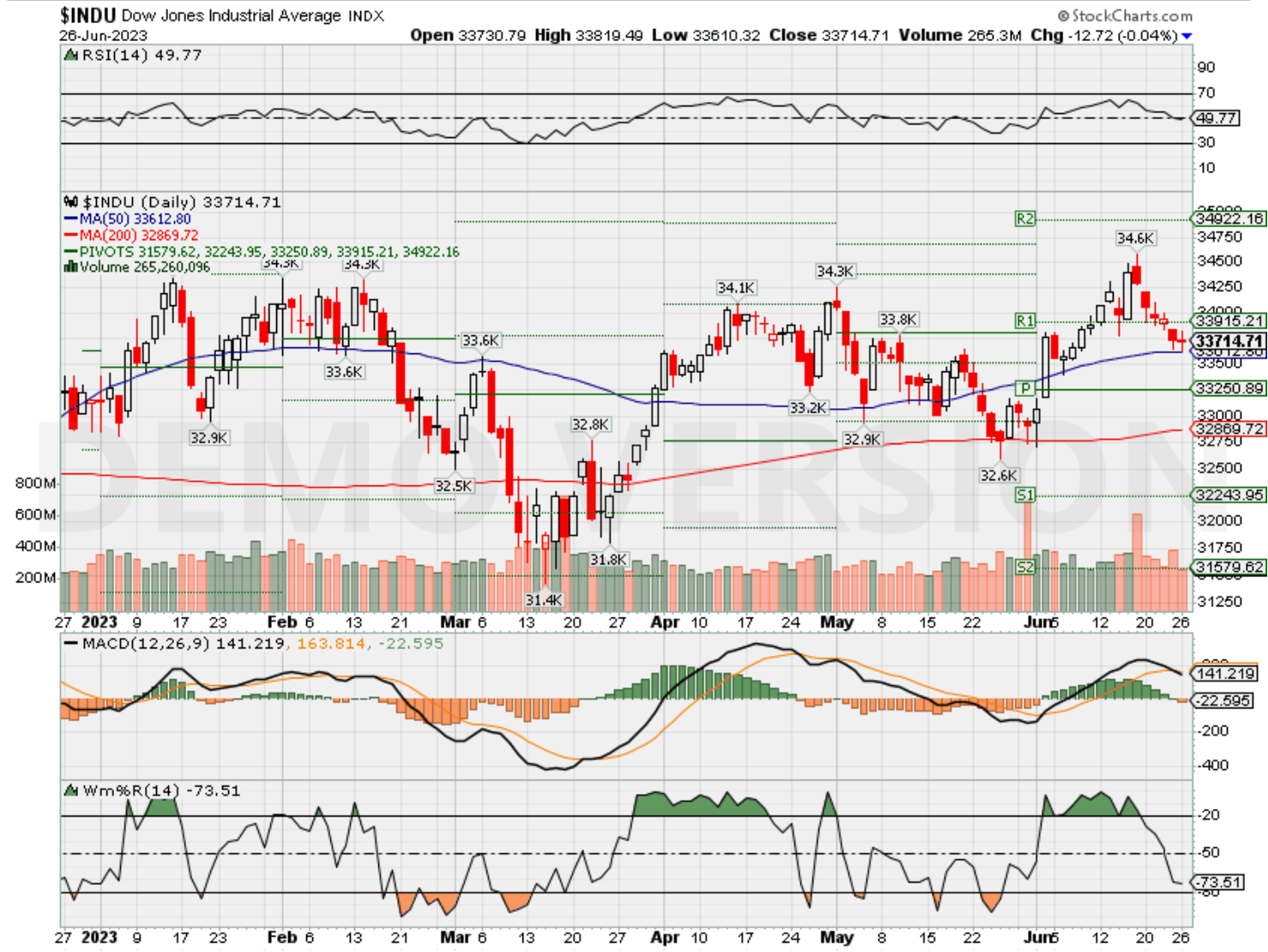

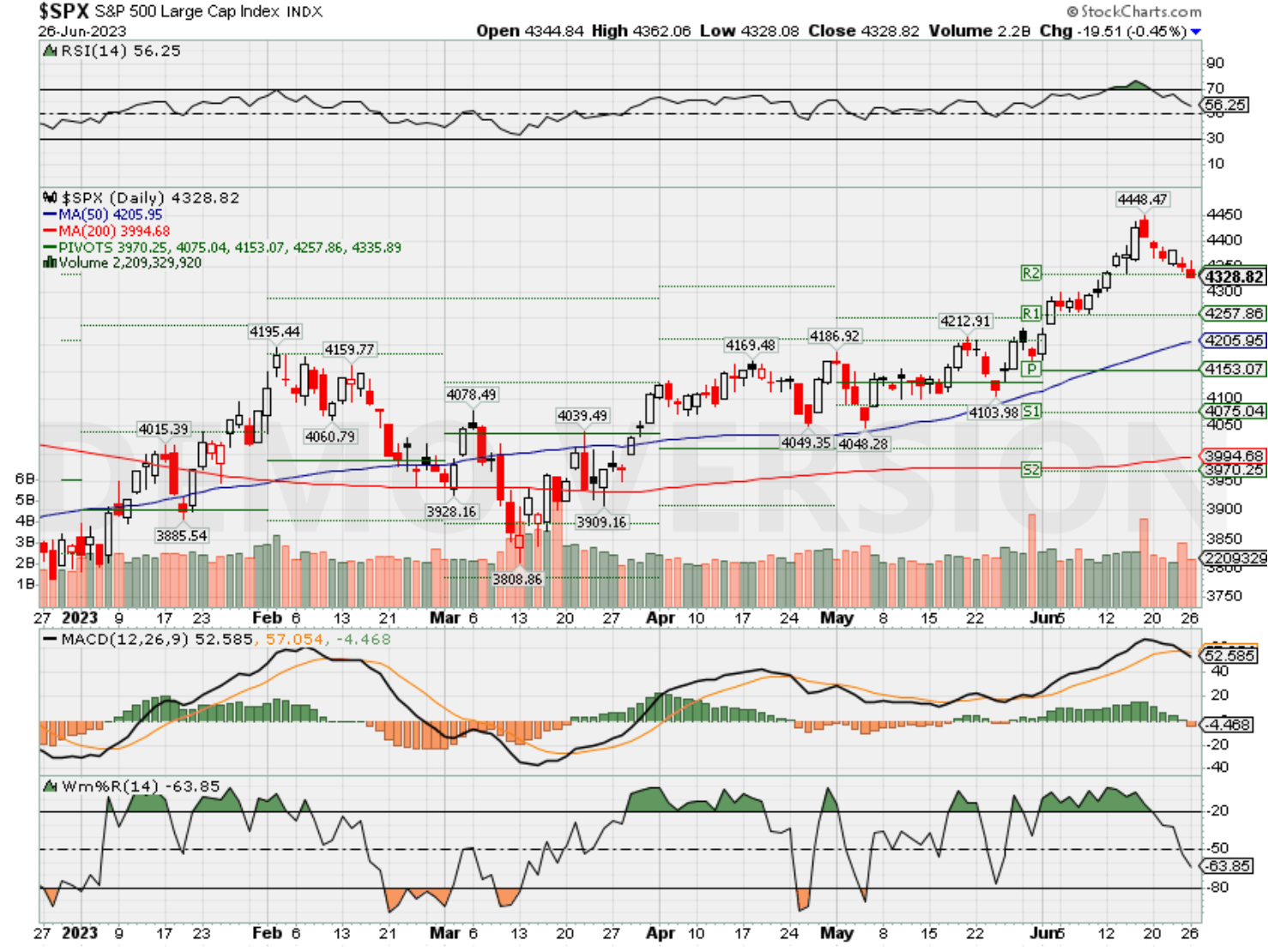

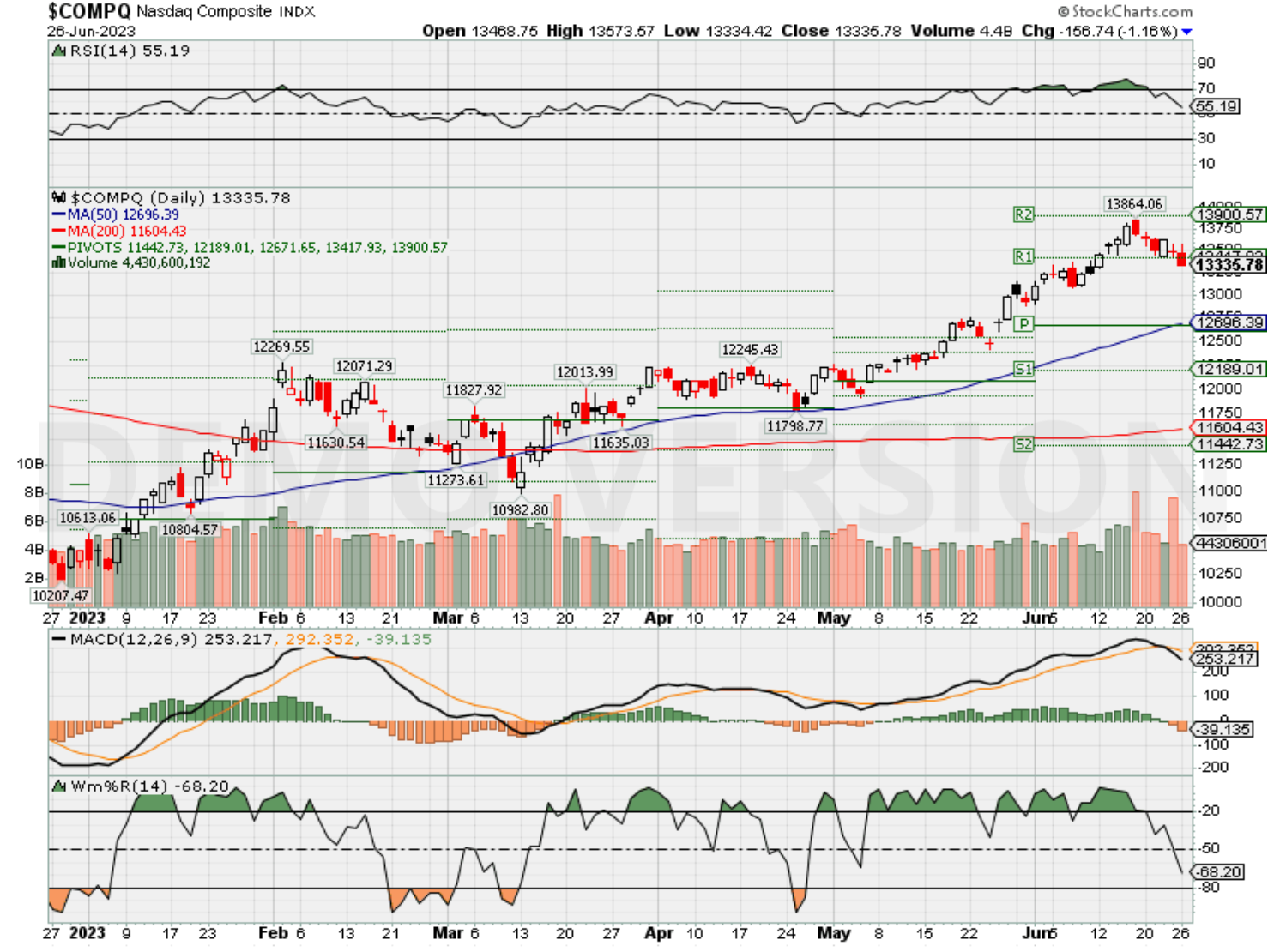

HI Market View Commentary 06-26-2023

What do you do when you run into hard things within the market?

16.4% loss occurred last week in a single 6 figure portfolio

You can ……. Learn from it, Make changes to fit current market conditions, adjust if warranted, do a better job paying attention and researching he market

IN REAL LIFE, the market isn’t easy and there is NO EASY FIX….ie, algorithm, system, higher return AI, magic fix,

What do you do to hedge a portfolio for protection to live another day? I was told get out and reset the portfolio. So….. Why didn’t you do it?

There are some things that you can’t make a mistake on ….. losing everything

The market doesn’t make sense right now

What it means?= More protection is ready to be added for a drop farther

Next Tuesday the market it closed and historically it is a dead week = flat

We at HI are planning on no webinars and just watching the market with added protection

We also are still fighting Schwab for the last of the accounts to get over which means we may be calling you to add protection in the Schwab login accounts

https://www.briefing.com/the-big-picture

Last Updated: 23-Jun-23 15:06 ET | Archive

Stock market diverges from recession view

Two roads diverged in a wood, and I —

I took the one less traveled by,

And that has made all the difference.

–Robert Frost

There has been a divergence of sorts between the stock market and Treasury market since the middle of October 2022. That is when the S&P 500 bottomed following the insufferable slide that began in January 2022 on the back of valuation concerns, rampant inflation, and a shift to an aggressive rate-hike campaign by the Federal Reserve.

The catalyst for the turn in October, ironically, was a bad September Consumer Price Index. It was so bad that there was a feeling that it could not get any worse. By and large, market participants had that right.

Total CPI was up 8.2% year-over-year last September and core CPI, which excludes food and energy, was up 6.6%. The latest readings recorded just a few weeks ago showed total CPI up 4.0% year-over-year in April and core CPI up 5.3%.

Core inflation is still too high, and the Fed has an aim to solve that with additional rate hikes. The question is, just how well will the economy handle additional rate hikes, let alone the 500 basis points of rate hikes recorded since March 2022?

The improvement in stock prices suggests the economy should handle things just fine. The widening in Treasury spreads, however, is leading some to think that the economy just might follow a different road.

Things Have Changed

Typically, longer-dated maturities have higher yields than shorter-dated maturities because one is taking on more risk for the longer holding period. When the S&P 500 bottomed last October, the spread between the 2-yr note yield and the 10-yr note yield was inverted by nearly 40 basis points, meaning the 2-yr note yield was yielding nearly 40 basis points more than the 10-yr note yield.

In this instance, the inversion was a reflection of market participants’ concerns that the Fed would have to be aggressive in raising rates; and that by doing so, the Fed would effectively slow the economy in a pronounced way that would get inflation under control.

Meanwhile, the spread between the 3-month T-bill yield and the 10-yr note yield flattened during the stock market’s sell-off in 2022, but it was still positive by about 20 basis points when the S&P 500 bottomed in October 2022. Oh, how things have changed.

Today the spread between the 3-month T-bill yield and the 10-yr note yield is inverted by 157 basis points. That’s better than where it was at the end of May, but it remains a long way from suggesting the Treasury market thinks the economic outlook is hunky dory. The same goes for the 2yr10yr spread, which is inverted now by 100 basis points.

It is a peculiar divergence indeed. The stock market has been rallying off its October lows for a variety of reasons, but prominent among them is the notion that the economy will avoid a hard landing, that the Fed is close to being done raising rates because inflation is headed back to the Fed’s two percent target rate, and that earnings growth will accelerate again in 2024.

When grading on a curve so to speak, the Treasury market seems to be seeing things differently.

Supply Lines

To be fair, the Treasury market is not only seeing, but also staring at a wall of new supply coming its way as the Treasury Department works to replenish its General Account. The bulk of the issuance, which is estimated to be around $1 trillion, is expected to include mostly shorter-dated maturities.

What we are driving at is that the widening inversion taking place as the stock market has broken out to its highest level since April 2022 could be based more on supply considerations than a forlorn economic outlook. To that end, we would be remiss not to point out that high-yield spreads have come in about 100 basis points since the stock market bottomed in 2022 and are sitting around the same area they were at when the year began, and 2023 recession calls were high pitched.

Nonetheless, the inversion is not a welcome development for banks, which borrow at short-term rates and lend at long-term rates, so they would have an increased tendency to tighten their lending standards, thereby curbing the credit expansion that is a lifeblood for economic growth. At the same time, the demand for new loans will go down because of the higher borrowing costs and that, too, would crimp growth prospects.

So, supply is one thing to explain the inversion, but we cannot entirely dismiss growth concerns as a causal factor.

What It All Means

The relatively calm demeanor of high-yield spreads, however, continues to be a feather in the cap for proponents of the soft landing/no landing view. It runs counter to the recession outlook that is presumably being presaged by 14 straight monthly declines in the Leading Economic Index.

Arguably, it could be the calm before the storm, yet the economic hurricane someone once said we should prepare for is still nothing more it seems than a tropical depression. Q1 real GDP growth was 1.3% and the latest Atlanta Fed GDPNow model estimate for Q2 real GDP growth is 1.9%.

For a forward-looking market, then, one has to respect the fact that high-yield spreads aren’t yet sniffing bigger economic problems down the road. That is perhaps why the stock market is looking away from the widening spreads in the Treasury market and showing some broadening in this year’s gains beyond the mega-cap stocks.

It likely also helps explain why the countercyclical utilities, health care, and consumer staples sectors are not only underperforming the market-cap weighted S&P 500 (like most sectors are) but also, more tellingly, the equal-weighted S&P 500.

The stock market’s forward view doesn’t see dark storm clouds on the horizon, only some grey clouds that also feature a silver lining of an acceleration in earnings growth in 2024. Maybe that’s when the long and variable lags of the Fed’s rate hikes will show up and storm clouds will appear. Maybe.

Thus far, when it comes to recession views, the stock market has taken the road less traveled by in 2023 and that has made all the difference.

—Patrick J. O’Hare, Briefing.com

(Editor’s Note: The next installment of The Big Picture will be published the week of July 3)

Where will our markets end this week?

Higher

DJIA – Bullish

SPX –Bullish

COMP – Bullish

Where Will the SPX end June 2023?

06-26-2023 +2.0%

06-20-2023 +2.0%

06-12-2023 +2.0%

06-05-2023 +2.0%

Earnings:

Mon: CCL

Tues: WBA

Wed: GIS, BB, FUL, MU

Thur: NKE

Fri: STZ

Econ Reports:

Mon:

Tue Durable Goods, Durable goods ex-trans, FHFA Housing Price Index, S&P Case Shiller Report, Consumer Confidence, New Home Sales

Wed: MBA,

Thur: Initial Claims, Continuing Claims, GDP , GDP Deflator, Pending Home Sales,

Fri: Personal Income, Personal Spending, PCE Core Pricing, PCE Pricing, Michigan Sentiment

How am I looking to trade?

Adding protection based on technical analysis on indexes and individual stocks

www.myhurleyinvestment.com = Blogsite

info@hurleyinvestments.com = Email

Questions???

Here’s why the market is ignoring a tell-tale sign that a recession is coming

PUBLISHED MON, JUN 26 20232:18 PM EDTUPDATED 46 MIN AGO

Jeff Cox@JEFF.COX.7528@JEFFCOXCNBCCOM

A trader works on the floor of the New York Stock Exchange, June 9, 2023.

Michael Nagle | Bloomberg | Getty Images

For just shy of a year now, the bond market has been signaling that a recession is on the horizon. For the better part of the past six months, the stock market has been ignoring it.

In early July 2022, the 2-year Treasury yield surpassed that of the benchmark 10-year note, a phenomenon known as an inversion that has preceded each of the six recessions the U.S. has experienced going back to 1980.

The time span between the initial inversion and recessions generally has been six to 12 months, putting the economy squarely in the sights of a seemingly inevitable downturn. Yet, stock market investors seem either not to notice or not to care, pushing the S&P 500 up about 13% year to date and nearly 11% from a year ago as gross domestic product has remained positive through the past three quarters.

The apparently broken relationship may lie in what a peculiar time this has been for the financial and economic worlds since the Covid-19 pandemic broke out in March 2020.

“The market’s certainly not acting like it would if this ‘Waiting for Godot’ recession was right around the corner. It’s a very odd thing,” said Art Hogan, chief market strategist at B. Riley Wealth Management.

“I would say it’s much more about what started this conundrum, the combination of pandemic policy, pandemic reopening and hyperaggressive monetary policy. Throw that together, and it can throw off a lot of signaling.”

Indeed, a “this time is different” narrative could well apply to a situation the economy has never faced before: A unique global pandemic, met with the most aggressive fiscal and monetary response in history, all of which helped create the highest inflation level in more than 40 years, requiring a strong policy pivot in which the Federal Reserve is trying to engineer a soft landing that could include a shallow recession.

For that reason, comparing short-term bond yields against the 10-year may not be as useful a measuring stick.

A 71% recession probability?

“There isn’t anybody alive who can tell us what the playbook should look like after a pandemic,” Hogan said. “What we have historically counted on for good signaling is [now] a weird confluence of events.”

For its part, the Fed concentrates more on the relationship between the three-month Treasury and the 10-year. That curve flipped in late October 2022, and just a few weeks ago, hit its widest gap ever.

The New York Fed uses a model that computes the recession probability over the next 12 months using the relationship. As of the end of May, that was around 71%. The inversion level is little changed since then, so the recession probability likely is about the same.

However, other indicators are not as clearly pointing to recession.

Most notably, the labor market has been uncannily strong, with a 3.7% unemployment rate despite the Fed raising benchmark interest rates 5 percentage points since March 2022. The services part of the economy remains strong, and even housing numbers of late are turning around.

The Fed, however, remains in inflation-fighting mode, raising short-term rates and possibly distorting the yield curve. Indeed, the central bank held off on a June hike but indicated two more increases are coming in 2023.

“The Treasury yield curve tells an important but incomplete story about the US economy’s risk of imminent recession,” Nicholas Colas, co-founder of DataTrek Research, wrote in his market note overnight Sunday. “Monetary policy is purposefully tight at the moment because strong labor markets are still feeding inflationary pressures. That the 3m/10y and 2y/10y spreads are in very unusual territory is the Fed’s way of addressing that problem.”

Colas noted that the Fed “has no other viable option now” as it seeks to pull down inflation, even if that means risking a recession.

“Markets understand that but take comfort that the current labor market picture offsets some of that risk,” he added.

A recession unlike others

There’s also the “rolling recession” narrative to consider.

Multiple sectors of the U.S. economy — autos, housing and manufacturing, to name three — have experienced what could qualify as contractions, and it’s possible others could follow suit without tipping the headline GDP number negative.

Wharton Business School Professor Jeremy Siegel sees the economy slowing further ahead. A key narrative from those looking for a recession is the lag effects that Fed policy will have.

In fact, Siegel said the economy could slow so much that the Fed won’t be able to deliver on the two potential rate hikes that officials penciled in following the policy meeting earlier in June. If that happens, markets are going to have to take notice.

“It’s hard to see upside catalysts for the market in the second half of this year,” Siegel said Monday on CNBC’s “Squawk Box.” “I think the bright side of a mild recession is that not only will we not get rate increases, but … we could get rate decreases by the end of the year.”

“I’m not talking about disaster,” he added. “But when people are saying, ‘what is on the upside?’ I just don’t see as many factors.”

Disney: Look Past The Political Rhetoric

Jun. 26, 2023 2:55 PM ETThe Walt Disney Company (DIS)CMCSA, NFLX, PARA, PARAA, PARAP, WBD, SPY52 Comments3 Likes

987 Followers

Follow

Summary

- Disney faces negative sentiment due to political rhetoric and “wokeness” accusations, but its core business remains strong and focused on children and families.

- The company’s recent performance has been affected by factors such as the integration of 21st Century Fox and regional issues in India and Southeast Asia.

- Long-term investors may find an attractive entry point in Disney’s stock, as the company is expected to continue growing, improving profitability despite short-term challenges.

Joe Raedle/Getty Images News

Negative Press

For more than a year Disney (NYSE:DIS) has been the target of Florida Governor Ron DeSantis as well as many who no longer “approve” of some of Disney’s content or feel that it is “woke.” The impact of DeSantis’ interest in Disney or that of the anti-woke crowd is dubious at best as Disney is generating revenue at or near all-time record levels. While profitability has suffered as a result of rising expenses, it is important to keep an objective, long-term perspective, and understand the fundamental status of the business.

Attention was drawn to Disney’s wokeness mostly as a result of former CEO Bob Chapek’s comments regarding Florida’s so-called “Don’t Say Gay Bill.” That brought the ire of Governor DeSantis and his acolytes. Governor DeSantis then took it upon himself to use the power of his office to go on the offensive against Disney, focusing on the Reedy Creek Improvement District, currently known as the Central Florida Tourism Oversight District. This district covers just over 39 square miles of land where the Walt Disney World Resort is located. The district was established in 1967 to oversee the land use, enact environmental protections, and to provide essential services including fire, EMTs, water/sewer, electricity, roadway maintenance, etc.

This is not a referendum on whether Disney should control the district or what role it should play in its management. The issue is mentioned to highlight how it has contributed meaningfully to the negative sentiment around the company, regardless of its validity. I have not seen any accusations from the Florida governor’s office in relation to that arrangement stating that Disney has broken any laws, violated any contracts, or partaken in any unfair or unusual business practices that would illicit any investigation. There appears to be no tangible or objective evidence of any wrongdoing related to that issue. It seems reasonable to conclude that the governor’s political opinions and feelings were the impetus for any potential conflict in my view.

Target Audience

Disney owns and controls a significant catalogue of intellectual property. It is what underpins everything the company does through branding, marketing, merchandising, and entertainment channels. Historically, the bulk of those properties used for content creation and distribution were focused on children’s entertainment. That continues to be the main driver of the business through movies, merchandise, streaming content, and park attendance. Beyond content appealing to the younger audience, Disney also produces and distributes sports content and that associated with legacy brands including Star Wars and Marvel Comics.

Understanding that Disney’s business caters to children and families is critical to looking past the current political rhetoric. Disney’s business is durable and will probably outlive everyone reading this sentence. I believe the current mood or politically-charged opinion of older, more conservative-leaning individuals are largely irrelevant. Park attendance is driven by children begging their parents and those parents taking them, spending a lot of money doing so. The same dynamics are at play for subscribing to Disney+ or going to the theater or purchasing merchandise. Today is no different than any other period in time: 5-year old girls and 8-year old boys don’t care about politics, wokeness, or Ron DeSantis. They enjoy the characters and their stories. That’s it.

It’s also important to understand that Disney is a global business with paying customers that are indifferent to American politics. Visit Disney World and there will be people from all around the world. Those people have different backgrounds and different politics, but they spend money just the same. And ultimately that’s what matters.

While I understand that the various narratives about Disney, good or bad, can drive stock prices in the short run, in the long run, when these arguments and opinions are in the rearview mirror, it will be the fundamentals that drive the stock. As a result, this mismatch may be creating an opportunity for patient investors. And if the people most negative on the company are driven by the current wokeness craze and headlines about petty politics rather than the long-term fundamentals, then I am happy to take the other side of that trade.

Recent Performance

Disney reported revenue of $21.8 billion for the second quarter 2023, ended April 1 of this year, a year-over-year increase of 13.5%. The company shed about 4 million total net subscribers from Disney+, ending the quarter with 157.8 million total subscribers, missing analyst expectations of 163.17 million. This weakness was driven by Disney+ Hotstar. Disney+ Hotstar is the version of its streaming service that Disney offers customers in India and other parts of Southeast Asia. Much of these recent losses has been driven by reduced programming for the Indian Premier League cricket matches.

Core Disney+ subscribers were higher during the quarter. Average revenue per paid subscriber increased both for the quarter and year-over-year in aggregate, although Disney+ Hotstar declined in that metric as well. Between the U.S. and Canada, the subscriber base shrunk by about 300,000, although international markets, excluding Disney+ Hotstar, added about 1 million subscribers. Hulu gained 200,000 subscribers during the quarter while ESPN+ added 400,000.

While revenue at its media and entertainment distribution segment continues to grow, albeit at a low single digit rate, expenses have outpaced that growth resulting in negative segment operating income. The largest contributor to this decline is the decline in revenue and stubbornly high expenses within Disney’s linear networks. While revenue was lower at both domestic and international channels, the weakness in international was far greater. Lower advertising revenue was the primary driver of weakness within its international channels, with airing fewer cricket matches for the Indian Premier League again the largest culprit.

Disney parks continued to be a source of strength with operating results exceeding Wall Street estimates for the quarter.

Recent performance in the stock has suffered due to the negative sentiment combined with narrow profit margins and general uncertainty about growth and profitability. The stock is significantly underperforming the broader market, declining 6.6% over the last year compared to a 16.5% gain in the S&P 500 on a total return basis.

1-Year Total Return: DIS versus SPY (Seeking Alpha)

Valuation

The stock is trading at about a 40% discount to historical value when using the metrics in the table below. This is a starting point and not enough information from which to draw a conclusion. It is possible that the stock was overvalued during the last 5 years, skewing the averages higher, or that the stock is undervalued currently, or most likely that it’s some combination of both.

| Valuation Metric | DIS | DIS 5-Year Average | % Difference to 5-Year Average |

| P/E Non-GAAP (‘FWD’) | 22.29 | 41.63 | -46.47% |

| EV/Sales (‘FWD’) | 2.36 | 3.84 | -38.60 |

| EV/EBITDA (‘FWD’) | 13.82 | 21.60 | -36.02% |

| EV/EBIT (‘FWD’) | 16.20 | 27.13 | -40.30% |

| Price/Cash Flow (‘FWD’) | 16.01 | 26.70 | -40.03% |

| Price/Book (‘FWD’) | 1.61 | 2.72 | -40.92% |

Valuation Versus Peers

While Disney appears significantly undervalued based on its historical valuation, the same cannot be said when making a peer comparison. Disney’s value as measured by the metrics in the table below is at or near the top end of the range with the four competitors/peers shown here. It is difficult to find a truly comparable company for Disney given its wide array of businesses and the scale of those businesses. For example, It makes sense to look at Netflix (NFLX) on the basis of the streaming businesses, but Netflix lacks parks, merchandise, traditional movie production and distribution, real estate operations, etc. Comcast (CMCSA) has overlap on linear television and parks through NBCUniversal, but it also has cable and internet service that better resembles a utility than a consumer discretionary type business. Similarities and differences of this scale exist across the peer group. That said, Disney appears cheap versus Netflix and expensive versus Warner Bros. Discovery (WBD), Comcast, and Paramount Global (PARA). The question is how should this be weighted relative to Disney’s historical valuation.

| Valuation Metric | DIS | Warner Bros. Discovery (WBD) | Netflix (NFLX) | Comcast (CMCSA) | Paramount Global (PARA) |

| P/E Non-GAAP (‘FWD’) | 22.29 | 13.14 | 37.72 | 10.95 | 23.39 |

| EV/Sales (‘FWD’) | 2.36 | 1.77 | 5.82 | 2.19 | 0.84 |

| EV/EBITDA (‘FWD’) | 13.82 | 6.89 | 27.15 | 7.11 | 11.03 |

| EV/EBIT (‘FWD’) | 16.20 | 445.20 | 30.77 | 11.75 | 13.19 |

| Price/Cash Flow (‘FWD’) | 16.01 | 5.57 | 46.11 | 5.87 | NM |

| Price/Book (‘FWD’) | 1.61 | 0.63 | 7.92 | 1.95 | 0.44 |

Dividend

The last dividend paid by Disney was in December 2019, and was subsequently suspended at the onset of the pandemic. Prior to that, Disney had paid dividends for more than 30 consecutive years. Given the volatility in cash flow over the last several years, and the likelihood that that will continue, I suspect that the decision to reintroduce the dividend is years off. That said, the company could easily cover the dividend amount paid in 2019 from operating cash flow.

Profitability

While revenue continues to grow and the gross margin remains at least close to multi-year averages, operating expenses remain stubbornly high relative to revenue, causing net margins to plummet. This in turn has resulted in much lower returns on equity, assets, and total capital. For these figures to rebound, Disney will need to make meaningful improvements to managing its expenses.

| Profitability Metric | DIS | DIS 5-Year Average | % Difference to 5-Year Average |

| Gross Profit Margin (‘TTM’) | 33.04% | 35.84% | -7.81% |

| Net Income Margin (‘TTM’) | 4.74% | 7.04% | -32.68% |

| Return on Common Equity (‘TTM’) | 4.37% | 7.81% | -44.03% |

| Return on Total Assets (‘TTM’) | 2.01% | 3.23% | -37.64% |

| Return on Total Capital (‘TTM’) | 2.95% | 4.52% | -34.62% |

As shown in the following three charts, Disney had been successful at increasing returns since the bottom reached during the 2001-2003 recession. The steep decline in profitability started in late 2018 and continued through 2020 as the integration of its purchase of 21st Century Fox. Since then, Disney has been actively cutting costs to improve profitability through measures including shutting the Fox 2000 Picture studio in 2020, layoffs at Fox’s Film Division, canceling numerous Fox films, and selling the Fox Sports Network, among many other efforts.

Long-Term ROE Trend (Seeking Alpha)

Long-Term ROA Trend (Seeking Alpha)

Long-Term ROTC Trend (Seeking Alpha)

Outlook

Disney is a ‘Hold’ for those with an investment horizon shorter than 1 year, and a ‘Buy’ for those with investment horizons measured in years and decades. I am always a long-term investor and believe that Disney will continue to grow while better managing expenses. At the current share price below $90, recovering half the 40% discount to the 5-year average valuation would represent about 30% of upside. I believe it is reasonable for a move of this magnitude to occur in the coming 12-18 months, driven by improved profitability and erosion of negative sentiment about the company.

Risks

Many risks Disney faces have been touched on throughout this article, including consumer sentiment, preferences, and tastes. Not all new efforts will bring success. Not all Disney movies will break box office records. This is reality, and it is the responsibility of Disney management to navigate through these challenges in its effort to increase shareholder value.

Profitability remains a challenge and any continued headwinds, regardless of source, across business segments pose risks to the company and its share price. Most of Disney’s products and services are considered discretionary spending, and because of this are sensitive to shifts in the economy. While cost cutting and integration in the wake of the Fox deal remains important, effective execution on continuing operations is critical: Growing Disney+ subscribers profitably, developing and producing appealing content for movies, shows, etc., continuing to operate profitably at the parks, etc. Failure in any of those areas poses a material risk to the company and its share price.

Final Thoughts

Disney is an American institution that has brought fun and entertainment through its movies and parks for the better part of the last 100 years. It is a resilient and innovative company, and there is no reason to believe that it won’t continue to be so for many years and decades to come.

The woke and other political narratives are overhyped in my opinion, and it is reasonable to expect that any negative impact they may have will be temporary, creating an attractive entry point for patient investors.

While the company’s performance has been rocky in recent years, that has been driven by several factors. The acquisition and integration of 21st Century Fox has not gone smoothly, the rapid rollout and acceptance of Disney+ has been met with rising expenses that have eaten into profitability, and the performance of streaming and linear programming in India and Southeast Asia has been erratic. The loss of streaming subscribers has been used as evidence of the decline of the brand, although most of those losses have been driven by specific regional factors.

As a shareholder and customer of Disney’s streaming service, parks, movies, and merchandise, I am confident that the business will continue to grow on the top line while expenses are reigned in to boost future profits.

Disney’s performance is always a little volatile. Park and movie attendance are driven by numerous factors beyond Disney’s direct control. Beyond weather and the economic environment at any given time, the company needs to be nimble in serving evolving interests, preferences, and tastes. It has never been easier for consumers to purchase or cancel services, or switch services, or whatever seems to make sense that day. Specifically, streaming customers can come and go based on the ebb and flow of new content. This is far greater flexibility than ever afforded by linear TV or cable service in general, and creates an ongoing challenge for Disney and its competitors.

Disney is a brand that has and should continue to endure. My opinion is that the stock is trading at a discount, but that a turnaround may not be quick and will likely experience some setbacks. Because of this I suggest that investors take a longer-term approach when valuing the stock and deciding whether it is a good fit for their portfolios.

Before adding to an individual position, especially given the short-term uncertainty at Disney, investors should consider the risks of this stock and how any position in it might impact long-term total returns and long-term investment objectives. Thank you for reading. I look forward to seeing your feedback and comments below.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of DIS NFLX SPY either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

https://seekingalpha.com/article/4613558-sell-alert-3-reits-that-likely-will-cut-their-dividends

Sell Alert: 3 REITs That Likely Will Cut Their Dividends

Jun. 26, 2023 8:05 AM ETBDN, GPMT, GPMT.PA, SLG, SLG.PI, VGSIX, VGSLX, VGSNX, VNQ

Summary

- Some REITs yield as much as 15 to 20%.

- Such high dividend yields are rarely sustainable.

- We highlight 3 REITs that will likely cut their dividend.

- High Yield Landlord members get exclusive access to our real-world portfolio. See all our investments here »

Lemon_tm

Co-produced by David Ksir

REITs (VNQ) have become a popular choice for income-oriented investors due to their high dividend yields.

Following the recent crash, there is a large number of REITs that are today trading at near all-time high dividend yields of 15% or even 20%. Many investors are blinded by these high yields, expecting the dividend payments to continue, just to find out shortly after that the dividend wasn’t sustainable.

Moreover, a cut is almost never fully priced-in which means further downside as the dividend is cut. This is a very painful scenario for investors, which is why I try my best to stay away from REITs that could potentially cut their dividends in the near future.

Historically, the best way to assess the risk of a dividend cut has been to keep a close eye on the payout ratio. As long as it was reasonable and the REIT was generating enough cash flow to cover the dividend payments and their capex, then the dividend was safe in most cases.

Recently though, the outlook for some REIT sectors has deteriorated so much that companies are choosing to cut their dividend even when they seemingly don’t have to. Of course, I’m talking about the office sector here which has been facing the perfect storm lately. With peak uncertainty regarding interest rates, work from home, and their ability to refinance near-term debt maturities, many office REITs are making the decision of cutting their dividends to preserve liquidity, despite already having low payout ratios.

I see most of these cuts as justified and good in the long term, especially since the market isn’t really giving these companies any credit for paying such high dividends. But that doesn’t make these REITs investable at the moment.

Today I highlight 3 REITs that are at risk of cutting their dividend over the rest of this year.

Brandywine Realty Trust (BDN)

BDN is a relatively small office REIT focused heavily on the Philadelphia market with about a 20% minority of their portfolio located in Austin, Texas.

The company owns a mix of brand-new, well-located Class-A buildings, but it also has some Class-B properties that struggle to attract tenants.

BDN’s offices are pretty traditional with the majority of tenants in sectors where work-from-home (WFH*) has become the norm. This includes businesses such as legal services, finance, insurance, and banking.

Life Sciences, which have been getting a lot of attention for their resilience to WFH, currently only account for 4% of the portfolio, though management is pushing to increase this to 20% over the next 5 years.

Brandywine Realty Trust

BDN has been punished harder than most by the market, likely due to its smaller size and concentration risk in Philadelphia.

As a result, its price has plummeted and the stock now yields a staggering 18%, despite a reasonable payout ratio of 66%. This makes BDN one of the highest-yielding REITs at the moment.

Data by YCharts

Operational performance over the last couple of quarters has been relatively good. The REIT maintains an occupancy of around 90%, with Philadelphia CBD leading at 96% and Austin struggling a bit at 83%, as it is now seeing increased competition due to the highest levels of new supply ever.

But leasing is slowing down as the REIT has now seen two consecutive quarters of significantly negative net absorption and only very modest new lease rent increases of 4% YoY.

And with ongoing quarterly lease expirations of 250,000 sqft or more and a low tenant retention, the occupancy is likely to come under pressure over the next couple of quarters.

Brandywine Realty

Here’s the problem.

In order to attract tenants to their properties to maintain a reasonable level of occupancy, BDN will have to do one of two things. Either, it will have to offer cheaper rents or it will need to offer additional incentives such as longer rent-free periods or increased fit-out contributions. Both will be very costly.

In addition to this, the company might also have to incur additional CAPEX for their suburban Class-B properties to try to attract tenants and keep the existing ones.

Whether BDN will succeed in maintaining its occupancy is unknown, but additional leasing incentives will inevitably hurt the company’s liquidity. Combined with an upcoming 2024 unsecured debt maturity of $350 Million, which will be difficult and costly to refinance, and a number of projects under construction, which will require additional capital, the company is now clearly in a position where it needs to retain as much cash as possible.

Since the market isn’t giving the stock any credit for its 18% dividend yield, management might as well cut it to preserve some liquidity, reinvest in its properties, and reduce their high leverage of 7.4x adjusted EBITDA.

I see a dividend cut for Brandywine as highly likely.

Granite Point Mortgage Trust (GPMT)

GPMT is a medium-sized mortgage REIT (mREIT) with a portfolio of $3.6 Billion worth of senior loans provided to various real estate projects in the US. The company has a heavy office exposure of 41%, followed by multifamily at 31% and hotels and retail both at around 10%.

Granite Point Mortgage Trust

Its stock price has plummeted over the past 18 months and the stock now trades at a steep discount to its book value and yields 15%, despite a first 20% dividend cut already taking place at the end of Q3 2022.

Data by YCharts

Evaluating mREITs can be tricky because they are significantly discounted on the one hand, but they also suffer significant risks on the other.

Granite Point trades at a discount primarily because of three factors:

- High interest rates, which act as a double-edged sword for any mREIT. They allow the company to charge higher interest on the entirely floating-rate portfolio, but at the same time, it significantly increases the probability of default as borrowers may not be able to make the increased payments or may simply decide to hand over the keys to property if its valuation drops below the loan balance.

- High office exposure increases the probability of defaults even further as office values have taken a significant hit in recent years and are facing the worst market sentiment ever.

- High leverage of 2.7x amplifies potential losses to shareholders.

Management knows that defaults might be coming, which is why they have been building up their CECL reserve from just $37 Million last year to $133 Million this year, but the reserve still only covers 3.8% of the total portfolio.

That is not very much when you consider that last quarter the mREIT already faced one default of a $114 Million loan on a retail property.

And even excluding the provisions for credit losses, Granite Point isn’t generating nearly enough in distributable earnings to cover the dividend. Over the past 12 months, the company paid dividends of $0.90 per share, while it only generated $0.43 per share in distributable earnings. That’s hardly sustainable.

Granite Point Mortgage Trust

While the dividend has been confirmed for Q2 2023 at $0.20 per share, the company is clearly in a situation where it should preserve liquidity to prepare for further defaults and since the market is effectively pricing in a further dividend cut, management might as well go ahead and do it.

I see a dividend cut for Granite Point Mortgage Trust as likely.

SL Green Realty Corp. (SLG)

SL Green is the biggest office landlord in New York City. The company’s footprint in Manhattan is unmatched as it has been directly involved in over 200 properties in this affluent market and to this day, it still owns some of the most recognized buildings such as One Vanderbilt Avenue.

SL Green Realty

SL Green Realty Corp

The bulk of SLG’s portfolio is Class-A office buildings and the company has been investing heavily to ensure that their buildings stay up to date. This, of course, requires them to spend a lot of additional capital and/or take-on more debt in hopes of attracting or retaining more tenants.

The office sector has been facing pretty severe headwinds recently and unfortunately for SLG, these have been amplified in NYC because the city has also been experiencing an outflow of people and jobs since Covid. What this means is that the battle to maintain occupancy is not about to get easier anytime soon.

In the meantime, the stock price has taken a significant hit and currently yields almost 14%, despite a small 13% dividend cut already taking place in Q3 2022.

Data by YCharts

Some argue that SLG is already trading at a significant discount to NAV and that it is now a good buying opportunity. I’m not entirely against this view, but it’s obvious that the company will need a lot of liquidity (1) to provide above-standard incentives to tenants and (2) to de-leverage its balance sheet which has a very high net debt / EBITDAre of 13x.

Despite the worst market sentiment since the Great Financial Crisis, the board recently confirmed the June monthly dividend of $0.27 per share, suggesting no further cuts.

The dividend seems well covered by FFO, but facing significant CAPEX, I prefer to look at AFFO and it paints a very different picture.

The full year 2023 AFFO is expected at $3.16 per share which is below the current annualized dividend of $3.25 per share, which would indicate that another dividend cut is highly likely.

Conclusion

The recent market selloff has created many buying opportunities in the REIT sector, but not all REITs are worth buying. Quite a few REITs are at high risk of cutting their dividend in the near future and this could lead to further downside.

It is more important than ever to sort out the good from the bad apples when investing in REITs.

DISCLAIMER: Jussi Askola is not a Registered Investment Advisor or Financial Planner. The information in his articles and his comments on SeekingAlpha.com or elsewhere is provided for information purposes only. Do your own research or seek the advice of a qualified professional. You are responsible for your own investment decisions. High Yield Landlord is managed by Leonberg Capital.

Show more

Show More

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Prediction: Apple Will Win NBA Rights. Here’s Why It Could Be a Game Changer

By Jeremy Bowman – Jun 24, 2023 at 8:00AM

KEY POINTS

- After launching Vision Pro earlier this month, Apple needs to give it attractive content.

- NBA rights are coming up for bid in 2025, and Apple could be an ideal bidder.

- With a billion-plus fans globally, the NBA could boost both Vision Pro and Apple TV+.

The iPhone maker now has a big incentive to land a major sports deal.

For years, tech companies have unsuccessfully tried to make headsets the next big thing. Ever since the launch of Google Glass, the concept of augmented reality and virtual reality was to have been just around the corner, but multiple attempts, including Meta‘s series of Quest devices, have failed to capture the mainstream.

Apple‘s (AAPL -0.76%) Vision Pro, which the tech giant launched at its Worldwide Developers Conference earlier this month, seems like the best attempt yet to convert the masses to headset computing. Unlike previous iterations such as the Meta Quest, the Vision Pro headset can be transparent, allowing users to make eye contact with those around them. It also seems better designed for augmented reality, meaning it enhances existing reality with on-screen features.

However, the question that has dogged past headsets remains a challenge for Apple. How will consumers use the device, and will they be convinced that its value is worth the $3,500 price tag? Here’s one possibility.

Apple referred to the new device as “magical” several times in the launch presentation. The bulk of the introduction focused on applications for work and entertainment, such as FaceTime, looking at photos and videos, gaming, and video entertainment, like movies.

Now that the Vision Pro has been unveiled, the next challenge for Apple is to stuff it with content and applications that will make it a must-use device. In order to do that, it will rely on developers, much in the way it has with the iPhone. It even included Walt Disney CEO Bob Iger in the launch, who promised that Disney+ would be included on the Vision Pro from day one.

Apple teased the value of sports several times in its presentation, both in gaming and watching live. The tech giant has also been rumored to be preparing a bid for rights to air NBA games when they come up in 2025.

IMAGE SOURCE: APPLE.

Why the NBA would be a great fit for Apple

Apple is among the expected bidders for NBA rights, and it’s easy to see why. With its launch of Apple TV+ in 2019, the iPhone maker made it clear that it saw value in adding a streaming service to its portfolio.

The company has also experimented with sports, adding free major league baseball games to its service, among other offerings. Live sports have continued to be an attractive draw to both viewers and advertisers at a time when streaming content, like TV shows and movies, has exploded.

Acquiring rights to air NBA games could be the blockbuster piece of content that Apple needs to jump-start sales of the Vision Pro. The company could reimagine the sports-watching experience with its spatial computing device, potentially giving viewers the ability to see unique camera angles, get instant updates on stats and players, and even watch the game with a friend on FaceTime.

The NBA would also make an attractive partner for Apple. Both are massive global brands. Apple now has an installed base of more than 2 billion devices, while the NBA has an estimated 1.5 billion-2 billion fans around the world.

Basketball is the world’s most popular sport after soccer, but unlike soccer, the NBA has no real competition from other basketball leagues. The NBA has become global as both its fan base and many of its top players, including stars Nikola Jokic, Joel Embiid, and Giannis Antetokounmpo, come from outside the U.S. This global reach makes the NBA a great fit for Apple, and a deal could give a boost to both the Vision Pro and Apple TV+.

The iPhone maker also has more money to throw at the league than any other potential bidder with approximately $165 billion in cash and investments on its balance sheet and annual net profits that now hover around $100 billion. Apple’s relationship with Disney, which owns ESPN, could also provide an outlet for it to host NBA games on the new spatial computing device if it’s unable to secure its own rights to the league.

Now, with the launch of the Vision Pro, Apple has an added incentive to obtain the broadcast rights. Doing so could help it sell devices, not just subscriptions. Apple doesn’t need the NBA for the Vision Pro to be a success, but it’s the kind of move that could help attract attention and build demand for the product. Don’t be surprised if Apple makes a big play for the NBA as 2025 comes around.