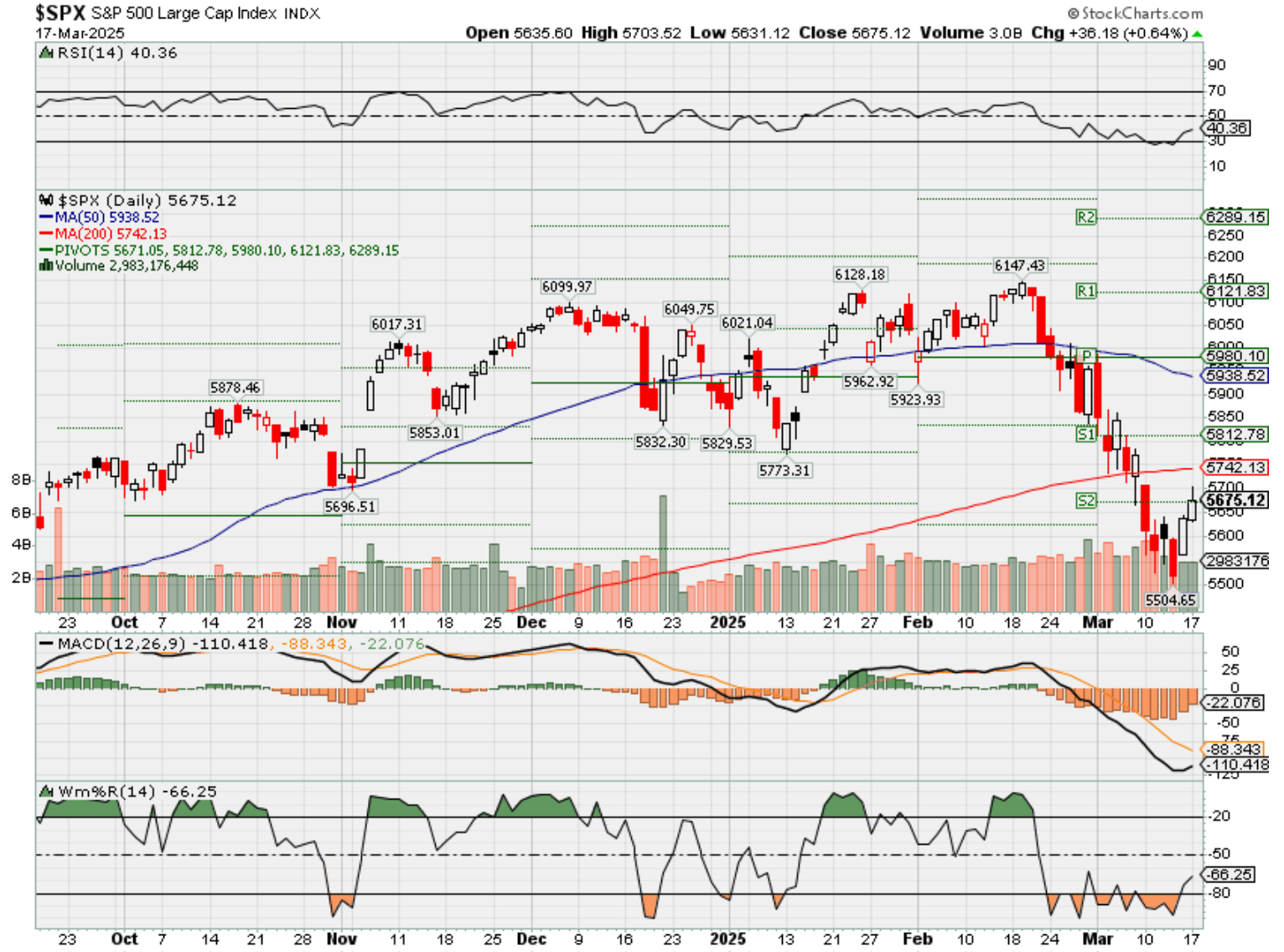

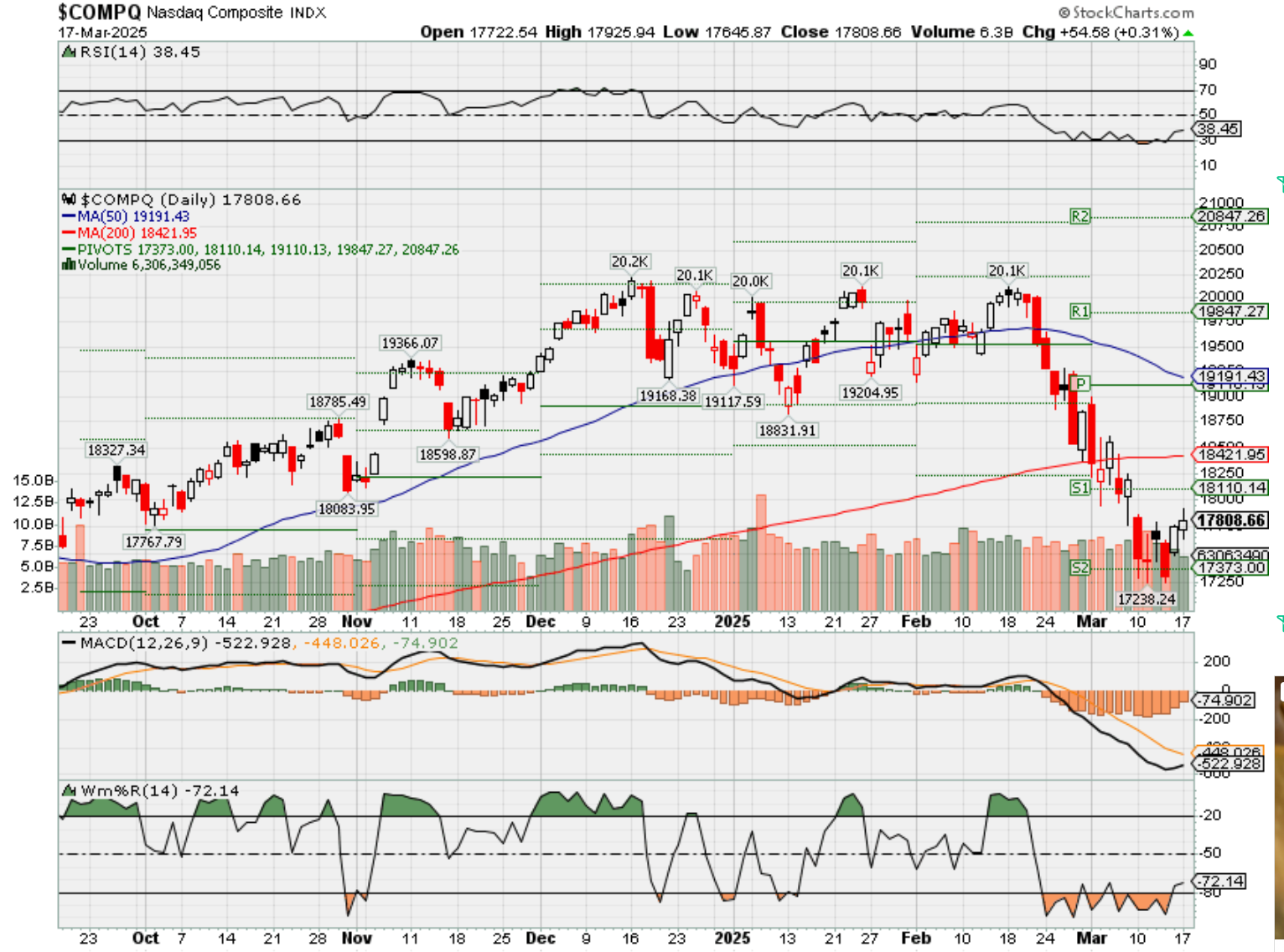

HI Market View Commentary 03-17-2025

Market uncertainty has led us to be more nimble in moving protection around

We want to have “some” protection in place instead of not enough

6 Bear Market Stops

- Canada & Mexico come to terms with Trump

- A Ukraine/Russia Resolution

- Tax Breaks – Doge found us money = Deficit Cut or Cash in our pockets

- Better China relations

- 20-35% drop makes the market cheap – we entered correction (-10%)

- The US economy resets – Entitlement problem

https://www.briefing.com/the-big-picture

The Big Picture

Last Updated: 14-Mar-25 16:58 ET | Archive

How bad can a recession be?

Column summary:

- Earnings estimates decline in a recession.

- The depth and/or duration of any recession will ultimately dictate how bad an earnings decline will be.

- Portfolio adjustments can mitigate recession risks.

Recessions are part of the business cycle. Fortunately, they do not happen often, but when they happen, they hurt in more ways than one. People lose their jobs, credit defaults increase, businesses suffer as customers spend less, loans are harder to get, and stock prices take a hit.

Why do stock prices take a hit?

- Earnings contract and earnings estimates get cut.

- Investors refocus efforts on preserving capital versus the traditional pursuit of seeking a return on capital.

- Emotional selling, driven by the fear of suffering additional losses, takes root.

- Margin calls happen as stock prices slide, triggering forced sales for overleveraged investors unable to meet margin loan requirements.

- Investor confidence is shaken, resulting in fewer buyers and more sellers.

The main item at the root of it all, though, is that first item: earnings contract and earnings estimates get cut.

Some Brutal Episodes

Not all recessions are the same.

The Great Recession of December 2007 to June 2009 (sparked by the financial crisis) was brutal. It lasted 18 months, housing prices plummeted, the unemployment rate spiked to 10%, and the S&P 500 declined as much as 57%.

The COVID recession was also brutal. The unemployment rate spiked to 14.8% and the S&P 500 declined as much as 32%. The remarkable thing about the COVID recession, though, is that it lasted just two months (February 2020 to April 2020) in NBER Business Cycle dating terms thanks to the massive fiscal and monetary policy stimulus implemented by Congress and the Federal Reserve. The psychological and economic effects of that recession, however, lasted a lot longer than two months.

Still, with the U.S. economy and global economy effectively grinding to a halt in early 2020, one can imagine how that quickly changed the earnings outlook. You can see that in the chart below.

The forward 12-month EPS estimate, which stood at $175.00 on January 20, 2020, dropped to $138.48 as of May 15, 2020. That is a 20.9% decline. The average peak-to-trough earnings drop in a recession since 1960 has been about 31%, according to Yale University Professor Robert Shiller’s data.

In one sense, then, the COVID recession wasn’t nearly as bad as the Great Recession, but it was worse than the recession associated with the dot-com bust and 9/11.

Recession Talk in the Air

Lately, there has been a lot of talk about the U.S. economy facing the risk of a recession. That narrative has picked up with the inversion of the 3-month T-bill yield and the 10-year Treasury note yield, the arrival of some disappointing economic reports signaling some weakness in consumer spending and consumer confidence, and of course the cloud of uncertainty swirling around tariff and counter-tariff actions.

The price action in the stock market has exacerbated the recession worries, partly because it has featured the outperformance of the counter-cyclical sectors and partly because of the reduced wealth effect tied to the roughly $5 trillion decline in the S&P 500 market cap.

The S&P 500 has declined as much as 10.5% since hitting an all-time high on February 19. The Nasdaq has dropped as much as 14.7% from the all-time high it reached in December, and the Russell 2000 has declined as much as 19.5% from the all-time high it hit in November.

You wouldn’t have any inkling that the ‘R’ word was even being mentioned, however, when looking at the forward 12-month EPS estimate. In the same time the S&P 500 has declined more than 10%, the forward 12-month EPS estimate has increased 1.0% to $277.08, according to FactSet. Given that, the forward 12-month P/E multiple has contracted to 20.3x from 22.4x.

So, how bad could a recession be?

First, there has to be one, and secondly, the depth and/or duration of any recession will ultimately dictate how bad an earnings decline will be. In modern times, the Great Recession stemming from the financial crisis is about as bad as it gets from both a depth and duration standpoint; we saw a 35.3% cut in the earnings estimate during that period. The COVID recession was worse in terms of its depth but not anywhere close in terms of its duration.

The current forward 12-month estimate isn’t taking any recession risk into account, which is why it can be said that there is a lot of downside risk in it if a recession were to come to fruition.

Using the last three recessions as an approximate guide for the scope of estimate declines, we can approximate what the S&P 500 price risk might be based on a range of average historical multiples — 5yr (19.8), 10yr (18.3), 20yr (16.2), and 25yr (16.7). The S&P 500 is currently trading at 5,630.

- A 14% cut to the EPS estimate

| P/E Multiple | EPS Est. | Price |

| 19.8 | $238.29 | 4,718 |

| 18.3 | $238.29 | 4,360 |

| 16.2 | $238.29 | 3,860 |

| 16.7 | $238.29 | 3,979 |

- A 21% cut to the EPS estimate

| P/E Multiple | EPS Est. | Price |

| 19.8 | $218.89 | 4,334 |

| 18.3 | $218.89 | 4,006 |

| 16.2 | $218.89 | 3,546 |

| 16.7 | $218.89 | 3,655 |

- A 35% cut to the EPS estimate

| P/E Multiple | EPS Est. | Price |

| 19.8 | $180.10 | 3,566 |

| 18.3 | $180.10 | 3,296 |

| 16.2 | $180.10 | 2,918 |

| 16.7 | $180.10 | 3,008 |

Briefing Analysis

The recent sell-off in the stock market hasn’t felt good. It has happened quickly, not in a fearful kind of way but in a recalibration kind of way. Valuations were stretched, economic news was mostly disappointing, tariff actions cranked up, and a market hitting all-time highs roughly four weeks ago, and savoring the idea of tax cuts and deregulation, was suddenly hearing voices about a possible recession.

It may ultimately turn out to be nothing more than voices in the market’s head, but if nothing else, the recession narrative has fostered the reminder that nothing good happens in terms of earnings estimates when a recession hits.

We have some historical guidelines for earnings estimate trends in prior recessions, but each recession is different. There is no recession today and there may not be a recession anytime soon — or perhaps there will be. The market will sniff it out and price it in long before the NBER will slap a date on it.

This bull market has clearly been disrupted by the idea of a growth slowdown that could turn into something more. If you want to insulate your investment portfolio for a growth slowdown or a recession, here are several ways to do so:

- Add exposure to countercyclical sectors like health care, consumer staples, and utilities.

- Lean more on stocks of high-quality companies that have a sound financial position and a history of regularly increasing their dividend.

- Preserve capital while generating income with the purchase of government bonds and investment-grade corporate bonds.

- Allocate some money to alternative investments like precious metals.

- Tamp down individual stock risk with the purchase of mutual funds and or ETFs.

- Raise some cash to deploy in the event of a material downturn in the market.

Nobody likes the idea of a recession, but they are part of the business cycle. In the same vein, a downward revision to earnings estimates is part of a recession experience. How that translates into stock prices will have a lot to do with the severity of the recession. There isn’t a recession embedded in the current earnings estimate, yet the stock market is seemingly bracing for a disruption of some kind to the estimate trend. Accordingly, stock prices have taken a hit.

—Patrick J. O’Hare, Briefing.com

Where will our markets end this week?

Lower

DJIA – Bearish

SPX – Bearish

COMP – Bearish

Where Will the SPX end March 2025?

03-1702025 -4.0%

03-10-2025 -1.5%

03-03-2025 -1.5%

Earnings:

Mon:

Tues: TME,

Wed: GIS, FIVE, SMCI

Thur: DRI, FDX, NKE, JBL, MU,

Fri: CCL,

Econ Reports:

Mon: Empire, Retail Sales, Retail Sales ex-auto, Business Inventories, NAHB Housing Market Index, Empire Manufacturing

Tue Housing Starts, Building Permits, Import, Export, Capacity Utilization, Industrial Production,

Wed: MBA, FOMC Rate Meeting,

Thur: Initial Claims, Continuing Claims, Phil Fed, Existing Home Sales, Leading Indicators,

Fri: OPTIONS EXPIRATION

How am I looking to trade?

Now we are protecting for technical crossovers to the downside AND tariff risk.

www.myhurleyinvestment.com = Blogsite

info@hurleyinvestments.com = Email

Questions???

China’s Baidu launches two new AI models as industry competition heats up

Published Sun, Mar 16 20254:54 AM EDT

Key Points

- China’s Baidu said on Sunday it has launched two new artificial intelligence models, including a new reasoning-focused model that it said rivalled DeepSeek’s model, as it vies to stand out in a fiercely competitive AI race.

- “ERNIE X1 delivers performance on par with DeepSeek R1 at only half the price,” Baidu said of one of the new models.

- One of China’s earliest tech giants to launch a ChatGPT-style chatbot, Baidu has struggled to gain widespread adoption for its Ernie large language model.

China’s Baidu said on Sunday it has launched two new artificial intelligence models, including a new reasoning-focused model that it said rivalled DeepSeek’s model, as it vies to stand out in a fiercely competitive AI race.

Chinese AI startup DeepSeek’s roll-out of AI models which it says is on par with, or even better than, industry-leading models in the United States at a fraction of the cost, has roiled the industry and re-energised the global AI race.

“ERNIE X1 delivers performance on par with DeepSeek R1 at only half the price,” Baidu said of one of the new models. The X1 has “stronger understanding, planning, reflection, and evolution capabilities,” Baidu said, adding that it is the first deep thinking model that uses tools autonomously.

Baidu said its latest foundation model ERNIE 4.5 has “excellent multimodal understanding ability. It has more advanced language ability, and its understanding, generation, logic, and memory abilities are comprehensively improved.”

It also has “high EQ”, and it is easy to understand network memes and satirical cartoons, Baidu said.

One of China’s earliest tech giants to launch a ChatGPT-style chatbot, Baidu has struggled to gain widespread adoption for its Ernie large language model, despite claiming performance comparable to OpenAI’s GPT-4, amid fierce competition.

Multimodal AI systems are capable of processing and integrating various types of data including text, video, images and audio, and can convert content across these formats.

Trump and Putin expected to speak this week as US pushes for Russia-Ukraine ceasefire

By Reuters | Posted – March 16, 2025 at 11:34 a.m.

KEY TAKEAWAYS

- President Donald Trump plans to speak with Vladimir Putin to discuss a Russia-Ukraine ceasefire.

- U.S. envoy Steve Witkoff describes recent Moscow meeting with Putin as “positive.”

- Trump warns conflict could escalate without ceasefire and seeks Putin’s cooperation.

WASHINGTON — President Donald Trump is expected to speak with Russian President Vladimir Putin this week on ways to end the three-year war in Ukraine, U.S. envoy Steve Witkoff told CNN on Sunday after returning from what he described as a “positive” meeting with Putin in Moscow.

“I expect that there will be a call with both presidents this week, and we’re also continuing to engage and have conversation with the Ukrainians,” said Witkoff, who met with Putin on Thursday night, adding that he thought the talk between Trump and Putin would be “really good and positive.”

Trump is trying to win Putin’s support for a 30-day ceasefire proposal that Ukraine accepted last week, as both sides continued trading heavy aerial strikes through the weekend and Russia moved closer to ejecting Ukrainian forces from their months-old foothold in the western Russian region of Kursk.

Trump said in a social media post on Friday that there was “a very good chance that this horrible, bloody war can finally come to an end.” He also said he had “strongly requested” that Putin not kill the thousands of Ukrainian troops that Russia is pushing out of Kursk.

Putin said he would honor Trump’s request to spare the lives of the Ukrainian troops if they surrendered. The Kremlin also said on Friday that Putin had sent Trump a message about his ceasefire plan via Witkoff, expressing “cautious optimism” that a deal could be reached to end the conflict.

In separate appearances on Sunday shows, Witkoff, Secretary of State Marco Rubio, and Trump’s national security adviser, Mike Waltz, emphasized that there are still challenges to be worked out before Russia agrees to a ceasefire, much less a final peaceful resolution to the war.

Asked on ABC whether the U.S. would accept a peace deal in which Russia was allowed to keep stretches of eastern Ukraine that it has seized, Waltz replied, “Are we going to drive every Russian off of every inch of Ukrainian soil?” He added that the negotiations had to be grounded in “reality.”

Rubio told CBS a final peace deal would “involve a lot of hard work, concessions from both Russia and Ukraine,” and that it would be difficult to even begin those negotiations “as long as they’re shooting at each other.”

Trump has warned that unless a ceasefire is reached, the conflict between Moscow and Kyiv has the potential to spiral into World War Three.

His administration took steps last week to induce further cooperation on a ceasefire. On Saturday, Trump said that General Keith Kellogg’s role had been narrowed from special envoy for Ukraine and Russia to only Ukraine, after Russian officials sought to exclude him from peace talks.

A license allowing U.S. energy transactions with Russian financial institutions expired last week, according to the Trump administration, raising pressure on Putin to come to a peace agreement over Ukraine.

The Treasury Department is looking at possible sanctions on Russian oil majors and oilfield service companies, a source familiar with the matter said, deepening steps already taken by Biden.

The Key Takeaways for this article were generated with the assistance of large language models and reviewed by our editorial team. The article, itself, is solely human-written.

Trump administration sends a clear message to the oil and gas industry: ‘You’re the customer’

Published Sat, Mar 15 20259:18 AM EDT

Key Points

- Interior Secretary Doug Burgum and Energy Secretary Chris Wright made clear this week they want to make it as easy as possible to drill on federal land and waters.

- Burgum said he views companies developing resources on federal lands as “customers” who are contributing to the national “balance sheet.”

- “You’re the customer,” the interior secretary told oil, gas and mining executives at a conference in Houston.

Interior Secretary Doug Burgum: We’re bringing back manufacturing and mining to the U.S.

HOUSTON — The officials leading President Donald Trump’s energy agenda made clear to oil, gas and mining executives this week that they have an ally in Washington who intends to make it as easy as possible for them to drill in federal lands and waters.

Interior Secretary Doug Burgum told executives gathered for the world’s largest energy conference that the Trump administration does not view climate change as an existential threat. Energy Secretary Chris Wright said rising global temperatures are simply a byproduct of developing the country’s national resources to support economic growth and national security.

Burgum leads Trump’s recently established National Energy Dominance Council and Wright serves as his deputy on the interagency body tasked with boosting production. Burgum was effusive in his praise of the oil and gas industry during remarks delivered at CERAWeek by S&P Global conference.

“I’m going to share two words that I do not think that you have heard from a federal official in the Biden administration during the last four years. And those two words are thank you,” said Burgum, who previously served as governor of North Dakota, a state that produces 1.2 million barrels of oil per day.

Burgum leaned on his experience as software company executive to lay out his view of the interior department’s role. The department under his leadership views the companies developing resources on federal lands as “customers” who are contributing revenue to the nation’s “balance sheet,” Burgum said.

“If someone was sending me revenue, they weren’t the enemy. They were the customer,” Burgum said. The administration loves anyone who wants to harvest timber, mine for critical minerals, graze cattle, or produce oil and gas on federals, the interior secretary said.

Royalties sent from lease agreements on federal land will help the U.S. pay down its national debt and balance the budget, Burgum said. “You’re the customer,” the interior secretary told the executives.

The value of nation’s abundant natural resources far outweighs its $36 trillion in debt, Burgum said. If financial markets understood the value of America’s natural resources, the 10-year long-term interest rate would come down, Burgum claimed.

“The interest rates right now are one of the biggest expenses we have as a country,” Burgum said. “So one of the things that we have to do is unleash America’s balance sheet, and President Trump is helping us do that,” he said.

Burgum slammed the Biden administration’s focus on climate change as an “ideology.” He said the Trump administration views Iran acquiring a nuclear weapon and China winning the artificial intelligence race as the two existential threats facing the U.S. rather than global warming. Wright said Biden had a “myopic” and “quasi religious” belief in reducing emissions that hurt consumers.

Burgum and Wright dismissed policies that support a transition from fossil fuels to renewable energy, arguing that wind and solar won’t be able to meet rising energy demand in the coming years from artificial intelligence and re-industrialization.

“There is simply no physical way that wind, solar and batteries could replace the myriad uses of natural gas. I haven’t even mentioned oil or coal yet,” Wright said at the conference. Wright previously served as CEO of oilfield services company Liberty Energy and a board member at nuclear startup Oklo.

Oil execs see allies in Washington

Oil executives are enthusiastic about the change of administrations in Washington, returning the praise they received from Trump’s energy team during the week.

ConocoPhillips CEO Ryan Lance said Wright and Burgum “understand the business,” describing them as the best energy team the U.S. has seen in decades. TotalEnergies CEO Patrick Pouyanné said he was “impressed by the quality of our counterparts.” Chevron CEO Mike Wirth said the industry is “seeing some reality come back to the conversation.”

“For years, my message has been, we need a balanced conversation about affordability, reliability and the environment, and focusing only on climate leads us to ignore the first two,” Wright said.

Energy Sec. Wright: We can get to no or very low tariffs, but it’s got to be reciprocal

The executives all referred to the Gulf of Mexico as the Gulf of America, following Trump’s executive order to rename the body of water. The president issued an order on his first day to repeal Biden’s ban on offshore drilling in 625 million acres of U.S. coastal waters.

BP CEO Murray Auchincloss briefly slipped before correcting himself when discussing how generative AI is helping with exploration: “We started doing this in the Gulf of Mexico, uh America, and we spread that to other nations as well.”

But Trump’s calls to “drill, baby, drill” are running up against market reality. The CEOs of Chevron and Conoco said U.S. oil production will likely plateau in the coming years after hitting new records under the Biden administration.

“Chasing growth for growth’s sake has not proven to be particularly successful for our industry,” Wirth said. “At some point, you’ve grown enough that you should start to move towards a plateau, and you should generate more free cash flow, rather than just more barrels.”

Lance sees U.S. oil production plateauing later this decade and then slowly declining.

“Maybe it’s time to go back to exploring the Gulf of America,” Pouyanné said. “The new administration is opening the Gulf. It has been slowed down after the Macondo drama,” he said, referring the Deepwater Horizon oil spill, the largest in the history of marine drilling operations.

U.S. oil producers are scheduled to meet with Trump next week, industry lobby group American Petroleum Institute said in statement.

After such a relentless market correction, the relief rally faces a high burden of proof

Published Sat, Mar 15 20259:07 AM EDT

Michael Santoli@michaelsantoli

It felt better, but did it mean anything?

Friday’s zippy 2.1% bounce in the S&P 500, at minimum, interrupted one of the more relentless retrenchments from a record high Wall Street had seen.

The index took a mere three weeks and a day to fall just over 10% from its peak on Feb. 19 through Thursday’s close, in its way an equal and opposite reaction to the imperturbable rally that had lifted the market to those highs.

Without reciting the entire lab report on what has the market under the weather, like most corrections this one has a composite of causes.

It starts with the pre-existing condition of a highly concentrated, expensive index riding elevated expectations for an ideal economic and policy backdrop into 2025.

An initial infection (a winter soft patch in consumer spending and a rethink of the sustainability of the AI-buildout theme) led straight to some complications: Walmart’s downbeat outlook on Feb. 20 worsened the “growth scare” while helping to kneecap the crowded momentum cohort of stocks, which included Walmart, Costco, Eli Lilly and JP Morgan, along with Nvidia, Meta Platforms and the like.

Finally, the medication for the top-heavy market – rotation into value and overseas stocks – had the side effect of swamping the index due to the enormous size of stocks being sold versus those being bought.

And, yes, the erratic declarations of escalating tariffs and haphazard cuts in government employment have generated a near-constant barrage of “tape bombs” to keep traders off balance.

A one-day relief bounce can’t cure all that, but Friday’s pop did at least check off a few initial boxes on the correction-comeback worksheet. The rise was overwhelmingly broad, the upside NYSE volume falling a whisper shy of 90%.

At minimum, it broke an uncommonly persistent downtrend, with daily intraday losses that formed an unnervingly linear angle of descent. The S&P 500 hadn’t closed above its five-day moving average – yes, five-day – in March, until it easily surpassed it on Friday. Constructive, but not decisive.

It’s mildly heartening to the bulls that the pop came on a day when a wretched University of Michigan consumer sentiment report fell shy of forecasts while showing a drop in confidence in the job market and another rise in inflation expectations.

Resilience against an admittedly impressionistic and politically inflected survey is at least a decent hint that the recent sell-off already took account of the downturn in “soft data” and for the market to deepen the pullback by much from already oversold levels, it would take tangible evidence of a faltering economy.

Consumer-discretionary stocks, on an equal-weighted basis, had spent weeks collapsing relative to defensive consumer staples, as seen here. A key indicator of the market’s macro message, this relationship has round-tripped since Election Day and sits somewhere close to a make-or break level.

Bank of America’s consumer-stock trading desk shared a comment Friday from a client on the urgent downside reversal in cyclical stocks: “We might be late innings in the positioning unwind, but we’re early innings in the recession risk narrative. And thus, does the recession overhang/uncertainty keep mean reversion buyers on-hold?”

Of course, we get more growth scares than recessions, which is a slight comfort, perhaps. We’ll get a fresh monthly retail-sales report next week, which will be a timely test of whether consumers are acting much more cautious or mostly just speaking that way to pollsters.

A market low is a process

The standard playbook for evaluating corrections and comebacks requires a recitation of the time-yellowed clichés: V-bottoms happen, but they are relatively rare. A market low is a process, not a moment. And short, sharp rallies are common but always have much to prove.

At the S&P 500 closing print at 5,638, it had merely bounced to the high of the prior few days and sits below its mid-July peak. From here it needs to climb another 1.8% just to get back to its 200-day moving average. Larry McMillan of McMillan Analysis offers the reminder that snapback rallies in corrections often extend to a 20-day average before failing; that threshold is now 4% above where the index finished the week.

One would also want to see if the market could rise on a day when the aggressive tariff threats are flying, as a further sign it is building calluses against the policy friction. Friday was a rare session when all was quiet on this front.

Other modestly hopeful factors to toss onto the pile:

- Fast corrections such as this one are somewhat more likely to be short-lived setbacks worth buying.

- This drop was among the seven briefest 10% declines in history. Fundstrat Research says after all of the prior six, the market was higher three, six and 12 months later.

- The S&P has been down four straight weeks and it’s pretty rare to lose over five in a row. Next week’s options expiration is handicapped to exert an upward bias.

- And this is exactly the time of the year when seasonal forces start to turn more positive.

EquityClock.com

Beyond the tactical X’s and O’s that inform the opportunistic gambits and systematic wagers of the short-term money, it’s fair to observe that the market has undergone a tidy little reset in valuation and expectations.

Lower valuation

In a timely call, Truist Wealth chief market strategist Keith Lerner downgraded equities to neutral in late February just after the market peaked. Last Tuesday, he suggested a decent amount of risk had been bled from the market.

He noted the S&P 500 dropped two P/E points, from 22-times forward profits to about 20, in rapid fashion. In recent years, that’s around where the tape has tended to stabilize. He adds that the magnitude of the index drop roughly means “the market is ‘pricing in’ about a 1 in 3 chance of recession versus almost nothing a few weeks ago.”

I’ll add that the mega-cap-growth Nasdaq 100 index, still 11% off its high, has fallen three forward-P/E turns to below 24, and is now at its ten-year average valuation premium to the S&P 500. The equal-weight S&P 500 is right at its 15-year P.E average near 16.

None of this makes the market inexpensive or represents a wide margin of safety. And, of course, such ratios are only as good as the earnings forecasts, which are hanging in there but would appear to have more downside risk than upside.

Yet if the urgent unwind in momentum strategies has abated (as many sell-side trading desks insist is likely), it’s plausible to look for the mega-cap tier of the market to perhaps begin showing defensive characteristics against macro and policy flux, as it has in the past.

None of this adds up to an emphatic case that the messy sell-[off has run its course. Payback for two straight 20% up years might not be complete. While sentiment has soured and some oversold conditions preceded Friday’s rebound, key indicators had only begun to hint at a possible capitulative washout.

And, of course, the speed and haphazard nature of the Trump administration’s policy blitz – and officials’ open willingness to accept or even invite economic pain in pursuit of their goals – are hard-to-handicap factors. I’ll continue to argue that the downside leadership of the correction did not line up with what one would expect if it were “all about tariffs.” But that doesn’t mean that President Trump’s war of choice against allies in pursuit of his version of trade parity in manufactured goods will not pressure the economy and the mindset of asset allocators indefinitely.

Still, the market behavior to date – as dizzying and against-consensus has it’s been – has not deviated enough from a typical setback in a post-election growth scare to insist that the rules for assessing this market’s prospects have changed definitively with the leadership the White House.

https://www.theverge.com/news/629940/apple-siri-robby-walker-delayed-ai-features

Leaked Apple meeting shows how dire the Siri situation really is

The company is aiming to get some of the AI-powered features announced last June into iOS 19 — but it’s not guaranteed.

by Chris Welch

Mar 14, 2025, 1:27 PM MDT

Chris Welch is a senior reviewer who has worked at The Verge since its founding in 2011. His coverage areas include audio (Sonos, Apple, Bose, Sony, etc.), home theater, smartphones, photography, and more.

In recent weeks, Apple has been unable to escape headlines about its slow progress with everything having to do with Siri and artificial intelligence. The company has officially delayed features first promised last June intended to modernize Siri and give Apple a much-needed boost in the AI race. We still don’t know when those Apple Intelligence capabilities will arrive, and if a recent all-hands meeting is anything to go by, neither does Apple itself.

Bloomberg has the full scoop on what happened at a Siri team meeting led by senior director Robby Walker, who oversees the division. He called the delay an “ugly” situation and sympathized with employees who might be feeling burned out or frustrated by Apple’s decisions and Siri’s still-lackluster reputation. He also said it’s not a given that the missing Siri features will make it into iOS 19 this year; that’s the company’s current target, but “doesn’t mean that we’re shipping then,” he told employees.

“We have other commitments across Apple to other projects,” Walker said, according to Bloomberg’s report. “We want to keep our commitments to those, and we understand those are now potentially more timeline-urgent than the features that have been deferred.”

The meeting also hinted at tension between Apple’s Siri unit and the marketing division. Walker said the communications team wanted to highlight features like Siri understanding personal context and being able to take action based on what’s currently on a user’s screen — even though they were nowhere near ready. Those WWDC teases and the resulting customer expectations only made matters worse, Walker acknowledged. Apple has since pulled an iPhone 16 ad that showcased the features and has added disclaimers to several areas of its website noting they’ve all been punted to a TBD date. They were held back in part due to quality issues “that resulted in them not working properly up to a third of the time,” according to Mark Gurman.

Apple has not publicly commented on the situation beyond last week’s statement, when it said the advanced Siri capabilities were “taking longer than expected.” But Walker told his staff that senior executives like software chief Craig Federighi and AI boss John Giannandrea are taking “intense personal accountability” for a predicament that’s drawing fierce criticism as the months pass by with little to show for it beyond a prettier Siri animation.

“Customers are not expecting only these new features but they also want a more fully rounded-out Siri,” Walker said. “We’re going to ship these features and more as soon as they are ready.” He praised the team for its “incredibly impressive” work so far. “These are not quite ready to go to the general public, even though our competitors might have launched them in this state or worse,” he said of the delayed features.