxy’s James Gunn at the helm.

There are a few in between to keep an eye on, but the reason these specific dates are so important is because in addition to being the top three “it” films of the summer – each carries a different distribution method.

Fast 9 was only theaters, Suicide Squad will be a free hybrid and Black Widow is a premium hybrid.

They are basically a built-in barometer around audience’s willingness to go back to the theater – so what did we learn?

Fast 9 scored $70 million and Black Widow is pulled in $80 million.

Interesting right?

Even with a streaming option at there for Widow it still outperformed F9.

And keep in mind these are three-day non-holiday weekend totals and all three of these films cater to the same audience. They also all have the same style and are the same tentpole level of release we’d expect during the summer.

It is too early to make projections around what Suicide Squad will do, but you can bet when those come in it will spark a fascinating conversation. Remember the (poorly received version) set a ton of August records with a $135 million opening in 2016 and this version has been unquestionably better received off initial footage.

So can it match that total?

It’s doubtful, but given COVID it wasn’t ever really presumed to be an option either. Granted based on this weekend’s information that target range is going to be all over the place.

Again, the better question is how much of an impact will the free HBO Max option have? And what impact will it have going forward?

That’s an answer we’ll have to wait and see – but where investors’ focus towards the industry should be for the moment is the realization there is a universe where studios can double-dip with audiences and earn more money.

With Disney, you really could also take it a step further and instead of wondering if the company left money on the table, ask if by NOT doing this going forward, is Disney leaving money on the table?

Again, it’s a loaded question because there are so many things at play. Not the least of which is Disney understands the value of the traditional model and the shared theatrical experience.

To me though it speaks to a larger point in which all this time we saw the streaming and traditional options as rival methods that could never co-exist – but now we’ve seen they can. It may not always be to the same level but it leaves room for both models to profit.

Disney, for its part, has signaled that Jungle Cruise will be its last Disney+ Premier title for the immediate future and that starting in September with the NEXT Marvel film they will be going back mostly to the theatrical model, albeit likely with a smaller exclusivity window.

Although that was PRIOR to this weekend and the massive streaming take Black Widow pulled in via Disney+ Premier.

This weekend aside, other studios had made similar comments about a return to the traditional model, such as Warner Bros.. Yet as it did for Disney, the streaming option has helped them with their streaming platform HBO Max. As a result, what we will likely see across the board is a re-distribution of films based on where studios think they will be most successful.

In The Heights is a great example, the movie flopped in theaters, but had it been streaming only, the perception would have changed. You would have just seen the sparkling reviews and outside of unreliable third-party data, there would have been no real signs the movie missed the mark with audiences.

For a movie like Heights that is clearly going to make an awards play, that box office black eye is going to come back and haunt it later on. It’s also why creatives like Adam Sandler jumped to Netflix (NASDAQ:NFLX) – no blowback from low totals.

The pandemic changed everything – literally everything.

With entertainment, especially movies it may have been for the better as what we are seeing is the collapse of the “window” system which was archaically outdated – but profitable to a lot of people so they fought to keep it in place.

As a reminder the concept was built around the 90 day window where theaters had exclusivity over the films, but now in many cases that has shrunk to 40 to 45 days and in some cases it’s non-existent.

Some of these changes were happening pre-COVID, but were sped up in a big way as a result of the pandemic and those learnings will continue into 2022 and beyond.

For now, it is tricky because in streaming there are usually no hard and fast metrics – either the unbelievable (i.e. Netflix’s two-minute viewing numbers) or the non-existent, so when investors get box office data it is welcomed news – and now with Disney pulling back the digital curtain even further, the game has again changed.

The other thing to keep in mind is we don’t know if this is Disney’s new normal with streaming releases OR if this will lead others to reveal similar data. In reality this could be a one-off move designed solely to send a message to those who doubted their strategy.

Regardless it is an evolution of the medium and until we have enough of a sample size, shareholders need to take each data point as it comes. Only then can we look at the sum of the parts.

One thing is becoming clearer though, streaming is presenting a lot more viable options that we ever thought possible, for both studios and their investors.

China is cracking down on stocks that trade on U.S. exchanges. Here’s what it means if you hold them

PUBLISHED WED, JUL 7 202110:42 AM EDTUPDATED MON, JUL 12 202111:50 AM EDT

SHAREShare Article via FacebookShare Article via TwitterShare Article via LinkedInShare Article via Email

KEY POINTS

- Beijing is stepping up its oversight on the flood of Chinese listings in the U.S., which are overwhelmingly tech companies.

- The State Council said the rules of “the overseas listing system for domestic enterprises” will be updated, while it will also tighten restrictions on cross-border data flows and security.

- Market analysts say regulatory pressure could not only threaten the IPOs in the pipeline but could also upend the popular Chinese ADR market.

China’s most powerful companies — including Didi, Alibaba and Tencent — are suddenly under immense scrutiny as the country vows to crack down on domestic companies that list on U.S. exchanges, a move that could upend a $2 trillion market loved by some of the biggest American investors.

Beijing is stepping up its oversight on the flood of Chinese listings in the U.S., which are overwhelmingly tech companies. The State Council said in a statement Tuesday that the rules of “the overseas listing system for domestic enterprises” will be updated, while it will also tighten restrictions on cross-border data flows and security.

The crackdown on tech is not a new trend, but because the nation has the ability to move quickly, any action could wreak havoc in major areas on Wall Street. Market analysts say it could not only threaten the IPOs in the pipeline, but it could also pressure the popular Chinese ADR market.

Weigh the risks of owning ADRs

There were at least 248 Chinese companies listed on three major U.S. exchanges with a total market capitalization of $2.1 trillion, according to the U.S.-China Economic and Security Review Commission. There are eight national-level Chinese state-owned enterprises listed in the U.S.

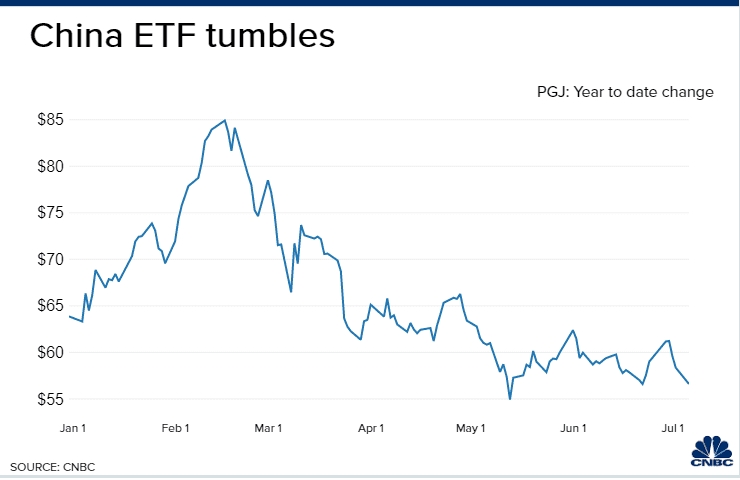

The Invesco Golden Dragon China ETF (PGJ), which tracks U.S.-listed Chinese shares consisting of ADRs of companies that are headquartered and incorporated in mainland China, has lost a third of its value from its February peak amid the increased regulatory pressure. ADR stands for American depositary receipt and they are effectively a way for U.S. investors to buy stakes in foreign companies.

“U.S. investors will have to weigh the risks of owning ADRs at a time when tensions between Beijing and Washington remain elevated while all global investors will have to balance the allure of China’s vast addressable market with the possibility that officials may reshape company prospects at the stroke of a pen via the imposition of regulatory strictures,” BCA Research chief global strategist Peter Berezin said in a note Wednesday.

Ride-hailing app Didi became the latest victim of Chinese authorities’ clampdown. The stock tumbled nearly 20% on Tuesday after Beijing announced a cybersecurity investigation, suspending new user registrations.

Republican Sen. Marco Rubio told The Financial Times in a statement Wednesday that it was “reckless and irresponsible” to allow Didi, an “unaccountable Chinese company,” to sell shares on the New York Stock Exchange.

Meanwhile, Nasdaq-listed Weibo is now planning to go private after its operator Tencent reportedly experienced regulatory probe particularly in its fintech business. Beijing has looked to rein in Chinese billionaire Jack Ma’s Alibaba by unleashing a series of investigations since last year.

“You have to be able to understand the political and national security dynamics that go into an investment, a deal, your engagement with a Chinese company, your investment with the Chinese company, your interest in doing cross-border business,” Longview Global managing director and senior policy analyst Dewardric McNeal said. “This is not clean and neat and just the numbers.”

Some of these major Chinese companies are darlings on Wall Street. For years, Alibaba has been among the five-most owned stocks by hedge funds, along with Facebook, Microsoft, Amazon, Alphabet, according to Goldman Sachs.

Billionaire investor Leon Cooperman recently said Baidu and Alibaba were some of his biggest holdings as he touted stock-picking as a way to success for the second half of the year.

IPOs in jeopardy

Chinese regulators are eyeing a rule change that would allow them to block a domestic company from listing in the U.S. even if the unit selling shares is incorporated outside China, Bloomberg news reported citing people familiar with the matter.

The move could be a huge blow for Chinese companies which have clamored to list in New York in recent years. In 2020, 30 China-based IPOs in the U.S. raised the most capital since 2014, data from Renaissance Capital shows.

There could be fewer and slower new listings in U.S. due to the government crackdown, said Donald Straszheim, senior managing director of China research at Evercore ISI Group.

“Beijing [is] not trying to stop all U.S. listings. Still business ties between the U.S. and China are better than not, ” Straszheim said in a note. ” Beijing [Is] trying to add a layer of protection against corporate foreign compliance.”

As of late April, about 60 Chinese companies were still planning to go public in the U.S. this year, according to the New York Stock Exchange.

— CNBC’s Hannah Miao, Evelyn Cheng and Michael Bloom contributed reporting.

HI Financial Services Mid-Week 06-24-2014