HI Market View Commentary 03-25-2019

What I want to talk about today?

Two main points – What are experts using to trade and what if my results are not matching the S&P 500

The experts have no better “legal” information that you or I now due to the internet

You have to work as hard as they do and that’s why it in impossible to trade for a hobby!!!!

I do my research to make my best “educated” decision on when and how to protect stock ownership, so I can add more shares and/or lower cost basis until my stock takes off like a rocket !!!

Where will our markets end this week?

Lower

DJIA – Bearish

SPX – Bullish

COMP – Bullish

Where Will the SPX end April 2019?

03-25-2019 0.0%

Earnings:

Mon: RHT

Tues: CCL, KBH,

Wed: LEN, FIVE, FUL, PVH

Thur: SPWH,

Fri: BB, KMX

Econ Reports:

Mon:

Tues: Housing Starts, Building Permits, FHFA Housing Price Index, Consumer confidence, New Home Sales

Wed: MBA, Trade Balance, Current Account Balance,

Thur: Initial, Continuing, GDP-3rd Est, GDP Deflator, Pending Home Sales

Fri: Personal Income, Personal Spending, Michigan Sentiment, Chicago PMI, New Home Sales,

Int’l:

Mon –

Tues –

Wed –

Thursday –

Friday-

Sunday –

How am I looking to trade?

Short term stock only positions

Short term spread trades

Get through monthly options expiration on this Friday

And add May options the end of March for Tax/Earning protection

RHT – 3/26

www.myhurleyinvestment.com = Blogsite

customerservice@hurleyinvestments.com = Email

Questions???

Suze Orman: If you get a tax refund, you’re ‘making one of the biggest mistakes out there’

Published Thu, Mar 21 2019 • 12:38 PM EDT • Updated Fri, Mar 22 2019 • 11:10 AM EDT

As tax season continues, many Americans look forward to a hefty refund. But Suze Orman, financial expert and the best-selling author of “Women and Money,” says getting that check from the government shouldn’t be a reason to rejoice.

“If you’re getting a tax refund, you are making one of the biggest mistakes out there,” she tells CNBC Make It.

That’s because a refund is an indication that you’ve basically given the government an interest-free loan.

Here’s why: If you typically receive a substantial refund, it means that more taxes are taken out of your paychecks than you actually owe. The government uses that money throughout the year and then, when you file your taxes in April, it pays you back the extra amount you contributed.

LIVE, NEWS-MAKING DISCUSSIONS

UNIQUE, IN-PERSON EXPERIENCES

If you adjust the amount that’s withheld from your income so less is taken out, you’ll get a smaller refund, or no refund at all, but you’ll see more money in each paycheck.

Though getting a refund may feel like a windfall — the average one is around $2,600 — Orman argues that you could put that money to better use throughout the year. After all, “it’s not as if the government pays you interest on that money,” she says. “You have money that they are holding for you just to get a refund, when you could be getting that extra $100 or $200 a month.”

’’

You have money that they are holding for you just to get a refund, when you could be getting that extra $100 or $200 a month.

Suze Orman

BEST-SELLING AUTHOR OF ‘WOMEN AND MONEY’

As tax season continues, many Americans look forward to a hefty refund. But Suze Orman, financial expert and the best-selling author of “Women and Money,” says getting that check from the government shouldn’t be a reason to rejoice.

“If you’re getting a tax refund, you are making one of the biggest mistakes out there,” she tells CNBC Make It.

That’s because a refund is an indication that you’ve basically given the government an interest-free loan.

Here’s why: If you typically receive a substantial refund, it means that more taxes are taken out of your paychecks than you actually owe. The government uses that money throughout the year and then, when you file your taxes in April, it pays you back the extra amount you contributed.

If you adjust the amount that’s withheld from your income so less is taken out, you’ll get a smaller refund, or no refund at all, but you’ll see more money in each paycheck.

Though getting a refund may feel like a windfall — the average one is around $2,600 — Orman argues that you could put that money to better use throughout the year. After all, “it’s not as if the government pays you interest on that money,” she says. “You have money that they are holding for you just to get a refund, when you could be getting that extra $100 or $200 a month.”

That money could be going straight into a retirement account, where it could start earning interest, for example, Orman suggests. Or you could pay down your credit card balance or student loan debt and avoid racking up additional interest there.

You could “do all kinds of things with that to create more for yourself,” she says.

For Orman, the bottom line is that getting a tax refund is “the biggest waste of money that you will ever get.”

Adjust your withholding so you’ll get more over the course of the year and less at tax time, she suggests. To do that, you’ll need to review your W-4, which is the form that determines how much income tax is withheld from your pay.

If you’re not sure how much you should be withholding, the IRS calculator can give you an idea.

https://seekingalpha.com/article/4249009-allowed-one-investment

If I Was Only Allowed One Investment, This Is It

Mar. 15, 2019 5:48 AM ET

Deep Value, value, growth at reasonable price, medium-term horizon

Summary

Cash is suitable for the short term. Stocks are the best place to be over the long run.

Most investors, most of the time, are sitting on the sidelines. They’re waiting for a better chance to buy at a lower price, or a better chance to sell at a higher price.

Stock prices are often wildly optimistic, meaning everything has to go right for a good outcome. They’re also often wildly pessimistic, meaning you can pick up the stocks of solid companies for peanuts.

In my view, for multiple reasons, there’s one single way for private investors to get the best results from stocks. That’s to always aim to buy stocks when the price is cheap, relative to value. Then wait.

This idea was discussed in more depth with members of my private investing community,OfWealth 3D Stock Investor.

Update, March 18, 2019, 1:15 p.m.: This article has been updated from the original version, which used an inflation-adjusted value for the October 2007 high in the S&P 500. Related figures have been recalculated based on the actual high of 1,549.

About 25 years ago, I was a fresh-faced graduate trainee at a leading investment bank in London. One day, my parents dragged me along to a garden party organised by some friends.

Once there, I was introduced to the global head of the bank’s stock trading business, who must have been a mutual friend of the hosts. He was someone I knew by reputation, but not that I’d actually met before. He made a surprising revelation during our conversation.

He was a nice guy. Old school. Mostly we exchanged the usual chit chat that you get at these events. But one thing that surprised me has always stuck in my mind.

You see, he admitted that he never invested in stocks for his personal account. That was a big deal, given that he was the guy running one of the biggest traders and brokers of stocks in the world.

His reasoning was simple. Since his entire career (translation: annual bonus) was linked to the fortunes of the stock market, he didn’t think it wise to also keep his fortune in stocks.

(He did actually have a big position in the bank’s own stock, since he was a board director. But that was also heavily linked to the fortunes of the stock market – giving him even more reason to look elsewhere with the rest of his money.)

That was an extreme case. Very few private investors have their careers tied to financial markets (or enjoy the lucrative bonuses of professional stock traders). Which means almost all private investors should have substantial investments in stocks, given the profits they offer over time.

Last time, I looked at how the performance of stocks smashes that of bank deposits. Cash is suitable for the short term. Stocks are the best place to be over the long run. But let’s dig further, to see how to make the most out of stock markets.

Stocks for the ultra-long run: US stocks since 1928

(Log scale, nominal, dividends excluded)

Source: Macrotrends

The key here is to understand the difference between a stock’s current market price and its true value. The price is merely the point at which the last trade happened. It’s where marginal buyers and sellers meet.

Most investors, most of the time, are sitting on the sidelines. They’re waiting for a better chance to buy at a lower price, or a better chance to sell at a higher price. Or they’re just happy to sit on what they’ve got, and wait for a very long time. (See here for more on the mechanics of price setting in markets.)

Stock prices are often wildly optimistic, meaning everything has to go right for a good outcome. They’re also often wildly pessimistic, meaning you can pick up the stocks of solid companies for peanuts. Put another way, sometimes they’re way above a reasonable assessment of underlying value, and sometimes they’re deeply below it.

In my view, for multiple reasons, there’s one single way for private investors to get the best results from stocks. That’s to always aim to buy stocks when the price is cheap, relative to value. Then wait.

All other things being equal, this increases the dividend yield, if nothing else. That’s because dividend payments are usually based on underlying company profits, not on the stock price.

The dividend per share (DPS) is the total money allocated to dividend payments by the company, divided by the number of shares. If DPS is $1 and the stock price is $20, then the dividend yield is 5%. If DPS is still $1 but the stock price has dropped to $10 for some macro reason, such as a general market collapse, then the dividend yield increases to 10%.

We can’t know the precise future prospects of the company, either before or after that stock price fall. But we do know that the dividend yield has doubled after the price fall (assuming the company can still afford the payments, which can be assessed by looking at its cash flows and current cash position). The higher yield improves the prospects of strong future profits, all other things being equal.

Buying at that lower price also adds a substantial chance that you’ll enjoy much bigger price gains in the coming years. That’s as short-term market pessimism passes, and the stock price rises back up to (or above) the real value.

Even during a recession, when company profits may fall, in most cases they’ll recover later. Since most of the value of any stock derives from profits that will be generated way out into the future, smart investors can exploit market short-termism to their great advantage. (See more explanation about where a stock’s value come from here and here.)

Of course, not every single stock investment works out, even when you buy them cheaply. Even long-established companies can sometimes get into trouble. That can be either of their own making (mismanagement, strategic missteps, fraud, etc.) or due to factors outside their control (such as new competitors or government regulations).

But if you apply the approach consistently – of buying well across many stocks, or stock indices – you’re sure to do well on average. Buying stocks when they’re cheap reduces risk, and increases likely future profits.

It’s just a question of having the patience and conviction to see it through. That means ignoring short-term price falls, other than seeing them as an opportunity to buy something even more cheaply.

In my last article, I made this statement: “Cash is low risk in the short run, but high risk in the long run. A portfolio of stocks is precisely the opposite. It’s riskier in the short run, but low risk in the long run.”

I then explained my reasoning. But now I’d like to back it up with more evidence. I’ll do that by looking at the outcome for an investor that bought US stocks at one of the worst possible times – at the market peak just before the global financial crisis. How would that investor have done, up until today?

In October 2007 the S&P 500 index traded at 1,549. By March 2009, the index was briefly down 57%. That would be enough to scare practically any investor.

But, by March 2013 it had made back all the losses…less than 6 years after the previous peak. That’s despite the huge banking sector still being in trouble, and having diluted the hell out of existing shareholders with massive capital raises to shore up balance sheets.

By October 2017, a decade after the 2007 peak, the index reached 2,575. That’s a total gain of 66%, equivalent to 5.2% a year (compound). On top of that, there would have been dividends of around 2% a year, for 7.2% total average annual return.

Let’s assume the index investment was then sold. After taxes on capital gains and income, the net return would be around 5.5% a year. That’s equivalent to a total return of 70% over a decade, with compounding (i.e. assuming the net dividends were reinvested).

Total inflation was 18% over those 10 years, which works out at about 1.7% a year (compound). That means the net (post-tax), real (after-inflation) return would have been 3.8% a year. It works out as an increase in purchasing power of 45% over a decade.

Remember: that was from buying stocks at the worst possible moment, just ahead of the biggest financial crisis since the 1930s. And you’d still have increased the purchasing power of the invested funds by 45% over a decade. This illustrates how stocks are great sources of profit over the long run, whatever happens in between.

Of course, few people would have been fully invested in stocks for that whole time. By October 2007, it was already clear that all was not well in the financial system. At that time, it didn’t make sense to have a 100% allocation to stocks.

Instead, hedging the risks with an allocation to long-dated US treasuries made sense, given you could get yields around 5%. Or simply having bank deposits, since they paid decent interest too.

Either way, a big position in cash or treasuries protected an investor from the stock market collapse. Once the dust had settled, say in early 2010, the bonds and cash could have been switched into cheap stocks. Then the investor could have ridden the recovery right up to today. That way, they’d have done much better than owning only stocks right through the turmoil.

Nowadays, bond yields are pretty low. Especially for long-dated bonds, this makes them highly exposed to any increase in inflation and interest rates. So cash makes the better stock hedge at the present time, even though interest rates are low.

Put another way, if you have 40% in stocks today and the market keeps going up you’ll still get at least some stock profits. But if there’s a major drop in stocks – for example if a recession finally bites – a big allocation to cash will allow you to pick up more stocks later, at lower prices – thus riding the likely recovery.

This is why I currently recommend a relatively light allocation to stocks of just 40%. This bull market is long in the tooth. But even current stock investments are still likely to do well eventually, especially if bought at undemanding valuations today.

A major market crash (say -40%) or sudden drop (say -20%) may not actually happen in the near future. So it still pays to own at least some stocks, especially if bought well.

Look at it this way. The trailing price-to-earnings ratio of the S&P 500 was 21.73 in September 1991, which is about the same as today’s level. If you’d bought the index back then, and just held on until today, you’d have made 9.6% a year (with dividends reinvested and before taxes). That’s 7.2% a year above inflation, over almost 28 years.

Even after taxes, that would probably have worked out close to 6% net, real return a year. At that rate, an investment doubles its purchasing power every 12 years.

Even stocks aren’t always a good idea

Of course, there have been some extreme episodes when owning stocks was a bad idea. Investors that bought at the very peak of the 1929 bubble, just ahead of Wall St. Crash and Great Depression, had to wait until about 1944 to break even.

But even then, the real (pre-tax) return was 5.9% a year for anyone that stuck with it until 1959, meaning three decades. And that was after enduring by far the biggest ever crash in US stocks, in percentage terms (around -90% between September 1929 and June 1932).

Things were also tough for anyone that bought US stocks in late 1968. After inflation, it took until 1984 to break even, including dividends. That’s because inflation took off, and valuation multiples such as the market P/E collapsed by the late 1970s. But after 30 years – up to late 1998 – the average real return was up at 6.5% a year (before taxes).

The case for stocks is strong, especially if you own a diversified bunch of them. Even for those in the past that bought into stock indices at market peaks, they’ve always resulted in strong returns over 30 years or so. Which is about the time frame that most private investors should be thinking about.

Even over 10 years, the range of outcomes for every starting year since 1950 is between -3% and +21%. It’s clear that the odds are stacked in the favour of stock investors that take a long-term approach.

The following chart shows how the range of historical outcomes narrows as holding periods become longer, using data for US stocks since 1950. No single 20-year period made less than 4% nominal return. Bonds did well too, in the past. But I can’t see how that will be repeated in future, given still-low bond yields today. (Unless we’re about to experience deep and prolonged deflation, which seems highly unlikely given how central bankers behave these days.)

Source: JP Morgan Asset Management

Putting this together, if someone told me I had to pick one single investment, and could not touch it for at least a decade, it would definitely be a stock index. But which one?

I’d probably choose to invest in the MSCI All-Countries World Index of stocks (ACWI). Over half of it’s made up of US stocks, with the rest split between other countries, both developed and emerging markets.

At the end of February, the MSCI ACWI had a trailing price-to-earnings ratio of 16.9. It also had a dividend yield of 2.6%. Since US companies make big cash distributions in the form of stock buybacks, and there are lower levels in other places too, I estimate the total distribution yield is about 4%.

Corporate profits should roughly grow in line with nominal GDP growth in the countries where they operate. Let’s say nominal GDP growth across the world averages about 4-5% in future, measured in US dollars (being 2% inflation and 2-3% real growth on top).

Add that to the distribution yield and this stock index looks good for about 8-9% a year, over the long run and in US dollars.

Now let’s see… 8-9% a year on highly diversified stocks… or 2.6% on US treasury bonds… or even less on cash? It’s clear which is preferable.

For a one-stop shop of stock investing, you can buy the iShares MSCI ACWI ETF (NASDAQ:ACWI). With a more targeted approach – especially one that’s focused on deep value stocks – you’re likely to do even better.

Disclosure: OfWealth expressly prohibits its writers from having a financial interest in any individual securities they recommend to their readers, other than collective investments such as exchange traded funds.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

https://seekingalpha.com/article/4250939-facebook-stalls-pre-earnings-still-cheap

Facebook Stalls Pre-Earnings But Is Still Too Cheap

Mar. 25, 2019 8:37 PM ET

Summary

In spite of Facebook’s recent news, I set a price target of $188.99 by the end of the next quarter.

Technical patterns in Facebook are mostly bullish and show the stock to have investors with dip-buying habits.

Facebook has an upward bias in regard to news events; investors should not worry too much.

Pre-earnings drift is also a significant factor for upward pressure on the stock over the next month.

Looking for more? I update all of my investing ideas and strategies to members of Exposing Earnings. Start your free trial today »

Last time we looked at Facebook (FB), we predicted the stock’s movement after the post-earnings gap. The prediction proved true, with the recommend two-week exit point coinciding almost perfectly with the completion of the pullback. I then said that FB would resume its upward momentum, which also came true but a slew of negative news reversed the trend.

The Problem with Glamour Stocks

FB’s stock sees extra volatility for being a highly followed company. Stocks that have large amount of associated news tend to post excess gains and losses on the days surrounding those news events. The current big piece of Facebook news is the report showing a large amount of sensitive data was logged internally.

This was mostly taken as bad news, as common sense would dictate, retarding the stock’s three day mini-rally and producing a single black crow, which is a bearish reversal candlestick. However, I believe this is not only an overreaction to the news but good news. First, the overreaction: It is an overreaction because every tech company privy to private information must find a balance between logging data for the sake of solving system problems and ensuring privacy for the sake of protecting its customers.

Second, my view is that the fact we are reading about this means that the staff of Facebook cared enough to report this finding. There was no cover-up; rather, an internal investigation was conducted, implying future improvements in customer privacy. Facebook holds the monopoly on social media marketing and thus cannot turn to others for best practices; it must pioneer them itself.

Pre-earnings Drift

This news produced a small drop in Facebook (thus far) at exactly one month before its earnings report:

{kind=link}

(Source: NASDAQ)

One month ahead of earnings is usually when pre-earnings drift begins. We might look at FB’s earnings as a possible trade in my newsletter, but for now I can say that a preliminary analysis implies upward pre-earnings drift. Thus, all things being equal, FB should rise from here, thereby making the current dip a potential entry point for excess returns.

A contradictory signal: Dips followed by analyst downgrades do tend to cause downward drift. Needham reduced FB from a buy to a hold. But to counterbalance this, Nomura upgraded FB from a neutral to a buy one week earlier.

After Pre-earnings Drift: An Earnings Pre-preview

Earnings will be the key here. FB has shown amazing earnings growth over the past five years. However, this earnings growth is slowing. This is mean reversion and is a phenomenon linked to future underperformance in maturing growth stocks such as Facebook.

Margins, however, are still strong and improving at fast paces. The company’s operating margin is nearly 50%; the profit margin is nearly 40%. Yet return on equity is roughly average for this sector.

Strong earnings should help solidify these margins. Although glamour stocks typically present concave payoffs on earnings, FB’s cognitive dissonance profile – measured by how it (and thus its investors) reacts to news events – shows an overall upward bolstering effect. FB has a very strong underreaction response to bad news, an upward bias for neutral news, and a slightly dampened response to positive news.

Technical Warning Signs?

Technically, FB has a double top in its charts, which is typically treated as a bearish signal:

{kind=link}

(Source: Damon Verial; data from Yahoo Finance)

However, these chart patterns are theoretical – and if any backtesting is performed it is done so across the general market. I backtested this pattern on FB specifically and found it not to be a bearish signal. Instead, based on FB’s current place in its technical patterns, it may rise up to 15% over the next two quarters.

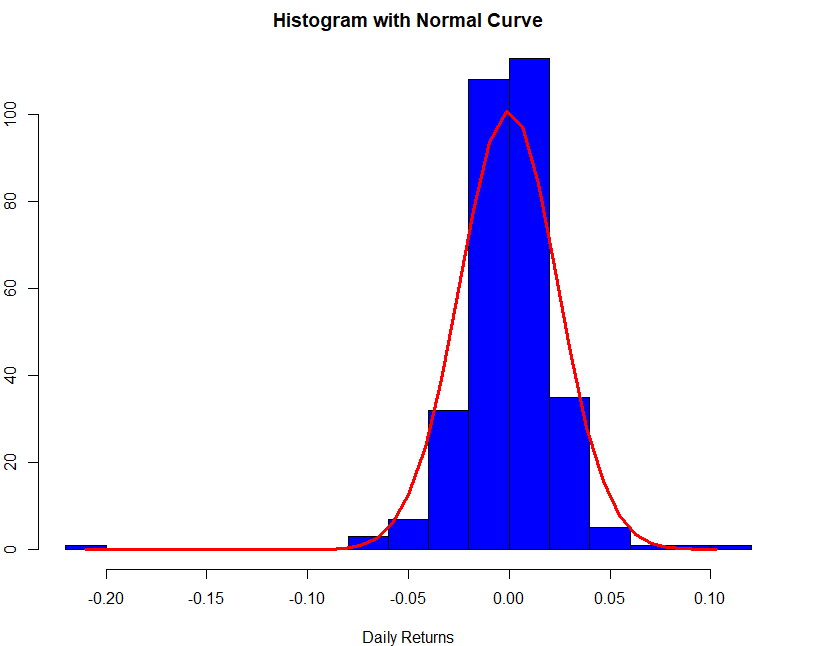

It is normal to see large down gaps in Facebook’s chart. These down gaps are typically area gaps that fill slowly. You can see FB’s distribution of returns is roughly Gaussian but with negative skew; the general description of FB’s movement pattern is that it sometimes suffers large drawdowns but continues its upward momentum over time:

{kind=link}

(Source: Damon Verial; data from Yahoo Finance)

Ignoring gaps, you can see FB’s Markov chain pattern. This random walk is almost random but slightly biased toward moving upward. This pattern is common among stocks for which dip-buying is popular (i.e., down days produce more buying action, while up days do not produce a particular bias):

{kind=link}

(Source: Damon Verial; data from Yahoo Finance)

Conclusion

In short, the technical and pre-earnings drift patterns point to upward movement in the stock. The main concerns at the moment are news-based. But the cognitive dissonance analysis shows that FB is bolstered against most news events.

In addition, the recent news events are subjective. While FB has recently gotten a lot of bad press, my interpretation is not negative. Note that these issues say little-to-nothing about FB’s other revenue sources, such as WhatsApp and Instagram – the latter, in particular, showing huge growth in digital marketing spending.

I suggest FB longs hold through the pre-earnings drift, at least. I will likely take a more in-depth look at FB for a possible earnings play in my newsletter. But from my preliminary statistical analysis, holding through earnings and the following quarter should produce alpha.

Happy trading.

Exposing Earnings is an earnings trade newsletter (with live chat) that is based on statistics, probability, and backtests. My models are unavailable anywhere else online, as I designed them myself, keeping the code private for Exposing Earnings subscribers and myself. If you want a definitive answer on which way a stock will go on earnings, the probability of the prediction paying off, the risk/reward of the play, and my specific options strategy for the play, click here.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

2 comments

hi!,I really like your writing so a lot! share we keep up a correspondence extra approximately

your article on AOL? I need a specialist on this space to solve my problem.

May be that is you! Having a look forward to look you.

I’ve been surfing online more than 3 hours today,

yet I never found any interesting article like yours. It’s pretty worth enough

for me. In my view, if all site owners and bloggers made good content

as you did, the net will be much more useful than ever before.