HI Market View Commentary 07-29-2024

Expectations are one to maybe two rate cuts – most likely a September or December ¼ point cut

GDP numbers last week estimate 1.9% actual 2.8%

Current market conditions are volatile because nobody knows

Last Three weeks the Nasdaq fell 8.5% – IS that enough of a pullback to start another leg higher?

Russel 2000 problems – Volume – They are smaller companies that can’t be directly invested in for returns, institutional investors don’t play in the kiddy sand box.

Cash we are creating large amounts of cash through put profits – Roll down the puts for a profit and have ATM for many stocks. DIS, UAA, F we will let the puts “put” the shares to someone at $14.50, SQ rolled down puts and added shares,

We still have profits in NVDA, MU, AAPL

Earnings – 160 companies this week = Means I am super busy running numbers

Presidency –

Republican = Pro Business, Lower Taxes, Oil/Nuclear Power Independence

Democrats = Pro Poor, More Government Programs/Handouts, Pro Education, Solar Power Independence https://www.crfb.org/papers/trump-and-biden-national-debt

Both Parties ran up the deficit = Obama ran the deficit up by 50% of when he started office

https://www.oaktreecapital.com/insights/memo/the-folly-of-certainty

The Folly of Certainty

The impetus for my memos can come from a wide variety of sources. This one was inspired by an article in The New York Times on Tuesday, July 9. What caught my eye were a few words in the sub-headline: “She doesn’t have any doubt.” The speaker was Ron Klain, a former Biden chief of staff. The subject was whether President Biden should continue to run for reelection. And the “she” was Jen O’Malley Dillon, Biden’s campaign chair. The article went on to quote her as having said, “Joe Biden is going to win, period,” in the days just before his June 27 debate against former President Donald Trump.

And, with that, I had the subject of this memo: not whether Biden will continue campaigning or drop out – or whether he’ll win if he continues – but rather how anyone can be without doubt. It’ll be another of my “shortie” memos given the uncertain shelf life of the Biden candidacy.

This choice of subject calls to mind another time I heard a highly credentialed person express absolute certainty. In that case, an acknowledged expert in foreign affairs told a group I was part of there was “a 100% probability that the Israelis would ‘take out’ Iran’s nuclear capability before year-end.” He seemed like a genuine insider, and I had no reason to doubt his word. Yet, that was 2015 or ’16, and I’m still waiting for “before year-end” to come around (in his defense, he didn’t say which year).

As I indicated in my memo The Illusion of Knowledge (September 2022), there’s no way a macro-forecaster can produce a forecast that correctly incorporates all the many variables that we know will affect the future as well as the random influences about which little or nothing can be known. It’s for this reason, as I’ve written in the past, that investors and others who are subject to the vagaries of the macro-future should avoid using terms such as “will,” “won’t,” “has to,” “can’t,” “always,” and “never.”

Politics

When the 2016 presidential election rolled around, there were two things about which almost everyone was certain: (a) Hillary Clinton would win but (b) if by some quirk of fate Donald Trump were to win, the stock market would collapse. The least certain pundits said Clinton was 80% likely to win, and the estimates of her probability of victory ranged upward from there.

And yet, Trump won, and the stock market rose more than 30% over the next 14 months. The response of most forecasters was to tweak their models and promise to do better next time. Mine was to say, “if that’s not enough to convince you that (a) we don’t know what’s going to happen and (b) we don’t know how the markets will react to what actually does happen, I don’t know what is.”

Even before the much-discussed presidential debate of three weeks ago, no one I know expressed much confidence regarding the outcome of the coming election. Today, Ms. O’Malley Dillon would likely soften her position regarding the certainty of a Biden victory, explaining that she was blindsided by the debate result. But that’s the point! We don’t know what’s going to happen. Randomness exists.

Sometimes things go as people expected, and they conclude that they knew what was going to happen. And sometimes events diverge from people’s expectations, and they say they would have been right if only some unexpected event hadn’t transpired. But, in either case, the chance for the unexpected – and thus for forecasting error – was present. In the latter instance, the unexpected materialized, and in the former, it didn’t. But that doesn’t say anything about the likelihood of the unexpected taking place.

Macro Economics

In 2021, the U.S. Federal Reserve held the view that the bout of inflation then underway would prove “transitory,” which it has subsequently defined as meaning temporary, not entrenched, and likely to self-correct. I think the Fed might have been proved right, given enough time. Inflation might have retreated of its own accord in three or four years, after (a) the Covid-19 relief funds that caused the surge in consumer spending were spent down and (b) the global supply chain returned to its normal operations. (However, not slowing the economy would have brought the risk that inflationary psychology might take hold in those 3-4 years, necessitating even stronger action.) But because the Fed’s view wasn’t borne out in 2021 and waiting longer was untenable, the Fed was forced to embark on one of the fastest programs of interest rate increases in history, with profound implications.

In mid-2022, there was near certainty that the Fed’s rate increases would precipitate a recession. It made sense that the dramatic increase in interest rates would shock the economy. Further, history clearly showed that major central bank tightening has almost always led to economic contraction rather than a “soft landing.” And yet, no recession has materialized.

Instead, late in 2022, the consensus among market observers shifted to the view that (a) inflation was easing, and this would permit the Fed to start cutting interest rates, and (b) rate cuts would enable the economy to avoid recession or ensure that any contraction would be mild and short-lived. This optimism ignited a stock market rally in late 2022 that persists today.

And yet, the anticipated rate reductions in 2023 that undergirded the rally didn’t transpire. Then, in December 2023, when the “dot plot” of Fed officials’ views called for three interest rate cuts in 2024, the optimists driving the market doubled down, pricing in an expectation of six. Inflation’s stubbornness has precluded any rate cuts thus far, with 2024 more than half over. Now the consensus has coalesced around the idea of a first cut in September. And the stock market keeps hitting new highs.

The optimists today would likely say, “We were right. Look at those gains!” But, regarding interest rate cuts, they were simply wrong. For me, all this does is serve as another reminder that we don’t know what’s going to happen or how markets will react to what does happen.

Conrad DeQuadros of Brean Capital, my favorite economist (how’s that for an oxymoron?), has supplied an interesting tidbit for this memo on the subject of economists’ conclusions:

I use the Philly Fed’s Anxious Index (the probability of a decline in real GDP in the upcoming quarter) as an indicator that a recession has ended. By the time more than 50% of the economists in the survey project a decline in real GDP in the coming quarter, the recession is over or close to being over. (Emphasis added)

In other words, the only thing worthy of certainty is the conclusion that economists shouldn’t be expressing any of it.

Markets

The rare person who in October 2022 correctly predicted that the Fed wouldn’t cut interest rates over the next 20 months was absolutely right . . . and if that prediction kept them out of the market, they’ve missed out on a gain of roughly 50% in the Standard & Poor’s 500 index. The rate-cut optimist, on the other hand, was absolutely wrong about rates but is likely much richer today. So, yes, market behavior is very tough to gauge correctly. But I’m not going to take time here to catalog the errors of market savants.

Instead, I’d like to focus on why so many market forecasts fail. The performance of economies and companies might tend toward predictability given that the forces governing them are somewhat . . . shall I say . . . mechanical. In these areas, one might say “if A, then B” with some degree of confidence. Predictions here might, therefore, have some chance of being correct, albeit that’s mostly the case when trends continue unabated and extrapolation works.

But markets swing more than economies and companies. Why? Because of the importance and unpredictability of market participants’ psyches or emotions. Thanks to further help from Conrad DeQuadros, I can illustrate the greater variability of markets, as follows:

| 40-Year Standard Deviation of Annual Percentage Changes | |

| GDP | 1.8% |

| Corporate profits | 9.4 |

| S&P 500 price | 13.1 |

Why is it that stock prices rise and fall so much more than the economies and companies that underlie them? And why is it that market behavior is so hard to predict and often seems unconnected to economic events and company fundamentals? The financial “sciences” – economics and finance – assume that each market participant is a homo economicus: someone who makes rational decisions designed to maximize their financial self-interest. But the crucial role played by psychology and emotion often causes this assumption to be mistaken. Investor sentiment swings a great deal, swamping the short-run influence of fundamentals. It’s for this reason that relatively few market forecasts prove correct, and fewer still are “right for the right reason.”

* * *

Today, pundits are making all sorts of predictions about the upcoming presidential election. Many of their conclusions seem well-reasoned and even persuasive. We hear and read statements from those who believe Biden should and shouldn’t drop out; those who think he will and won’t; those who think he can win if he stays in the race; and those who think he’s sure to lose. Obviously, intelligence, education, access to data, and powers of analysis can’t be sufficient to produce correct forecasts. Many of these commentators possess these attributes, but clearly, they won’t all be right.

Over the years, I’ve often cited the wisdom of John Kenneth Galbraith. It’s he who said, “There are two kinds of forecasters: those who don’t know, and those who don’t know they don’t know.” I find myself using this quote all the time. Another of my favorite Galbraith quotes is from his book A Short History of Financial Euphoria. In describing the reasons for “speculative euphoria and programmed collapse,” he discusses two factors “little noted in our time or in past times. One is the extreme brevity of the financial memory.” I often cite this factor, too.

But I don’t remember ever writing about his second factor, which Galbraith says is “the specious association of money and intelligence.” When people get rich, others take that to mean they’re smart. And when investors succeed, it’s often assumed their intelligence can lead to similarly good results in other fields. Further, successful investors often come to believe in the strength of their own intellect and opine about fields with no connection to investing.

But investors’ success can be the result of a string of lucky breaks or a propitious environment, rather than any special talents. They may or may not be intelligent, but often they don’t know any more than most others about subjects outside of investing. Nevertheless, many are unsparing with their opinions, and those opinions often are highly valued by the general populace. That’s the specious part. And today we find some of them speaking with conviction on all sides of the issues related to the election.

A lot has been said about those who express certainty. We all know people we’d describe as “often wrong but never in doubt.” This reminds me of another of my favorite quotes, one that’s attributed (perhaps tenuously) to Mark Twain: “It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so.”

Back in mid-2020, when the pandemic seemed to have become a more or less understood phenomenon, I slowed the pace of my memo writing from the one-a-week pattern of March and April. In May, I took the opportunity for two non-Covid-related memos titled Uncertainty and Uncertainty II, in which I devoted a significant amount of space to the subject of intellectual humility. While these memos were on one of my favorite topics, they generated little response. So, I’ll quote a bit from Uncertainty and hopefully give you reason to look back at them.

Here’s part of the article that first brought the subject of intellectual humility to my attention:

As defined by the authors, intellectual humility is the opposite of intellectual arrogance or conceit. In common parlance, it resembles open-mindedness. Intellectually humble people can have strong beliefs, but recognize their fallibility and are willing to be proven wrong on matters large and small. (Alison Jones, Duke Today, March 17, 2017)

. . . To put it simply, intellectual humility means saying “I’m not sure,” “The other person could be right,” or even “I might be wrong.” I think it’s an essential trait for investors; I know it is in the people I like to associate with. . . .

No statement that starts with “I don’t know but . . .” or “I could be wrong but . . .” ever got anyone into big trouble. If we admit to uncertainty, we’ll investigate before we invest, double-check our conclusions and proceed with caution. We may sub-optimize when times are good, but we’re unlikely to flame out or melt down. On the other hand, people who are sure may dispense with those things, and if they’re sure and wrong, as the Twain quote suggests, the outcome can be catastrophic. . . .

. . . maybe Voltaire said it best 250 years ago: Doubt is not a pleasant condition, but certainty is absurd.

There simply is no place for certainty in fields that are influenced by psychological fluctuations, irrationality, and randomness. Politics and economics are two such fields, and investing is another. No one can predict reliably what the future holds in these fields, but many people overrate their ability and attempt to do so nevertheless. Eschewing certainty can keep you out of trouble. I strongly recommend doing so.

P.S.: Last summer’s Grand Slam tennis tournaments provided the inspiration for my memo Fewer Losers, or More Winners? Similarly, this past Saturday’s women’s final match at Wimbledon has provided a snippet for this memo. Barbora Krejcikova prevailed over Jasmine Paolini to win the women’s title. Before the tournament, bettors considered Krejcikova a 125-to-1 shot. In other words, they were sure she wouldn’t win. The bettors may have been right to doubt her potential, but it seems they shouldn’t have been quite so certain in making their predictions.

And speaking of the unpredictable, I can’t fail to mention the recent attempt on Donald Trump’s life, an event that could well have had a more grave and impactful result. Even now that it has happened and President Trump has escaped serious injury, no one can state with certainty how it will impact the election (though at present it appears to bolster Trump’s prospects) or the markets. So, if anything, it reinforces my bottom line: making predictions is largely a loser’s game.

July 17, 2024

LEGAL INFORMATION AND DISCLOSURES

This memorandum expresses the views of the author as of the date indicated and such views are subject to change without notice. Oaktree has no duty or obligation to update the information contained herein. Further, Oaktree makes no representation, and it should not be assumed, that past investment performance is an indication of future results. Moreover, wherever there is the potential for profit there is also the possibility of loss.

This memorandum is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. Oaktree Capital Management, L.P. (“Oaktree”) believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.

https://www.briefing.com/the-big-picture

The Big Picture

Last Updated: 26-Jul-24 15:45 ET | Archive

Follow the bouncing polls

It is not a long time between now and November 5, but we venture to guess that it might feel like an eternity for the market.

What is so meaningful about November 5? That is the first Tuesday in November, which means it is Election Day. We can only hope that there is a clear-cut outcome that night in the race for president.

There is some writing on the wall, however, that suggests that might not be the case. That writing is all over the polling data.

And the Nominee Is…

Briefing.com does not take positions in the market, we do not manage money, and we do not hold a political bias. Never have and we’re not about to start now.

Party loyalists have their reasons for favoring their candidate, and time will tell that independents have their reasons, too. We know for certain that former President Trump is the Republican nominee for president and that Senator J.D. Vance (R-OH) is the Republican nominee for vice president.

Until a week ago, President Biden and Vice President Harris were going to be the Democratic contenders. That all changed after President Biden dropped out of the race, bowing reportedly to party pressure to do so. In conjunction with that decision, he endorsed Vice President Harris for president.

An endorsement is not a nomination, but it is looking highly probable that Vice President Kamala Harris will be the Democratic Party’s nominee for president. Who her running mate will be is still very much up in the air.

The Democratic National Convention is going to be held August 19-22 in Chicago. A formal nomination process will take place there.

Pollsters, understandably, are not waiting for that formal process to be conducted. Heck, they were already measuring voters’ feelings about a Trump-Harris matchup before President Biden dropped out of the race.

That is no longer hypothetical. Their canvassing with respect to the presidential race now revolves squarely around voters’ positions/feelings about former President Trump and Vice President Harris.

Don’t Forget about Congress

RealClear Politics does an excellent job of aggregating the polling data. Readers should bookmark their page to stay on top of the polling data, which also includes key insight on Congressional races.

The battle for control of Congress also has the makings of being a tight race based on the latest polling data. While the presidential race will command most of the media’s attention, the Congressional vote should not be overlooked.

A presidential candidate can make a lot of claims about what they are going to do in office, but turning their fiscal policy into law requires legislation that is the domain of Congress.

It becomes a lot harder for a sitting president to get major fiscal policies enacted, as they envision, if their party does not control both houses of Congress. Conversely, the path to approval becomes easier when they have a mandate (i.e., their party controls both houses of Congress).

This is worth noting, knowing that the tax cuts enacted in 2017 under the Trump Administration expire at the end of 2025.

Currently, Democrats hold 47 seats in the Senate, Republicans hold 49 seats, and Independents, all of whom caucus with the Democrats, hold four seats. For all intents and purposes, then, the makeup is viewed as a 51-49 split in favor of the Democrats. The vice president casts any tie-breaking vote in the Senate.

There are 34 Senate seats up for election on November 5. Most of those seats are deemed “secure,” which is to say the incumbent, or the candidate for the party currently holding a Senate seat, is widely expected to win their election. Seven races, though, are considered to be a toss-up, and all of those seats (Arizona, Michigan, Montana, Nevada, Ohio, Pennsylvania, and Wisconsin) are currently held by Democrats.

In the House of Representatives, all 435 seats are up for election on November 5. The current composition of the House features 220 Republicans, 212 Democrats, and three vacancies, so a slight majority for Republicans.

According to the nonpartisan Cook Political Report, 193 Republican seats are considered to be solidly Republican in the coming election, nine more seats are likely to favor Republican candidates, and eight races are apt to lean Republican.

On the Democrat’s side of the aisle, 173 seats are deemed to be solidly Democrat, whereas 16 more seats are likely to favor Democrat candidates, and 14 races are apt to lean Democrat.

That leaves 22 seats that are considered to be toss-ups where either party has a good chance of winning.

An Important Margin of Error

In terms of the presidential polls, 19 polling results have been released since July 5. According to the aggregation by RealClear Politics, former President Trump came out ahead of Vice President Harris in 13 of them; meanwhile, Vice President Harris came out ahead in four of them, two of which were conducted before President Biden had dropped out of the race. The two presidential candidates were tied in two of the polls.

The edge former President Trump had over Vice President Harris exceeded the margin of error in five of the polls. In the four polls giving an edge to Vice President Harris, her spread over former President Trump was equal to, or less than, the margin of error in each of them.

**RV = registered voters

**LV = likely voters

Altogether the latest aggregation of polls conducted between July 5 and July 24 show former President Trump leading Vice President Harris by an average of 1.9 points. The average margin of error for the polls is 2.7.

In other words, the average lead former President Trump has over Vice President Harris is within the average margin of error, meaning it might not be a lead at all — or it could be an even bigger lead than it appears.

The takeaway point is that it is anyone’s guess, which is to say there is ample uncertainty at this juncture about the outcome of the presidential race, which could even be swayed by the presence of Independent Robert F. Kennedy, Jr., although he is currently on the ballot in only nine states.

What It All Means

How many times have you heard that the market doesn’t like uncertainty? How many times have you heard that the market has the ability to climb a wall of worry? Probably too many to count. Life is inherently uncertain and yet the Dow Jones Industrial Average, Nasdaq Composite, and S&P 500 all hit record highs earlier this month.

This political uncertainty — not to mention the geopolitical uncertainty — is a bit of a different animal, because elections dictate the path of policymaking.

There promises to be ample political drama between now and November 5, and maybe even after November 5. Part of the drama each week will be the latest poll results related to the presidential race.

The market has preconceived notions about who would be the more market-friendly candidate, but of course the market isn’t Republican or Democrat. Rather, it is comprised of Republicans, Democrats, Independents, Libertarians, Greens, and the politically disinterested.

Accordingly, there will be reasonable theories as to why the market, and certain industry groups, are moving one way or the other on the latest polling data.

If former President Trump and Vice President Harris are both unable to escape the confines of a lead that is within the average margin of polling error, the market seems unlikely to be able to escape the uncertainty associated with that dynamic.

It is not a long time between now and November 5, but there is a lot of political wood to chop between now and then, which is why the market is apt to remain choppy in the interim as it follows the bouncing polls in a tightly contested race.

—Patrick J. O’Hare, Briefing.com

Earnings dates:

AAPL 08/01 AMC

BA 07/31 BMO

BABA 08/08 BMO

BIDU 08/22 BMO

DG 08/29 est

DIS 08/07 BMO

JCI 08/01 est

META 07/31 AMC

MU 09/25 est

O 08/05 AMC

SQ 08/01 AMC

TGT 08/21 BMO

UAA 08/09 est

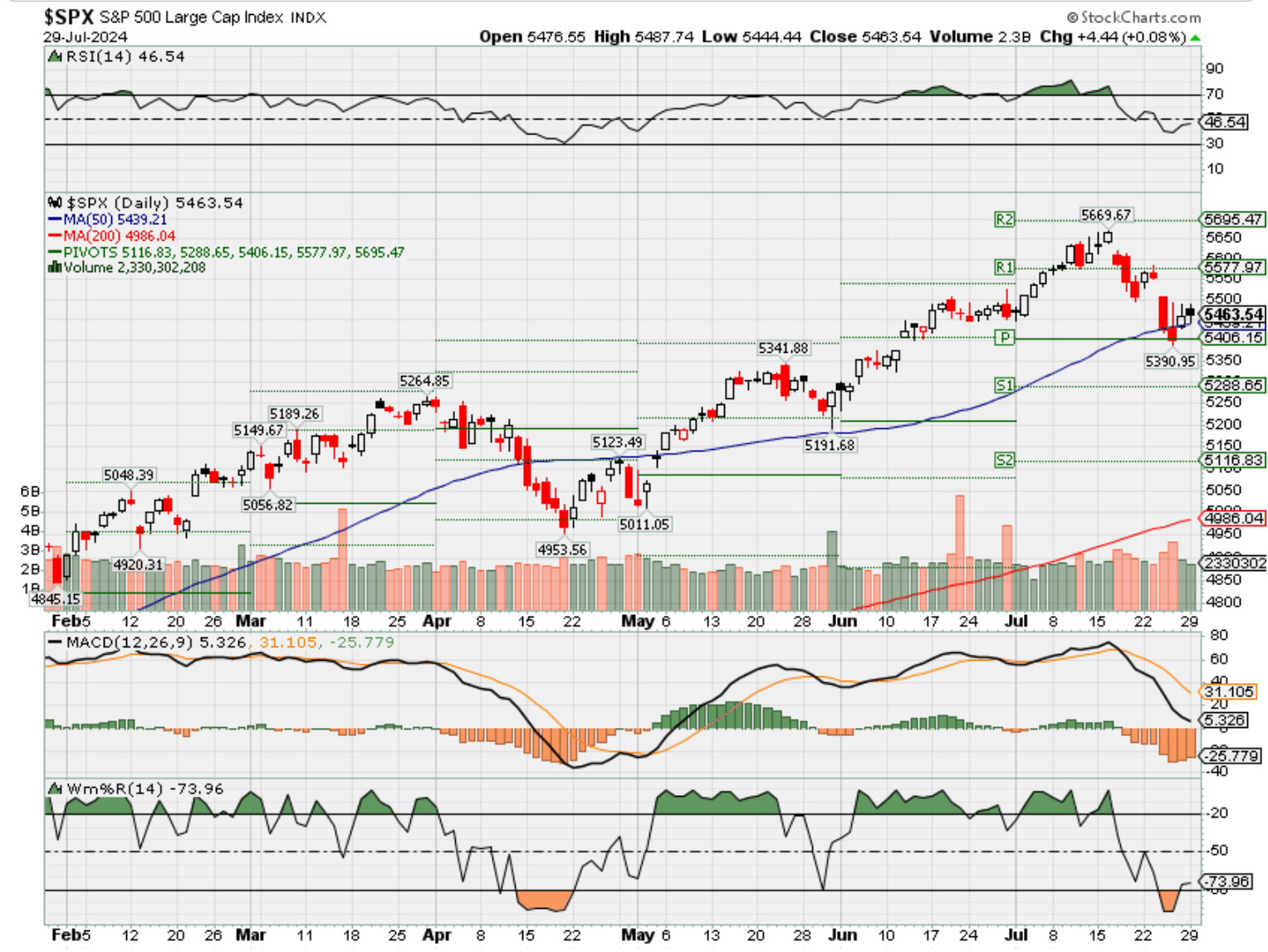

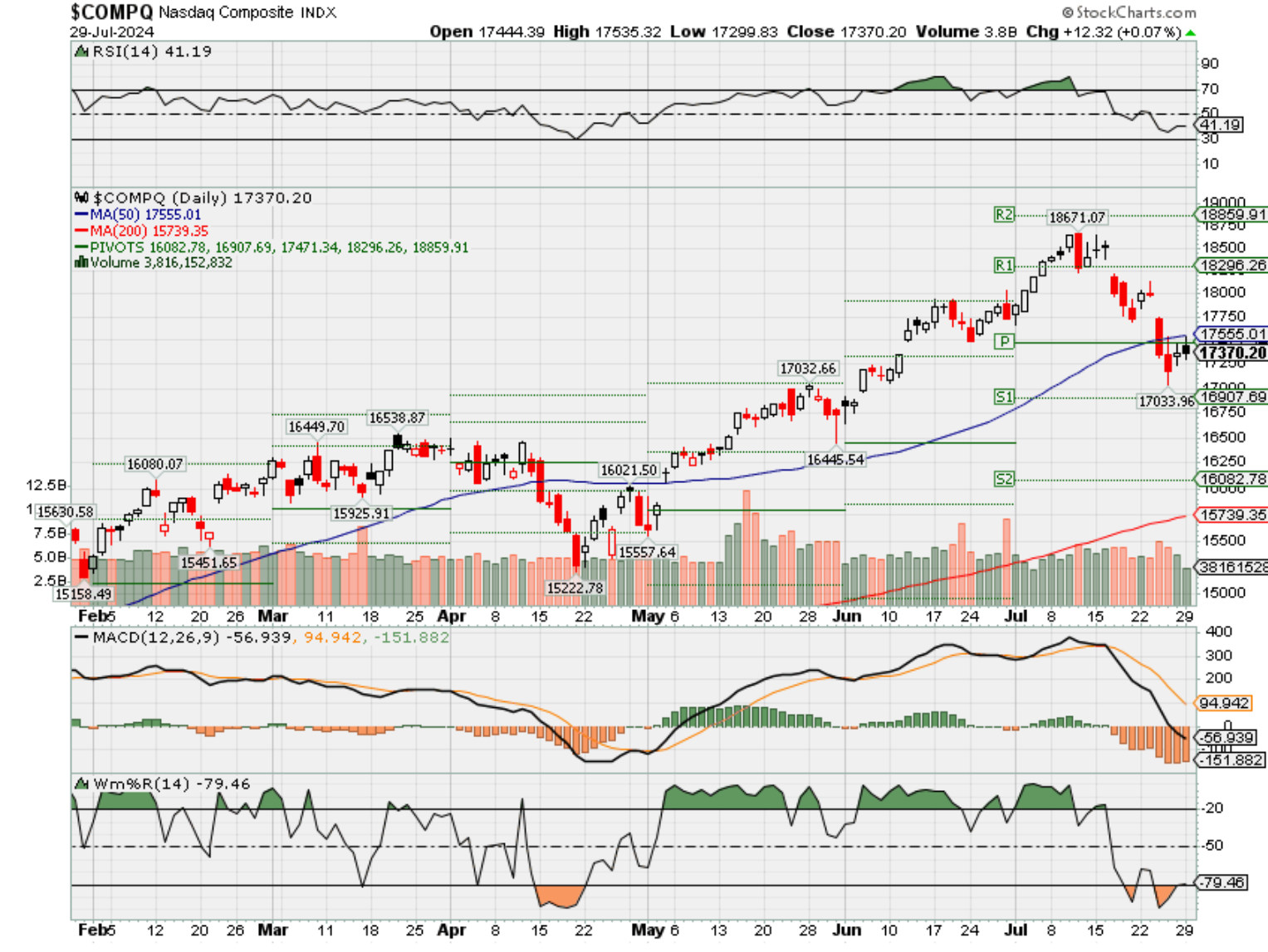

Where will our markets end this week?

Lower

DJIA – Bullish

SPX – Bearish

COMP – Bearish

Where Will the SPX end July 2024?

07-29-2024 -2.00%

07-22-2024 +2.00%

07-15-2024 -2.00%

07-08-2024 -2.00%

07-01-2024 -2.00%

Where Will the SPX end August 2024?

07-29-2024 -2.00%

Earnings:

Mon: MCD, CHK, FLS, RMBS,

Tues: BP, GLW, JBLU, MRK, PFE, PSX, DENN, EA, FSLR, SWKS, SBUX, AMD, FSLR, MSFT

Wed: GOLD, CLH, DD, GEMN, GEHC, KHC, MAR, TMUS, ALMT, BALY, CHRW, CAKE, EBAY, ETSY, MGM, NE, PDM, QCOM, WDC, BA, META

Thur: ADT, BUD, COP, CROX, CMI, GWW, HTZ, SIRI, WEN, BZH, CLX, COIN, DASH, DKNG, LOCO, GDDY, INTC, ROKU, TWLO, X, D, LAD, AMZN, AAPL, SQ

Fri: CVX, XOM, FLR, AMC

Econ Reports:

Mon:

Tue FHFA Housing Market index, S&P Case-Shiller Index, Consumer Confidence,

Wed: MBA, ADP Employment, Pending Home Sales, FOMC Rate Decision,

Thur: Initial Claims, Continuing Claims, ISM Manufacturing Index, Productivity, Unit Labor Costs, Construction Spending,

Fri: Average Workweek, Non-Farm Payroll, Private Payroll, Unemployment Rate, Hourly Earnings, Factory Orders

How am I looking to trade?

Protection On Everything

www.myhurleyinvestment.com = Blogsite

info@hurleyinvestments.com = Email

Questions???

Can Boeing get back to its glory days?

PUBLISHED THU, JUL 18 20246:00 AM EDTUPDATED SUN, JUL 21 20249:33 AM EDT

KEY POINTS

- Boeing’s leaders say they have charted a path forward to stamp out safety and manufacturing flaws on its best-selling planes.

- Plans include better oversight, improved safety and manufacturing procedures, more robust worker training, and buying back a key supplier.

- Industry watchers and insiders say a string of decisions stretching back decades led to the problems at the longtime touchstone of American manufacturing quality and innovation.

Boeing executives spent years after two fatal 737 Max crashes trying to convince Wall Street, regulators, airlines and the flying public that they had an eagle eye on quality, reliability and safety.

Then on Jan. 5, about six minutes and 16,000 feet into a packed flight out of Portland, Oregon, a door plug blew out of a nearly new Boeing 737 Max 9. The panel was missing key bolts that hold it in place, which the company had removed to fix damaged rivets, according to early accident reports.

No one was seriously injured, but the harrowing flight jolted Boeing’s leaders back into crisis mode. It also reignited scrutiny and skepticism from the same groups the iconic plane-maker spent years trying to win back after the two Max crashes.

Now Boeing’s leaders say they have charted a path forward to fix the company: Better oversight, improved safety and manufacturing procedures, and more robust training for workers, many of them new hires after pandemic-era buyouts and layoffs of thousands of employees.

Boeing this month unveiled a long-awaited deal to buy back its troubled fuselage supplier, Spirit AeroSystems, in a bid to help stamp out production flaws.

A week later, Boeing said it reached a deal with the Justice Department to plead guilty to a federal charge of conspiracy to defraud the U.S. government tied to the fatal 737 Max crashes. Attorneys representing crash victims’ families blasted the agreement as a “sweetheart” deal. If approved by a federal judge, it would allow Boeing to avoid a potentially lengthy and costly criminal trial, though it would also brand Boeing as a felon.

“This past January, the facade quite literally blew off the hollow shell that had been Boeing’s promises to the world,” Sen. Richard Blumenthal, D-Conn., said in testimony for a Senate panel hearing he called last month, where Boeing CEO Dave Calhoun was roasted by lawmakers.

Industry watchers and insiders say a string of decisions stretching back decades — from a 1997 merger to outsourcing — led to the problems at the longtime touchstone of American manufacturing quality and innovation. Boeing employs some 170,000 people, and its products have landed everywhere from the Maldives to the moon.

Even with its road map in hand, fixing its problems and restoring Boeing’s reputation will take years — and it won’t be cheap.

And Boeing still has plenty of people to convince.

Boeing hasn’t posted an annual profit since 2018, and the plane maker’s shares have tumbled about 30% this year while the broader market rallied. Its stock closed at a high of $440.62 in March 2019, days before the second Max crash. It now trades closer to $185 per share.

Boeing finance chief Brian West told investors in May that the company expects to burn, rather than generate, cash this year, some $8 billion in the first half of 2024. It reports quarterly results on July 31.

“This company is more important than a few quarters of Wall Street,” Aengus Kelly, CEO of aircraft leasing giant AerCap, a major Boeing customer, said in an interview in the spring. “It has to be nurtured and rebuilt.”

Boeing will be back on the global stage next week during the biennial Farnborough Airshow in the United Kingdom, one of the world’s largest aircraft shows. But the manufacturer will have a muted presence: It’s not sending its yet-to-be-certified 777X, 737 Max 7 or Max 10 planes as Boeing employees focus on the fixing problems at home rather than showcase its new planes as it did during past air shows.

Delayed deliveries

Boeing began 2024 fresh from a surge in annual jetliner sales and a jump in deliveries, welcome tallies that appeared to show the company was turning a corner after the fatal dives of two 737 Maxes in 2018 and 2019 that killed all 346 people on the flights.

But the Jan. 5 door plug blowout on Flight 1282, operated by Boeing’s crosstown customer Alaska Airlines, brought a swift response from regulators. The Federal Aviation Administration barred Boeing from increasing output of its Max planes and stepped up hands-on inspections at production plants. The FAA said in March that its audit found “non-compliance issues in Boeing’s manufacturing process control, parts handling and storage, and product control.”

Its production limitations have exacerbated delivery delays for Boeing customers, a slowdown that’s impacting its commercial jet business, as airlines pay the bulk of a plane’s price when they receive it. That division accounted for more than 43% of Boeing’s nearly $78 billion in revenue last year.

In the first half of 2024, Boeing delivered 175 airplanes, compared with the 323 aircraft that Airbus handed over during the same period. The two companies dominate the commercial jet market.

Leaders at the top of major airlines from Emirates to Southwest have aired their frustration with the jet maker as deliveries run behind schedule. Southwest, United and American have blamed slowdowns in hiring and changed flight plans on Boeing’s delays.

“Boeing needs to become a better company,” Southwest CEO Bob Jordan said at a JPMorgan industry conference in March, an uncharacteristically strong comment from the leader of the all-Boeing 737 airline.

Even if planes arrive late, compensation doesn’t often make up for the shortfall of jets.

“I’m not in the compensation business. I’m the airline business,” Etihad Airways CEO Antonoaldo Neves said in an interview.

Why the Boeing 737 Max has been such a mess

Tight supply at both Boeing and Airbus makes shifting orders over to the European company nearly impossible. Both companies are sold out of narrow-body planes through almost the end of the decade. Boeing has an order book of more than 5,400 jetliners, after accounting adjustments, while Airbus has about 8,000 unfilled orders.

And Airbus isn’t on solid ground either, warning customers and investors last month that supply chain problems will slow its planned ramp up in production and slow deliveries.

Earlier this year as airline executives’ patience wore thin, they sought meetings with Boeing’s board chairman, people familiar with the matter said.

Shortly afterward, Boeing in March announced a leadership shake-up, with the head of its all-important commercial airplane unit replaced. CEO Calhoun, an alumnus of General Electric and Blackstone, said he would step down by the end of the year. Boeing replaced its chairman, too, installing ex-Qualcomm CEO Steve Mollenkopf.

Boeing hasn’t yet named a replacement for Calhoun. The CEO of Spirit AeroSystems, Pat Shanahan, who previously worked at Boeing and served as former deputy secretary and acting secretary of defense under former President Donald Trump, is considered a strong contender.

Across the airline industry, executives publicly and privately say they would rather Boeing take the time to fix problems than face prolonged uncertainty over when new planes will be delivered.

Long history

The 108-year old Boeing has a firm place in American history. Its bombers were crucial in World War II. It has built presidential aircraft. Former Presidents Barack Obama and Donald Trump have each held events at Boeing 787 Dreamliner factories. And in space, a Boeing-built rocket propelled Apollo 11 to the moon in 1969.

Most of the general public knows Boeing as the company to usher in the jet age. It designed and launched four aircraft in just over a decade, including the first 737.

The narrow-body plane was soon dwarfed by Boeing’s groundbreaking and more glamorous jumbo jet, the 747, which could fit more than 500 people, and in some configurations, a piano bar. The 737 was dubbed “Baby Boeing” and went on to become the company’s bestseller, helping to make Boeing the largest U.S. exporter. It has built more than 11,000 of the 737s to date.

“Without Boeing, the world is a worse place,” AerCap’s Kelly said.

But within a five-month span in 2018 and 2019, two Max 8 planes crashed: one in Indonesia operated by Lion Air that plunged into the Java Sea, killing the 189 people on board; and one operated by Ethiopian Airlines that crashed shortly after takeoff from Addis Ababa, killing the 157 people on that flight.

Pilots in those Boeing planes fought against a flight-control system, the Maneuvering Characteristics Augmentation System, that pushed the nose of the planes downward repeatedly. The Department of Justice later alleged the company misled the FAA about the system, the charge to which Boeing ultimately agreed to plead guilty.

Last year, it looked like Boeing was back on a better footing.

“I have heard those outside our company wondering if we’ve lost a step. I view it as quite the opposite,” Calhoun said in note to employees last October.

Months later, the powerful blast from the Alaska Airlines door plug blowout ripped off head rests, seatbacks and the first officer’s headset, leaving a gaping hole in row 26. The incident terrified passengers and exposed the most serious in a series of quality control issues on Boeing jets. Previous issues included mis-drilled holes and incorrect spacing on some of Boeing fuselages.

The manufacturer’s production portfolio includes a host of jets that are regularly flown commercially around the world: the workhorse 737, the wide-body 787 Dreamliner, and soon, once approved by regulators, the 777X.

And while production flaws make headlines, Boeing jets continue to carry travelers safely around the world, with more than 13,000 at the end of last year. The company has a 45% market share of commercial jets currently flying, according to AeroDynamic Advisory.

Across all of its divisions, its customers also include the U.S. and foreign militaries, and NASA — and some of those units haven’t been without issue either.

“Our airplanes have carried the equivalent of more than double the population of the planet,” Calhoun said in testimony to a Senate panel last month for a hearing titled “Boeing’s Broken Safety Culture.”

“Getting this right is critical for our company, for the customers who fly our planes every day, and for our country,” he said. He apologized during the hearing to the family members of the Lion Air and Ethiopian crash victims, as they held posters with pictures of lost loved ones.

Boeing CEO Dave Calhoun apologizes to families of crash victims

Cost-cutting proves costly

Critics say a yearslong push to reward Boeing shareholders and lower costs came at the expense of building totally new aircraft, in favor of updating older models. Boeing also outsourced production of key parts to suppliers that it increasingly put under pressure to deliver, exposing the supply chain to potential flaws.

United CEO Scott Kirby told CNBC in January that he believes the issues date back to Boeing’s merger with competing airplane manufacturer McDonnell Douglas in 1997. The tie-up is often cited as a turning point for Boeing that replaced its once engineering-led culture with a greater focus on returns.

From 2010 to 2019, Boeing spent $68 billion on stock buybacks and dividends, according to Melius Research analyst Rob Spingarn.

“This is a long time building,” Kirby said.

In 2001, Boeing moved its corporate headquarters from its original home in Seattle to Chicago, farther away from the factory floors where it had built aircraft since the early 20th century. In 2022, it moved headquarters again to Arlington, Virginia.

In 2005, Boeing sold its Wichita division that makes fuselages for many of its planes to a private equity firm for just under $1 billion. That spinoff would eventually become Spirit AeroSystems, which Boeing is now buying back for about $4.7 billion plus debt.

And in 2020, Boeing said it would consolidate 787 Dreamliner production in South Carolina, more than 2,400 miles away from its other manufacturing facilities in Washington state, including where the Dreamliners were previously built. It also outsourced parts production to a network of suppliers.

Those moves have been put under a microscope in recent years as Boeing disclosed recurring production flaws. Allegations from whistleblowers at the company and at Spirit have claimed Boeing was cutting corners in production.

Why Boeing wants to buy back Spirit AeroSystems

Calhoun, when asked about outsourcing production to Spirit, told CNBC in January: “Did it go too far? Yeah … probably did, but now it’s here and now I gotta deal with it.”

Flaws on its planes have cost Boeing billions of dollars due to periods of production drops, delivery pauses and compensation to customers.

Turning a page

Boeing does say that it’s on the right track.

For one, it’s been forced to slow production of its planes. While painful in the near term because it drives up costs and deprives the company of new planes to hand over to customers, executives say it’s the way to make sure manufacturing flaws don’t reappear.

Jefferies estimates Boeing produced about 24 Max jets a month in the second quarter and could move to roughly 35 a month in the last three months of the year. Boeing has said it aims to increase rates to about 50 Max planes a month in the next few years.

It’s also brought employees into the recovery effort. The company has held so-called “stand-downs” at its factories to pause work and discuss problems on the line.

And its plea deal with the DOJ, if approved by a judge in the coming weeks, could allow the company to settle a federal probe with a roughly $244 million fine and a probationary period of three years, during which time an independent monitor would oversee quality control, and other conditions.

Boeing’s CEO Dave Calhoun and chief engineer Howard McKenzie turn to face those who lost loved ones in fatal crashes as they testify before a Senate Homeland Security and Governmental Affairs Committee Investigations Subcommittee hearing on the safety culture at Boeing, on Capitol Hill in Washington, U.S., June 18, 2024.

Kevin Lamarque | Reuters

“We are taking comprehensive action today to strengthen safety and quality,” Calhoun said in his testimony before the Senate panel last month. “And, we know, as America’s premier aerospace manufacturer, this is what you and the flying public have every right to expect from us.”

Goldman Sachs aerospace analyst Noah Poponak said Boeing can “still make a product that’s a total marvel. If they can get their act together, I think their reputation can improve quickly.”

Promoting and building up the Boeing workforce will be key in the coming years, according to Alex Krutz, managing director of Patriot Industrial Partners, an aerospace consulting firm.

The company has more competition for new workers than in previous generations in the Seattle area, he said, because of rapid expansion of tech companies there in the past few decades, as well as engineering competition from the private space industry.

“Companies thrive or don’t based on leadership,” he said.

The rise and fall of the Boeing 747

The International Association of Machinists and Aerospace Workers, District 751, which represents some 30,000 Boeing technicians in Washington State and Oregon, is currently in contract negotiations with company, seeking more than 40% raises and a seat on Boeing’s board.

“We have more leverage than we’ve ever had in our history,” said Jon Holden, president of IAM District 751. “There’s massive demand for new airplanes.”

Some analysts say designing a new plane could help attract talent and set the company up for years to come, a project that was largely set to the backburner after the crashes.

The advice of Richard Aboulafia, an longtime aerospace analyst and a managing director at AeroDynamic Advisory is simple: “Begin a new program, and say, ‘We’re a company with a future.’”

Alphabet meets earnings expectations but misses on YouTube ad revenue

PUBLISHED TUE, JUL 23 202412:00 PM EDTUPDATED WED, JUL 24 20249:22 AM EDT

KEY POINTS

- Google parent company Alphabet reported earnings after the bell.

- Alphabet’s revenue was up 14% year over year, driven by search as well as cloud, which surpassed $10 billion in quarterly revenues and $1 billion in operating profit for the first time.

- The company reported ad revenue of $64.62 billion — up from $58.14 billion last year, showing that Google’s advertising business continues to grow after rising inflation and interest rates tightened marketing budgets in 2022 and 2023.

Alphabet beats on revenue and earnings

Google parent company Alphabet reported second-quarter results after the bell Tuesday that were in-line with analyst estimates on revenue and earnings, but missed on YouTube advertising revenue.

Alphabet shares were down about 2% in after-hours trading.

Here’s how the company did, compared with estimates from analysts polled by LSEG:

Earnings: $1.89 a share vs. $1.84 per share expected

Revenue: $84.74 billion vs. $84.19 billion expected

Here are other numbers Wall Street was watching:

- YouTube advertising revenue: $8.66 billion vs. $8.93 billion, according to StreetAccount

- Google Cloud revenue: $10.35 billion vs. $10.20 billion, according to StreetAccount

- Traffic acquisition costs (TAC): $13.39 billion vs. $13.54 billion, according to StreetAccount

Alphabet’s revenue was up 14% year over year, driven by search as well as cloud, which surpassed $10 billion in quarterly revenues and $1 billion in operating profit for the first time.

The company reported ad revenue of $64.62 billion — up from $58.14 billion last year, showing that Google’s advertising business continues to grow, though at a slower pace than in the first quarter, after rising inflation and interest rates tightened marketing budgets in 2022 and 2023.

While YouTube ad revenue missed estimates, it still grew to $8.66 billion compared to $7.66 billion in the year-ago quarter. Though it’s the largest video platform in the world, it faces increased competition from social video sites like TikTok.

Net income increased to $23.6 billion, or $1.89 per share, compared to $18.4 billion, or $1.44 per share, in the year-ago quarter.

The company’s “Other Bets” unit, which includes its self-driving car company Waymo, brought in $365 million, up from $285 million a year ago. Finance chief Ruth Porat announced on the company’s earnings call that Alphabet is committing a new $5 billion multiyear investment in Waymo.

During the second quarter, Alphabet saw a number of expansion updates, including for Waymo, which opened its service to all San Francisco users. The move was its second citywide rollout, following a 2020 debut in the Phoenix metropolitan area.

CEO Sundar Pichai said on the earnings call that Waymo is now making 50,000 weekly paid public rides, primarily in San Francisco and Phoenix.

“Our strong performance this quarter highlights ongoing strength in Search and momentum in Cloud,” Pichai said in the earnings release. “We are innovating at every layer of the AI stack. Our longstanding infrastructure leadership and in-house research teams position us well as technology evolves and as we pursue the many opportunities ahead.”

Ford shares tumble 13% after massive earnings miss

PUBLISHED WED, JUL 24 202412:00 PM EDTUPDATED THU, JUL 25 20246:47 AM EDT

KEY POINTS

- Ford Motor came in short of Wall Street’s second-quarter earnings expectations while beating on revenue, due to warranty costs that have plagued the automaker for several years now.

- The automaker increased its target for free cash flow but maintained its 2024 earnings guidance, disappointing some investors who had hoped for a hike.

- Ford CEO Jim Farley told investors Wednesday that his Ford+ restructuring plan remains on track to make the automaker more profitable.

DETROIT — Ford Motor came in short of Wall Street’s second-quarter earnings expectations while beating on revenue, due to warranty costs that have plagued the automaker for several years now.

The automaker increased its full-year target for free cash flow but maintained its 2024 earnings guidance, disappointing some investors who had hoped for a hike. Ford’s guidance for the year includes adjusted earnings before interest and taxes, or EBIT, of between $10 billion and $12 billion.

Shares of the automaker were down about 13% after markets closed. The stock closed Wednesday at $13.67 per share.

Here is how the company did, compared to estimates from analysts polled by LSEG:

- Earnings per share: 47 cents adjusted vs. 68 cents expected

- Automotive revenue: $44.81 billion vs. $44.02 billion expected

The Detroit automaker said its profitability was affected by increases in its warranty reserves used to pay for vehicle issues. The costs are related to vehicles for the 2021 model year or older, Ford Chief Financial Officer John Lawler said during a media briefing.

Ford said recent initiatives to improve quality and vehicle launches are paying off and are expected to help bring down future warranty costs.

“We’re making real progress in raising quality, lowering costs and reducing complexity across our entire enterprise,” Lawler said during a media briefing. “We’re making real progress on quality that will benefit us down the road.”

Lawler declined to disclose Ford’s total warranty cost for the second quarter but said it was $800 million more than the previous quarter.

Performance of several auto stocks in 2024.

Net income for the second quarter was $1.83 billion, or 46 cents per share, compared to $1.92 billion, or 47 cents per share, a year earlier. Adjusted EBIT declined 27% year over year to $2.76 billion, or 47 cents per share, compared to $3.79 billion, or 72 cents per share, during the second quarter of 2023.

Ford’s overall revenue for the second quarter, including its finance business, increased about 6% year over year to $47.81 billion.

Ford CEO Jim Farley told investors Wednesday that his Ford+ restructuring plan remains on track to make the automaker more profitable.

“We are absolutely a different company than we were three years ago,” Farley said during the company’s earnings call, noting the “remaking of Ford is not without growing pains.”

Ford’s traditional business operations, known as Ford Blue, earned $1.17 billion during the second quarter, while its Ford Pro commercial business earned $2.56 billion. Its “Model e” electric vehicle unit lost $1.14 billion from April through June.

The Ford+ plan initially focused heavily on EVs when it was announced in May 2021 during the company’s first investor day under Farley, who took over the helm of the automaker in October 2020. It has since shifted to focus more on customer choice and next-generation EVs to drive profits.

Farley said Ford’s “more realistic and sharpened” EV plan, including focusing on a small next-generation EV platform, will prove worthwhile for the company in the years ahead.

As of Wednesday’s close, Ford’s stock was up more than 10% this year, as pricing in the automotive industry has remained more resilient than expected, but some Wall Street analysts believe automaker profits may have peaked.

“We don’t see the second half being much different than the first half, or falling off,” Lawler said. “There’s going to be puts and takes in any half of the year … that was part of our guidance, and we’re planning on managing that.”

There was pressure on Ford to raise its guidance after crosstown rival General Motors raised its yearly guidance Tuesday for the second time this year.

GM’s second-quarter results also beat Wall Street’s top- and bottom-line expectations, but the automaker’s stock on Tuesday declined 6.4%.

Short seller Andrew Left of Citron charged with fraud by prosecutors, SEC

PUBLISHED FRI, JUL 26 20248:22 AM EDTUPDATED 36 MIN AGO

KEY POINTS

- Federal prosecutors criminally charged the well-known short seller Andrew Left with securities fraud related to allegedly using his public platform to illegally profit from manipulating stock market activity.

- Left and his firm Citron Capital also were separately charged in a civil fraud action by the Securities and Exchange Commission, which accused them of “engaging in a $20 million multi-year scheme to defraud followers by publishing false and misleading statements regarding his supposed stock trading recommendations.”

Federal prosecutors have criminally charged the activist short seller and analyst Andrew Left with securities fraud related to allegedly using his public platform to illegally profit to the tune of at least $16 million from manipulating stock market activity contrary to positions he presented to the public from 2018 through 2023.

Left, a 54-year-old Florida resident who has been a frequent guest commentator on CNBC and other business cable news channels, and his hedge fund Citron Capital also were separately charged in a related civil fraud action by the Securities and Exchange Commission.

That civil complaint in Los Angeles federal court accused Left and Citron of “engaging in a $20 million multi-year scheme to defraud followers by publishing false and misleading statements regarding his supposed stock trading recommendations.”

The action alleges fraudulent conduct relating to 23 companies on at least 26 separate occasions.

“Left bragged to colleagues that some of these statements [he made] were especially effective at inducing retail investors to trade based on his recommendations and said that it was like taking ‘candy from a baby,’” the SEC alleged in that complaint.

The companies identified in the criminal indictment as ones Left allegedly traded on in ways contrary to his public stances on their stock prices included Nvidia, Tesla, the social media company X, formerly known as Twitter, Meta, Roku, Beyond Meat, American Airlines, Palantir, XL Fleet, Invitae, General Electric, Namaste Technologies, and India Globalization Capital.

The indictment alleges that, among other things, “Left coordinated with hedge funds to disseminate short reports and information to be posted on Twitter, coordinated with hedge funds regarding the timing of publication, and enabled the hedge funds to trade in the Targeted Securities before the reports were disseminated.”

“In exchange for sharing his planned announcements with the hedge funds in advance of posting them publicly, the hedge funds paid defendant Left a portion of their trading profits,” the indictment says.

Left, who lives in Boca Raton, is expected to be arraigned in the next several weeks in Los Angeles federal court on the 19-count criminal indictment, the U.S. attorney’s office in L.A. said in a statement.

He declined to comment on the indictment and the SEC complaint when contacted by CNBC.

Left’s lawyer, James Spertus, in a statement, said, “Mr. Left is a publisher who has taken extraordinary steps to comply with all laws, and neither the [Department of Justice] nor the SEC allege that he ever once published information he believed was not true when published.”

“Instead, the DOJ and SEC allege that Mr. Left had a duty to disclose his private trading intentions when publishing truthful information, which is a defective theory for many reasons, including the fact that Mr. Left’s publications contain detailed disclosures written by sophisticated attorneys informing readers that Mr. Left is trading in the securities he writes about,” Spertus said.

The attorney also said the indictment and complaint threaten “the integrity of the securities markets and put the health of our financial system at risk by trying to silence a publisher of truthful information who also trades in the securities he writes about.”

“The allegations filed today should concern all investors because the publication of truthful information is critical to efficient markets,” Spertus said.

Akil Davis, the assistant director in charge of the FBI’s Los Angeles Field Office, in a statement, said, “Mr. Left’s presence on financial television networks and his significant online following provided him with a credible platform to allegedly disguise his intentions and manipulate the investing public for personal gain.”

The indictment says that Left used Citron’s online platform to comment on publicly traded companies and claim that their stock was incorrectly valued by the market, either too high or too low.

“Left’s recommendations often included an explicit or implicit representation about Citron’s trading position and a ‘target price,’ which defendant Left represented as his own view of the Targeted Security’s true value,” the indictment says.

“Left knew that his recommendations influenced investors’ decisions to buy or sell stock and thereby empowered him to manipulate the price of a Targeted Security,” the indictment said.

“By using the Citron Twitter Account to generate ‘catalysts’ — events with the ability to move stock prices — defendant Left profited from his advance knowledge that he was about to trigger such movements in the market.”

After using his influence to manipulate a stock’s price, Left “closed his positions to capitalize on the temporary price movement caused by his public statements,” the indictment alleges.

The indictment and SEC complaint give specific examples of Left’s alleged manipulation, and exploitation of his contacts with business media outlets, including CNBC.

The SEC complaint says that in May 2019, Left and Citron Capital had a short exposure in Beyond Meat, which meant they would profit if its stock price dropped.

Left’s other company, Citron Research, on May 17, 2019, issued a negative tweet on Beyond Meat, which recommended that readers sell the stock and assign it a target price of $65 per share, at a time when the stock was selling at about $87 per share.

″$BYND has become Beyond Stupid” and “We expect $BYND to go back to $65 on earnings,” that tweet said. “Despite his negative statements to the market, only 10 days before Left told a colleague that he thought the price of BYND would increase, stating “i think BYND goes to 100,’” the SEC said in its complaint.

Within seven minutes of the tweet, Left exited the majority of his short exposure to Beyond Meat, and Citron Research “completely covered its short positions within 12 minutes of the tweet,” the complaint said.

“Later that day, in advance of an article CNBC planned to release, a reporter emailed Left asking whether he still held a trading position in BYND. In response, Left stated that he ‘shorted some today,’” the complaint says.

“This statement was materially false and misleading because Left had exited the majority of his short exposure and Citron Capital had already sold all of its short exposure,” the complaint alleges. “Six minutes after this email exchange, Citron took additional short exposure in BYND, before the release of the CNBC article.”

“Within an hour, CNBC published an article titled ‘Short seller says Beyond Meat hype is ‘beyond stupid,’ places bet against the shares,’” the complaint says. “After the article was released, Citron exited this additional short exposure.”

Left, who previously lived in Beverly Hills, California, is charged in the indictment with one count of engaging in a securities fraud scheme, 17 counts of securities fraud and one count of making false statements to federal investigators.

If convicted, he would face a maximum possible sentence of 25 years in prison for the securities fraud scheme alone.

SEC accuses activist investor Andrew Left and Citron of making $20 million by misleading investors

SEC charges firm with allegedly selling stocks after recommending that readers of its website buy them

By Steve Gelsi

Follow

Last Updated: July 26, 2024 at 11:45 a.m. ET

The SEC has charged Andrew Left and Citron Capital with committing fraud by allegedly selling stocks after telling readers to buy them.PHOTO: SAUL LOEB/AGENCE FRANCE-

The U.S. Securities and Exchange Commission has charged activist short seller Andrew Left and his firm, Citron Capital LLC, with running a $20 million multiyear “scheme to defraud followers by publishing false and misleading statements regarding his supposed stock trading recommendations.”

The SEC has charged Left and Citron Capital with violating antifraud provisions of federal securities laws. The U.S. Justice Department’s fraud unit also announced charges against Left in a criminal investigation.

Citron Capital did not respond to an email from MarketWatch seeking comment.

The SEC charged Left with allegedly using the Citron Research website and related social-media platforms at least 26 times to publicly recommend long or short positions in 23 companies.

When the prices of the stocks moved an average of 12%, “Left and Citron Capital quickly reversed their positions to capitalize on the stock price movements,” the SEC alleged.

Left bought back stock right after advising readers to sell, and sold stock immediately after making his buy recommendations, the SEC said.

Also read: ‘Like taking candy from a baby’: How Andrew Left allegedly played the market like a fiddle

Kate Zoladz, director of the SEC’s Los Angeles regional office, said Left “took advantage of his readers” in order to realize “$20 million in ill-gotten profits.”

In June, the SEC settled public administrative charges against investment adviser Anson Funds Management LP and Toronto-based Anson Advisors Inc. for conduct involving their relationship with Left and others.

Anson Funds Management and Anson Advisors used the Cayman Islands–registered Anson Investments Master Fund, or AIMF, to take short positions in cannabis stocks while also working with a publisher to distribute bearish information on those same equities, the SEC said in a statement at the time.

Become a more knowledgeable investor today

Unlock this special offer to make the most of your money with personalized financial insight from MarketWatch + Barron’s.

Citron Capital and Left have been vocal as activist shareholders that take positions in companies and then try to carry out changes in order to unleash value and boost stock prices.

MarketWatch has reported comments by Citron Research on a number of high-profile stocks, such as GameStop Corp.

In February, shares of Esports Entertainment Group Inc. rallied after Citron Research said GameStop should buy the online gambling company.

Nvidia could be on the verge of a massive technical sell-off, chart analyst warns

PUBLISHED FRI, JUL 26 20241:30 PM EDTUPDATED 2 HOURS AGO

Jesse Pound@/IN/JESSE-POUND@JESSERPOUND

Nvidia’s slump is hitting some technical milestones that suggest the stock could continue to slide, according to Raymond James.

Shares of the dominant maker of chips used in artificial intelligence are down about 8% in July. Raymond James chart analyst Javed Mirza said in a July 25 note to clients that Nvidia has triggered a “mechanical sell” signal based on a moving average convergence/divergence indicator, or “MACD,” which measures price momentum — and it is not the only technical signal flashing sell.

“In conjunction with price moving below an important technical level at the 50-day moving average … and Volume showing early signs of selling pressure … these three early technical negatives suggest an intermediate-term (1-3 month) corrective phase is attempting to take hold,” the note said.

The key level to watch is Nvidia’s 50-day moving average, currently around $118 per share, according to Mirza.

“A multi-day close below important technical support at the 50-day moving average … would confirm a new short-term corrective phase was underway. This would then open the door for a filling of the gap around 94.94 … or another 16.9% downside from current levels,” the note said.

Nvidia has been the biggest beneficiary of the excitement around artificial intelligence. Other tech companies have been spending billions to order chips from Nvidia, which is seen as far ahead of its competitors in building high-end semiconductors. The stock is up more than 400% over the past three years.

However, investors seem to be growing a bit skeptical around AI’s immediate contribution to higher corporate profits, at least in the near term. If that view spreads to executives at Big Tech companies such as Alphabet, it could result in new orders for Nvidia slowing down.

Nvidia is set to report its second-quarter results on Aug. 28.

— CNBC’s Michael Bloom contributed reporting.

Buy top tech stocks like Apple ahead of their results before it’s too late, Bank of America says

PUBLISHED SAT, JUL 27 20248:43 AM EDT

There’s still plenty of buying opportunities among technology stocks, according to Bank of America.

The investment bank says stocks like Apple are table-pounding buys ahead of quarterly results this week.

CNBC Pro combed through Bank of America research to find buy-rated tech stocks with more room to run.

They include: Microsoft, Apple, Micron Technology, Shopify and Sea Limited.

Apple

Bank of America recently raised its price target on the iPhone maker to $256 from $230.

Analyst Wamsi Mohan said Apple is firing on all cylinders ahead of what he says is a “refresh(ed) iPhone cycle.”

Recent survey checks by the bank indicate that Apple’s iPhone user base is poised to upgrade to products containing AI features.

Brand loyalty is paramount, according to the bank.

“14% of respondents in the U.S. reported that they are planning on buying the Apple Vision Pro,” Mohan wrote.

Apple is scheduled to report earnings next Thursday, August 1.

“We reiterate our Buy rating based on an expected multi-year iPhone cycle driven by GenAI, strong services growth and margin expansion,” he said.

Shares are up 13.2% this year.

Shopify

Time to buy shares of the Canadian provider of websites for businesses, according to Bank of America.

Analyst Brad Sills recently upgraded Shopify to buy from neutral as a “more balanced growth & margin profile” take hold.

The company’s transformation under a new chief financial officer is underway, too, Sills said, as quarterly results loom large in early August.

“Revenue growth and disciplined spending point to healthy margin expansion going forward,” he wrote.

Sills sees Shopify with many competitive advantages that portend well for big share gains down the road.

“Shopify appears well positioned to continue capturing share of the eCommerce market, while achieving better scale and [free-cash flow] conversion,” he went on.

Shares are down 23% in the U.S. this year.

Sea Limited

Shares of the Singapore-based tech internet company are up 61% this year, but have more upside, Bank of America said.

Analyst Sachin Salgaonkar urged clients to remain calm as trends are showing improvement in the company’s gaming and Shopee divisions. Shopee is Sea’s Southeast Asia e-commerce platform.

“In our view it is placed well to ride e-com boom in SE Asia given its increasingly dominant online marketplace (Shopee), while its expansion into Brazil offers further long term growth potential,” he wrote.

The bank says losses are bottoming while also acknowledging that the competition arrayed against Sea is real. Still, the Wall Street firm reiterated its buy rating, urging clients to own shares for the long term.

“We see stable competition trends in the region and expect take rates to improve,” he added.

Sea is expected to report quarterly earnings in August.

Micron

“AI driving strong pricing, mix, edge opportunity ahead. We were pleased to host Micron CFO Mark Murphy, CVP Satya Kumar and IR Samir Patodia for well attended investor meetings in Boston and New York. Key message very bullish re: pricing, visibility, supply discipline and mix improvement towards differentiated AI computing and enterprise storage products.”

Microsoft

“We believe that MSFT is well positioned to generate sustained low double digit growth in the coming 3-5 years, led by continued adoption of Azure cloud infrastructure platform, cloud based Office 365 productivity suite & more profitable Games & Game Pass revenue in Xbox.”

Sea Limited

″“In our view it is placed well to ride e-com boom in SE Asia given its increasingly dominant online marketplace (Shopee), while its expansion into Brazil offers further long term growth potential. … We see stable competition trends in the region and expect take rates to improve.”

Apple

“Strong multi-year iPhone refresh cycle with aging installed base; PO to $256. … .We reiterate our Buy rating based on an expected multi-year iPhone cycle driven by GenAI, strong services growth, and margin expansion. … 14% of respondents in the U.S. reported that they are planning on buying the Apple Vision Pro.”

Shopify

“Revenue growth and disciplined spending point to healthy margin expansion going forward. … Shopify appears well positioned to continue capturing share of the eCommerce market, while achieving better scale and FCF conversion. … More balanced growth & margin profile.”

Markets now pricing in three rate cuts before the end of the year following better inflation news

PUBLISHED FRI, JUL 26 202412:01 PM EDTUPDATED FRI, JUL 26 202412:14 PM EDT

Jeff Cox@JEFF.COX.7528@JEFFCOXCNBCCOM

Improving news on inflation again has raised investors’ hopes that the Federal Reserve soon will start to aggressively lower interest rates.

Following Friday’s Commerce Department report that the annual inflation rate as gauged by the Fed’s favorite measure had cooled to 2.5%, traders increased the probability that not only will the first rate cut in more than four years come in September, but a series also will follow through the end of the year.

Futures market pricing now indicates that while the Fed will remain on hold at next week’s policy meeting, it will commence cutting in September and move again in November and December. The core personal consumption expenditures, or PCE, price index, which the Fed more closely uses to guide policy and which excludes food and energy inputs, was slightly higher, at 2.6%.

“Investors are now fully pricing in 25 basis-point rate cuts in September and December with strong probabilities for cuts in the November and the January meetings,” Joseph Brusuelas, chief economist at RSM, said in commentary following the PCE release.

“If that forward-looking market data holds, such a move implies a full 100 basis-point reduction in the federal funds rate from its current range of 5.25% to 5.5% to 4.25% to 4.5% over the next 180 days,” he added.

Still premature to talk about a dramatic amount of rate cuts coming, says Apollo’s Torsten Slok

The market-implied probability for a September cut nudged up to about 90% Friday morning, according to the CME Group’s FedWatch Tool that measures fed funds futures pricing.

Traders further assigned a 67% chance of a November reduction — that month’s meeting begins the day after the presidential election — and a 64% probability for December. January was still seen as less than 50%.

Fed funds futures have been an unreliable guide this year for Federal Open Market Committee decisions. Traders in early 2024 were pricing in at least six cuts this year, but the central bank’s rate-setting group has remained on hold for a year.

However, officials in recent days have shown more of an inclination to cut.

In congressional testimony earlier this month, Fed Chair Jerome Powell noted the risks of holding rates too high for too long and said additional good inflation data would “strengthen our confidence” that reductions are warranted.

Governor Christopher Waller echoed those comments, saying the Fed is “getting closer” to easing.

Following the two-day meeting that concludes next Wednesday, the Fed meeting schedule is empty for August, save for the all-important annual conclave in Jackson Hole, Wyoming. Fed chairs traditionally have used the retreat to make significant policy speeches.

HI Financial Services Mid-Week 06-24-2014