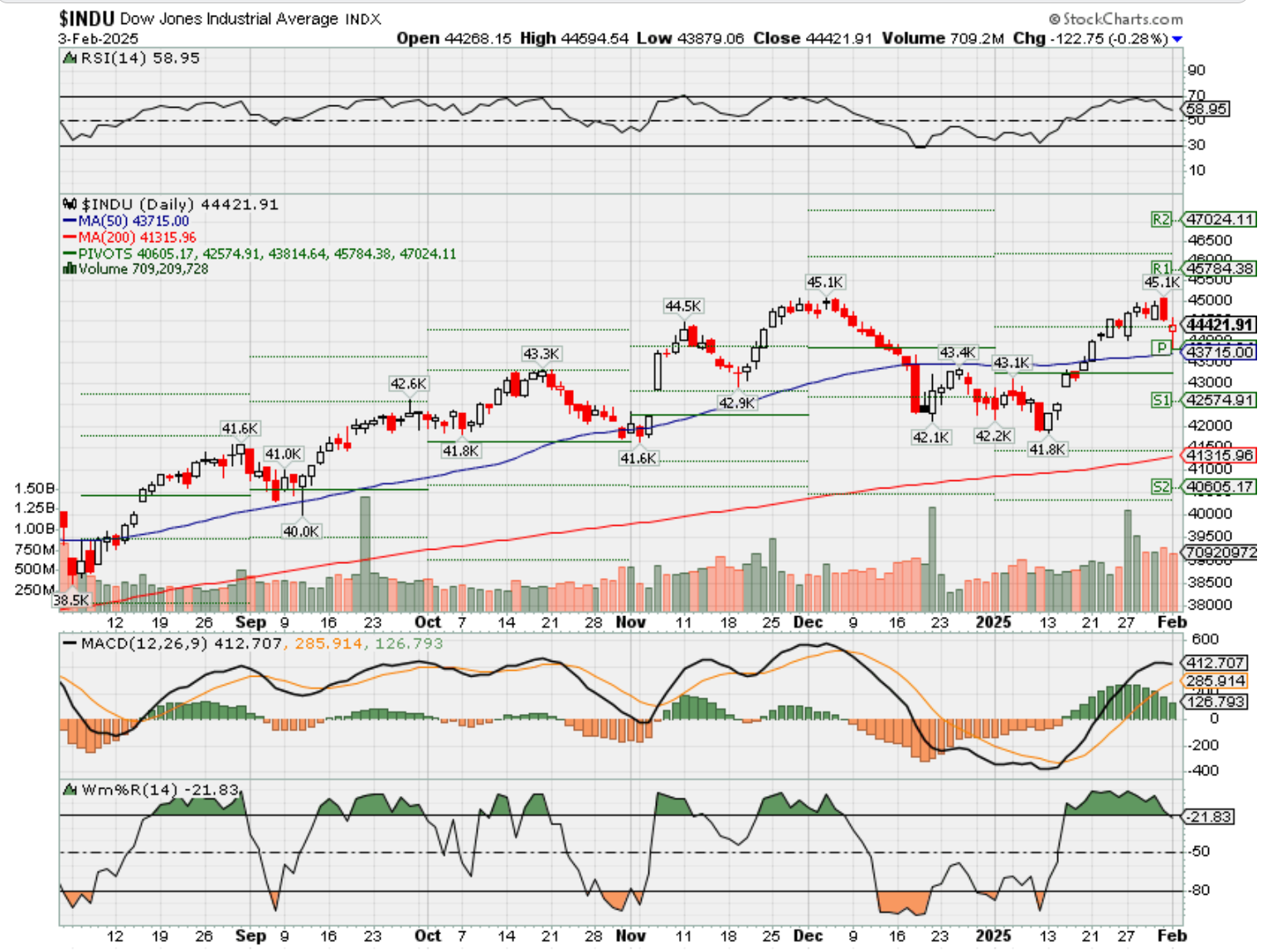

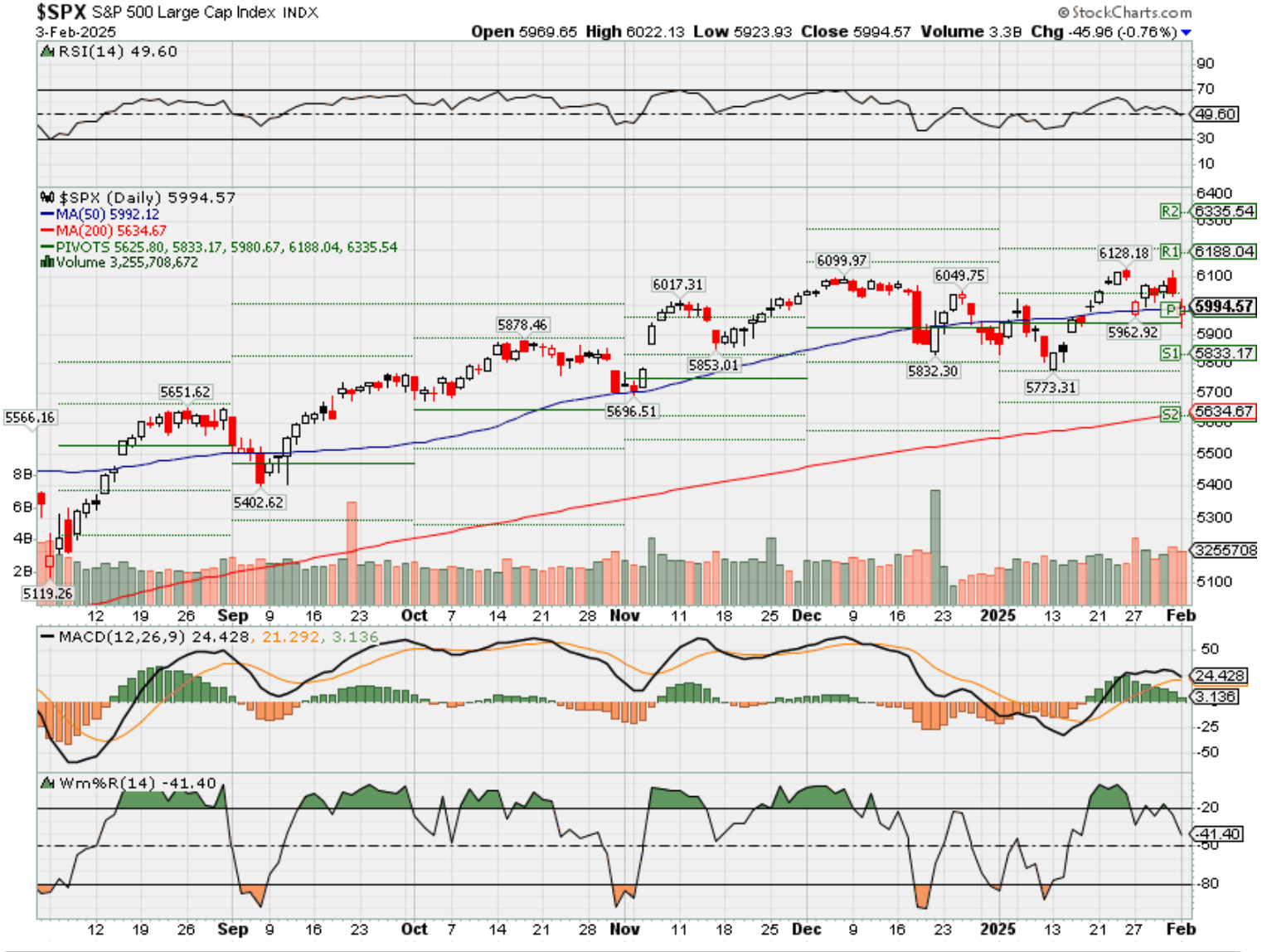

HI Market View Commentary 02-03-2025

What happened today in our markets?= Tariff Talks dropped the market -0.76

Tomorrow is would be the buy in day for the first of the month with new money

YES someone sold META today for a $21 loss

We felt pretty comfortable with what had protection and what didn’t

TODAY when the market was down -1.02 we were up +0.30

![]()

![]()

![]()

GOOGL and DIS have protection OTM slightly lower than the stock is currently trading

Earnings dates:

BABA 02/06 BMO

BIDU 02/26 est BMO

DG 03/13 est BMO

DIS 02/05 BMO

F 02/05 AMC

GOOGL 02/04 AMC

KO 02/11 est BMO

MU 03/19 est AMC

NVDA 02/26 AMC

O 02/20 est AMC

SQ 02/20 AMC

TGT 03/12 est BMO

https://www.briefing.com/the-big-picture

The Big Picture

Last Updated: 31-Jan-25 14:19 ET | Archive

The best return of all to normal

Interest rates are higher these days for a variety of reasons. Some think they are too high for the good of the economy. Others think they are right where they belong because of how good the economy is.

Somewhere in that mix is a tussle over sticky inflation and misgivings about the U.S. fiscal situation.

What is clear in the chart below is that Treasury yields are roughly where they were before the Great Financial Crisis unfolded (i.e., the last time things were “normal”).

From QE to QT

As the financial crisis unfolded, the Federal Reserve took extraordinary measures that included lowering the fed funds rate to the zero bound and blowing out its balance sheet with a massive program buying Treasury and agency mortgage-backed securities.

The latter was known as a quantitative easing program, whereby the Federal Reserve purposely worked to suppress market rates with its purchases to stoke loan demand and stronger spending activity. This “QE” program was not normal, yet Ben Bernanke, and then Jerome Powell, embraced this policy tool during their respective crisis management phases.

Nowadays, the Federal Reserve is working to shrink its balance sheet with a quantitative tightening program (“QT”).

It has had some success shrinking its balance sheet from roughly $9 trillion in 2022 to “only” $6.8 trillion today. For some normal perspective, however, bear in mind that the Fed’s assets were roughly $900 billion when the Great Financial Crisis exploded in 2008.

The Fed is trying to return to normal by shrinking its balance sheet. Ultimately, it looks destined to be stuck in the “new normal” of a bloated balance sheet for some time for several reasons:

- The U.S. is a deficit-financed growth company that perennially requires the issuance of debt to pay for outlays that aren’t fully covered by receipts.

- The Federal Reserve, under its ample reserves regime, intends to slow and then stop the decline in its balance sheet when reserve balances are somewhat above the level it judges to be consistent with ample reserves1. At his most recent press conference, Fed Chair Powell observed that the most recent data suggest that reserves are still abundant, remaining roughly as high as they were when the runoff began.

- Improved yields in other sovereign bond markets threaten to reduce the level of purchase activity by foreign buyers.

- The geopolitical risk China faces by holding dollar-denominated assets, which could be frozen in the event of a hostile action (i.e., invading Taiwan), has presumably tempered some of the buying activity by the Treasury market’s second largest foreign buyer (behind Japan).

Fed Takes Normal Stance

Quantitative easing is no longer a theoretical concept. It is now enmeshed as a viable instrument in the Fed’s toolbox.

What do you think will happen if the U.S. has an economic crisis that destabilizes the financial system?

There will be rate cuts of course, but if it is a profound crisis that kills consumer demand and investor confidence (as profound crises are wont to do), it is a safe bet that the Fed will go back to the QE well.

Let’s hope that it isn’t necessary again. It isn’t normal.

What is looking closer to normal these days is the level of the fed funds rate. It, too, recently sat at levels (5.25-5.50%) last seen before the start of the financial crisis.

The Fed has implemented 100 basis points of easing since last September, yet Fed Chair Powell said this past week that it is the broad sense of the FOMC that the Fed doesn’t need to be in a hurry now to adjust its policy stance. That thinking is tied to the fact that the progress of inflation toward the 2% target has slowed, the labor market has remained solid, and the economy is growing nicely. At the same time, there is heightened uncertainty about what impact President Trump’s tariff proposals will have on inflation and the economy.

The Fed is in a wait-and-see mode, which is normal. Raising rates or lowering rates at successive meetings isn’t normal. To be sure, a policy rate at the zero bound for years on end isn’t anywhere close to normal either.

The Fed, to its credit, has the policy rate back at a level that gives it optionality to cut more if needed, and it got it there without tanking the economy.

Market rates went up with the policy rate and in recognition of an economy that showed signs of acceleration despite the rate hikes. Surprisingly, they also went up after the Fed started to cut rates again in September 2024.

This is where we get back to the tussle over inflation and the U.S. fiscal stance. Fed Chair Powell thinks the move by the 10-yr note is more of a term premium story and not because of expectations about Fed policy or about inflation. Some will debate that view, but implicit in it is a belief that worries about the deficit are the main driver.

We won’t expound on the deficit situation here other than to say that it isn’t normal that the budget deficit as a percentage of GDP is as high as it is with an economy as strong as the economy we have now. Treasury market participants, we suppose, are wrestling with the idea of how much worse it could get if there is an economic downturn or growth from deficit-financed tax cuts doesn’t materialize as advertised; hence, the increase in the term premium.

There is a lot of energy right now behind the idea of the Trump administration cutting the cost of government (without touching Social Security, Medicare, or Medicaid). The feasibility of that effort is in question, though, with Congress controlling the purse strings and politicians needing to deliver on the special interests of their respective constituencies at the risk of losing their job if they don’t.

In the past, talking about cutting the deficit was cheap. We’ll see if that remains the case. It is too early to tell, but there has certainly been a lot of talk about cutting the deficit and getting the U.S. back on a sustainable fiscal track. Wouldn’t that be a nice return to normal?

What It All Means

It hasn’t been easy seeing market rates return to normal levels. Any prospective homeowner will tell you that, as would any homeowner hoping to move but not wanting to give up what we might say is an abnormally low mortgage rate.

Savers and investors, though, have had a lot to cheer watching market rates move higher. Now, they have options to get some real return on Treasury securities, certificates of deposit, high-yield savings accounts, and money market funds that carry less risk.

Investors can strike a better balance in their investment portfolios, which per chance got too overweight with stocks when real returns on savings accounts and Treasuries, for instance, were negative.

There is a real option again to diversify. In other words, there is an alternative to stocks should one choose to go down that road.

One of the best things we saw during the DeepSeek selloff was the safe-haven buying interest in the Treasury market.

That was a normal reaction, and participants didn’t have to accept abnormally low yields for going there. Market rates were at normal levels. It has been a long, tough road getting them back there, and it may just be the best return of all to normal for investors, assuming inflation and the deficit can be successfully redirected to a normal path.

—Patrick J. O’Hare, Briefing.com

Where will our markets end this week?

Lower

DJIA – Bullish

SPX – Bullish

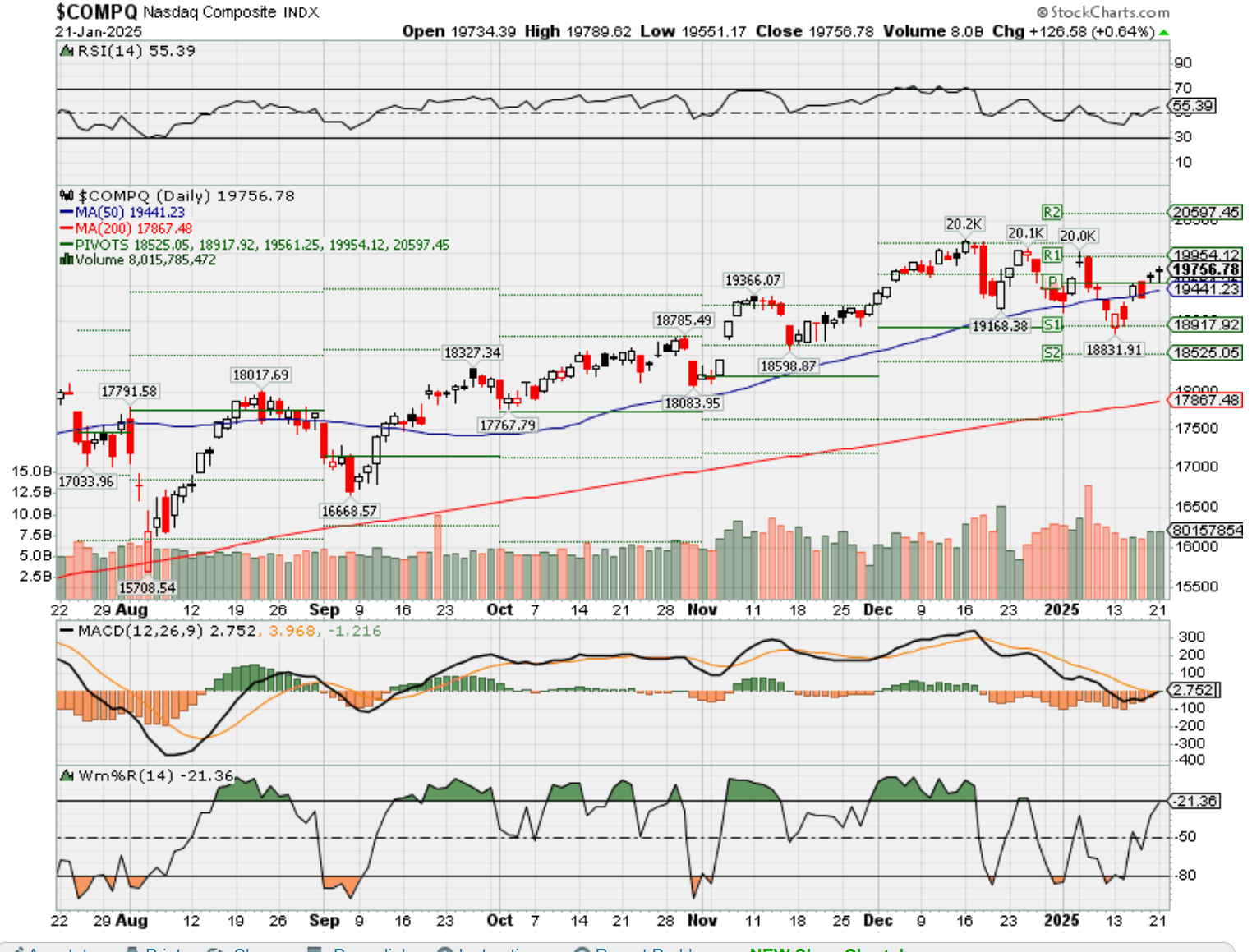

COMP – Bearish

Where Will the SPX end February 2025?

02-03-2025 -1.0%

Earnings:

Mon: CLX, PLTR, RMBS

Tues: CMI, EL, MRK, PYPL, PEP, PFE, UBS, AMD, AMGN, EA, JNPR, MAT, SNAP, AMD, GOOGL

Wed: HOG, ODFL, UBER, YUM, ALL, MET, DIS, F,

Thur: BMY, COP, LLY, HLT, TPR, UAA, GPRO, AMZN

Fri:

Econ Reports:

Mon: ISM Manufacturing, Construction Spending,

Tue Factory Orders,

Wed: MBA, ADP Employment, ISM Services, Trade Balance,

Thur: Initial Claims, Continuing Claims, Productivity, Unit Labor Costs,

Fri: Average Workweek, Non-Farm Payroll, Private Payroll, Hourly Earnings, Unemployment Rate, Michigan Sentiment, Wholesale Inventories, Consumer Credit,

How am I looking to trade?

Now we are protecting for Q4 earnings in 2025

www.myhurleyinvestment.com = Blogsite

info@hurleyinvestments.com = Email

Questions???

David – Will be continue to follow META at the outrageous multiples = YES and we will do a JAN 26 720/800 call options spread. We will spend $31 to make the next $80

We will book roughly a 166% ROI

Trump slaps tariffs on Mexico, Canada and China

Published Sat, Feb 1 20255:07 PM ESTUpdated Mon, Feb 3 20258:34 AM EST

Key Points

- President Donald Trump is imposing 25% tariffs on imports from Mexico and Canada, as well as a 10% duty on China. Energy resources from Canada will have a lower 10% tariff.

- The tariffs on Canadian goods are expected to take effect on or after 12:01 a.m. ET on Tuesday. There is no official metric on when the tariffs would be lifted.

- Tariffs would escalate if the countries retaliate in any way against the U.S.

- Trump has long favored tariffs as a tool to negotiate demands from U.S. trading partners, including longstanding allies.

U.S. President Donald Trump is pushing ahead with long-threatened import tariffs on goods from Canada, Mexico and China.

On Saturday, Trump signed an order imposing 25% tariffs on imports from Mexico and Canada, as well as a 10% duty on China. Energy resources from Canada will be hit with a lower 10% tariff to “minimize any disruptive effects we might have on gasoline and home heating oil prices,” according to a senior administration official.

Together, the U.S. does about $1.6 trillion in annual business with the three countries. Trump is seeking to use the tariffs as both bargaining chips and methods to effect foreign policy changes, specifically the immigration and drug trade issues.

In a message posted on X, Trump cited powers he has under the International Emergency Economic Powers Act. The president said he enacted the levies “because of the major threat of illegal aliens and deadly drugs killing our Citizens, including fentanyl.”

“We need to protect Americans, and it is my duty as President to ensure the safety of all,” he added.

The tariffs on Canadian goods are expected to take effect on or after 12:01 a.m. ET on Tuesday. There is no official word on when the tariffs would be lifted. A senior administration official said Saturday, “There’s going to be a wide range of metrics” to consider.

Also, under the new order, the tariffs would escalate if the countries retaliate in any way against the U.S.

In a CNBC interview Friday, Peter Navarro, Trump’s senior advisor for trade and manufacturing, stressed the dual importance of protecting the economy as well as public safety.

“We’ve got the Super Bowl coming up, and eerily, the amount of people that fit in the [New Orleans] Superdome are almost exactly equal to the number of people dying every year here in America from fentanyl, and that comes from China and Mexico,” Navarro told CNBC in an interview Friday. “This is why we have these kind of discussions.”

Tariffs are duties imposed on foreign goods that are paid by U.S. importers. Economists broadly oppose tariffs, arguing that they result in higher prices for domestic consumers.

But Trump has long promoted tariffs as a way to negotiate better deals with U.S. trading partners, protect domestic industries from foreign competition and gain revenue.

In the Oval Office on Friday, Trump said his decision to slap tariffs on goods from Canada, Mexico and China is “pure economic.”

However, economists worry they could reignite inflation at a time when it appears price pressures are beginning to abate. The Commerce Department reported Friday that an inflation reading closely watched by the Federal Reserve rose to 2.6% in December, but the details in the report appeared more positive. Fed officials have said they are monitoring the impact of fiscal policy.

Trump has vowed to impose new or additional tariffs on numerous other categories of foreign goods, including microchips, oil and gas, steel, aluminum, copper, and pharmaceuticals, including “all forms of medicine.” He has also said he will “absolutely” slap tariffs on the European Union.

The move Saturday, which carries economic risks for the nation as well as for the political capital Trump has accrued since his inauguration, brought objections from congressional Democrats and concern from business leaders.

“The President is right to focus on major problems like our broken border and the scourge of fentanyl, but the imposition of tariffs under IEEPA is unprecedented, won’t solve these problems, and will only raise prices for American families and upend supply chains,” John Murphy, senior vice president and head of international at the the U.S. Chamber of Commerce, said in a statement.

United Auto Workers President Shawn Fain said the union supports aggressive tariffs to protect the interest of workers, not when used as foreign policy tools that use “factory workers as pawns.”

Former Bank of Canada Governor Mark Carney, who is running to lead the Liberal Party, called the tariffs “a clear violation of our trade agreement and require the most serious trade and economic responses in our history.”

Economists worry that the tariffs could reignite inflation at a time when it appears price pressures are beginning to abate.

“It will be very important to have a better sense of the actual policies and how they will be implemented, in addition to greater confidence about how the economy will respond,” Fed Governor Michelle Bowman said.

Speaking to CNBC on Friday morning, Chicago Fed President Austan Goolsbee said the key will be whether the tariffs are one-off events or lead to retaliation.

A range of industries, from homebuilders to alcohol producers, also weighed in on the impact tariffs would have on their businesses and consumers. Other company leaders voiced their concerns about the threat of tariffs ahead of Saturday’s order.

On Saturday, following Trump’s imposition of tariffs on Mexico, Canada and China, House Committee on Agriculture Chairman Glenn “GT” Thompson, R-Pa., issued the following statement: ″President Trump’s tariff policy has been an effective tool in leveling the global playing field and ensuring fair trade for American producers. Look no further than Colombia’s about-face on accepting repatriated criminal migrants at the mere threat of tariffs.”

He added: “I look forward to working alongside of President Trump to support our hardworking producers and to make agriculture great again.”

— CNBC’s Kevin Breuninger and Jeff Cox contributed reporting.

Apple shares rise 3% as boost in services revenue overshadows iPhone miss

Published Thu, Jan 30 202512:00 PM ESTUpdated Thu, Jan 30 20258:32 PM EST

Key Points

- Although Apple’s overall sales rose during the quarter, the company’s closely watched iPhone sales declined slightly on a year-over-year basis.

- Overall China sales declined 11.1% during the quarter to $18.51 billion.

- Apple CEO Tim Cook told CNBC’s Steve Kovach that iPhone sales were stronger in countries where Apple Intelligence is available.

Apple’s overall revenue rose 4% in its first fiscal quarter, but it missed on Wall Street’s iPhone sales expectations and saw sales in China decline 11.1%, the company reported Thursday.

But shares rose about 3% in extended trading after the company gave a forecast for the March quarter that suggested revenue growth.

Here’s how Apple did versus LSEG consensus estimates for the quarter that ended Dec. 28.

- Earnings per share: $2.40 vs. $2.35 estimated

- Revenue: $124.30 billion vs. $124.12 billion estimated

- iPhone revenue: $69.14 billion vs. $71.03 billion estimated

- Mac revenue: $8.99 billion vs. $7.96 billion estimated

- iPad revenue: $8.09 billion vs. $7.32 billion estimated

- Other products revenue: $11.75 billion vs. $12.01 billion estimated

- Services revenue: $26.34 billion vs. $26.09 billion estimated

- Gross margin: 46.9% vs. 46.5% estimated

Apple said it expected growth in the March quarter of “low to mid single digits” on an annual basis. The company also said it expected “low double digits” growth for its Services division. Apple said it expected the strong dollar to drag on Apple’s overall sales about 2.5%, and after accounting for currency, the overall growth rate would be similar to the December quarter’s 6%.

Wall Street was expecting guidance for the March quarter of $1.66 in earnings per share on $95.46 billion in revenue.

Apple’s profit engine, its Services division, which includes subscriptions, warranties and licensing deals, reported $23.12 billion in revenue, which is 14% higher than the same period last year. Apple CEO Tim Cook told analysts on a call Thursday that the company had more than one billion subscriptions, which includes both direct subscriptions for services such as Apple TV+ and iCloud, as well as subscriptions to third-party apps through the company’s App Store system.

Although Apple’s overall sales rose during the quarter, the company’s closely watched iPhone sales declined slightly on a year-over-year basis. The December quarter is the first full quarter with iPhone 16 sales, and Apple released its Apple Intelligence AI suite for the devices during the quarter.

Apple’s iPhone miss versus LSEG estimates was the biggest for the company in two years, since its first-quarter earnings report in fiscal 2023. At the time, Apple said its miss was because it was unable to make enough iPhone 14 models because of production issues in China.

In the first fiscal quarter, the company saw significant weakness in Greater China, which includes the mainland, Hong Kong and Taiwan. Overall China sales declined 11.1% during the quarter to $18.51 billion. It is the largest drop in China sales since the same quarter last year when they fell 12.9%.

Cook told CNBC’s Steve Kovach that iPhone sales were stronger in countries where Apple Intelligence is available. Currently, the software is only available in a handful of English-speaking countries, and it isn’t accessible in China or in Chinese.

“During the December quarter, we saw that in markets where we had rolled out Apple intelligence, that the year-over-year performance on the iPhone 16 family was stronger than those markets where we had not rolled out Apple intelligence,” Cook said.

He added that the company planned to release additional languages in April, including a version of Apple Intelligence in simplified Chinese.

Cook told CNBC that there were three factors in the company’s China performance. He said half of the 11.1% decline was due to a change in “channel inventory,” the fact that Apple Intelligence has not launched in the region and that after the quarter ended, China issued a national subsidy that would stimulate some Apple product sales.

“If you look at the negative 11, half of the decline is due to a change in channel inventory, and so the operational performance is better,” Cook said.

The company reported $36.33 billion in net income during the quarter, up 7.1% from $33.92 billion in the same period last year.

In its fiscal first-quarter earnings report on Thursday, Apple reported a gross margin — the profit left after accounting for the cost of goods sold — of 46.9%. That is the highest on record, surpassing the 46.6% margin the company recorded in the period ending March 2024. Apple said it expected gross margin in the March quarter to be between 46.5% and 47.5%.

Apple’s iPad and Mac sales showed strong growth over last year’s struggling sales in the holiday quarter. Mac revenue rose 15% to $8.98 billion and iPad revenue grew 15% to $8.08 billion. The company’s Mac division posted its best growth since the fourth fiscal quarter of 2022.

The company released new Macs during the quarter, including the new iMac, Mac Mini and MacBook Pro laptops in October. Apple also launched a new iPad Mini during the quarter. Cook attributed the growth in those segments to new products.

“It’s driven by the significant excitement around our latest Mac lineup,” Cook said.

Cook told analysts on an earnings call that the company had an active base of 2.35 billion active devices, up from the 2.2 billion figure the company provided a year ago.

The company’s “other products” category, also called Wearables, which includes the Apple Watch, AirPods, Beats and Vision Pro sales, declined 2% on a year-over-year basis to $11.75 billion in sales.

Apple said it would pay a dividend of 25 cents per share and spent $30 billion on dividends and share repurchases during the first quarter.

How fractional hiring creates a paradigm shift in the workplace

It’s a new age of opportunity and innovation, but a few factors are holding businesses back from taking full advantage of this. A significant hurdle is the scarcity of skilled labor, stemming from demographic shifts like an aging population and declining birth rates. The COVID-19 pandemic exacerbated these shortages by disrupting labor markets and fostering hesitancy among workers to re-engage in certain sectors. Furthermore, evolving skill demands in a digital economy have created mismatches between available positions and workers’ capabilities. Changing work attitudes, such as a preference for remote or flexible arrangements, have reshaped workplace dynamics, leaving many hiring managers uncertain about attracting highly skilled workers.

Given these societal shifts and mounting hiring pressures, managers must reconsider their assumptions about the future of work. They must also shed outdated hiring practices. Fraction, a novel venture founded by Praveen Ghanta, Alyssia Maluda and Jeffrey Baker, is offering innovative solutions to address these challenges.

A strategic concept: Fractional hiring

Fractional hiring is a strategic approach where businesses engage professionals part-time or on a project-specific basis, leveraging their expertise without committing to full-time employment. This model enables organizations to access specialized skills precisely when needed, transcending the limitations of traditional employment structures. By embracing fractional hiring, businesses tap into a diverse pool of talent to navigate the dynamic currents of the modern economy.

One entrepreneur’s fractional awakening: Praveen Ghanta

In 2007, Praveen Ghanta found himself at a crossroads. Moving from New York City to Atlanta meant leaving behind the lucrative tech jobs he once knew. With a surplus of time and a need for flexibility, he delved into the world of contract positions. Juggling roles at Oracle and Air2Web, he soon realized the potential of fractional work.

Left to right: Praveen Ghanta, Jeffrey Baker and Alyssia Maluda

Working part-time for multiple companies wasn’t just a way to make ends meet; it was a revelation. Ghanta’s employers were happy with his work, and he received positive reviews and bonuses. But beyond financial gains, fractional work kept him sharp. Seeing how different companies tackled similar problems enhanced his skills and broadened his perspective.

When the startup bug bit him, Ghanta co-founded HiddenLevers. Fractional hiring became their mantra. They needed senior talent without diluting their equity stakes or breaking the bank. Their first fractional hire—a senior integration developer—proved a game-changer. Over nine years, he completed and maintained over 25 integrations, showcasing the power of fractional work.

They continued to build their team with fractional hires, from their future CTO to senior front-end developers and QA engineers. By 2020, they had a full-fledged software development team, thanks to fractional hiring. Even more than bringing efficient hiring to the team, fractional hiring turned out to be the key to staying true to the company’s vision.

An AI-powered solution for significant transformation

For his new venture, Ghanta has teamed up with Alyssia Maluda, who brings a unique blend of startup acumen and industry insight from the fintech sector, as well as Jeffrey Baker, whose software development expertise comes from a passion for creating industry-specific solutions. Together, they founded Fraction, which empowers businesses to update talent acquisition and workforce optimization with its AI-powered CTO. Even beyond the bionic CTO, Fraction offers a suite of services tailored to the evolving needs of the modern workforce, providing tools for flexibility and efficiency.

Whether through fractional hiring solutions for accessing top-tier talent part-time, an AI-enhanced CTO, or AI-powered tools for enhancing productivity, Fraction offers solutions that transcend traditional boundaries. Fraction has mapped the way forward, and they’re ready to share what they know.

INVESTMENT OUTLOOK

An environment favorable to bonds

Amid a backdrop of global straining against inflationary headwinds, the United States experienced exceptional economic and financial market performance in 2024. Your clients may be wondering, “Will it continue, what’s the investment forecast, and how can I prepare for 2025 and beyond?” The Vanguard Economic and Market Outlook for 2025 offers some guidance—including investment insights about the potentially favorable long-term environment for bonds.

Monetary policy in most developed markets has meant falling inflation the past two years, accompanied by slowdowns. But the United States saw accelerating economic growth and full employment, with no discernible effect from restrictive monetary policy.

Supply-side forces, including a surge in both labor productivity and available labor, have been tailwinds aiding the U.S. economy’s resilience. Among the downside risks to bonds and equities we’re most closely monitoring is a rise in long-term rates due to continued fiscal deficit spending or removal of supply-side support. The potential upside for bond returns, however, should not be discounted.

Evaluating the long-term attractiveness of fixed income

Fixed-income markets have flourished as part of the recent U.S. growth story. In looking ahead to 2025, our investment forecast notes several factors likely to continue a hospitable backdrop for bonds into the long term:

- Higher starting yields have greatly improved the risk-return trade-off in fixed income.

- Over the next decade, we expect 4.3%–5.3% annualized returns for both U.S. and global ex-U.S. currency-hedged bonds.

- Although we expect rate cuts to reduce the Fed’s policy rate to 4%, cuts beyond that would prove difficult, as any weakening of growth would have to be weighed against a potential inflation revival.

- While central banks are now easing monetary policy, we maintain our view that policy rates will settle at higher levels than in the 2010s. This environment sets the foundation for solid cash and fixed income returns over the next decade.

- The persistence of supply-side drivers (labor productivity and available labor) would support trend growth and thus, real rates. Alternatively, risks associated with geopolitics, global trade, and immigration policies could also keep rates high, due to inflation expectations.

Within this overall 2025 investment outlook, our U.S. equity view is more cautious—ultimately, high starting valuations will drag long-term returns down. Our structural theme holds even in a scenario where central banks briefly cut rates below neutral to allay temporary growth wobbles. Our forecast suggests the era of sound money—characterized by positive real interest rates—lives on.

Fixed income may serve an essential, yet nuanced role in your clients’ portfolios. Our fixed-income solutions help you construct portfolios designed to meet clients’ specific preferences and needs.

IMPORTANT: The projections and other information generated by the VCMM regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. Distribution of return outcomes from VCMM are derived from 10,000 simulations for each modeled asset class. Simulations as of November 8. 2024. Results from the model may vary with each use and over time. For more information, please see the important information slide.

PORTFOLIO SOLUTIONS

Fixed income solutions tailored to client needs

The way your clients process changing market conditions reflects specific needs, risk tolerances, and goals that also guide how you construct the fixed income portion of their individual portfolios. We’ve assembled these conceptual portfolios to guide how you align the appropriate fixed income opportunity with the power of behavioral coaching. Consider them as a launching point for how you can customize fixed income holdings according to your clients’ unique objectives.

HI Financial Services Mid-Week 06-24-2014