HI Financial Services Commentary 04-17-2018

You Tube Video Link: https://youtu.be/PsHJQWRUd4E

What I want to talk about today?

How are you able to be so calm over the volatility we’ve had and how do you do it?

What happening this week and why?

Where will our markets end this week?

Higher

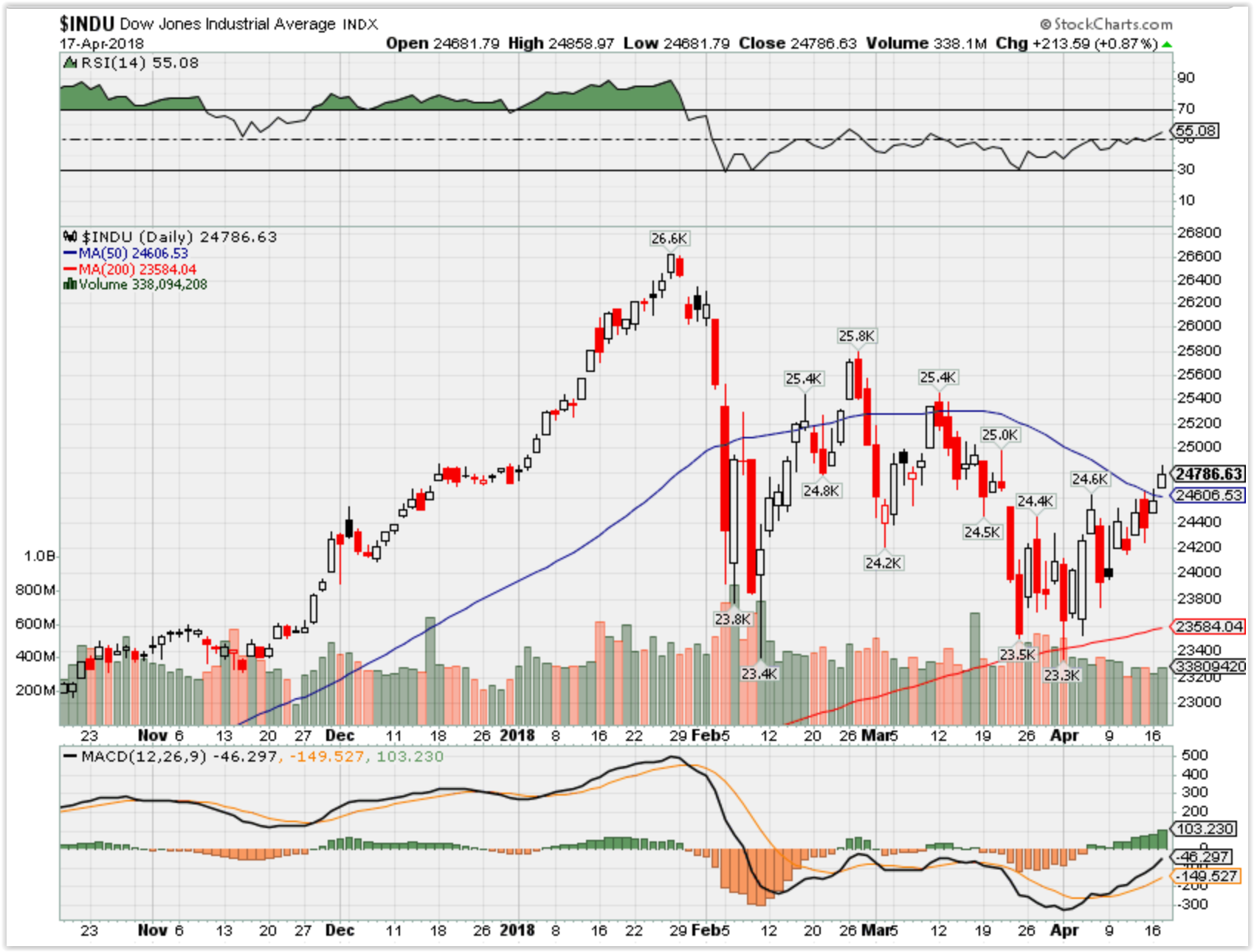

DJIA – Bullish

SPX – Bullish

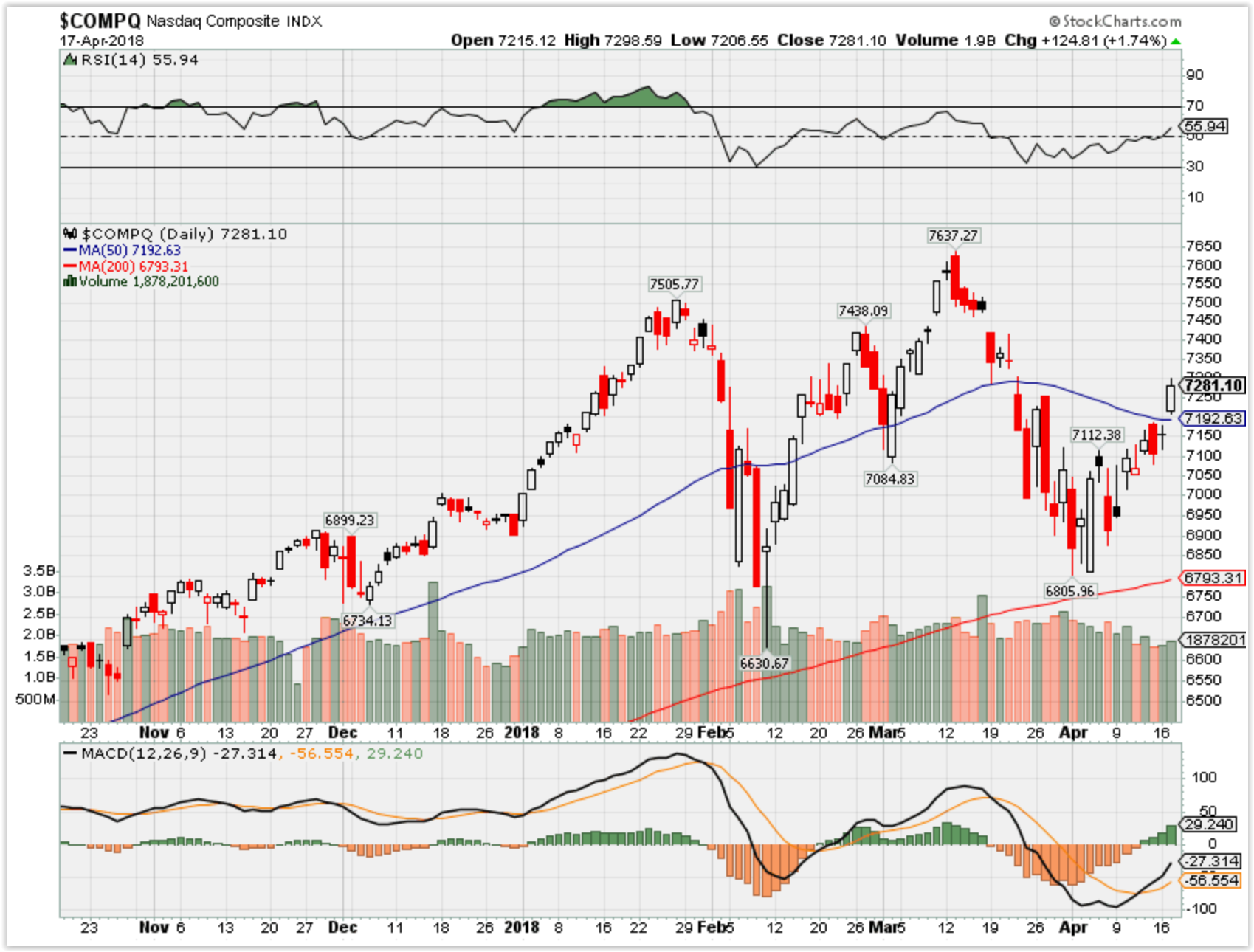

COMP – Bullish

Where Will the SPX end April 2018?

04-10-2018 0.0%

04-10-2018 -2.0%

04-02-2018 -2.0%

03-28-2018 -2.0%

Earnings:

Tues: GS, CSX, IBM, JNJ, PGR, UAL, ISRG, IBKR

Wed: ABT, AA, MS, USB, AXP, VMI

Thur: GWW, KEY, NUE, PM, SNA, ETFC

Fri: BHGE, ERIC, GE, HON, SLB, SWK, WM

Econ Reports:

Tues: Housing Starts, Building Permits, Industrial Production, Capacity Utilization

Wed: MBA, Fed Beige Book

Thur: Initial, Continuing Claims, Phil, Fed, Leading Indicators

Fri: OPTION EXPIRATION

Int’l:

Tues –

Wed –

Thursday –

Friday-

Sunday – JP:PMI Manufacturing Index Flash

How am I looking to trade?

Build my earnings list a couple of weeks before AA Reports

AAPL – 05/01 AMC

AOBC 06/28

BAC – 04/16 BMO

BIDU – 04/26 est

DIS – 05/08 AMC

F – 04/25 AMC

FB – 04/25 AMC

FCX – 04/24 BMO

KMX – 04/04 BMO

MO – 04/26 BMO

V – 04/26 AMC

ZION – 04/23 AMC

UAA – 05/01 BMO

www.myhurleyinvestment.com = Blogsite

customerservice@hurleyinvestments.com = Email

Questions???

https://seekingalpha.com/article/4162179-apple-time-cash-flood

Apple: Time For The Cash Flood

Apr. 10, 2018 2:20 PM ET

Long/short equity, growth at reasonable price, research analyst, Deep Value

Summary

Apple is set to announce updated capital return plans following tax repatriation.

The tech giant has $163 billion in net cash plus strong free cash flows to flood the market with cash.

The company is likely to boost the net stock buyback yield back to the 7% levels.

Share count reductions should help offset some of the weakness from iPhone sales.

When Apple (AAPL) reports FQ2 results for the period ending March on May 1, the tech giant is set to outline the capital allocation plans after tax repatriation. The cash flood could be the catalyst for the stock soaring to $200 and becoming the first stock to top the $1 trillion mark in market cap.

$200 Target

Back on April 5, Citi (NYSE:C) reiterated a $200 price target on the stock due in part to expected massive capital returns. The biggest issue is that iPhone X demand continues to struggle and might hit future earnings expectations.

The stock has about 16% upside to reach this price target. Such a gain would send Apple’s market cap up toward just shy of $1 trillion depending on the level of stock buybacks. The downside of reducing the share count is a lowered market cap.

The issue of the day though is the massive cash position and debt loads at the end of December. Apple ended 2017 with a cash balance of $285 billion and a debt position of $122 billion for a net cash position of $163 billion.

Source: Apple capital return history

My previous research suggested that Apple wouldn’t push the net cash position below $120 billion. The CFO suggested on the FQ1 earnings call that the company would move more toward a net cash neutral position over time.

What exactly this means is entirely unclear. What’s known is that the current cash balance amounts to 19% of the $860 billion market cap.

Apple now regularly announces capital return plans along with the FQ2 report at the start of May. Last year, Apple added $50 billion to the program bringing the lifetime total to $300 billion. Citi analyst Jim Suva sees the tech giant adding $100 billion to the total and doubling the annual share buybacks.

Apple spent $33 billion on share buybacks last year, so the suggestion is that the company spends over $60 billion this year. At a current stock price of $173, Apple could repurchase about 347 million shares or nearly 7% of the outstanding shares.

The stock had a similar 7% net stock buyback yield back in 2016 when Apple was extremely cheap and nearly doubled in the following two years.

A similar plan in FY19 would lead to a nearly 15% reduction in the share count without a meaningful impact to the net cash balance due to ongoing cash flow generation.

Earnings Hit?

A big part of what Apple can spend on capital returns are the free cash flows going forward. The key here is that tax benefits have offset some of the weakness expected out of the key iPhone X.

Goldman Sachs (NYSE:GS) cut revenue estimates by about 2% for the next couple of years due to iPhone X weakness. So far though, EPS estimates have mostly held up with analyst targets of $13.00 in FY19 and $14.30 in FY20.

AAPL EPS Estimates for Current Fiscal Year data by YCharts

EPS estimates for FY18 and FY19 already have come off the highs. The big question is whether these numbers fall further.

The estimate is that Apple generates up to $60 billion in FCF a year now after several years of reaching $50 billion. As one can quickly realize, three years of FCF at those levels will exceed the current net cash balance showing the importance of growing the business and not just the current balance sheet.

Three years at FCF levels of $60 billion plus the current net cash balance adds up to nearly $350 billion in available cash to invest or return to shareholders. A $1 billion hit here and there to FCF doesn’t greatly impact that Apple will have nearly 40% of the current market cap in cash to distribute by the end of 2020.

Also, remember that those EPS estimates don’t always factor in the benefits of stock buybacks. The estimates by Citi of annual stock buybacks of $60 billion don’t actually top the FCF by that much so those buyback levels are sustainable.

With a standard 10% dividend hike to a quarterly payout of $0.70, Apple would pay out about $14 billion annually for dividends. Only the dividend payout and tax repatriation payments averaging $5 billion per year would actually dig into the cash balance, still leaving Apple with a net balance far above $100 billion for an extended period.

As an example, the FY20 EPS estimate of $14.30 is only a 10% gain from FY19 levels. The projected stock buyback levels would account for the majority of those EPS gains, suggesting the business isn’t going to see any gains under that scenario. Or stated another way, any upside in the business will contribute to higher profits than the current projection.

Takeaway

The key investor takeaway is that Apple is set to at least double the share buyback plan while making the traditional 10% hike to the dividend. With more than $30 per share in net cash, the stock is extremely cheap, trading at 10x FY20 EPS estimates. This valuation remains supportive of the company ramping up stock buybacks which will further boost forward EPS estimates and make the stock even cheaper.

The big cash flood should boost the stock to new heights including reaching $200 and approaching the $1 trillion market cap. Ironically though, aggressive stock buybacks could actually hold back the company hitting that huge milestone though rather meaningless to shareholders. Either way, the flood of cash should propel Apple higher.

Disclosure: I am/we are long AAPL.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: The information contained herein is for informational purposes only. Nothing in this article should be taken as a solicitation to purchase or sell securities. Before buying or selling any stock you should do your own research and reach your own conclusion or consult a financial advisor. Investing includes risks, including loss of principal.

Like this article